The rapid deployment of renewable generation, and its impact on the electricity system in terms of transmission capacity management, balancing intermittency and frequency control has triggered the need for an entirely new suite of flexibility products. At the same time, the opportunities to earn income streams from the need to manage these constraints, is also undergoing rapid change, not all of it planned.

On the one hand, Ofgem is progressing with its network charging reforms with a view to make the recovery of network costs from users more cost reflective, and removing the distorting effects of the current arrangements. These changes have been in the pipeline for some time as Ofgem has made no secret of its desire to reduce the level of market distortions seen in the current charging regime, although the proposals are deeply unpopular among flexibility providers.

On the other hand, the situation for market participants has been significantly disrupted by the decision by the European General Court last December that the GB Capacity Market state aid approval was flawed leading to a suspension of the market and the removal, for the time being at least, of a major income stream for many market participants (not just providers of flexibility).

The future of flexibility markets

There have been suggestions that proposed network charging reforms will destroy the market for flexibility however this seems unlikely given the fundamental need for flexibility has not diminished. National Grid currently spends around £1 billion per year on balancing the electricity system, a figure that has been steadily growing since 2010, and is set to continue to rise. National Grid, alongside the Distribution Network Operators (who are evolving into Distribution System Operators (“DSOs”) is in the process of upgrading the suite of flexibility products it procures.

“The power system is rapidly evolving towards a decarbonised, decentralised and digitalised future… Over the period to 2030 we expect balancing and ancillary power markets to double in size to around £2 billion per year –opening up opportunities for flexible generators and storage to access new revenue streams,”

– Richard Howard, Research Director, Aurora Energy Research

A 2018 report by Aurora Energy Research last year predicted that the GB power market transition will create a £6 billion flexibility market by 2030, with around 13 GW of new flexible and distributed generation capacity being commissioned, including gas reciprocating engines and batteries. The report forecast that balancing and ancillary power markets will double by 2030 to around £2 billion per year, largely due to the roll-out of further renewable energy generators.

A 2016 study by the Carbon Trust and Imperial College London estimated the benefits of a smart energy system to be £17-40 billion to 2050, while a 2015 analysis for the Committee on Climate Change estimated £2.9 billion per annum in gross benefits of flexibility by 2030.

In its Forward Plan for 2019-21, National Grid set out its ambitions for all market participants of 1 MW and above to have equal access to all its ancillary service markets and the Balancing Mechanism through a single integrated platform by 2023. The design of these markets is intended to allow participants at all network levels, including distribution or community levels, to stack value regardless of who owns or operates those networks. By 2023, the expectation is that the wholesale electricity market will have hundreds of participants, and there will be a liquid day-ahead auction providing a strong price reference for short-term power.

The challenge for market participants is making sense of all of these changes and developing robust business models able to leverage the available opportunities despite high levels of uncertainty around exactly how those opportunities will emerge.

Revenue opportunities: frequency control

Historically, National Grid has procured frequency response through a number of routes:

- Mandatory Services: these are ancillary services which certain transmission-connected parties (typically large generators) are required to provide to help manage short-term frequency variability arising from changes in the generation mix.

- Firm Frequency Response (“FFR”): parties can enter into a Framework Agreement to provide FFR based on an asset or combination of assets. FFR has been used to secure a committed level of frequency response on a longer-term basis (1–24 months).

- Specific contracts, such as Frequency Control by Demand Management and Enhanced Frequency Response (“EFR”): used where technical or operational reasons prevented parties from participating in the other frequency markets.

Over the last couple of years National Grid has made a number of modifications to its frequency response products including the introduction of a Firm Frequency Response Bridging contract to remove barriers to entry for smaller parties, a reduction of the minimum participation size in FFR from 10 MW to 1 MW, allowing parties to stack two different FFR contracts so virtual power plants can grow, an increase in transparency through the Market Information Report, and reviewing and clarifying the testing guidance for Distributed Energy Resources (“DER”) providers.

