As the country basks in a heatwave, National Grid ESO has published its early outlook for next winter (this is the third year it has issued an early outlook, and it has come out a month earlier than in the past two years). The base case spare margin has increased from 3.7 GW last winter to 4.8 GW for this winter (last year the early outlook expected the spare margin to be 4.0 GW but this was later reduced to 3.7 GW when the final outlook was published in November).

The Demand Flexibility Service (“DFS”) is going to continue because ESO believes it is “prudent” to do so, but the coal contingency may be finished – the two units at West Burton A have now closed and are being de-commissioned, the one unit at Ratcliffe has returned to normal commercial operations. The two units at Drax notionally closed at the end of March, but apparently there are ongoing discussions to retain them as a contingency for next year (something Drax itself denies saying it has already started to de-commission them). It’s possible Drax is trying to leverage its market power since the station is essential for grid stability in its region, and it would be challenging for the market to lose generating capacity of this size, but the real issue isn’t coal but its biomass subsidies which are at risk of being removed.

In any case, by law all coal power stations must close by the end of October 2024 ie will not be available next winter. It could be argued that NG ESO needs to learn to do without, although it would be better if the mandatory closure date was altered. The closure date was brought forward in 2020 when the Government said it would implement an emissions intensity limit of 450 gCO2/kWh on the use of coal for electricity generation. The Government decided not to introduce emergency powers allowing the Secretary of State to suspend or modify the coal phase-out arrangements, something which now looks to have been short sighted. An impact assessment at the time had suggested there would be no security of supply risk associated with the early closure of coal plant.

The Government announced in June 2021 that it would introduce legislation to ensure the closure of coal power stations by 1 October 2024 “at the earliest opportunity”, but I have not been able to find the relevant legislation, so cannot comment on whether it did in the end include powers for the Secretary of State to delay the coal exit, or whether new legislation would be required.

Role of interconnectors: some of last year’s threats have retreated but fundamental risks remain

As with last year’s early outlook, the main headline is that interconnectors are expected to save the day if the GB market is tight. Last year, NG ESO had to move back from that position in its final winter outlook because the situations in both France and Norway were very tight. NG ESO assured us that Norwegian supplies would be secure despite worryingly low reservoir levels, and the fact that the French demand peaks and our occur at slightly different times meant the TSOs could juggle between themselves to ensure both Britain and France could receive imports from each other when needed. I remain unconvinced by that argument.

Norway’s reservoirs are looking healthier this year – water levels in the key NO2 region are just shy of the 20-year median where last year they were close to 20-year lows.

