A year ago I wrote a post about all the words we used in 2020, and it’s interesting how many of these were forgotten in 2021. Of course, covid was still a key theme of 2021, but it didn’t quite dominate our lives the way it did the previous year. I suspect that by the end of 2022 we will have finally moved on and by the end of the following year things will be more or less back to normal in a social sense (sadly I think we will be paying the price of dealing with the pandemic for many years to come).

2021 was a dramatic year in the GB energy markets

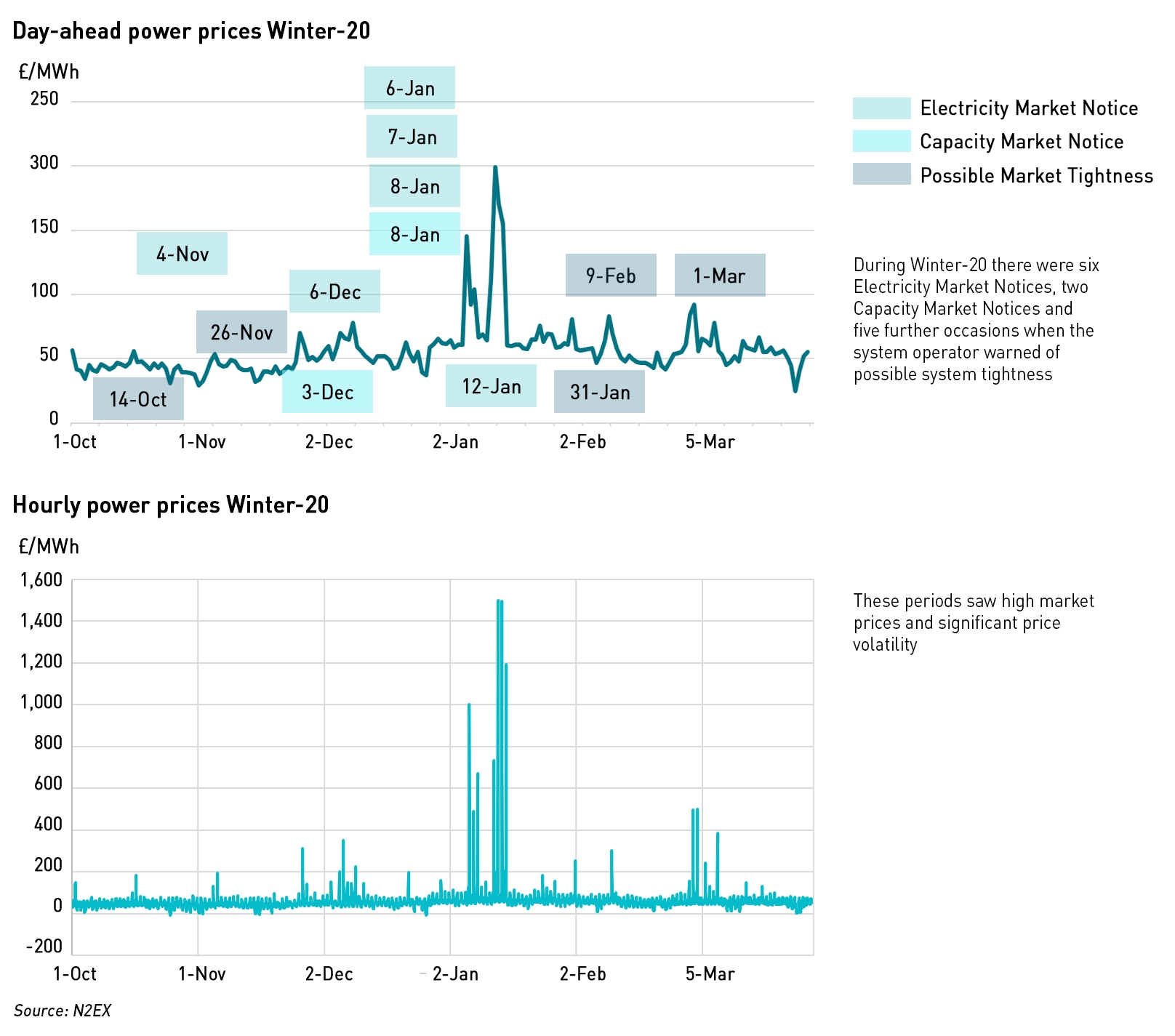

The year began with significant tightness in the power market, with three Electricity Market Notices and a Capacity Market Notice in the first eight days of the year. Imbalance prices hit £4,000 /MWh on 8 January. Late February/early March also saw market tightness due to an extended period of low wind output.

