Today the Government has announced a new consultation to promote energy security (yet to be published) as part of its ongoing Review of Electricity Market Arrangements (“REMA”). Two main elements are being highlighted – a desire for more gas-fired generation to provide a backup for renewables in the absence of bulk seasonal electricity storage, and a move towards locational power pricing, in an effort to try to persuade generation and demand to co-locate.

While the first is a good idea, the second is not.

Why we need more large-scale gas-fired generation capacity…

I have written many times about the growing risks to energy security as this decade progresses. Increasing demand from electrification will coincide with the closure of the last remaining coal plant (Ratcliffe, 2 GW) and the last four Advanced Gas Cooled Nuclear Reactors (4.7 GW). In addition, the futures of Drax (4 GW) and Lynemouth (0.4 GW) biomass plants is uncertain after 2027 when their subsidies expire. 10 GW of firm, non-intermittent generating capacity could leave the grid before the end of the decade.

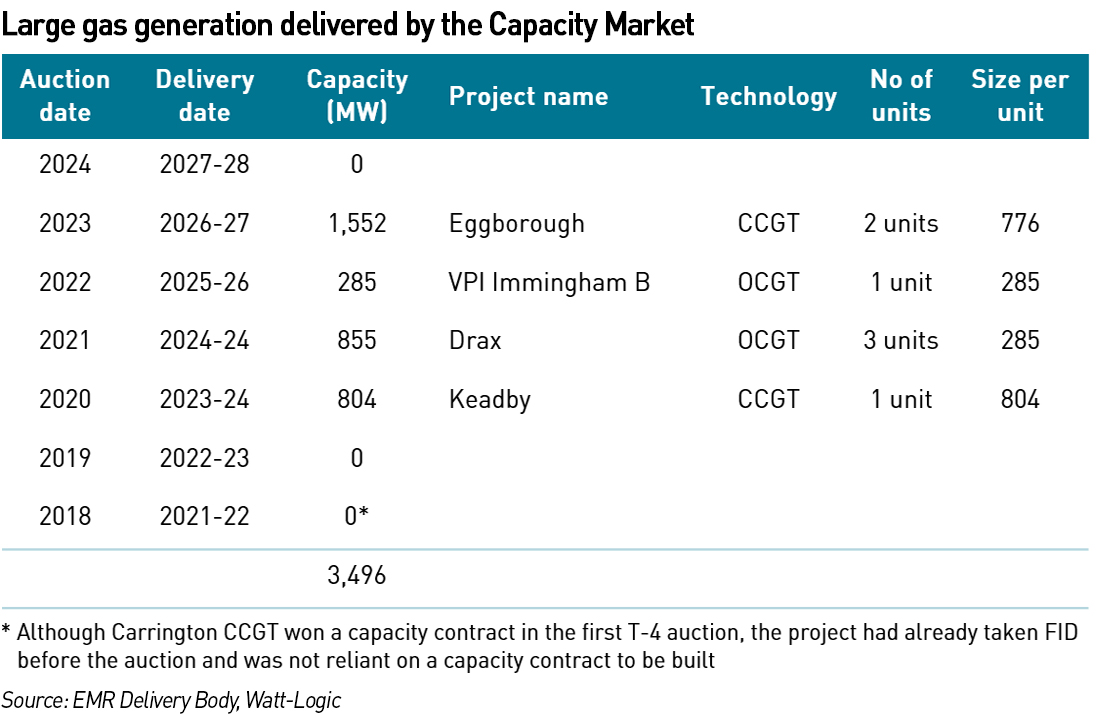

And it’s simply not being replaced at the necessary rate to ensure energy security – the Capacity Market which was designed to enable new large-scale combined-cycle gas power stations to enter the market has almost completely failed to deliver. Since the first long-dated capacity auction in 2018 only 3.5 GW new large-scale gas-fired plant has been awarded contracts, however in addition to the 10 GW of potentially retiring capacity between now and 2030, since 2018 13.5 GW of conventional capacity has already closed, including 3 GW nuclear (Dungeness, Hinkley Point B, Hunterston B) and 10.5 GW coal (Aberthaw, Cottam, Drax, Eggborough, Fiddler’s Ferry, and West Burton A). Of the new large-scale gas plant that has secured capacity contracts, one third is open rather combined cycle technology, which has higher carbon emissions.