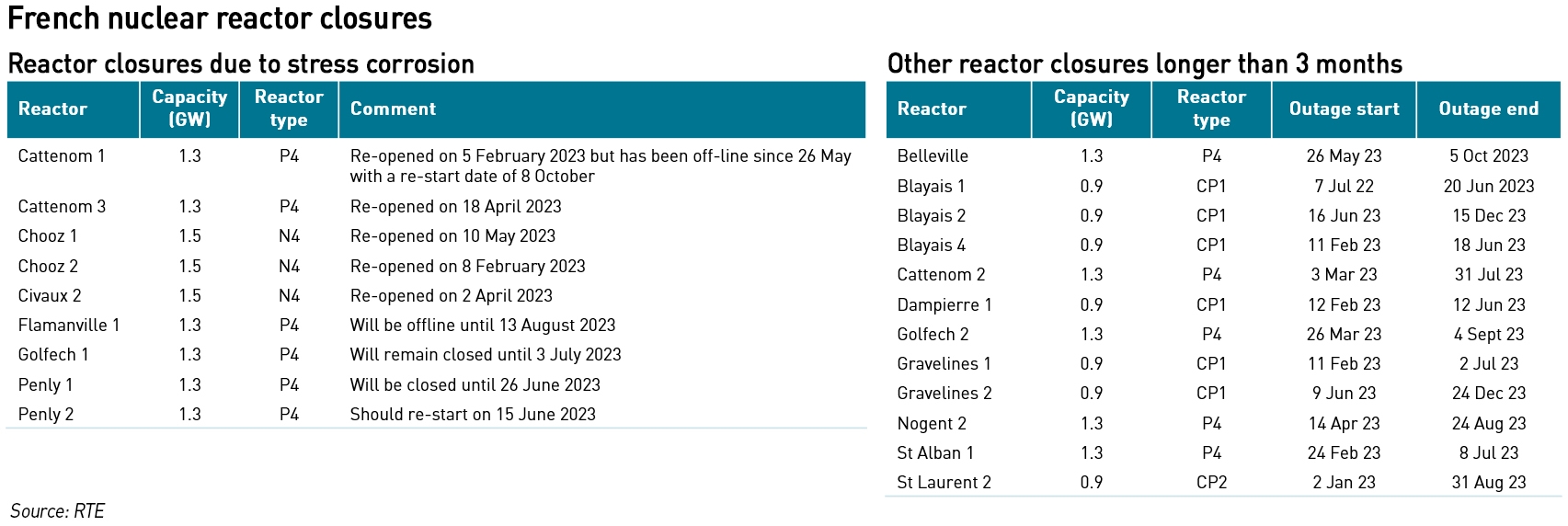

The situation in France has also eased, although it will take time to fully resolve the stress corrosion issue. While another three French reactors have opened since my last update in mid-March, and one is supposed to re-start today, three more remain off-line:

However, this is far from the end of the story. In April, French nuclear regulator, ASN approved EDF’s updated inspection and repair schedule following the additional defects discovered in March at Penly 1, Penly 2 and Cattenhom 3. EDF’s revised schedule provides for an acceleration of inspections of welds of the RIS (safety injection circuit to inject borated water in the event of a primary circuit failure) and RRA (cooling circuit used during reactor shutdowns) systems on which repairs had been necessary during the original construction of the reactors. EDF said 90% of the repaired welds it identified as a priority due to their repair conditions will be inspected before the end of 2023, with the remainder being reviewed by the end of Q1 2024. ASN has identified Nogent 1 and Curas 2 as particular priorities. EDF said it still expects output from its French nuclear power plants to be in the range 300-330 TWh in 2023.

