Almost out of the blue, last week, while all attention was on Brexit, came a decision from the General Court of the European Union that has led to the suspension of the GB Capacity Market. This means that all capacity payments are on hold, as are all future auctions.

The case before the Court was a legal challenge brought by Tempus Energy in December 2014 against the treatment of demand-side response (“DSR”) in the Capacity Market. Unlike generators which could secure 15-year contracts for new capacity, DSR provers could only achieve one-year contracts. The Court was asked to decide whether the European Commission had given sufficient consideration to the treatment of different types of capacity when granting state aid clearance to the scheme.

“This ruling should ultimately force the UK Government to design an energy system that reduces bills by incentivising and empowering customers to use electricity in the most cost-effective way – while maximising the use of climate-friendly renewables,”

– Sara Bell, CEO Tempus Energy

The Court concluded that in reaching its decision the Commission did not complete sufficient research and examination of the impacts of the Capacity Market on the operation of the internal energy market, and that the Commission could not have established whether there was any doubt about the impact on the operation of the internal market without conducting its own investigation, which it failed to do.

“We are extremely disappointed by today’s General Court judgment as the Capacity Market has proven that it can successfully deliver security of supply at the lowest cost to consumers,”

– Lawrence Slade, CEO Energy UK

What does this judgment mean for the UK capacity market?

The judgment suspends the state aid approval for, and therefore the legality of granting aid through, the capacity market. The Government has announced the scheme will now enter a “standstill period” which prevents it from holding any capacity auctions, making any capacity payments under existing agreements, or undertaking any other action which could be seen as granting state aid, until the scheme can be approved again.

“We are disappointed with this judgment but it poses no issues for our security of supply. As a responsible Government, we have prepared for all outcomes, and we will be working closely with the Commission so that the Capacity Market can be reinstated as soon as possible,”

– BEIS

The second of twelve monthly payments for the 2018-19 year was made the day before the ruling – as the payments relate to the underlying demand for electricity, holders of capacity contracts will have received less than half of their expected annual revenue. Guidance from National Grid has also raised the prospect of previously paid capacity payments being clawed back by the Government, although it hopes to avoid this. The share prices of all listed companies participating in the Capacity Market fell sharply.

BEIS is reviewing the judgment, including its implications for capacity providers, and will provide guidance to the market as soon as possible as to whether holders of capacity contracts must comply with their obligations during the standstill period and whether failure to do so would result in penalty payments or termination fees. A determination also needs to be made in relation to the retail price cap, and whether the capacity market component will be removed from the cap calculations.

It is also unclear what may happen in relation to previous auctions. The European Commission must review the Capacity Market arrangements, and if it determines that unacceptable discrimination between technologies exists, decisions will need to be made in relation to previous auctions, which would then been deemed to be invalid. Re-running those auctions would be difficult, but possibly unavoidable.

One of the few elements of good news for capacity holders is that all credit cover currently held in relation to the postponed auctions will be returned, and agreement holders may also request the return of credit cover for capacity agreements arising from past auctions.

The Government has responded that it is “doing everything [it] can to re-obtain state aid approval from the Commission as soon as possible”, however, the Commission will now need to undertake a formal investigation before providing state aid approval for the Capacity Market, which may take some time. BEIS is intending to seek separate state aid approval from the Commission to run a one-off replacement T-1 Auction, with the postponed T-4 hopefully being run as a T-3 auction in next year’s auction round, if approval has been granted for the scheme by then.

The industry response to the ruling has been largely negative, with generators expecting to see significant negative earnings implications.

“The consequences are absolutely huge. Immediate cessation of payments is going to have immediate consequences for electricity generators that were relying on them…. The lights are not going to go out. We certainly have enough power stations. But the consequence is the market price might go up,”

– Ed Reed, head of research, Cornwall Insight.

Limited impact in the short term, although it’s unclear what would happen in a scarcity event

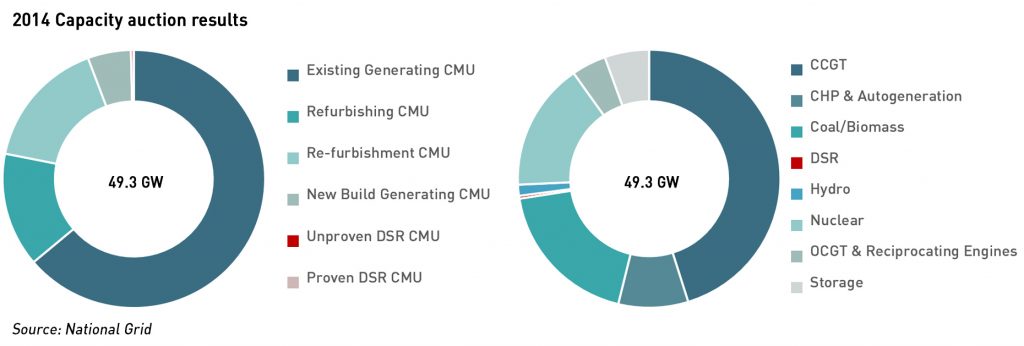

Since its inception, the Capacity Market has paid out more than £580 million to GB generators with an additional £4.1 billion of payments contracted, £1 billion of which remains to be paid for winter 2018 /19.

Most of the capacity in the current delivery period is was secured in the first T-4 auction in 2014, to which a capacity price of £20.8 kW currently applies (the £19.4 /kW clearing price adjusted for inflation). The impact of the suspension of these payments varies significantly by asset, due to differences in de-rating factors and contract length. It also depends on corporate factors such as the extent to which the profit margins of the asset depend on capacity payments, and the amount of debt associated with the asset.