In other words, since the first long-term capacity auctions, 10.5 GW of conventional capacity has closed, another 10 GW may close by 2030, making a total of 20.5 GW, with only 3.5 GW large-scale gas generation being delivered by the Capacity Market over this timeframe (and a further 840 MW of CCGT at Carrington which took FID before the first capacity auction, so while it has been built in this timeframe, it was not secured by the capacity contract it was later awarded).

It is pretty clear that the amount of firm, dispatchable generation that has closed and is likely to close up to 2030 is far greater than the amount of new firm, dispatchable capacity that has been secured to replace it, and this creates a potentially un-manageable risk to security of supply.

“There are no two ways about it. Without gas backing up renewables, we face the genuine prospect of blackouts. Other countries in recent years have been so threatened by supply constraints that they have been forced back to coal. There are no easy solutions in energy, only trade-offs. If countries are forced to choose between clean energy and keeping citizens safe and warm, believe me they’ll choose to keep the lights on. We will not let ourselves be put in that position. And so, as we continue to move towards clean energy, we must be realistic,”

– UK Government press release

That the Government wanted more gas-fired generation has never been a secret – back in 2016, there had been talk of an additional 26 GW by 2030 (per the 2012 Gas Generation Strategy). It’s just not been a focus in recent years. But today the Government is reminding us that gas generation is still a necessary bridging technology, that without it, blackouts are a real risk towards the end of the decade, and that it is one of the very few sources of generation that can be delivered quickly with a build time of just two years.

