Since the capacity market was authorised to re-start last October, following its suspension, there have been three auctions: a T-3 auction for the delivery year 2022/23, replacing the missed T-4 auction, a T-1 auction for 2020/21 and a T-4 auction for 2023/24.

Capacity market re-started with a T-3 auction for 2022/23

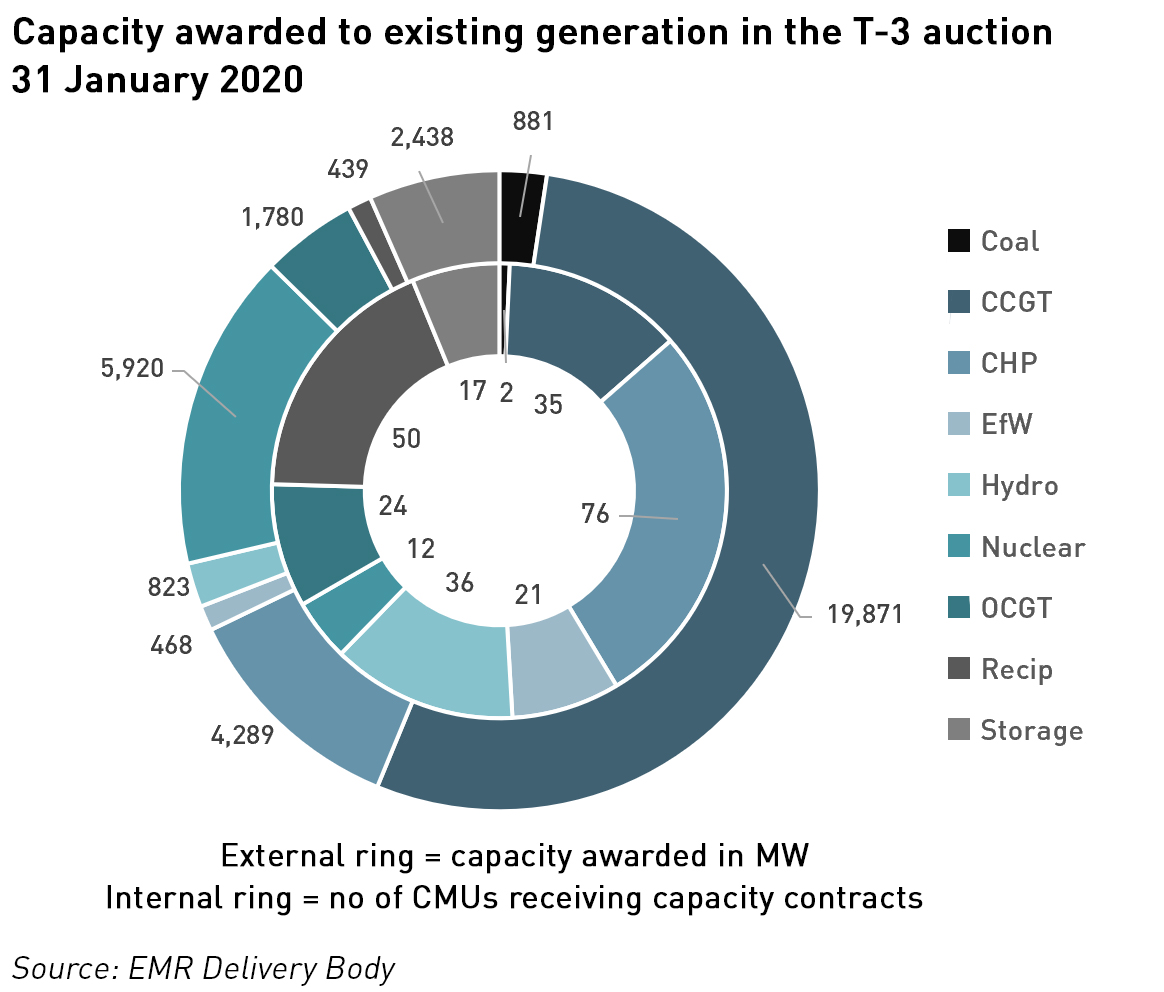

The T-3 auction concluded on 31 January, with just over 45 GW of capacity being procured, at a price of £6.44 /kW per year, a new low for the long-term auctions. Unsurprisingly, such a low price was not enough for new plant, with just 319 MW of contracts going to newbuild, split between reciprocating engines (150 MW), energy from waste (122 MW), storage (27 MW), onshore wind (15 MW) and combined heat and power (6 MW). The planned T-4 auction or 2023/24 in early March meant project developers could choose to hold off in the hope of higher prices in the later auction, a strategy that ultimately paid off.