Low wind also returned in September when day-ahead prices exceeded the highs seen in January. Balancing market prices reached £4,950 /MWh with coal units at Drax and West Burton firing up. Imbalance prices reached £3,400 /MWh. This period marked the first time that the impact of low wind conditions, and the fact that they are not rare, really began to enter the public consciousness, although Kwasi Kwarteng’s proposed solution of building more wind farms makes little sense.

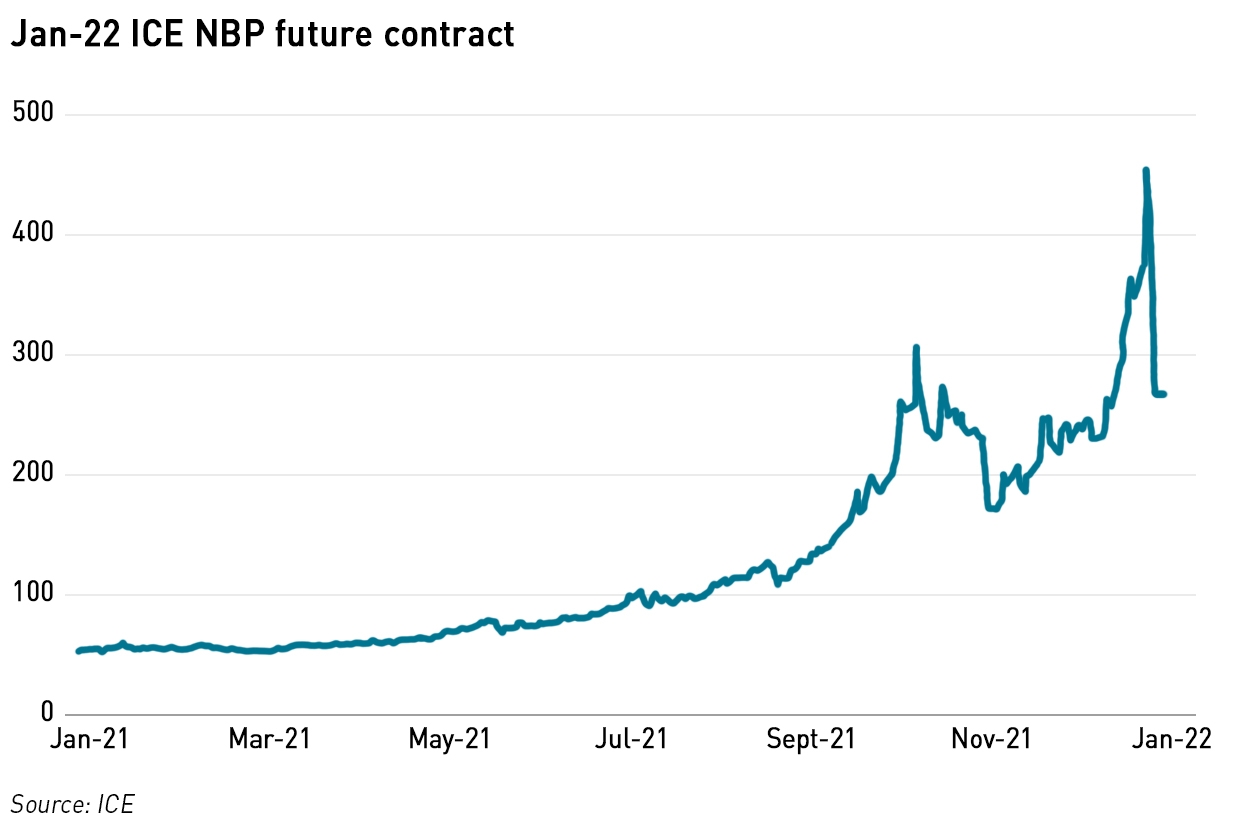

At the same time, global gas prices took off, as it became clear that winter was approaching with unusually low levels of gas inventories, and concerns over gas availability began to grow.