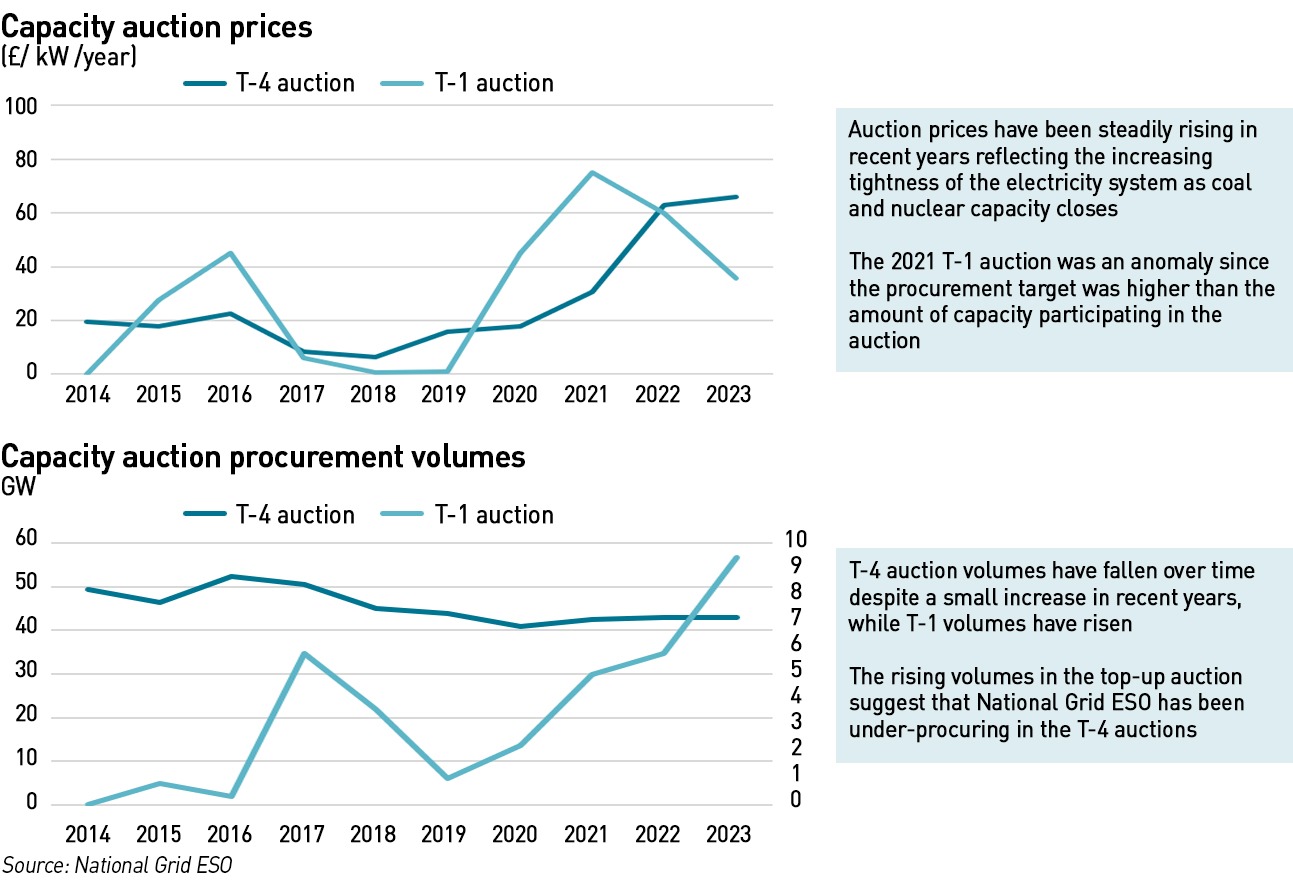

Last year, an unabated CCGT, the 1.5 GW Eggborough Power Station, won a 15-year contract meaning it would run past the 2035 date on which the GB power system is intended to be met zero. There was much angst about this. But the reality is that CCGT + CCS is currently unproven. Also, long-term capacity auction prices have been rising – this year’s auction was the highest priced yet. Any new gas generation being built from now on is likely to attract a cost premium due to the uncertainty over emissions rules and running hours once the 2035 deadline is reached.

…and why we do not need locational pricing

On the other hand, a move to locational or zonal pricing is not a good idea. The proposal appears to be to allow renewable generators to charge consumers more for locating closer to them, and that this will potentially save them money over time (“the reforms could save households £45 off their yearly energy bill” according to the press release). I think the chances of savings actually emerging are small, but in the near term, consumers would not only pay more, but they could be forced to live alongside ugly infrastructure they have time and again rejected in public consultations. People do not appear to want to live close to windfarms in particular, so the idea that they will be forced to not only have these machines close to their homes, they will have to pay extra for the privilege is unlikely to go down well with the public.

Not only is this likely to be unpopular among consumers, it’s unclear whether developers will be keen either. Developers have typically sought to build where their generation will be optimised ie in windy or sunny places. The south east of England is not particularly windy, it is densely populated, and there are many more people liable to object to developments being close to their homes. That means the development process is likely to be more of a headache, and since costs are already rising (and are likely to continue to rise) due to supply chain inflation, adding yet more cost is going to make life difficult.

So far consumers have bought into the narrative that renewables are cheap, but there must be limits to how far they can be misled over this – at some point they will notice that bills have risen significantly since we began the push for renewables, and that this is true in most countries that have developed intermittent renewables, and in particular wind power, at scale. People may wonder why, if the wind is free, not only are windfarms subsidised, but that subsidies are increasing. They may wonder why, if renewables are so cheap, they will be asked to pay more in their bills to have them built close to their homes. At some point they will realise that the intermittent renewables emperor has no clothes.

The arguments against locational pricing are well rehearsed and I have set them out in the past (they don’t avoid grid constraints because demand and generation don’t tend to co-locate, and they reduce liquidity by fragmenting the market). There is no good alternative to building new grid infrastructure – more transmission capacity will reduce curtailment and enable all generation to be delivered to demand centres. Trying to move the generation or demand is unlikely to be inefficient in a world where electricity costs are not necessarily the main drivers of business location. For example, datacentres require good telecom connectivity and the ability to hire staff – these are both more important than electricity costs when choices over location are made. Companies will respond to price signals, but people working in energy regulation tend to forget that energy price signals may not be the strongest price signals faced by businesses.

.

We will see what the outcome of this new consultation will be, but it should come as no surprise that the Government is renewing its push for more gas generation to support energy security. However, people would be forgiven for cynicism – consultations take time, which the current Government simply does not have since by law a General Election must be held before the end of January next year. That means it will be difficult to complete this consultation, digest the results, decide on a course of action and implement the necessary statutory or regulatory changes before Parliament is dissolved. We will have to keep our fingers crossed that action on energy security is not unduly delayed and that risks to security of supply are mitigated in a timely fashion.