As usual, CCGTs dominated, with existing CCGTs being awarded just under 20 GW of the 45 GW procured in the auction. Nuclear also did well with 13% of the contracts, while interconnectors also secured 13% of contracts, split between newbuild (6%) and existing assets (7%). Existing CHP secured just under 10% of the awarded capacity. No other asset class secured more than 4% of the total contracts.

Some existing large plant failed to secure contracts including all of the West Burton A and Drax units and 2 of the Ratcliffe units (1 & 4), increasing likely exit of coal before the October 2024 deadline, although 2 units at Ratcliffe did secure agreements. I will be writing about the future of coal on the system in another post shortly.

Some older gas plant also failed to secure agreements, making their future increasingly uncertain – some may decide to refurbish in order to improve their competitiveness, while others face closure. Hinkley Point B was the only nuclear unit to fail in the auction – Hunterston B had opted out before the auction. Ffestiniog Unit 4 also failed to secure an agreement.

Another notable feature of the T-3 auction was the inclusion of onshore wind for the first time. Of the 8 projects to enter, 5 were successful: Crookedstane (25 MW), Inverclyde (24 MW), Glen Kyllachy (50 MW), Beinn an Tuirc 3 (50 MW) and Halsary (29 MW). Due to the intermittency of wind power, the de-rating is very high, with de-rated capacity at only 8.2% of the nameplate capacity. The result is that the collective value of these contracts across the 15 years available to new-build is only £1.4 million.

Prices collapsed in the February top-up auction

The year-ahead (T-1) capacity auction for delivery next winter (2020/21) took place on 7 February, and with 1,024 MW of capacity being contracted at a price of just £1.00 /kW – the second lowest price to date after the delayed T-1 auction for winter season that just ended, which cleared at £0.77 /kW last June.

The auction was significantly oversubscribed, with more than 3 GW of de-rated capacity bidding against a target of just 300 MW. The 724 MW of excess capacity arose because the marginal unit in the auction was the 820 MW NemoLink interconnector – in such cases a net welfare algorithm is used to determine whether to accept a marginal unit and exceed the target or reject the unit and fall below. The algorithm subtracts the additional cost of procuring the marginal unit from the welfare gained by procuring it – if the result is positive and the welfare gained by procuring the additional unit outweighs the cost, the unit is included, and the clearing price is set to the exit bid price of that unit.

Unusually for a capacity auction, new-build capacity outstripped existing capacity, excluding the interconnector, with 76 MW of contracts being awarded to gas reciprocating engines (59 MW), energy from waste (15 MW) and CHP (2 MW). The 42 MW of contracts awarded to existing capacity were distributed between CHP (19 MW), energy from wate (13 MW), gas recips (7 MW) and short duration storage (4 MW).

However, significantly more existing capacity than newbuild participated in the auction, pushing prices down.

“Almost all the capacity was already operational, which indicates that an existing plant is willing to take low prices as an additional revenue stream rather than nothing at all. With such a low price, it raises the question of whether running these T-1 auctions for relatively low capacity is beneficial,”

– Ed Reed head of training, Cornwall Insight

DSR also performed well with 18 MW proven DSR and 68 MW unproven DSR. Anesco dominated the latter class, once again entering battery storage behind the meter.