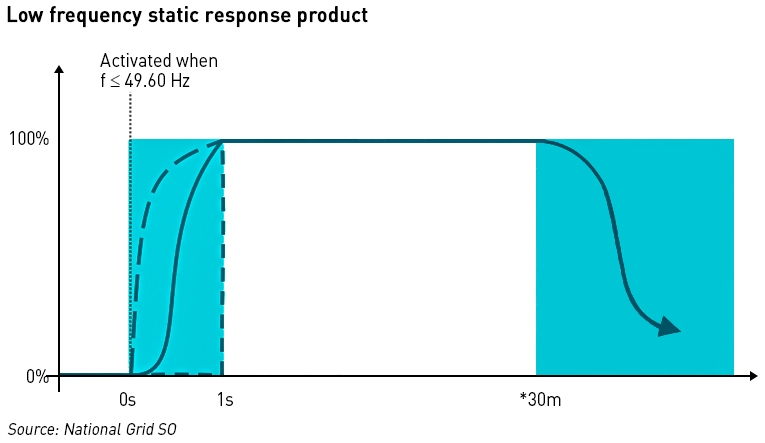

In December 2017, National Grid published a new roadmap for its frequency control and reserve markets, setting out the principles which are to govern the development of balancing services products with a view to providing greater clarity and investor certainty. Work in this area has been ongoing, and National Grid has recently launched a weekly auction trial. Phase 1 of the trial will go live across 25-26 April, and will see the procurement of 100 MW of a standardised version of the current Primary, Secondary and High Frequency Response service – the low frequency static response. Phase 2 will procure all four standardised versions of the current products – low static, high static, low dynamic, high dynamic – and will begin in Summer 2019.

The auction will be held every Friday morning with results being published by early afternoon, with products auctioned by four-hourly EFA blocks over the week. The first available delivery window will start at 23:00 on the same day. This will facilitate access to the market by technology types such as wind and DSR which are less forecastable.

The low frequency static response product will have service activation at 49.60 Hz, and a full response requirement within 1 second, with a 30 minute duration (unless advised that it is lower, before that week’s auction).

The weekly auction trial will create an opportunity for new technologies such as wind and solar to access the frequency response market. Alignment of procurement activities closer to real-time would also allow all market participants to assess which revenue streams offer them greatest value.

The trial will last for 24 months from the end of the development phase to allowt different parameters and approaches to be tested prior to full implementation.

A number of new frequency response products is also being considered:

- Dynamic Regulation: a symmetrical service with an equal upward (low) and downward (high) response requirement. The response time will be lower than for other products but providers will be required to offer a duration that allows for continuous operation.

- Dynamic Moderation: also symmetrical, with a rapid proportional response required occasionally to assist with the continuous Dynamic Regulation service.

- Dynamic Containment – High and Low: this service is not symmetrical so providers will be able to choose to provide either or both upwards (low) and downwards (high) response. Providers will need to deliver rapid proportional response for infrequent containment events.

- Static Containment – High and Low: also not symmetrical, with a requirement for providers to deliver rapid response for infrequent containment events

Revenue opportunities: reserve

Reserve is needed to ensure that imbalances arising from forecasting errors or unexpected losses on the system can be managed. It is manually instructed after automatic frequency response services have delivered, and can be either upward (an increase in generation/decrease in demand) or downward (a decrease in generation/increase in demand). Reserve is also used to describe the actions taken by National Grid to ensure that sufficient upward and downward flexibility is available.

A combination of balancing services products, the Balancing Mechanism and trading are used to provide reserve:

- Short Term Operating Reserve – provided by parties with a Framework Agreement, typically distribution and transmission connected generators. This market is accessed three times a year by National Grid as seasonal requirements change, and secures a committed level of positive reserve over a period of several months through three products (Committed, Flexible and Premium Flexible) with different levels of required firmness of availability. It is used to manage short-term supply losses, localised constraints or any other variability driven by changes in the generation and demand mix, and typically delivers from instruction in five minutes or beyond.

- Fast Reserve – National Grid locks in a committed level of positive reserve for periods of up to 23 months through a single product provided by parties with a Framework Agreement. This market is accessed monthly by National Grid and the service is used to manage short-term supply losses. It typically delivers in timescales of less than two minutes from instruction.

- Demand Turn-Up – typically aggregation of true demand and behind the meter generation delivered by parties who have a Framework Agreement. There are two products: Fixed and Flexible, which generally deliver in timescales of a few hours from instruction. The Fixed product allows National Grid to access negative reserve either for the following summer, while the Flexible product provides negative reserve for the following half-week.

- Specific contracts, such as Optional Reserve – used where there are technical or operational reasons why parties cannot participate in existing markets, or where there is currently no route to market for a specific additional service.