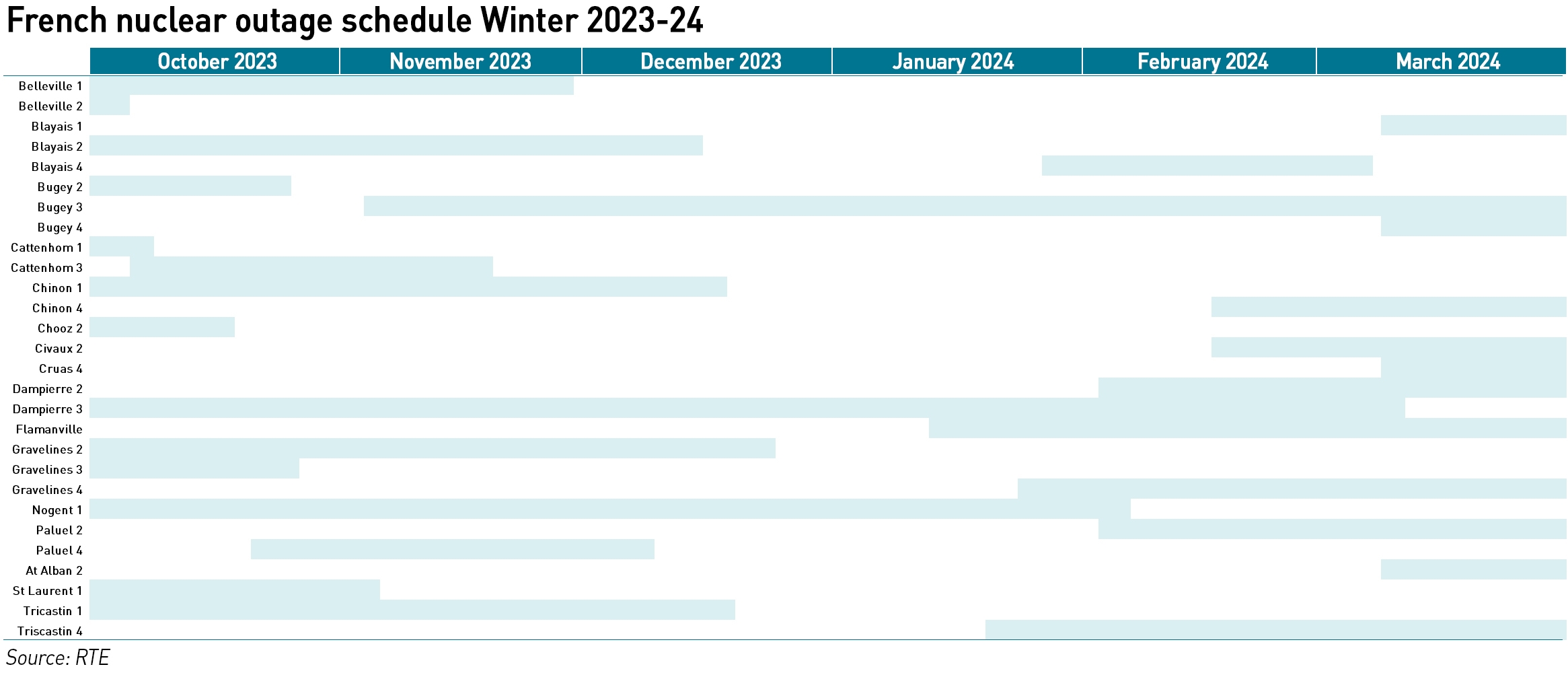

This winter, RTE expects 28 of the country’s 56 reactors to be off-line at one point or another, with the largest concentration (as expected) at the beginning and end of the winter. Of course there is a risk that reactors with outages early in winter will have delayed returns to service, potentially leading to market tightness during the coldest months.

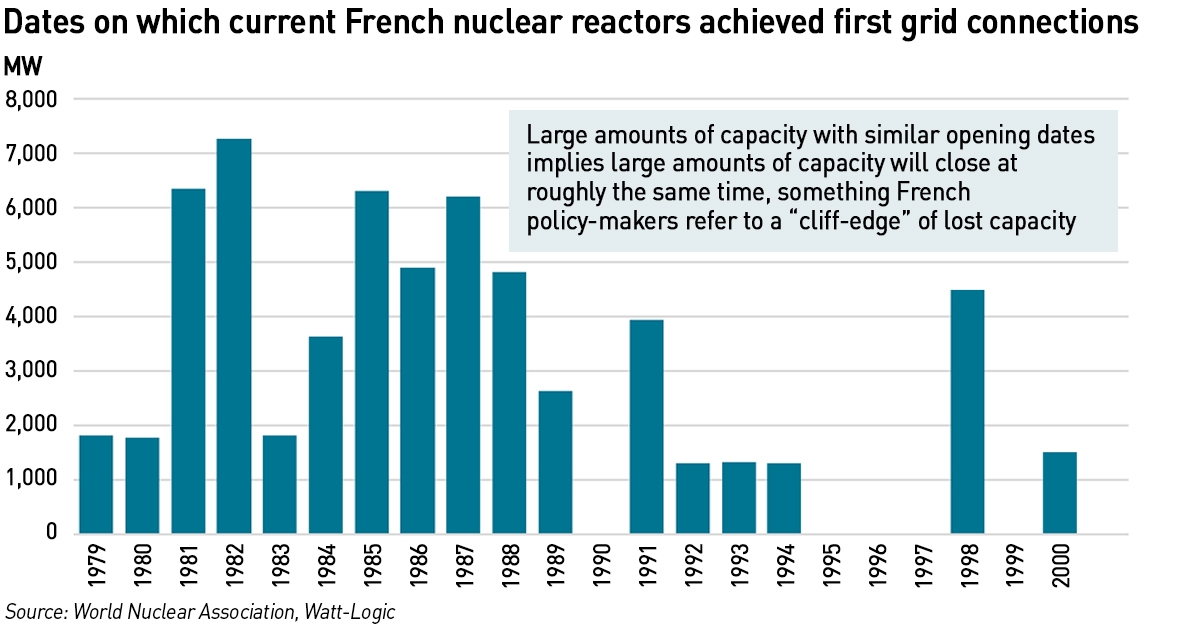

The French nuclear fleet is aging, and it is natural to expect its reliability to fall over time. Only one new reactor is under construction – the 1.6 GW Flamanville 3 – which might open in the first quarter of next year. French policy-makers are becoming increasingly concerned about a “cliff-edge” of reactor closures. The initial life expectations for these reactors was 40 years, although now EDF intends to keep them open for 50 or even 60 years.

