The first sections of the new electricity interconnector between the UK and Belgium were installed this month with the laying of the first 59km section of the Nemo Link, a joint venture between the UK’s National Grid and Belgium’s Elia System Operator, between the UK onshore landing point and the French offshore section. On 11 September the cable was successfully pulled-in at the beach of Pegwell Bay in Kent. The remaining 71km of double subsea cable will be installed in Belgian territorial waters during spring 2018, with the interconnector being scheduled to commence commercial operations in early 2019. Once operational, the 1 GW Nemo Link will increase Britain’s electricity interconnection with the Continent by 20%.

UK interconnection could treble, but more would be needed to meet carbon budgets

The UK currently has 4 GW of theoretical interconnector capacity (some of this is currently unavailable due to cable faults). A further 7.3 GW have regulatory approval in principle, and there are 2.4 GW of other proposed projects. There is strong interest from investors in supporting interconnector projects, particularly those within the cap-and-floor regime.

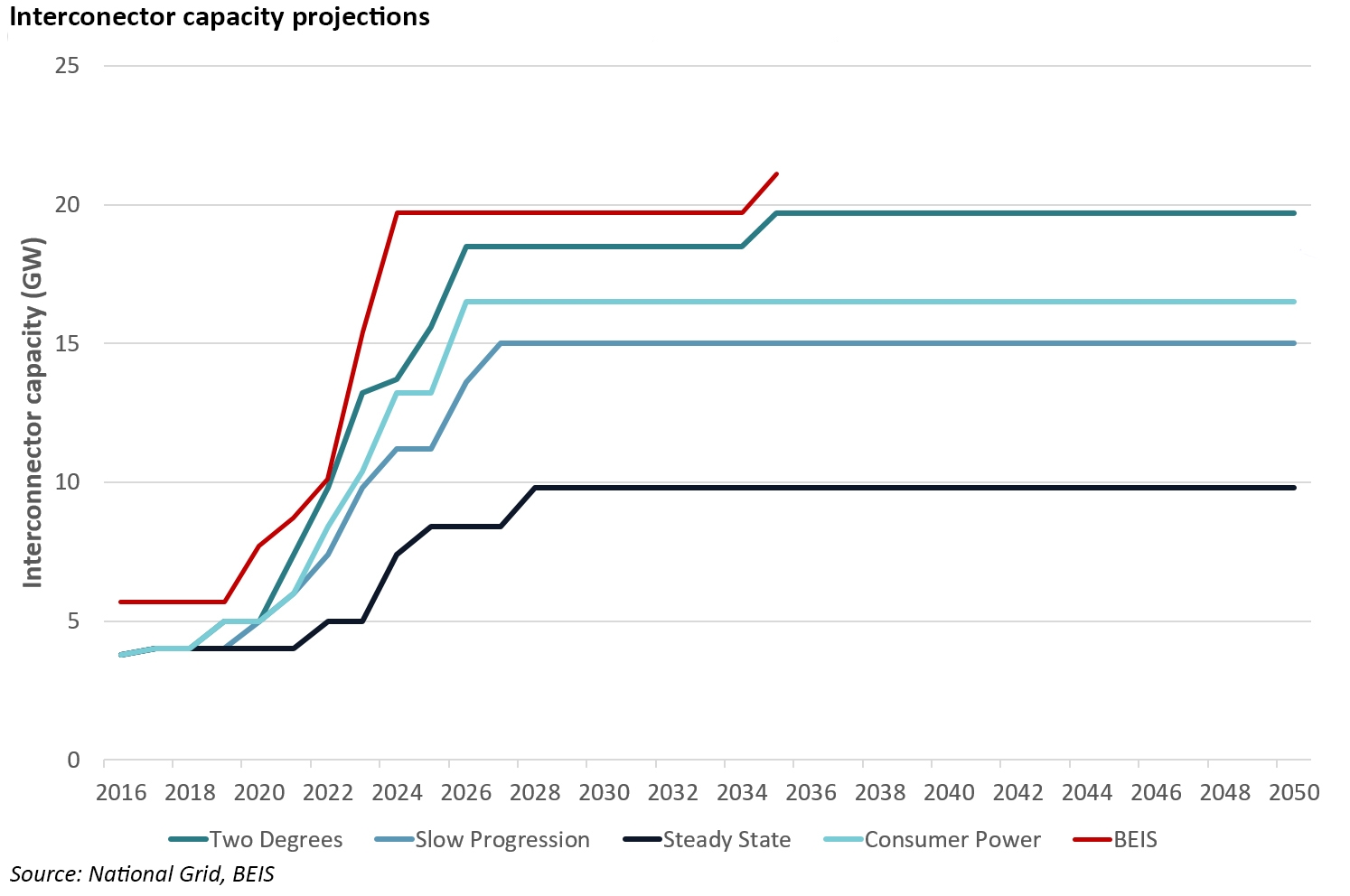

National Grid predicts varying levels of interconnection development in its Future Energy Scenarios, but in each case there are no new interconnectors built after the late 2030s due to market saturation or lack of available investment. National Grid also expects net imports of electricity in the 2020s on the basis that GB prices would be higher than those in neighbouring countries due to the impact of the carbon price floor. After 2030, sustained exports are expected, particularly in the Two Degrees scenario where high penetration of zero marginal cost generation lowers GB prices for long periods of the year. National Grid expects considerable variability of flows, with interconnectors frequently switching between export and import modes.

However, in its Updated energy and emissions projections published last November, BEIS has even more optimistic projections for interconnector capacity. Dr John Constable writing for the Global Warming Policy Forum provides the following analysis:

“…BEIS projections have little or nothing to do with comparative advantage. They are not grounded in economic analyses suggesting that within a few years it will be the best use of resources for UK consumers to buy over 20% of their electricity from overseas suppliers.

On the contrary, it seems clear that what BEIS has done is use imports simply as a free parameter. Where their models of new generation and output fail to meet projected demand they have assumed that imports will make up the balance. That is why the net imports fade away both in absolute quantity and in proportion after the mid-2020s, when new nuclear generation starts to be built.”