There was a peak in STOR utilisation for March 2018 as a result of the ‘Beast from the East’. Overall utilisation of STOR increased by 49% in 2018 compared to 2017, due to lower pricing which made STOR more economical to use against alternative actions.

However, in August 2018 National Grid reduced the operational window for STOR activation from four to two hours ahead of delivery, which has contributed to a significant reduction in the number and volume of STOR actions used to maintain headroom.

The decline in STOR utilisation may lead to STOR providers seeking to replace the lost value with higher availability fees or utilisation prices in future tender rounds.

Going forwards, National Grid will be forced to do more to balance the system with smaller participants as many traditional providers of flexibility are exiting the market. The system operator has committed to being able to balance a 100% low carbon system by 2025 – which will be impossible without the use of new smaller participants connected to the distribution networks.

Only a small number of providers (4 traditional and 3 DSF) currently participate in Fast Reserve due to the 50 MW threshold, so from 25 March this year, the entry level has been reduced to 25 MW. The greatest requirement for Fast Reserve is in the winter months, and 2018 saw an overall increase of 25% in utilisation compared with 2017.

All load response participating in the 2018 demand Turn-Up tender was accepted in 2018, although this did not include any storage, possibly due to the relatively low price for the service when compared to services more suited to the technical characteristics of storage such as frequency response. Overall, participation in the service in 2018 was lower than during 2017, with less than half of the capacity tendered in 2017 being offered in 2018; however the amount of capacity contracted was only slightly lower at 114 MW versus 139 MW in 2017.

As with other balancing services, National Grid is exploring rationalisation and simplification of its reserve products. It is also consulting on reducing or removing exclusivity clauses to enable greater participation by demand-side flexibility in the provision of these services, and hopes to expand access to both frequency and reserve to wind and solar in 2020.

Variable reserve requirements are growing, and are projected to increase over the coming years potentially doubling the 2017 requirement by 2022. A pan-European market for reserve (the Trans-European Replacement Reserve Exchange or “TERRE”) is also being developed, which will allow providers with over 1 MW capacity (individual or aggregated) to participate.

Revenue opportunities: restoration and reactive power

National Grid hopes that by the mid-2020s, it will be running a fully competitive black start procurement process with submissions from a wide range of technologies connected at different voltage levels on the network, with DSOs playing a more active role in the restoration approach. National Grid spent approximately £55 million on 18 black start contracts in 2017/18, and expects the number of individual services it will need to remain the same in the short to medium term. Contracts last between 3 and 6 years with an expected minimum annual availability of 85–90%.

As part of its reforms of balancing and ancillary services, National Grid has plans to improve the transparency around its black start services, open the service to a broader range of participants, and consider alternative approaches for procuring black start services. This includes the developing combined services, so that a potential provider no longer needs to meet all requirements by itself, but can combine with other providers, and removing barriers to entry to accommodate a wider range of technology participation focusing on interconnectors, DER, wind technologies and storage/batteries.

In January, National Grid ESO announced a new black start procurement trial which will examine the feasibility of expanding access to the service to non-traditional assets.

Reactive power (measured in Mvar) is used to control voltage levels and can be either generated if more is needed, or absorbed if there is too much in the system. When active power (MW) generation is greater than active power demand, the frequency increases. Similarly, when reactive power (Mvar) generation is greater than reactive power absorption, the voltage increases, however, unlike active power for frequency control, reactive power requirements are regional and vary significantly across the system.

Demand for active power in one region could be met by active power generation by any other region, but this is not true for reactive power where requirements need to be met locally. Management of reactive power also differs to active power in that many network assets such as transformers, overhead lines and cables are able to both generate or absorb reactive power.

When demand for active power is high, generally during winter peaks, network assets absorb reactive power. The requirement for reactive power generation has been decreasing over the past 10 years and National Grid expects this trend to continue. On the other hand, the need for reactive power absorption is greatest when demand for active power is low, and power flows through the network are also low, with network assets generating reactive power. This usually occurs overnight and during the summer. The requirement for reactive power absorption has consistently increased for the last 10 years this trend is expected to continue.

Currently, National Grid’s requirements for both generation and absorption of reactive power are met through a combination of balancing services and network asset investment. Network assets – primarily capacitors and reactors – which have historically provided the majority of baseload reactive power are very cost-effective. Balancing services are used to fill the gap when network assets are not available, something which has been increasingly necessary in recent years due to the pace and scale of changing reactive power flows – National Grid now spends over £150 million a year on these services.