The T-4 auction on 6 March saw a strong price recovery

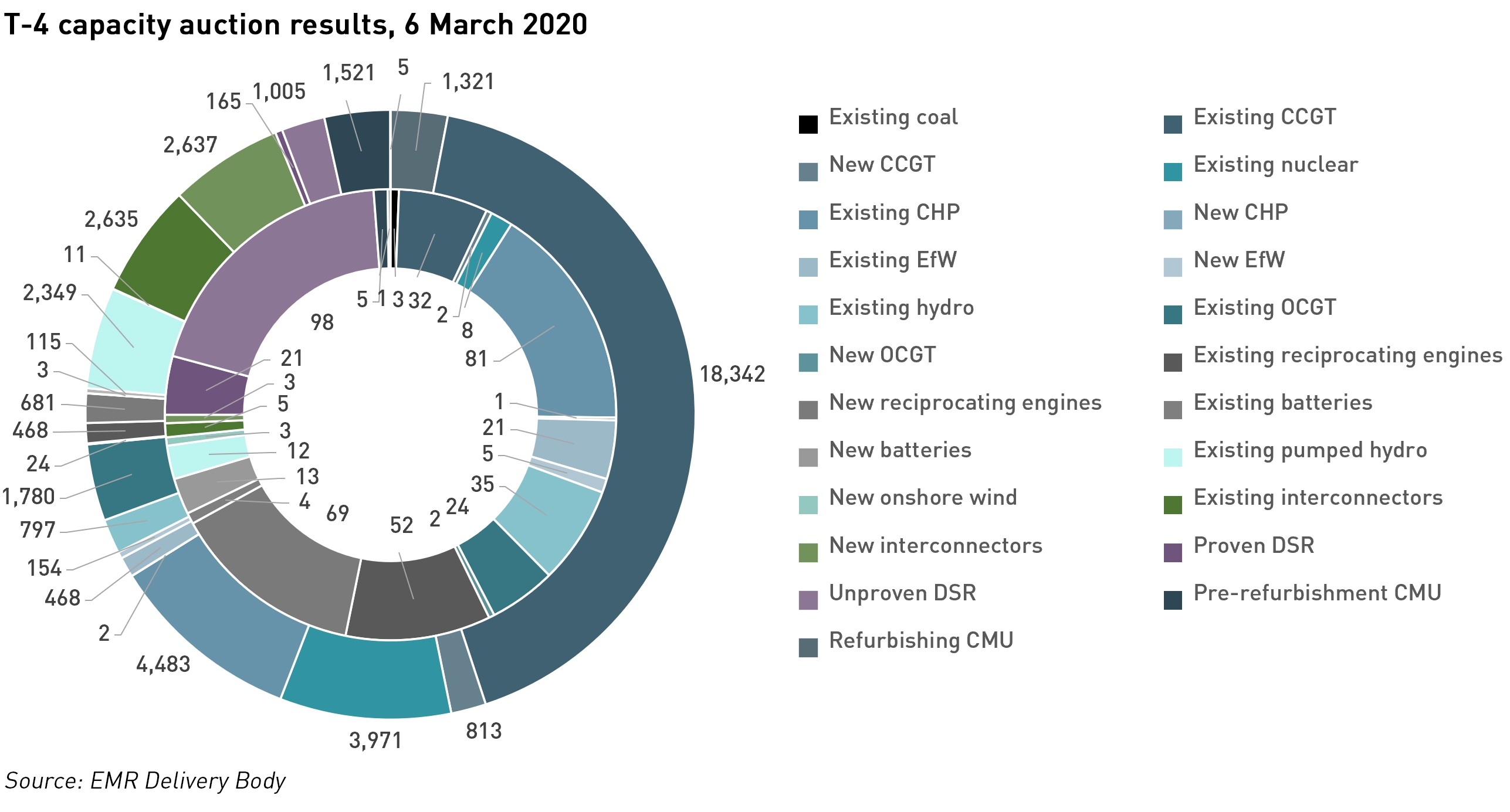

The final capacity auction taking place in Q1 2020 was the T-4 auction for the delivery year 2023/24, in which just under 44 GW of capacity was secured at a price of £15.97 /kW/y – almost 2.5x higher than the price of the T-3 auction held in January, and reversing the trend of falling long-term auction prices. The last T-4 auction in February 2018 cleared at £8.40 /kW/y.

The price was high enough to secure meaningful new-build capacity with 1.8 GW of contracts going to new plant including the 813 MW Keadby CCGT although this was already committed and so not genuinely incentivised by the auction. 715 MW of new gas peaking plants were successful, mostly gas engines.

2.7 GW of coal exited leaving only units 1, 2 & 4 of Ratcliffe in the capacity market. The share of nuclear power also fell, dropping from 13% in the T-3 auction to just 9%, with just under 4 GW being secured. Heysham 1 and Hartlepool exited. 3 GW of existing gas plants also exited including large CCGTS (Keadby, Medway, Baglan Bay, Sutton Bridge and Severn).

