Several people have reached out to me today asking me to comment on Ofgem’s announcement about the SOLR cost recovery, so I’m writing this quick blog on the subject.

Back in October, Ofgem published a letter setting out its plans to make temporary changes to the Supplier of Last Resort (“SOLR”) cost recovery process known as the Last Resort Supply Payment (“LRSP”), allowing some of those costs to be recovered more quickly than would normally be the case, given the large amounts involved.

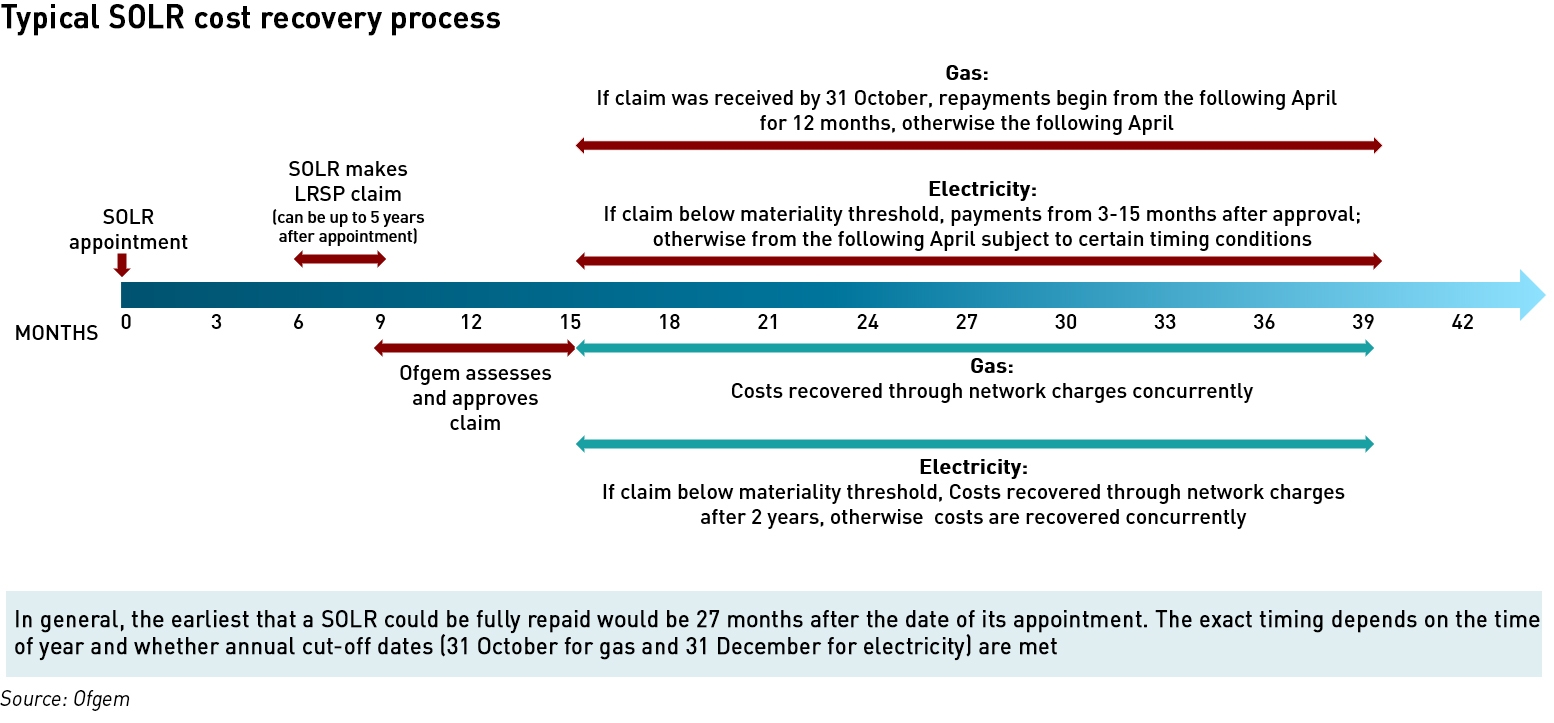

In normal circumstances, the earliest that SOLRs can begin receiving LRSPs is from around 15 months after their appointment, with full repayment coming around 12-15 months later. The main types of costs that can be claimed are the additional wholesale costs arising from having to buy energy on short notice for the new customers acquired through the SOLR process, and the cost of reimbursing consumer credit balances.