National Grid procures reactive power generation and absorption through two routes, however these can only be used if the provider is running when the requirement arises:

- The Obligatory Reactive Power Service (“ORPS”) must be provided by all generators with a Mandatory Services Agreement under the Connection and use of System Code (“CUSC”). Generally, all transmission-connected power stations with a generation capacity above 50 MW must be able to provide this service. The cost of this is currently £100 million per year.

- The Enhanced Reactive Power Service (“ERPS”) is a tendered commercial service for providers who can go beyond the obligatory reactive power requirements or who do not have to offer ORPS but can meet or exceed the ORPS performance standard. National Grid has not had a contract for this service since October 2009 and has received no tenders since January 2011.

As patterns of generation and demand have changed, the availability of ORPS providers at the times when they are needed is becoming less certain. This is most frequently seen during low active power demand periods in the summer, when conventional thermal plant that provides ORPS is less likely to run, leaving some areas of the country at risk of a voltage constraint, when voltage levels go outside secure limits unless the level of reactive power is changed.

This means that National Grid must ensure that sufficient ORPS providers are available in each region at all times, which is currently done through a range of active power procurement options, often when the active power itself is not needed, at a cost of £50 million each year. The reactive power itself is then procured through ORPS. The active power arrangements used to secure ORPS providers include:

- Regional voltage constraint contracts (“Constraint Management Services”) – tendered commercial services in regions where there is a voltage constraint to synchronise ORPS providers;

- Forward energy trades under a Grid Trade Master Agreement (“GTMA”) to synchronise ORPS providers; and

- Accepting offers from participants in the Balancing Mechanism (“BM”) to synchronise ORPS providers.

As the increase in renewable and small-scale generation connected to distribution networks is coinciding with the reduction of traditional providers of reactive power services, National Grid intends to work with DSOs to optimise the use of network assets (transformers, overhead lines, cables, capacitors and reactors) at all levels of the system, with transfers of reactive power between the transmission and distribution networks.

Revenue opportunities: the Balancing Mechanism and wholesale electricity markets

The BM is a core tool used by National Grid to ensure the demand and supply are balanced on the electricity network, and typically accounts for 5-15% of all contracted electricity volumes each year at a cost of £350 million. The BM is also used to address a range of other system needs such as managing voltage levels, which can be done more efficiently through the BM than by trying to contract specific services in the timescales involved. The BM is also used to manage constraints on the transmission.

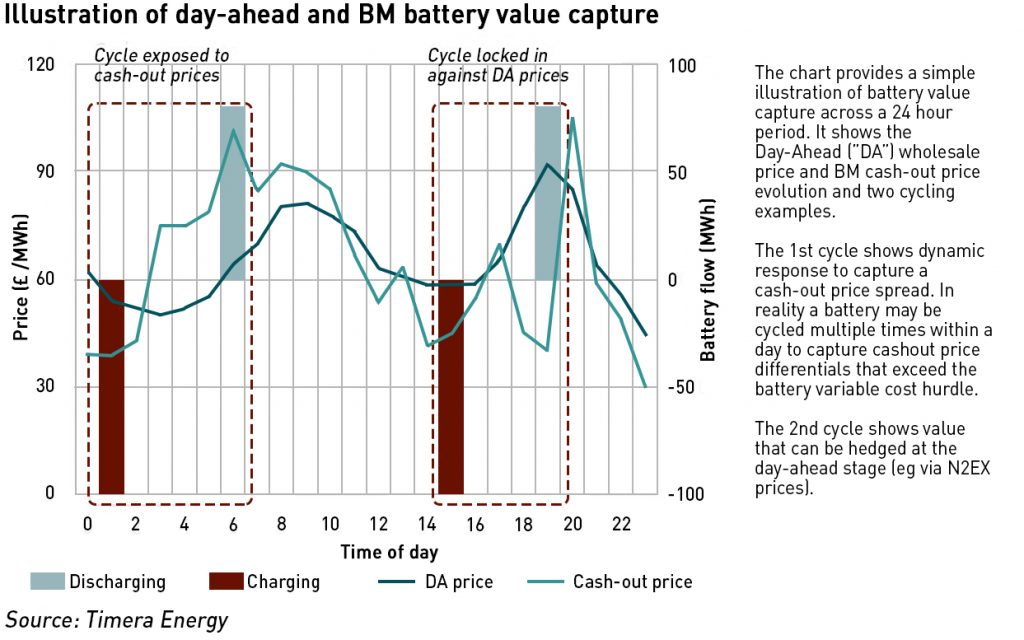

Currently, wholesale market and balancing returns typically make up more than 70% of required margin for small grid-connected providers of flexibility such as batteries, because these markets display far more volatility than the markets for ancillary services. Most of this value is currently captured by responding to forecast cash-out price differentials – also known as Net Imbalance Volume (“NIV”) chasing.

