Gas market tightness has caused prices to rise sharply over the past few weeks, not only pushing electricity prices higher, but also causing supply issues in industries such as fertiliser manufacture which rely on natural gas as a feedstock. This is creating major headaches for across the economy and is leading to questions about the UK’s security of energy supplies this coming winter.

Why are gas prices rising?

The gas market is experiencing both increasing demand and reduced supplies – a perfect storm for prices.

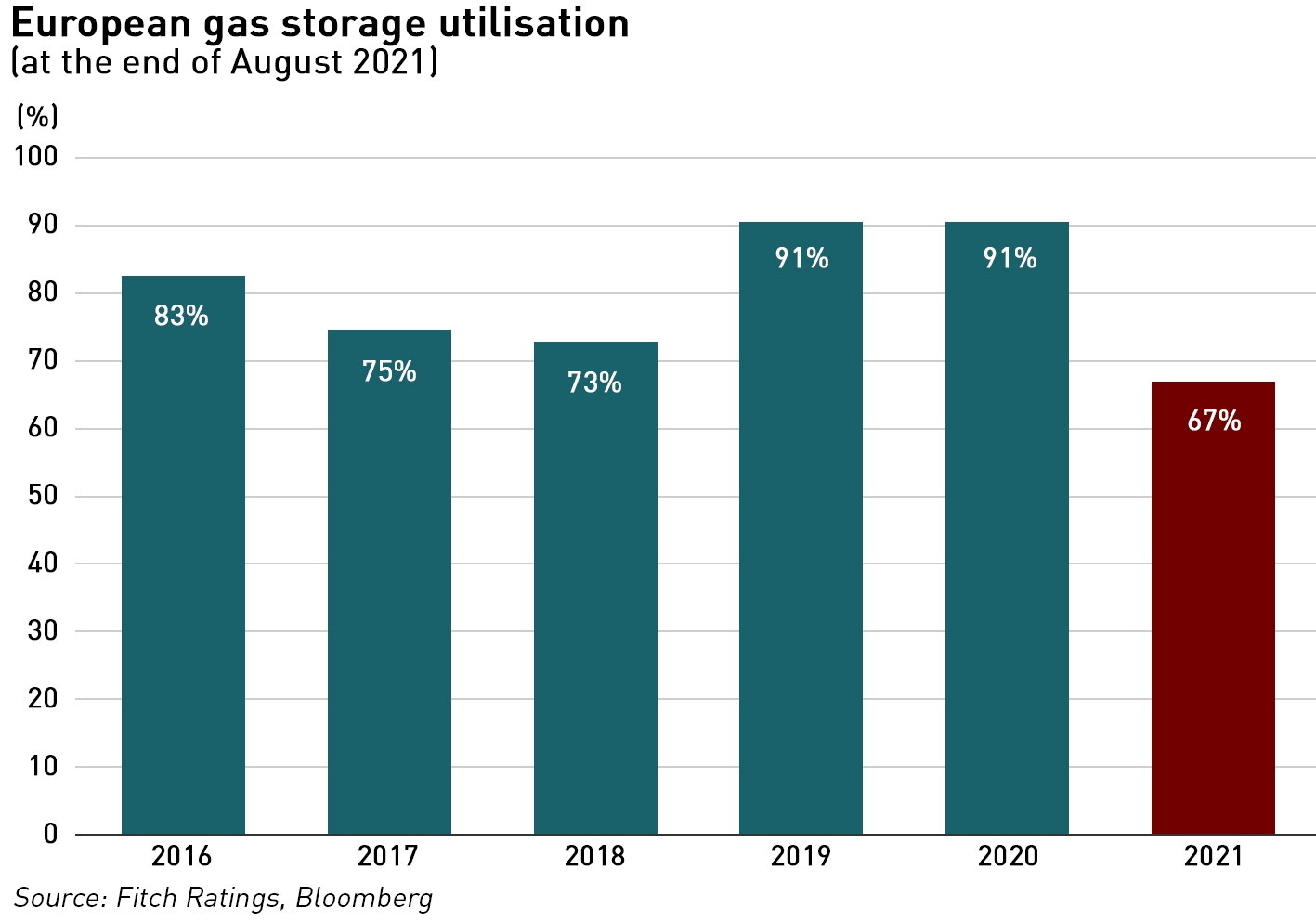

The pandemic saw energy demand fall across the globe as shelter-in-place orders reduced economic output and with it the demand for energy. However last winter saw prolonged cold weather across Europe and North America, particularly towards the end of the winter, causing storage levels to fall significantly. In a normal year, gas storage would re-fill over the summer when heating demand is low, but this has not happened at the pace required to be full ahead of this winter.

Inventories were further reduced this summer by the heat waves seen across the northern hemisphere (except in the UK which largely escaped the hot weather), and in China, while coal shortages in India and a lack of hydro-electric generation due to drought in Brazil have also fuelled the global demand for gas.

Flows of gas from Russia have been significantly lower, for reasons that are subject to some controversy. Some of the reason is the need to re-fill domestic storage after last winter as well as some reduced production levels, and maintenance on both the Yamal-Europe and Nord Stream pipelines. There was also a fire at one of Gazprom’s condensate treatment plants in Western Siberia in August. But there are also suspicions that Russia is trying to exert pressure on the EU and in particular Germany to approve the start-up of the Nord Stream 2 pipeline.