The share of unproved DSR jumped from 0.9% (410 MW) to 2.3% (1,005 MW), with batteries continuing to exploit the ability to register as DSR to avoid the penal storage de-rating factors. 115 MW of new batteries have secured contracts in the battery category, however a further 206 MW of new-build battery storage was unsuccessful indicating that despite the higher clearing price, it was still too low for many projects .

Interconnectors also did well, with new and existing interconnector categories each securing 2.6 GW of contracts, meaning that overall interconnectors will provide 12% of capacity during a scarcity event.

Capacity market prices likely to continue at higher levels in future

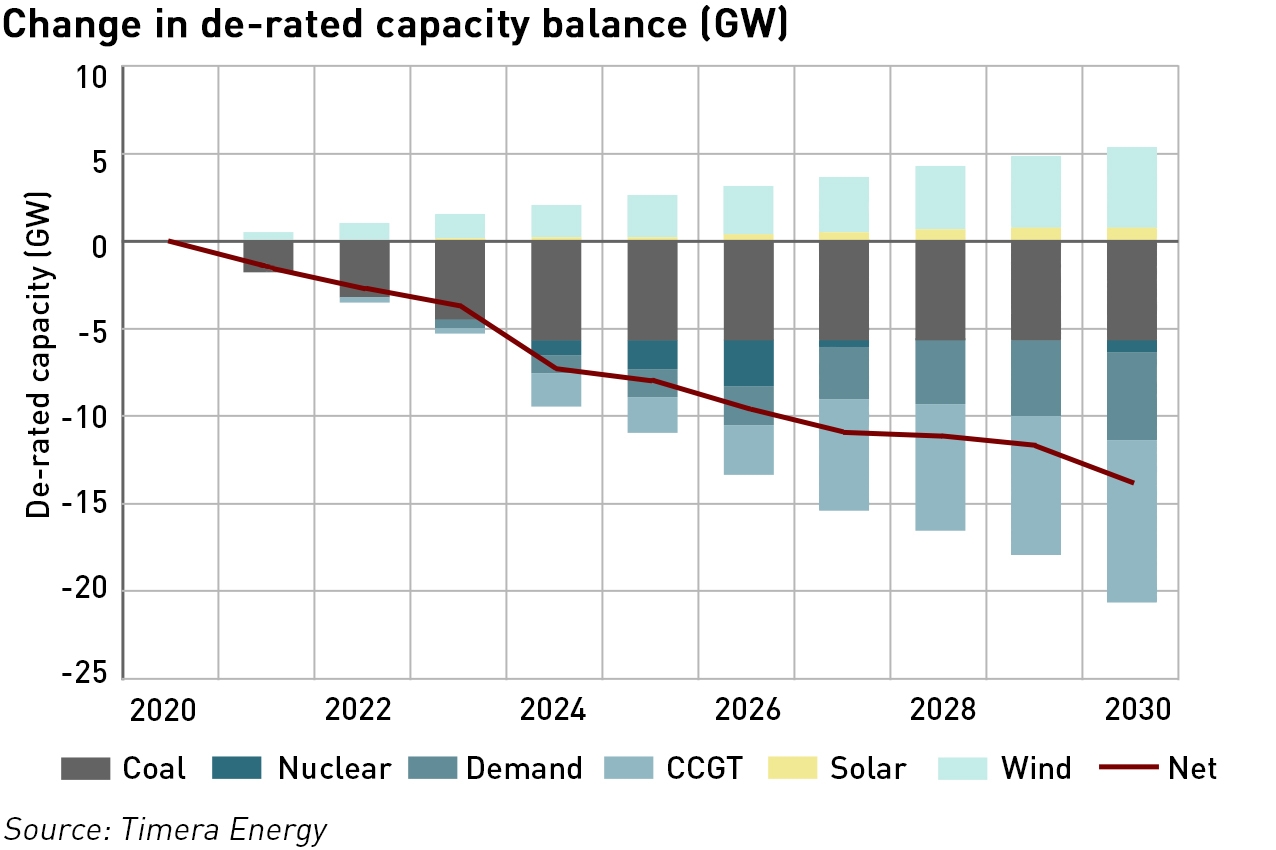

Analysis from Timera Energy suggests that the long-term auctions this year reflect a shift in the UK capacity balance with coal being largely driven out of the market in favour of new interconnector projects.