This conclusion seems reasonable since in the introduction to the report, it is explained that the projections indicate the broad actions that would be required in order for emissions to remain within the levels set in the carbon budgets, and imports are considered to be zero carbon for the UK. The projections suggest that 8 GW of interconnector capacity would be needed by 2020, growing to 20 GW by 2024. If all the projects currently mooted are delivered, the 2020 target could be met, however, there is no current visibility on how the full 20 GW could be achieved.

The BEIS projections also take no account of market conditions, and only the most ambitious of National Grid’s scenarios which do attempt to factor in market prices, is close to the levels of interconnection needed to meet the carbon budgets. It would also be interesting to consider at what point the market would become saturated: the merchant case for interconnection investment would disappear as prices between the connected markets converge, which will occur if the capacity constraint between the markets is removed.

Is more interconnection desirable?

Most studies into interconnection have been positive, concluding that more interconnectors would be positive for the UK. The Policy Exchange produced a report in November 2016 which summarised some of the findings of these studies:

- The ENTSO-E ten-year network development indicated that 7 out of 9 of the most economically beneficial potential interconnectors in Europe would be located between Britain and neighbouring markets. As the forecasts were based on annual prices, it is likely that they understate the potential benefits;

- Consultancy firm E3G and the European Climate Foundation found that much deeper interconnection across Europe (including up to 35 GW of interconnection between the UK and neighbouring markets) could yield savings on the Europe-wide cost of decarbonisation of up to €426 billion between 2020 and 2030. These savings would require an outlay of €30-138 billion on transmission infrastructure in addition to the €730-1400 billion desired for generation;

- Analysis carried out for DECC by Redpoint concluded that expansion of Britain’s interconnection would have net benefits for social welfare with the benefits greatest in scenarios with more intermittent renewable generation or a bigger divergence in carbon prices between the UK and the rest of Europe. They concluded that 5 GW of additional interconnection, to Norway France, Ireland and Belgium, fitted with a “least regrets” approach. The economic benefits from the modelled scenarios reach a maximum of £4.2 billion in the most conducive to interconnection;

- A 2014 report by National Grid estimated that doubling interconnection capacity would deliver £1 billion per year in benefits to customers by 2020;

- Pöyry’s work for the CCC suggests that up to 24 GW of GB interconnection could be attractive, while E3G forecats the number could be as high as 35 GW.