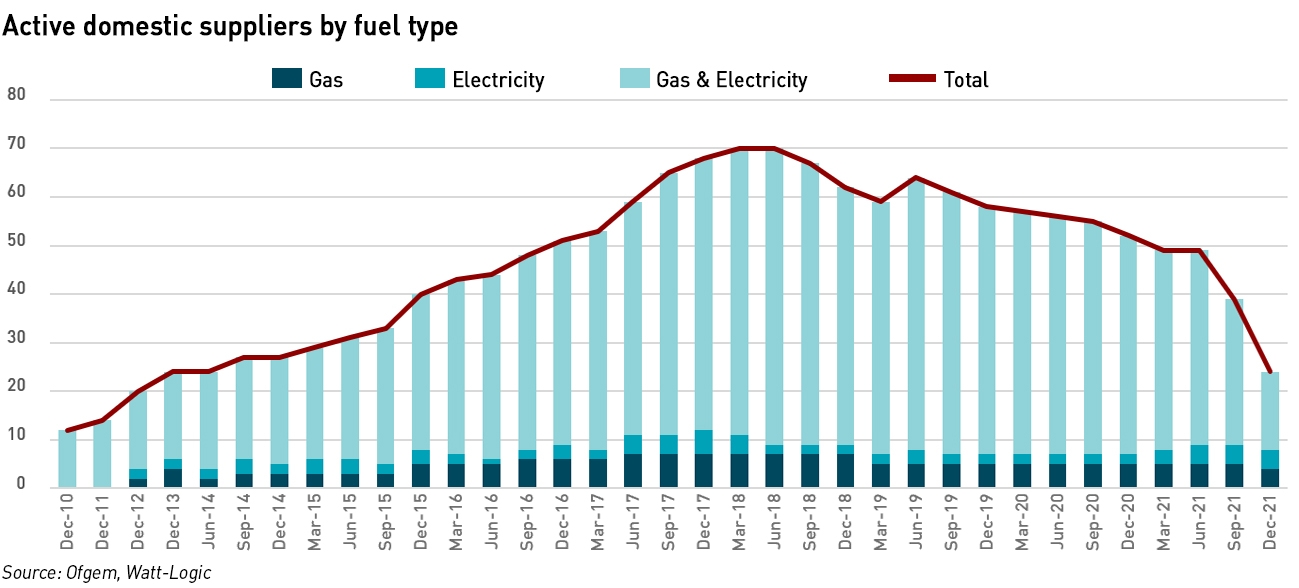

September also marked the start of the string of supplier collapses. By the end of the year more than half of the suppliers active in the domestic market at the beginning of 2021 had closed, leaving behind £ billions in SOLR costs. Bulb, the seventh largest supplier, was the largest casualty, and was placed into Special Administration.

We end the year with the markets in turmoil: wholesale prices continue to be high despite gas prices having fallen back from pre-Christmas peaks, and structural tightness threatens the electricity market. Ofgem is scrambling to address these issues, while the Government is again consulting on the future of the retail market.

So what can we expect in 2022?

More supplier failures

Given recent wholesale price trends, and the fact that the price cap will not be adjusted before the end of the winter, pressures on suppliers remain high and are growing. With every passing day, more fixed price contracts expire and more consumers move to the capped default tariff which is by far the cheapest in the market. Suppliers are now losing the equivalent of £1,000 per customer per year which is clearly unsustainable. It is entirely possible that more suppliers will collapse before the end of this winter.

More regulation in the supply segment

Ofgem has finally woken up to the need for prudential regulation in the retail energy market and will begin stress-testing suppliers in the New Year, although no information has been released about what form these tests will take. Ofgem is also consulting on a wide range of other reforms, none of which will address the core problem which is the inability of suppliers to properly pass on wholesale costs under the price cap. The extent of the reforms proposed by Ofgem will add further complexity to an already highly complex market. Some of these reforms are necessary, but there are serious doubts as to Ofgem’s ability to implement a suitable prudential regime – not only does Ofgem lack experience, but its track record on enforcement, as outlined in a highly critical report by Citizens Advice, is inadequate.

Significant price rises for consumers

Both Ofgem and the Government now want to use the price cap to insulate consumers from the effects of the steep rises in wholesale gas and electricity prices seen this winter, and are exploring other means of spreading out the impact of these increases. But whatever happens, consumers will definitely see a significant increase in the price cap in April, and fixed price deals are already much higher with some as high as £4,000 per year (dual fuel). This will make energy prices even more of a political issue than they are already.

More focus on security of supply

The rising cost of energy, both for domestic consumers and energy intensive industries, is putting energy firmly on the political agenda, and is re-opening discussions on security of supply. Should the UK invest in re-opening the Rough gas storage facility? Does the UK need to enter into strategic firm contracts for gas (the previously hailed deal with Qatar did not commit firm volumes, and there has been very little Qatari gas delivered to the UK this year)? Some commentators believe that high gas prices underline the need to move away from fossil fuels more quickly, but this is unrealistic, particularly within the energy sector.