This means that assets that rely on capacity payments in order to remain cashflow positive and/or to meet debt repayments will be most exposed to their suspension. Older, less efficient thermal assets will obviously be vulnerable, but also newer, projects that are still paying back project finance, which ironically could include DSR schemes.

Winter is generally the most profitable period for power stations, so it is unlikely that any will close or be mothballed in the near term despite the loss of capacity payments, even where their loss makes a project cash-flow negative, since higher winter prices provide the opportunity for losses to be mitigated.

The impact on wholesale prices this winter is therefore likely to be muted, not least because if there were opportunities for generators to change their market behaviour to increase earnings, they would have been doing that prior to the Court’s ruling.

In addition, National Grid has indicated that the system has sufficient capacity for the winter, so prices are unlikely to spike in the Balancing Market unless a combination of colder than expected weather and plant outages strikes.

“In the short term, i.e. this winter, system impact is likely to be minimal…. Profit impact for recipients of CM revenue will be painful, but the more important question at system level is whether it changes behaviour… Even for plant that depends on the CM payment for its survival such as low merit thermal, I would not expect the removal to cause it to temporarily cease generating, mothball or close immediately,”

– Ben Irons, director, Habitat Energy

Questions remain however as to what would happen if a capacity shortage did occur over the coming winter, and whether capacity market contract holders would still deliver on their commitments without any certainty of being paid. Units that participate in the Balancing Mechanism could access the market that way and secure the high prices that would be seen in a tight market, however many capacity contract holders are not Balancing Mechanism Units and cannot directly access this market.

Alternatively, National Grid might call upon older mechanisms such as the Strategic Balancing Reserve, and while this was expensive and inefficient, it might be necessary to secure reserve capacity over the winter.

Longer-term impact harder to predict, although investor confidence will be hit

Security of supply will certainly be at risk if the Capacity Market is out of operation for an extended period or abandoned altogether, and the spring could start to see older plant shutting down and new build projects being shelved. According to Aurora Energy, the removal of capacity payments will threaten the economic feasibility of 6.4 GW of contracted new–build assets and could precipitate the closure of up to 15.3 GW of existing assets by 2022.

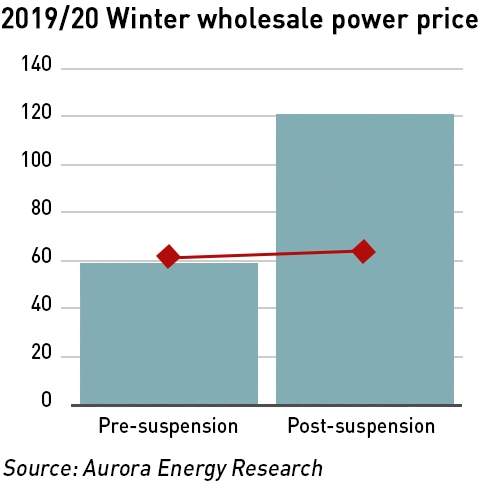

The resulting reduction in capacity would see both prices and volatility rise – Aurora has suggested that wholesale prices could double to around £120 /MWh next winter without the Capacity Market in place – winter 2019/20 prices rose by £1.4 /MWh within 24 hours of the ruling. Aurora has suggested that if capacity payments are not re-instated and 15 GW of capacity fails to deliver in winter 2019/20, wholesale prices would go as high as £121 /MWh due to a rise in scarcity levels and generators relying more on energy revenues to recover their costs.

The Government needs to work quickly to provide clarity on the implications of the suspension of the capacity market to current capacity holders, as well as determining the steps needed to re-gain state aid consent. This may require a re-design of the market that may bring in some of the new features, such as the inclusion of renewables, that had already been under consideration as part of the 5-year review.

However, this would be a significant undertaking, complicated by Brexit, meaning an interim solution is likely to be needed to ensure there is not a capacity crunch next winter if the spring sees a spate of plant closures.

The impact on the share prices of listed companies involved in the capacity market illustrates the affect of the issue on investors, who are already frustrated by the overall high levels of uncertainty in the GB energy market, with major changes such as the retail price cap and embedded benefit reforms having appeared almost overnight in the context of long-term investment horizons.

Uncertainty around the future of the capacity market will certainly have an impact on future investment opportunities, with marginal projects less likely to go ahead, and investors may well want higher returns to compensate for the wider risks they see as growing in the sector. This will increase the cost of capital for GB energy assets, and lead to higher bills for consumers.

Some commentators believe this is a fuss over nothing and that the market will be restored relatively quickly. Others are not so sure, particularly as the 5-year review was likely to bring further changes and these may well be incorporated into any re-design required for the re-instatement of state aid approval.

Among the likely changes are adjustments to de-rating factors, including for DSR, so while the decision of the General Court might appear to be positive for DSR, it may be a Pyrrhic victory if de-rating factors are adversely adjusted.

The curved ball here is Brexit – in the event of a “no-deal” Brexit, the General Court ruling will not be binding on the UK, and the Government will be free to continue with the Capacity Market in its current form.

Thank you for this review of the possible impacts of this court ruling. The statements of ‘those in charge’ that this winter 2018/2019 should not see any significant problems is a relief; I was expecting to see some increase in risks to supply.

So I can assume that the upturn in demand and in the use of coal in the last few days is to be expected due the cooler weather arriving and that we are currently suppling more energy to France.

I’ve just had a quick look at the Gridwatch data for the past couple of months and see we’ve been ramping coal production at the same time as exporting to France.

We’re definitely going to rely on coal for security of supply this winter, but it’s interesting to see us increasing coal use to support exports. It’s not exactly in line with the exiting coal / using interconnectors for security of supply and to bring in renewable energy from elsewhere narrative…