The main benefit of this strategy is it avoids the costs and complexity associated with submitting bids and offers into the BM, however the volumes of battery and gas engine capacity adopting this strategy are likely to quickly exceed total imbalance volumes, eroding available value. This would force small flexibility providers to fully participate in the BM in order to capture value.

National Grid has been working on expanding access to the Balancing Mechanism, providing access to smaller providers. Since the introduction of the first aggregated unit in August 2018, two aggregators, Limejump and Flexitricity, have been granted supply licences enabling them to participate in the BM, together offering 52 MW of power by January this year, which National Grid expected to almost treble over the first quarter of the year.

National Grid has recently introduced a distributed resource desk to enable power system engineers to instruct smaller users, and is currently investigating bulk dispatch. The desk is designed to deliver faster instructions.

At the same time, Elexon is implementing the necessary code changes to allow aggregators to access the BM without either special exemptions from certain industry code requirements, or the need for a supply licence. These changes will enable Virtual Lead Parties to accede to the Balancing & Settlements Code and allow BSC Parties and VLPs to register Secondary Balancing Mechanism Units.

Revenue opportunities: local flexibility markets

Last summer UK Power Networks (“UKPN”) indicated that it may need over 200 MW of demand-side response over the next four years in order to defer load related reinforcement, with contracts of between 1 and 4 years’ duration available. The company recently announced it had allocated £12 million of funding to buy demand-side services (possibly over the next two winters although this isn’t entirely clear) to help manage its grids in southeast and east England, and has reduced the minimum capacity threshold to 50kW in a bid to drive greater uptake.

UKPN expects that in the future it will also need to procure low voltage flexibility and demand turn-up products, and is also working with National Grid to see how demand response within its network can provide constraint management services to the transmission system.

“Local flexibility markets will play a paramount role to enable transactive energy platforms (e.g. peer-to-peer and V2G), energy storage investment and mobilise aggregate demand side response,”

– Head of Energy Innovation in Europe and Deputy Head

of Science & Innovation in the Nordics, under the auspice the UK Foreign &

Commonwealth Office and BEIS

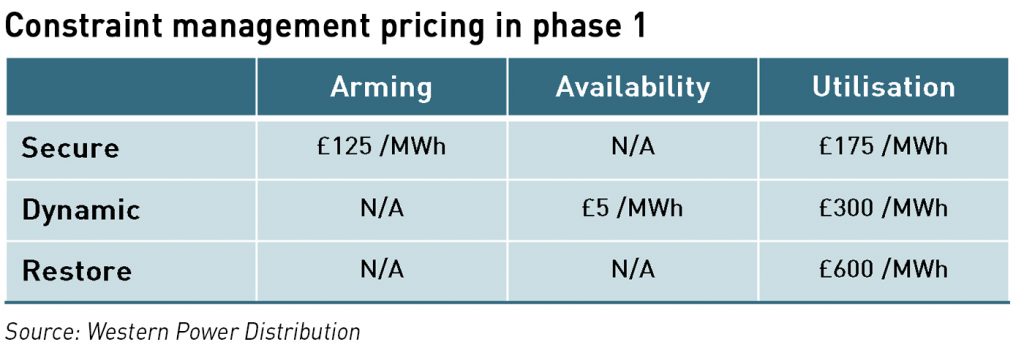

Western Power Distribution (“WPD”), has also launched a local flexibility market and has identified a need for 93.4 MW of demand response services in 2019 across three products:

- Secure (pre-fault constraint management): used to manage peak demand loading on the network and pre-emptively reduce network loading, offering a higher availability payment and lower utilisation payment;

- Dynamic (post-fault constraint management): used to support the network in the event of specific fault conditions, such as during maintenance work; offering a low availability payment and higher utilisation payment;

- Restore (restoration support): used to support power restoration following rare fault conditions. There is no availability payment, offering a premium utilisation payment instead.