These recovery mechanisms are set out in the supply, gas transporter and electricity distribution licences which cannot be easily or quickly amended, but Ofgem recognised that the scale of the recent SOLRs as well as the high cost of buying energy for the affected consumers in the current market conditions has placed unreasonable burdens on SOLRs (and may have threatened Ofgem’s ability to find suppliers willing or able to act as a SOLR).

.

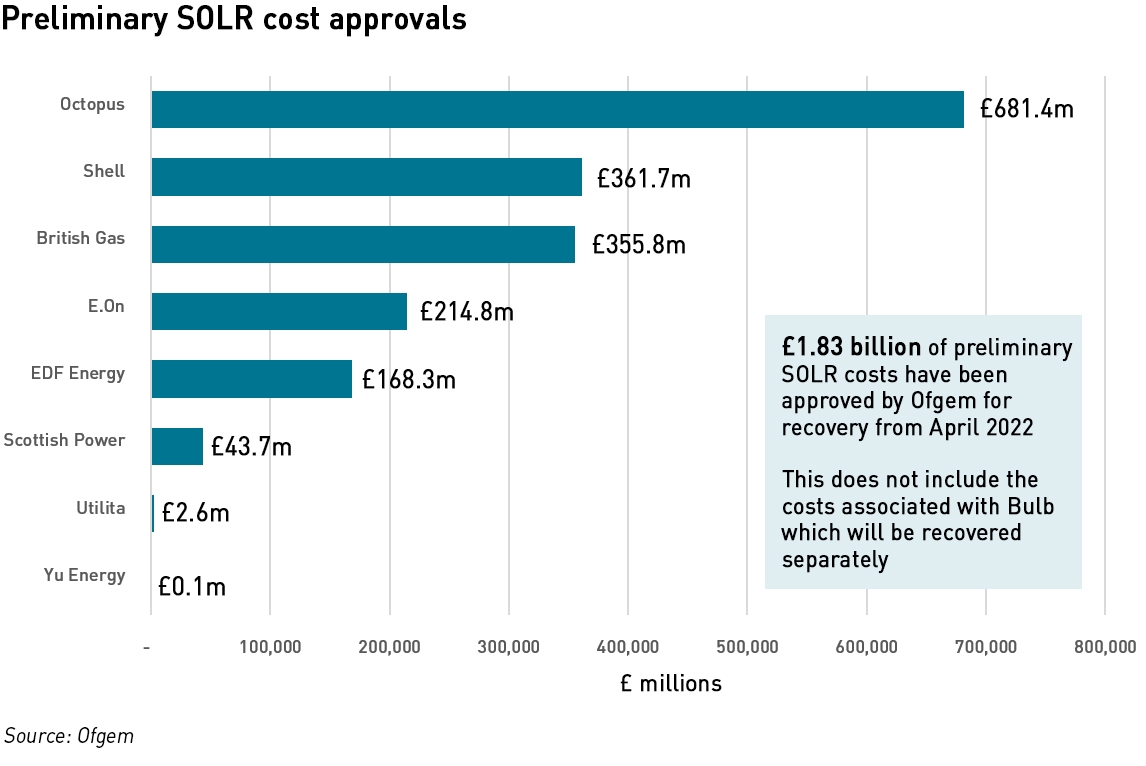

In order to speed up the cost recovery process, Ofgem has decided to allow SOLRs appointed since September to submit two claims per appointment, an initial amount relating to wholesale costs, and a subsequent reconciliation amount. Ofgem committed to approving these initial amounts before the end of this year, if submitted by the 6 December deadline, so that cost recovery could begin in April 2022. As a result of this, Ofgem has today approved £1.8 billion of initial SOLR costs which will be added to network charges from April.