.

UPDATE

The Second REMA Consultation can be found here. Responses are due by midnight on 7 May 2024.

The technical research supporting the consultation is quite extensive and can be found here.

Ay last is appears the penny has dropped

It is and has been obvious that we need gas CCGT not only as just ‘back up, for when the wind isn’t blowing as it is often said but as balancing and provision of inertia, reactive power etc. and in sufficient quantlty. Very much more than the 3.5 Gigawatt quoted.

I think the government are clutching at straws adding the wasteful and very expensive carbon dioxide capture to such plants just to keep their charade of net zero going. I’m surprised there has not been more adverse comment about Drax’s plans for it and the price tag estimated at close to what Hinkley Point is going to cost. The comparison is beyond ridiculous.

Drax is a pipedream – the idea that you would retrofit CCS onto such an old plant is more than a little bit nuts.

From what I understand, the current consultation proposal is just for more gas and not necessarily abated or hydrogen-ready plant, which is fine. The Government has already been thinking about whether 15 year capacity contracts could be suspended to allow abatement/h2 to be retrofitted down the line – but that would clearly have to be on terms acceptable to the contract holder. Whatever else we may criticise the Government for, failure to honour contracts isn’t something the market worries about. My feeling is this new gas will be expensive but there’s no getting away from that if you’re going to apply implicit or explicit carbon charging to fossil generation (the implicit being all the potential new rules on abatement etc)

Our country requires a coherent energy strategy for the 21st century. A overarching government body should take control of this which is supported by all parties. A change of government should not be allowed to impact the work or the actions that need to be taken. Politicising energy is a serious mistake as is allowing private enterprise to drive strategy. The gov should retain a 51% controlling interest at all times. A x party group needs to get a grip of this completely.

As you rightly say there is a need to keep the lights on. If experts call for more gas in the medium term, fine. The direction of travel though is important. My assumption is that when gas and oil production cannot meet demand, it’s either conflict or enacting the clean energy alternatives in a controlled way. I really do think that we will just have to get used to energy production being reasonably close to where we live if it’s cheaper and more efficient to do. How fond are we now of Battersea Power Station. Certainly, ofshore wind farms near me are well tolerated and do look quite well matched to the environment. When we do eventually move away from gas, I would like to think that Hydrogen storage in the depleted North Sea gas fields is feasible, not for piping into homes, but to burn and fuel conventional steam turbines. Is anybody close to trialling this?

Do we need to keep mentioning solar as part of the mix? If we have wind/nuclear and gas/Hydrogen enough for winter, what is the value of solar.

In these discussions, I have a strong view of how homes will be heated. A mix of heat pumps and off peak thermal storage – this because the wind blows at night.

We’d be much less fond of Battersea power station if it was still belching coal dust and other nasty stuff from its stacks!

I disagree that we have to compromise our living standards to facilitate the energy transition, and think that trying to force that on people will make the entire project fail. I don’t believe people are willing to accept their lives being worse as well as more expensive, particularly when there are perfectly acceptable alternatives – build more power lines. Also build more nuclear and focus less on intermittent generation. When you look at the raw material requirements for intermittent renewables, the ethics of them look pretty questionable, so let’s look at sustainability more holistically, and what is good for the wellbeing of both consumer and those living close to the mines etc necessary for delivering transition materials.

Solar has no value in a discussion about energy security, which is what this is, because the sun sets before the periods of peak energy demand – the winter evening peak is after dusk so solar makes no contribution.

Well of course the climate activists have immediately complained saying the Government should invest in renewables.

But just what renewables? They already know that renewables are intermittent, so if they invest in more, they’ll need to provide yet more base load.

Perhaps the activists should also look closely at the horrific conditions at some Chinese Solar panel producing plants.

Can anyone explain to me how we can cope with simply wind, solar and hydro which by definition are intermittent since no wind = no energy and no sun etc. etc. The greens seem to just say more investment in renewables! If there’s no wind them it doesn’t matter how many wind turbines you have, there’s no energy generated. Burning wood pellets is unsustainable and battery storage for now anyway looks prohibitive. Unless a miracle happens with fusion we need more nuclear stations and fast as we are closing/decommissioning them at an alarming rate. Much as I dislike this government it seems they are right in at least making the case that we desperately need more gas turbines.