“The primary price driver in the T-3 auction was the exit bids of existing capacity. That changed in the T-4 auction, where marginal pricing was dominated by the bids required to deliver new capacity. Expect much more of that to come,”

– Timera Energy

The chart below shows why capacity market clearing prices are likely to be more in line with the recent T-4 in future ie, out-turning in the £15-25 /kW range:

Despite the huge investment in new wind and solar build, the intermittency of these technologies means they attract significant levels of de-rating, meaning that on a de-rated basis, this capacity is substantially outweighed by the scheduled closures of coal and nuclear plant and the expected end-of-life closures of some CCGTs. Between now and October 2024, at least 10 GW of de-rated flexible coal, nuclear and gas-fired capacity will close, to be replaced with intermittent wind and solar, interconnectors, storage, DSR and gas peakers.

The red line illustrates the rising capacity deficit expected in the GB market across the next decade, which will need to be met by new capacity.

Cornwall Insight analysis supports the idea of higher capacity prices in future long-term auctions, but does not think they will reach the £30 /kW levels needed to bring forward new CCGT investments, although new peaking capacity could be seen. However, it sees other market mechanisms such as National Grid ESOs new balancing services as being more important drivers of new capacity, which would probably tend towards smaller plant than large CCGTs.

A growing reliance on interconnectors is a cause for concern

The success of interconnectors is still somewhat controversial since they do not represent either additional generation or demand reduction – the simply provide access to other European markets, with an assumption that a scarcity event in the GB market would not be reflected in the interconnected markets, and that electricity would flow inwards as needed.

Interconnector flows are determined by the price differentials between the interconnected markets, and the de-rating methodology assumes that electricity in GB will be more expensive than in its neighbours, however, where markets are highly weather correlated, high GB demand can be outstripped by that in France. As interconnector capacity grows, the GB market is increasingly used as a transit market for flows into France, which sees demand accelerate quickly in winter where the higher levels of electric heating cause demand to ramp quickly in cold weather, and in the summer, when hot weather can reduce nuclear capacity due to difficulties with cooling as river water warms.

Historically, the de-rating methodology considered the highest 50% peak demand periods during the winter quarter over the previous 7 years. The problem with this is that most of those periods would not be stress events…as I have described previously, in the periods of highest GB demand, the interconnector with France has tended to be exporting rather than importing, even though on normally the flows are in the opposite direction.