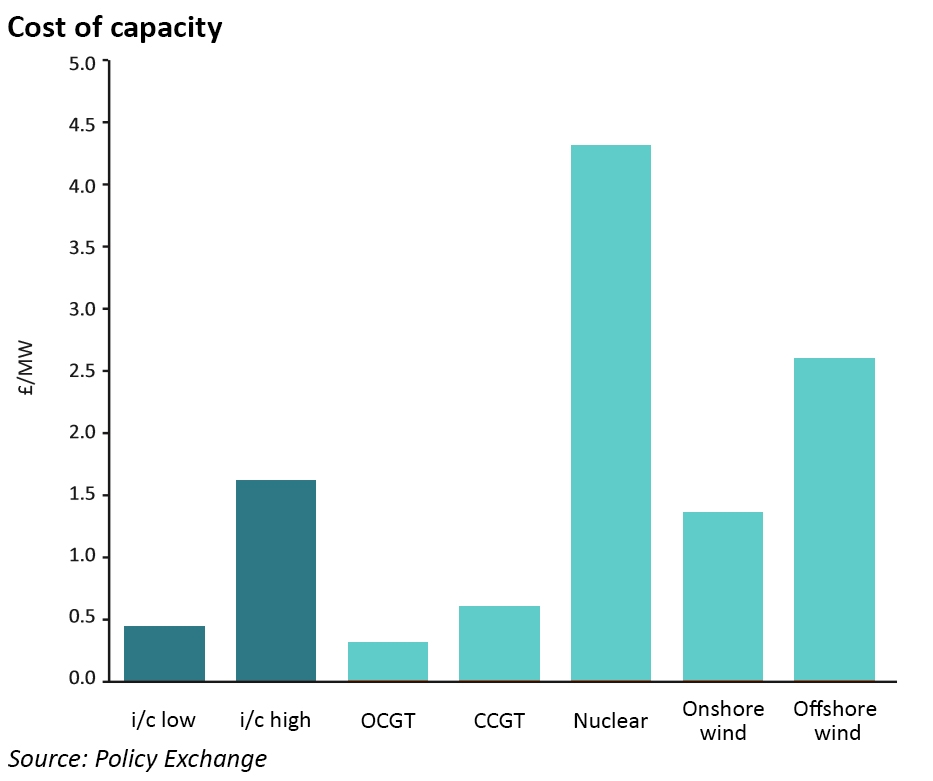

The report also references DECC data indicating the cost of capacity for interconnectors is competitive relative to alternative investments.

The report also references DECC data indicating the cost of capacity for interconnectors is competitive relative to alternative investments.

One thing the report does not appear to consider is the degree to which the modelling behind these figures takes account of all the relevant markets. Pöyry for example, only models the GB market in any detail and therefore the assumptions regarding interconnector flows are largely inputs to the model. Any conclusions about the usefulness of interconnection should therefore be treated with caution, as by definition, interconnectors cannot be assessed based on the dynamics of a single market.

Capturing the value of interconnectors in practical terms can also be challenging, as described in this analysis by Timera Energy, and the picture is further complicated when weather correlation is taken into account.

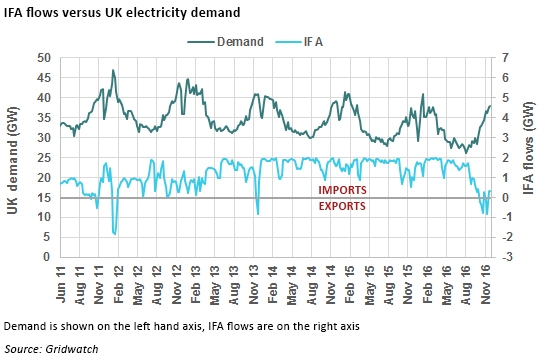

For example, if the high demand in the UK is a result of cold weather patterns across Northern Europe, the demand could be even greater in France, as the French electricity system has a higher degree of temperature sensitivity (due to the widespread use of electric heating, unlike the UK where gas is more common).

It is likely that France would need to limit exports and switch to importing in such circumstances, particularly if nuclear availability is low. This is supported by power flow data on IFA, which show UK exports of power to France coinciding with periods of high domestic demand:

The case for more interconnection also relies on the assumption that interconnectors provide a natural hedge against the intermittency of renewable generation, effectively diversifying GB’s electricity supplies….ie the way in which weather affects supply.

The table below shows inter-country wind correlation from a paper (Monforti et al, 2016) on the synchronicity of wind power production among European countries. It shows that, as expected, neighbouring countries can have highly correlated wind patterns (red indicates the strongest correlations, and green the weakest).

Wind generation in the UK is positively correlated with that in its neighbours – 75% with Ireland, 42% with France, 60% with Belgium and 63% with the Netherlands. The correlation with Scandinavian countries is lower, suggesting that interconnection with Norway and Denmark could indeed provide some degree of a hedge against wind variability in the UK.

This all suggests that that the picture regarding interconnectors is not straightforward and should not be automatically seen as the solution to the UK’s energy challenges. Some level of additional interconnection is likely to be beneficial, but whether seeking to import 20% of the country’s energy needs is sensible remains to be seen, particularly in a post-Brexit world.

WE may end up exporting if green policies leave continetal Europe shorn of reliable baseload energy…