Exactly – it’s not possible to balance the GB grid without gas as it stands. Some storage technologies may emerge eventually, but we have blackout risks between 2025-2035 – assuming thoese technologies, emerge, are commercialised and built in that timeframe is not credible. More CCGTs is like home insurance – we neither want nor expect our homes top burn down but we buy the insurance just in case.

At least govt have had moved the narrative into the reality of trying to get to net zero but mainstream TV media ive watched today have all managed to find an environmental zealot to condemn what is being done. Oh and they will be the same environmentalists who say more wind is the answer but no to the pylons and until the grid is reinforced we are pissing in the wind (pun intended) adding more wind as its being constrained off in increasing volumes. So where is the fix to ameliorate the current planning obstacles in all this – nowhere because apparently REMAs location pricing won’t need it!!

The real issue that remains, despite Kathryns work here, and others, is that journalists still don’t challenge the truth (there bloomin job) here over the real costs and risks of net zero and until they do we aren’t going to move the dial. A major blackout may jolt people into action but id say the ESO are pretty adept at managing the system and have the tools and our money to manage it for a few years yet. Also I doubt Labour will stand full square behind this with Miliband there so suspect it will be waisted six to nine months and they will want to recalibrate it and make it more green and as a result even worse.

Kathryn,

Thank you for producing your many good Blogs.

Surely there is something wrong with the Government’s thinking of replacing good Domestic Gas Boilers with Heat Pumps when the electricity is produced by gas? There is a place for both, which I have. Sounds like the “Dash for Gas” years ago which emptied the North Sea.

We need large gas powered generators because they are the only thing which can follow the vagaries of Wind & Solar generation, good though they are.

To have a national system which only produces power when the Sun is up & blowing Wind is surely in someone’s imagination.

We need a proven nuclear system – not EPRs.

96% of energy storage world wide is from pumped storage hydropower. Our most successful energy project was Dinorwig. There are 9 pumped storage projects that have had planning permission granted with 8 in Scotland and 0ne in South Wales. One at Glenmuchlock is a deep opencast pit filling with water that will require a bunded reservoir above that does not dam a stream. They are waiting for a cap-and-floor system of remuneration to attract investment similar to that that has opened up investment on transmission. In addition, there are a further 8 similar pits in the South Wales coalfield that can be put to this use as well as a further 12 similar deep quarries in Wales and England. Some countries are developing deep mines into PSH and heat projects that could heat homes, factories and greenhouses to provide winter vegetables. These projects would have multipurpose use by also providing additional water storage during summers and in addition to high level water for forest fire fighting. They will provide skilled and semi-skilled jobs in some of the most depressed areas of the country as well as reducing the UK’s carbon footprint. Building gas turbines that are only 40% efficient or turning gas into hydrogen with CO2 sequestration are plans by the oil companies to continue stoking the global warming that spells disaster to people in hot climates and guarantees climate change refugees arriving on our coasts.

I do not know what pricing models would support ling term energy storage.

And , indeed, the government seems confused as to what is Long Term Storage – and if it is only for electricity.

One government call, questioning if a cap and floor financing is required, casts Long as being 4 hours (such as Dinworig) or above. Whilst others (such as RAe) talk about interseason storage.

I suspect that some intermediate storage, capable of dealing with Dunkelflaute, of say 100 to 200 hours – as periods adjacent to the calm might regenerate the storage – but will depend upon the amount of overcapacity of wind.

But the Grid operator and OFGEM seem not to have any idea of the value or amount needed of such storage.

I liked the idea that Siemens-Gamesa had for using stranded (decommissioned) thermal generation assets (coal or gas fired – though nuclear too) and then using cheap thermal storage (~£5/kWh); this would obviously be better if used for gas turbine based generators, with their high thermodynamic efficiency).

So one could view gas-generation as part of a “no regrets” policy – and old nuclear too!

In principle such storage could be downsized for domestic application, (though I am not sure of availability of appropriate electricity generation equipment) but industrial applications and uses of such heat or waste heat might also have value