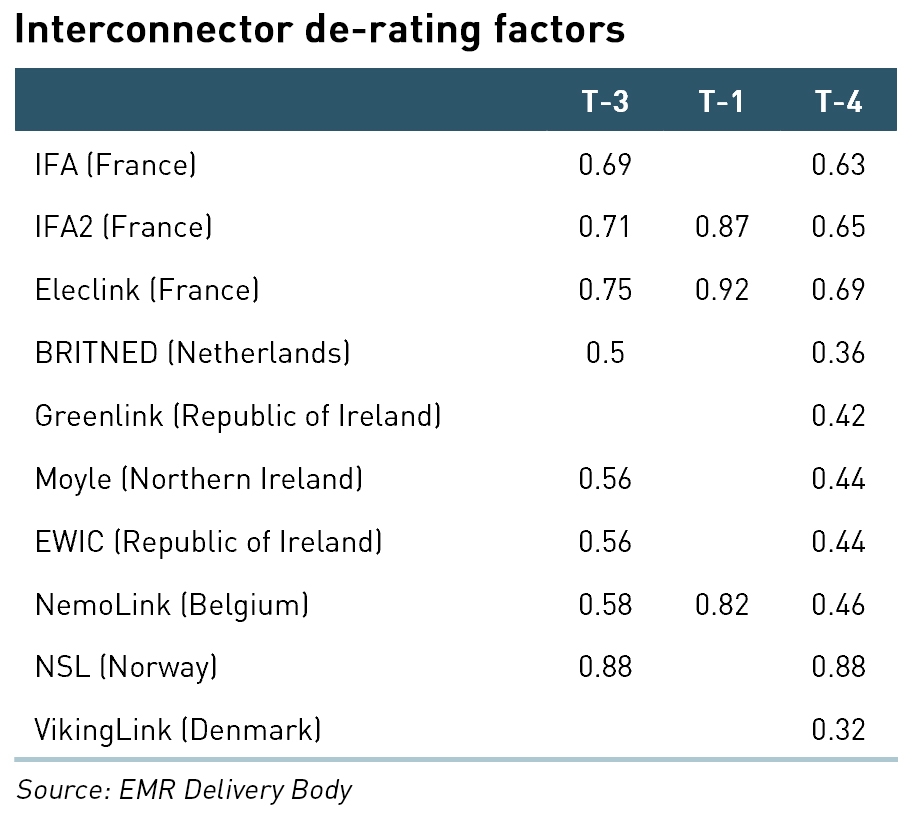

Some shortcomings in the methodology were recently addressed, but despite a significant reduction in their de-rating factors, the share of contracts awarded to interconnectors fell only marginally (from 13% to 12%) between the T-3 and T-4 auctions.

This success is indicative of the competitive advantage given to interconnection by the cap and floor mechanism and other EU directives insulating interconnectors from network charges, however, the inclusion of interconnectors was driven by the original state aid approval for the capacity market which required that non-domestic capacity must be able to participate. Back in 2014, this was considered too difficult to do directly as day-ahead market coupling was relatively new, so interconnectors were allowed to participate as a proxy for cross-border capacity.

When the state aid approval for the capacity market was re-stated by the European Commission on 24 October 2019, it was noted that the Government had committed to implementing a number of improvements to the market design to ensure the continued compatibility of the scheme with state aid rules in the future. One of these commitments relates to the direct participation of cross-border capacity in capacity auctions.

Although day-ahead market coupling is now more established, it would still be complex to accommodate non-domestic capacity in the market – BEIS has indicated that this will be the subject of a call for evidence, and requires the common methodologies which are currently under development by the European Network of Transmission System Operators for Electricity (ENTSO-E) to be delivered. It is likely that the consultations around this will highlight the deficiencies in the market coupling regime, where some TSOs have been seen to withhold interconnector capacity from the market to manage internal congestion and/or reduce their exposure to re-dispatch payments despite this being prohibited under EU law.

Other challenges include how to measure available interconnector capacity, how to ensure capacity providers are only providing capacity in one market, and how delivery will be measured when meters are located in foreign jurisdictions.

Given these difficulties, it is possible that the Government will see Brexit as an opportunity to step away from this commitment, although it does seem to be firmly convinced that interconnectors provide a positive contribution to security of supply. With interconnectors accounting to around an eighth of committed capacity in the market, this is a bet that has the potential to go horribly wrong.

Battery storage providers are gaming the system

Another area of controversy is around the behaviour of some battery storage providers in this year’s capacity auctions. The T-3 auction saw the inclusion of over 100 MW of batteries in the DSR category – by locating behind the meter, these batteries were able to achieve the DSR de-rating factor of 86% while in front of the meter short duration batteries are de-rated at between 10% and 20%.

Anesco secured the second-largest share of DSR capacity agreements with 72 MW split across 6 utility-scale batteries, while Eelpower secured just under 35 MW of DSR capacity agreements split across 3 assets. Anesco the dominated the DSR agreements awarded in the T-1 top-up auction the following week, securing more than 65 MW of 68 MW awarded to the asset class. It also secured a similar amount of contracts in the T-4 auction.

In response, Ofgem has said that “more thought” is needed on how DSR units can incorporate limited duration technologies when participating in capacity auctions.

The possibility that storage assets could by-pass the low de-rating factors for batteries was first raised by ScottishPower in March 2018, which proposed the creation of a separate Storage DSR class to which appropriate de-rating factors could be applied. The following month, Ofgem committed to consulting on the potential de-rating of storage-led DSR capacity contracts, possibly in 2019, however, when the consultation failed to materialise, there was nothing to prevent batteries from registering as DSR assets in this year’s auctions.

The government is now consulting on rule changes to the Capacity Market which could effectively shut this loophole. The consultation, launched in February, makes specific mention of standalone storage units entering the capacity market as DSR as an unintended consequence of existing regulations.