If they begin to close after 50 years, the closures will begin before the end of this decade, with the loss of 3.6 GW before 2030 and 33.9 GW by the end of 2035. Even if life extensions to 60 years are authorised, it is inevitable that reliability and therefore availability will fall. With new EPRs taking at least a decade to deliver and no projects other than Flamanville 3 in the pipeline, the next new reactor is unlikely to open before 2035.

So while the initial impact of the stress corrosion problem has abated, there is a strong chance that other issues, whether systemic or affecting individual reactors, will reduce French nuclear output in future, and this will inevitably affect the availability of exports.

While the prospect of blackouts this winter may be lower than last, underlying risks are still growing

Last winter I was concerned about the reliance on interconnectors, and indeed, NG ESO moved away from this position ahead of the winter due to the issues in Norway and France, instead introducing the DFS and coal contingency. In its final winter outlook last year, NG ESO raised the prospect of blackouts due to a potential shortage of gas should the EU restrict interconnector exports due to gas market tightness in Europe.

This year, the specific issues in Norway and France have eased, and there is no mention in the early outlook of concerns over gas supplies. However, there are still threats to gas security should Europe be unable to re-fill its storage facilities before next winter. I was never particularly persuaded by NG ESO’s fears over gas supplies last winter, but it is interesting that this has been completely ignored in this year’s outlook.

Before last year I had been consistently warning that Britain was facing a capacity crunch in the middle of this decade, as conventional generation is progressively replaced with intermittent renewable generation, leading to weather related security of supply risks. With the exception of France and Norway, most of our neighbouring countries are, like us, following a strongly wind-led energy transition. These nearby countries also share similar weather to us, and there can be times when all of these countries experience low wind output at the same time. This was observed during last summer’s heatwave when for around six weeks wind output was depressed (along with lower hydro production) across much of northern Europe. The risk is that collectively these countries wish to import more electricity at any time than France and Norway have available to export, or imports are constrained by interconnector capacity.

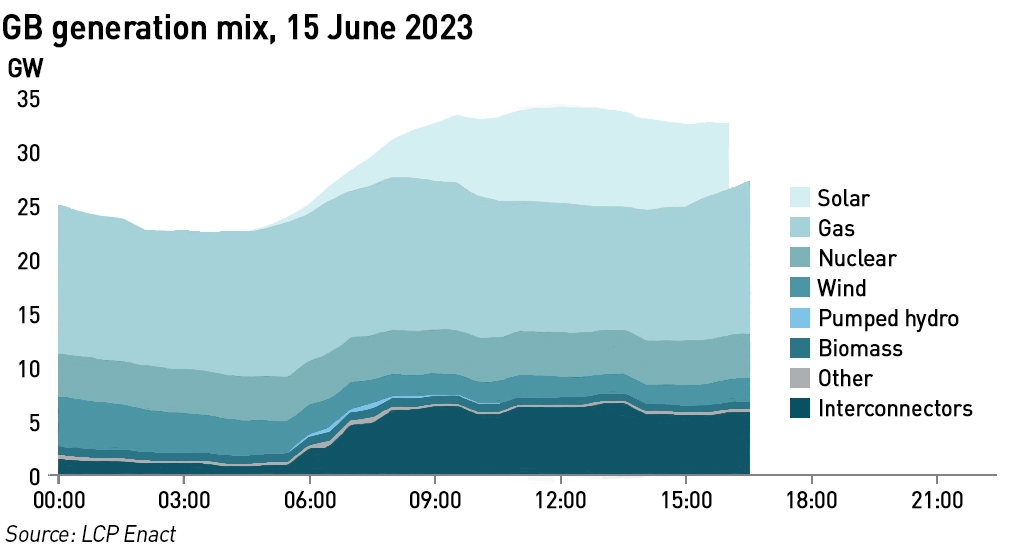

Today’s generation mix is a good indicator of the problem – on a hot summer’s day there is little wind output and we are relying on imports. If anything were to put those imports at risk – eg similar low wind output in our connected markets, then things could get very tight, particularly in winter when there is minimal solar generation.