1-year contracts are awarded through tenders carried out twice a year, and have the following key features: no exclusivity clauses; no obligation to provide availability; no penalties for non-delivery, only loss of revenue through underperformance clawback; shared and capped liabilities

Initially, most contracts will be awarded on a fixed price basis of £300 /MWh, but as the market develops, WPD expects to move towards a derived clearing price for the zone to be used in the contract, based on the highest price submitted by the group of lowest priced participants that can meet the full amount of system needs, including redundancy. As liquidity improves and WPD’s visibility, procurement, dispatch and settlement systems mature, it expects to shorten the length of the window to which the contract price applies, moving towards close to real-time market operation.

Scottish and Southern Energy Networks (“SSEN”) has announced plans to start procuring demand-side response services from households and communities as early as this summer. These services will extend beyond SSEN’s “Constraint Managed Zones” framework and apply across the entire network, and could range from small-scale renewables, battery storage, electric vehicles, demand side response and even energy efficiency measures that alleviate network constraints.

SSEN has indicated it expects to pay around £300 /MWh for flexibility, and will initially procure four services through the Piclo platform, with a further three to be added by the end of the year. The split between availability and utilisation payments will vary by service:

- CMZ Prevent: the traditional CMZ product that supports the management of peak demand.

- CMZ Prepare: to support the network during planned maintenance work.

- CMZ Respond: to support the network during fault conditions as a result of maintenance work.

- CMZ Restore: to support the network during faults that occur as a result of equipment failure.

There is no minimum threshold to register for the service, although one may be introduced ahead of the tenders – traditionally providers of constraint management services have been required to deliver at least 100 kW. This means that the role of aggregators is still open – SSEN has indicated its intention that providers should be able to provide the service without the need for an aggregator to intermediate, but a minimum threshold above the typical household capacity would ensure aggregators were still needed.

The scheme follows a five-year trial known as “SAVE” that involved 4,000 homes in the Solent region in which a range of delivery mechanisms was explored to see how households could provide demand reduction and response, and what changes to current market frameworks would be needed to facilitate small-scale market participation. The results of the trial are due to be published in June.

The need for local flexibility service is likely to be greater in the more densely populated south of the country, and this is reflected in the more advanced plans and larger requirements of the DSOs operating in those areas compared with network operators further to the north (for example, Northern Powergrid has only identified a need for 16 MW of flexibility services over the next four years).

What next?

The fate of the Capacity Market is still up in the air – the European Commission has appealed against the General Court’s decision, so until that plays out, the market will remain suspended. As we move into the summer, that might push older thermal plant out of the market, with owners potentially deciding to simply pay any penalties if the market ever re-starts. We have already seen this first closure announced with SSE saying it will close one of the units at its Fiddler’s Ferry coal plant, and although that in itself will have very little impact on the system due to the export constraints at the site, others may well follow suit.

National Grid will need to ensure appropriate capacity margins for next winter, and while the Government is hoping to bring forward legislation to enable a top-up capacity auction to take place in the summer, the system operator may have to fall back on old reserve products such as STOR or SBR. These are expensive, and would certainly have an adverse effect on bills, however it would provide opportunities for generators and DSR providers to fill the gap. This might appear to suit the likes of Tempus Energy whose complaint to the European General Court was behind the Capacity Market suspension if not for the fact that a lot of DSR is provided by on-site generation, much of which is thermal, and now faces restricted running due to the Medium Combustion Plant Directive (“MCPD”).

In this respect, a “no-deal” Brexit would be interesting, since GB would be free to have any sort of Capacity Market or other subsidy regime it wanted, being outside the EU state aid rules, and could also set aside the MCPD if needed (this would be counter to the Government’s de-carbonisation agenda, but a delay to permanent implementation would not be unfeasible).

It’s tempting to think that in the short-term, the winners from all of this could be mid-high efficiency CCGTs which are well positioned to participate in traditional reserve and balancing markets. Over the longer term, the new frequency and reserve markets and wider access to the Balancing Mechanism as well as access to local flexibility markets operated by DSOs should provide opportunities to support investments in DSR, storage and embedded generation, and the emergence of virtual power plants (“VPPs”) composed of aggregated distributed energy resources will provide small plant with straightforward market access opportunities.

Leave A Comment