“Standalone storage units entered into the CM as Unproven DSR create security of supply risks because the CMU’s contribution to security of supply is overestimated and therefore, we will have less capacity than expected to call upon during a system stress event. Whilst we believe this practice is limited at present, as it is difficult to finance new build storage on the basis of only one year of CM revenues, once Unproven DSR can access multi-year agreements this may lead to the problem becoming more widespread,”

– Capacity Market Consultation On Future Improvements

BEIS has proposed an amendment to the description of DSR in the capacity market legislation that would clarify that the baseline of imported electricity below which metered volumes are reduced cannot be primarily comprised of electricity used to charge a battery. The consultation closed in early March and the responses are being considered.

Wider capacity market consultation

In addition to seeking views on preventing batteries from entering the capacity market in the DSR asset class, the Government’s consultation seeks opinions on a number of other proposals:

- To allow all technologies except interconnectors (ie including DSR) to access multi-year agreements if they can meet the relevant capex threshold. Currently DSR is not deemed to have the higher capital costs that would make 3 or 15-year agreements necessary to support investment decisions, however, BEIS recognises that this situation is changing;

- To widen access to the market by reducing the minimum capacity threshold from 2 MW to 1 MW, which will ensure alignment with other markets and allow operators to stack revenues from these other markets with capacity contracts;

- To create a legislative obligation to procure in the T-1 auctions at least 50% of the capacity reserved as part of the parameter setting process for the T-4 auctions, regardless of subsequent adjustments to the projected capacity needs; and to set the methodology by which the minimum capacity to be set aside is determined. This would enshrine current practice in law;

- To allow any new capacity type which can effectively contribute to addressing the generation adequacy problem to be incorporated into the market as soon as it is able to make such a contribution. This also incorporates existing practice into legislation and ensure there are no delays in future;

- To establish a reporting and verification mechanism for carbon emission limits to support the implementation of emission limits in the capacity market;

- To remove the exclusion of plants with long-term STOR contracts from the capacity market. When the capacity market was first introduced in 2014 the payment of capacity revenues to units that also held long-term STOR contracts was expected to yield windfall profits, which would contravene state aid rules. Subsequent changes to market conditions have removed the likelihood of such windfall profits so it is no longer necessary to exclude these units;

- To add additional information to future Capacity Market Registers to help reduce the risk of fraud and error.

There are also a number of minor corrections and clarifications being proposed. It is unclear when the outcome of the consultation will be known, given the current covid-19 crisis and the focus of the Government being (rightly) elsewhere.

The higher prices seen may still be too low to bring forward new CCGTs

Despite the higher price of the T-4 auction, it was still too low to bring in new CCGTs other than one plant that was to be built anyway. This is because projects with lower capital costs such as OCGTs and reciprocating engines can out-bid CCGTs in the auction, and interconnectors are able to accept lower prices due to the benefits of their cap and floor revenue mechanisms.

With electricity demand likely to increase with at least some of the de-carbonisation of heating and transport being delivered through electrification, it is not at all clear that the capacity deficit identified by Timera Energy could be met without building some new large capacity.

Given the current difficulties with new nuclear projects (EDF remains notionally committed to Sizewell C but as Hinkley Point C barely secured board approval and given the wider problems EDF continues to have in delivering its new EPRs, this is by no means a certainty), it is likely that some new CCGTS will be needed to make up the capacity gap. It will be interesting to see whether Brexit sees the Government directly subsidise new gas plant, or whether it will continue to reply on the market to deliver the necessary price signals, despite its almost total failure to do so to date.

Either way, project developers continue to be faced with significant uncertainties as the capacity market rules are likely to change again following the current consultation, while National Grid is making major changes to its balancing products and Ofgem continues to progress changes to network charging. Unpicking the impact of all of this on new projects is no small task, and larger projects with higher capital costs and therefore higher financial risks will inevitably be less likely to emerge, potentially threatening the country’s capacity margins in the middle of this decade.

Hi,

Another very interesting post, although honestly it’s very complicated!

Sorry to ask a simple question but could CHP currently installed in buildings behind the meter take part in the capacity auction and what would be the de-rating assuming ‘normal usage factors’?