In Britain, the remaining 2 GW of coal plant is required to close before the start of Winter 2024-25 and two of the last five nuclear power stations (together 2.3 GW) are due to close at the end of Winter 2025-26. On the plus side, a new CCGT was awarded a capacity contract in this year’s T-4 auction and should open ahead of winter 2026-27.

I long have been concerned that the Capacity Market is not delivering enough new capacity to replace closing plant, particularly given the planned increases in demand due to electrification, a trend which is already underway with the expansion in electric car and heat pump use. These increases in demand will further stress the system, including in summer if people start to use heat pumps for cooling, creating demand for domestic air conditioning which is currently minimal. The strategy to manage this appears to be to rely on interconnectors and demand management.

As noted above, interconnectors might not be available when needed, and a reliance on interconnectors increases the concentration of risk since most of the interconnectors are large in capacity terms compared with a typical power station so an unplanned outage would have a bigger impact. And while there can be benefits to demand management, there can also be significant harms. Last winter saw some consumers going to great lengths to secure savings in the DFS, sitting in the cold and the dark to avoid electricity use, creating real welfare concerns. There are also economic consequences should businesses be required to turn down output in order to prevent blackouts.

There might be a smaller risk of blackouts this coming winter than last year, but the underlying risks inherent in our approach to the energy transition are still growing. The margin for error is reducing, and the risk that businesses will be forced to cut consumption in order to prevent a blackout is increasing year on year. NG ESO expects the spare capacity margin to be higher this winter than two years ago, largely based on new interconnectors having opened, but it de-rates these interconnectors using Capacity Market de-rating factors, which have never been tested in practice. And the Capacity Market rules only require interconnectors to be operating – there is nothing to prevent them from exporting during a system stress event, making the capacity issue worse.

NG ESO’s approach to managing security of supply through the energy transition seems to be highly theoretical, and fully take account of correlated risks. Indeed, as I have previously noted, ESO ignores the relationship between cold weather and still weather, using de-rating margins for wind based on average annual load factors, rather than average cold weather load factors which are likely to be much lower. It also says that it models the European power system when thinking about import availability, and while that is important, there’s a lot riding on those models being correct. Any modelling errors could have serious consequences, which may not become apparent until it is too late.

While I can understand NG ESO’s desire to re-assure the market, and give the Government confidence it can manage the grid through the transition to net zero, I would be happier if it gave a more comprehensive assessment of the risks we face and they way in which they overlap. I can’t help thinking that ESO is giving us all a false sense of security, and if its analysis is wrong – remembering that ESO’s analysis also underpins the Capacity Market and the amounts of capacity procured each year – there could be big trouble.

An excellent analysis of the situation. Over reliance on wind, solar and interconnectors is bound to go wrong at some point. Just a question of when.

Quite rightly no country is going to export power to us and turn their own lights off no matter how much we might be willing to pay.

The Russian sabre rattling threatening to target undersea connections to the UK puts offshore windxat risk as well as the interconnectors.

Even if the capacity market is changed to encourage new CCGT build it will need further modification to keep the stations available and viable with load factors as low as 5% by 2030 if renewables are built and perform.

There is an age issue with the existing CCGTs as by 2025 a good proportion will be 30 years old or more and will start to close.

We need a significant nuclear build of a proven reactor type such as the South Korean design to stand any chance of having enough secure and predictable generation.

The powers that be seem to fail to realise the potential disaster that could occur if this all goes wrong and we start to get recurring power shortages.

Industry could be decimated and people die. Once we get that far it would take years to fix.

Another excellent post. I personally think the decommissioning of coal powered stations is a terrible mistake.

If you look at China they are building more and more coal powered stations indicating that the – go green – policy is a complete sham.

Their actual green policy consists of spraying rocks and scrub green

Personally i see nothing less than a significant nationwide affecting blackout event will bring any reality to the conversation that the wind and the sun alone are not enough to ensure a stable power grid.

Agreed but until then we will have many winters of load shedding, each time met with an appropriate excuse and the promise of magic technology around the corner to stop it happening next time.