.

Of the £1.83 billion of costs approved by Ofgem, the largest single amount relates to the collapse of Avro, where Octopus has claimed an initial amount of £681 million to cover the costs of buying energy for its 580,000 customers. The costs relating to the collapse of Bulb are not included at this stage since the special administration cost recovery process will be different and possible spread over a longer timeframe. Ofgem has indicated that it may have wished to go further with its changes to the LRSP process but that it would have needed to make changes to licence conditions requiring statutory consultations for which there wasn’t time.

What is interesting about this is the role network companies play in the process. Arguably this should have nothing to do with network companies, and the only real reason they are involved is for administrative ease since they provide a mechanism by which the costs incurred by each SOLR can be socialised across the market as a whole. When SOLRs were rarely used, this was a convenient approach, but with the recent wide-scale use of SOLRs, covering some 4 million households as well as large numbers of non-domestic consumers, the high costs involved are material to the network companies and could create un-necessary risks to the segment.

Ofgem is trying to minimise this contagion risk, but one area of future reform might be to explore a means of recovering SOLR costs that by-pass network companies altogether. In order to push through this accelerated LRSP process, Ofgem is having to grant derogations to certain network company obligations, and provide assurances that it will not pursue enforcement action connected with some of these rules. All of this adds complexity and cost. The network companies are also concerned that this process could give rise to over-payments to some of the SOLRs which could be difficult to recover if the SOLR itself subsequently gets into financial distress. They may be comforted by early indications that credit ratings agencies do not see this adjustment as presenting a particular risk.

One thing is certain – energy bills will be much more expensive for consumers from April, with the price cap set to rise significantly. Cornwall Insight is predicting an increase of 46%, and says average bills could exceed £2,000 per year. It expects the total costs of the SOLRs this year to be around £2.4 billion, excluding Bulb, which equates to around £90 per household per year.

“With Ofgem examining a wide range of potential reforms to both the cap and the way in which the costs associated with supplier failures are recovered, we note that there is still a large amount of uncertainty relating to the level and structure of the cap,”

– Craig Lowrey, Senior Consultant, Cornwall Insight

In the meantime, wholesale prices in both gas and electricity continue to be very high. Recent cold weather in Russia has seen gas flows into Europe slowing, and an acceleration of storage withdrawals. Storage levels are now only at 59% compared with an average for late December over the past 5 years of 75%. Electricity markets are also tight as low wind conditions, the temporary closure of 4 French nuclear reactors and several CCGTs tripping in the UK all contributing to narrowing capacity margins. Coal has been running round the clock in GB to support the market.

Several people have reached out to me following my Christmas blog to say that, while they appreciate the tongue-in-cheek nature of the post, they think it’s rather closer to reality than might be expected. The pressures on European gas and electricity systems are rising, and policy actions such as the imminent closure in Germany of half of its remaining 6 nuclear reactors is likely to make matters a good deal worse. There may only be 9 days left in the year, but something tells me that the energy markets are not done making headlines in 2021…

So in the short term the OFGEM is paying these sums to the SOLRs but will have to recover the costs from the mugs who were too stupid to switch suppliers?

I also like the way we are having to run our coal stations at c1.8GW earlier and sending the same level over to France. Of course reality is actually we are importing via NEMO and BRITNED and then loading our SE England transmission network up to shift it back to France.

No, it’s network companies that pay suppliers while at the same time charging it back through network costs (paid by suppliers) which are then charged to consumers through bills.

Privatise the gains and socialise the losses. What a mess with many well paid jobs required to sort it all out. If only the same amount of money, brainpower and engineering effort was involved in planning a workable path to net zero.