Moving away from natural gas for heating is a project that will take decades and require £ billions in investment – there can easily be more gas price crises in the meantime. Similarly, the electricity system is a long way from being able to manage without gas – with coal due to close by the end of 2024, and the aging nuclear fleet declining in reliability, we are in fact building more gas capacity (two new-build 700 MW OCGTs won capacity contracts in last year’s auctions).

There are no easy answers here, and my suspicion is that as the political heat dies down, so will the motivation to act, and nothing of any substance will be achieved.

International interconnector tensions

Several European countries including Britain have been quietly building a reliance on imports into their core electricity requirements. Germany is now closing half of its remaining nuclear fleet which is going to have a significant impact on its neighbours: Germany has the highest electricity consumption in Europe, and in addition to exiting nuclear, it also plans to close its coal plant – although that will be impossible this decade. Germany has built significant renewable generation capacity, but most of this is located in the north of the country while industrial demand is in the south, and internal transmission capacity has failed to keep pace.

Several European countries including Britain have been quietly building a reliance on imports into their core electricity requirements. Germany is now closing half of its remaining nuclear fleet which is going to have a significant impact on its neighbours: Germany has the highest electricity consumption in Europe, and in addition to exiting nuclear, it also plans to close its coal plant – although that will be impossible this decade. Germany has built significant renewable generation capacity, but most of this is located in the north of the country while industrial demand is in the south, and internal transmission capacity has failed to keep pace.

In the past few years, many countries have connected their power grids to the extensive Norwegian hydro system, effectively using Norway to balance their electricity needs. As a result, Norwegian hydro levels are now at historic winter low levels, and although in theory these interconnectors should allow Norway to import cheap wind power from its neighbours, this is not happening in practice.

Even if it did, Norway does not have very much pumped hydro capacity, so cheap imports do nothing to restore the hydro balance even if they take place. Now Norwegian power prices, which have always been among the lowest in Europe, are beginning to rise, and with it fuel poverty is growing. This is creating political tensions in the country, with people beginning to question the wisdom of exporting so much of its hydro capacity.

Other countries are also looking at the extent to which subsidised renewable generation is being used to support consumers in other countries: Denmark exports around half of its subsidised wind power. As prices rise across the continent, this is an area which is going to attract attention, and may lead to countries reviewing their position on electricity exports and potentially restricting cross-border capacity or charging additional fees in order to ensure that the economic benefits of energy investments remain in the country which made those investments and are not realised by consumers in other countries.

.

I’m more confident in my predictions this year than I have been in the past – certainly I think there is little doubt about the first three on my list. The last one may not really emerge this year, but I definitely see this as a growing risk, so if not in 2022 then at some point soon, the use of interconnectors and reliance on electricity imports is going to become a source of political tension between European countries. In any case, what I can say with confidence is that 2022 is unlikely to be boring in the energy markets!

.

I wish you all a very happy and prosperous New Year!

As an engineer and a consumer of electricity I like stable and boring. I feel uneasy about exciting virtual reality games with serious winners and losers.

This morning nearly 20% of UK electricity (65% of that subsidised renewables) was exported on the inter connectors. Lets hope we were not selling it for the BM price of -£75. With demands at summer levels and high winds there was a feast of renewables with many constrained off and others exported. Lets hope that in times of famine the inter connector flows will be reversed and similarly priced.

An exciting new year.

If nothing else it gives you plenty to write about and much for us to read and comment so I thank you for taking the time to produce these blogs which have really shone a spotlight on the issues that most people have no real idea exists. Looks like Norwegians saving water today as we are sending them 0.74GW !!

Happy New Year

It seems Ireland (Both Northern and Republic) are missing from the interconnectors map, as isJersey (a tiddler, but important to them !)

I greatly enjoy reading your blog and the insight it gives.

Happy Year++

I applaud your insight and energy even at holiday time. But, of course, the demand for energy never ceases.

The Government may be able to fudge the solutions to many problems – but energy is not one of them! Having made such a mess of the nuclear power industry, one wonders whether they have really understood the problems involved for many years. Sadly, long term problems rarely have quick solutions.

On the topic of Norwegian electricity prices, it is significant that Norway has a lot of direct electric heating. It’s an interesting contrast with Sweden which has a lot of heat pump installs. Historically low Norwegian electricity prices have meant that the capex/opex trade-off between direct electric and heat pump has come out differently in the two countries.

What this means is that rises in historically low Norwegian electricity prices could lead to fuel / heating poverty much faster than elsewhere and this would result in substantial pressure to effectively decouple from the interconnected market by restraining the amount of exported hydro electricity through the interconnectors.