When reality strikes it will be far too late for any sensible planned response e.g. nuclear build out. This won’t be solved, our politicians are incapable of solving it. The reality is we face a future of blackouts just as South Africa is experiencing,

Your excellent post is right to consider the use of averages in modelling work.

There is an ongoing conceptual battle between power and energy to represent the future of electricity production. The electricity system, even with storage, is a power system where supply and demand must be matched second to second. Energy is an average, the more so over longer timescales. We are drifting into a future feast and famine of electricity production where on average everything is fine.

Everyone spuriously calculates the future generation capacity required based on the annual electrical energy consumption.

As a tea drinking nation I use an analogy of tea consumption. If you require a cup of tea a day, wind and solar will reliably produce enough electrical energy to supply you with your essential 365 cups a year. On average everything is fine. The problem is that on some days they will give you ten cups and on other days, with almost zero power output, they will give you none. What is the proposed solution? Change you drinking habits (encouraged by price), use gas (with high emissions), import it from our hopefully friendly and hopefully oversupplied neighbours (cost and emissions unknown) or store it (from days to months – not a cheap or palatable solution). If you throw away any tea you will shortfall on your essential annual target. More wind and solar capacity will be required to make up this shortfall – I have heard the cheerleaders say.

The popular solution of a significantly wind and solar power future, for which NGESO and to their shame other academic institutions are cheerleaders, is untested and unanalysed. Opaque computer models are run (with assumptions not stated) to back up a reassuring group think narrative. Some claim to run them through a twenty year time period. A computer model and long timescales are not required to check basic viability of a proposed solution. Pick a point in time that is stressed (low demand and high wind and solar output) and manually check (by simple transparent arithmetic) that supply and demand balance or can be made to balance without constraining off any wind and solar.

I look forward to further posts on NGESO’s and other bodies modelling techniques and assumptions.

Reading your comment I have an image of people struggling to drink 10 cups of tea to get their one-a-day average up!

The modelling by academic institutions and some consultancies is truly depressing since they seem to be more focused on telling a particular story (presumably to secure fee-earning business) rather than describing realistic but potentially undesirable outcomes. I’m not a modelling expert, but I think many people who lack modelling expertise defer too much to those that do, without questioning the things you don’t need to be a maths expert to question: are the inputs/assumptions reasonable and do the outputs make sense?

Over-reliance on black boxes is very dangerous, and whenever anyone says “our models tell us…” it is essential that those questions are asked.

I have had a go at digging behind the modelling that lies behind the consultancy reports for CCC, NG, BEIS and OFGEM. It is not a pretty picture. At every twist and turn assumptions are distorted to pretend that the house of cards doesn’t collapse. Wind is given outrageously high capacity factors, while worst cases are in fact merely an average year. Dunkelflaute spells are conveniently curtailed before the storage runs out. The storage round trip us impossibly efficient and like everything else is never costed. Demand is as flexible as necessary. Every corner of the modelling is stretched: interconnectors magically have surpluses available, EV efficiency in miles per kWh is super high, heating demand is tiny because insulation is to spaceship standards and people never go in and out. If in doubt, simply invent a new technology and assume it works. Don’t look at covering a run of years. One “difficult” day suffices without considering its onward impacts: if you run down car batteries there is no proper provision to recharge them in compensation.

It’s shockingly bad. It’s just propaganda, not serious work. Let them start by looking at the work of Prof Michaux on the limitations of resource availability and the implications for costs. Or Kathryn’s previous article on wind costs. They live divorced from reality until it slaps them in the face. Then they run away from it.

I attended an event in Parliament last week about long duration storage. In the discussions afterwards I made the point that I doubted we would get rid of unabated gas fired generation by 2050 and that it would probably never be economic to do so. We would be much better off just using gas to fill these low wind gaps and because the utilisation rates would be relatively low, the climate effects would be negligible and the costs of preventing it would never be economic. No-one disagreed…

NGESO seem to be placing a big emphasis on demand reduction through their DFS product (perhaps they should hire Lorraine Kelly to advertise it?). Now they want much greater participation from industry and business, with the Triad mechanism no longer operative. They are hoping that weak government subsidies on bills will leave behind a strong incentive to switch off. However, the noises about DFS are more propaganda than reality. Enough to power 10 million homes they claim falsely. Really the ASA should slap them down and demand that they inform the press and policymakers honestly. The peak DFS reduction as settled was just 294MW between 17:30 and 18:00 on 23rd January. Looking at the Household Electricity Survey (which is a decade badly out of date) I see that peak hours winter demand averages about 1kW per home, while on the coldest day they reported 1.6kW. So that’s enough for 0.18-0.29 million homes, an exaggeration of 33-55 times.

The press has picked this up as well. I ws interviewed on the Today programme this morning to talk about the way “NG now wants businesses to participate in DFS”. I said this isn’t news – businesses were able to participate in DFS last year, and more will this year now that triad avoidance is off the table (obviously without using that jargon!).

I explained that the underlying blackout risk is growing year on year (excluding last year which was exceptional due to the issues in France and Norway) because of the replacement of controllable thermal and nuclear generation with uncontrollable, weather-dependent renewables.

The interviwer said people could earn £10 per day with the DFS and I said that was only true if they were gaming it, and those loopholes are being closed, and most people only saved a few pence, while sitting in the cold and dark.

I wonder about the motives for absurd degrees of exaggeration about the benefits of DFS. The best level was paltry at about 0.6% of demand, and entailed accepting bids of up to £6,000/MWh from aggregators to provide the service. They would have done better to accept Drax coal at £4,000/MWh for a larger volume. The longer term motivation must be to gain enough acceptance and gradual shift in terms to the point where they include actual limitations on offtake or simply switching off supply imposed via the meter and monitoring system. Real power cuts, to ensure you comply with the contract you are coerced to sign because the alternatives are much more expensive. Alteady happening to a degree with higher pricing unless you take a smart meter, or even outright refusal to accept switchers on conventional meters. At the same time many consumers seem to be aware of the possibilities and intentions, and resist being remote controlled. Persuading more volunteers is not going to be successful if the reward is cut. You will be volunteered as if in the Army.

If you look at the assumptions made by e.g. Aurora for their net zero fables for the CCC they entail very substantial amounts of demand being curtailed when renewables fail. Regen’s effort for NG assumes 20-30GW of demand side response by 2035. That’s not going to be voluntary.

https://reports.nationalgrideso.com/bridgingthegapdayinthelife/

The NGESO FES 2022 provides just enough wind and solar generating capacity to meet the annual energy consumption ( using very optimistic capacity factors). It provides the 365 cups of tea a year required. It proudly states that there is insignificant curtailment. No tea is wasted.

However each revision of A Day in the Life 2035 (link above) becomes very slightly less optimistic. For their summer day story despite massive interconnector exports and storage developments they find they have “excess renewable energy”, “high curtailment” and a “low cost energy opportunity” – keep drinking those 10 cups of low or negative cost tea. (I am not an economist but is there any other successful industry with zero or negative prices).

I await a revised FES with increased wind and solar capacity to offset this curtailment. Perhaps 10 glasses of whisky are required to make sense of all this and provide comfort that their narrative is not nonsense and that disaster is not approaching.

I stopped bothering with the FES a couple of years ago, I did an analysis that I never got round to publishing, but it showed that outturn numbers often fell outside the range of their prevous predictions over the first 10 years of FES. When I challenged them on this they said they never back-test their FES models!

Unfortunately this is not just of academic interest, there are currently real world consequences. The Welsh government led by their consultants REGEN use the FES as the evidence base that their proposed 100% wind and solar policy is viable. Wales is about to be transformed.

Same thing with Labour nationally under the Ed Miliband policy. Their madcap ideas are based on the even stupider toy model run by EMBER (patron and founder Baroness Worthington who authored the Climate Change Act) with its outrageous assumptions. REGEN’s modelling is approved and directed by National Grid, which makes it marginally better, but still in the realms of infeasible wishful thinking.

Maybe I should update the analysis and publish it then. Might be a good summer project for one of my sons!

Kathryn, Thanks for another excellent overview of the present situation and the portents for the future.

There is one point I would like to raise with regard to the French nuclear fleet. It is undergoing a huge programme – the “Grand Carenage” – of refurbishment, modernisation and upgrading to the tune of about 55 bn euros – roughly 1 bn euros per reactor.

Do you not think that will address the reliability concerns as well as enabling extensions to the working lives?