“That’s because Gazprom is readying itself for starting Nord Stream 2 and it is hoping to exert an element of leverage in terms of trying to make sure that when all the regulatory t’s get crossed and i’s get dotted, that that process is as swift as possible,”

– Tom Marzec-Manser, lead European gas analyst, ICIS

European gas production has been depressed, with several outages disrupting flows from the North Sea. Norway has seen a several outages this summer, including at the giant Troll field, one of the key sources of gas into the UK. Production from Groningen gas field in the Netherlands is falling, with the possibility of closure three years ahead of schedule. Elsewhere Nigerian LNG production from Bonny Island was down by the equivalent of over 30 standard cargos between January and July of this year compared with the year before.

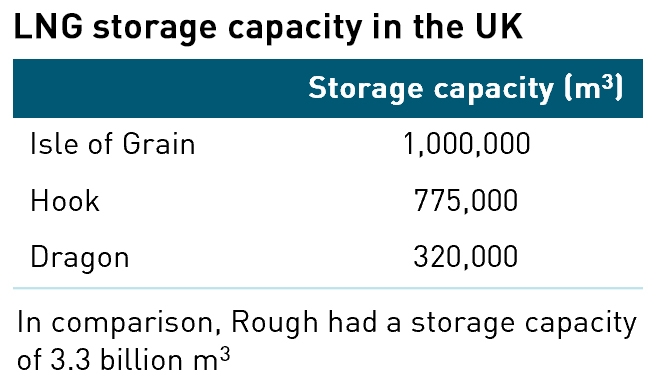

The UK is particularly vulnerable to lower volumes of gas in Europe. Since the closure of Rough in 2017, the UK has operated a “just-in-time” approach to gas procurement. The only meaningful storage capacity left is at the UK’s three LNG terminals, which collectively hold just over 2 million m3 of gas, and eight salt-cavern storage facilities – typically used for short-term cycling – with a combined capacity of around 1.7 billion m3 . This compares with the 3.3 billion m3 capacity at Rough alone.

In order to fill its LNG storage, the UK must attract LNG cargoes against stiff competition from Asia, where demand is rising fast, driven by surging economic activity in China. There is some capacity to swing volumes under long-term contracts with Norway, but there are concerns about our ability to attract pipeline gas from the Continent when Russian flows are down and countries upstream may prioritise their own needs. There is a tendency for some commentators to link this with Brexit, forgetting that Ireland is still an EU member and its gas supplies from Europe must transit the UK.

“We’re effectively at the end of the pipe — not just physically but politically as well. It’s far from inconceivable that we could have a problem in the event of a very cold winter,”

– Niall Trimble, Energy Contract Company

In Asia, the JKM marker shot up to all-time highs above US$20 /mmBtu. Some countries find these levels unaffordable and may cancel their LNG cargoes – a price rally in early 2021 forced Pakistan and Bangladesh to ration gas and cancel LNG deliveries – which may make volumes available to Europe.

How gas is priced in the international gas markets

The other interesting dynamic is in pricing. Historically, most of Russia’s gas sales to Europe were made through long-term contracts signed with monopoly exporter Gazprom, and were indexed to oil prices via complex averaging formulae with different time windows and lags. The reason for this oil indexation goes back to the days before gas markets were liquid and gas was priced on the basis of fuel switching with oil or coal. A few years ago when wholesale gas prices were lower than oil indexed prices, these contracts were very out of the money and their take-or-pay provisions were hurting European utilities. Now the reverse is true, with has prices at an oil-price equivalent of more than US$ 100 /bbl, people with oil-indexation benefit compared with those with pure spot gas exposure such as the UK.

Since 2005, the European gas pricing has evolved to gas-to-gas competition as is the case in the US market. Around 80% of the natural gas consumed in Europe in 2020 was priced based on gas-on-gas competition, with only about 20% still being indexed to oil. At the same time, gas pricing in east Asia continues to be predominantly based on oil-indexation. This makes the European gas markets more flexible, but exposes the region to strong international market fluctuations.

LNG in Asia is priced off the Japan-Korea Marker (“JKM”) which has become a key barometer of the of balance of the global LNG market determining the flow of cargoes into Asia versus Europe. Liquidity in JKM has grown rapidly in the last 3 years, with the marker being increasingly used as the basis for physical trades (both in and outside Asia) as well as a contract reference point for derivatives (such as JKM swaps) and even medium to longer term supply contracts. It generally moves in a relationship with the more liquid European benchmark, the TTF hub price, due to the large volumes of flexible LNG supply that can arbitrage price differences across Europe and Asia.

Asian LNG demand is less flexible than European gas demand, where large volumes of price responsive coal-to-gas switching flexibility in the power sector allows gas demand to respond to pricing, and, like the UK, Asian countries tend to have limited gas storage capacity, meaning they rely on a steady flow of LNG cargoes. Currently JKM prices are at record high levels making it difficult for Europe to secure cargoes.

In a balanced market, the marginal source of supply that balances the Pacific basin determines the price spread between Asia (JKM) and Europe (TTF) with the price spread being based on the cost of diverting a cargo to either Europe or Asia. This diversion cost is generally influenced by time charter rates, TTF prices (to value boil off cost), canal fees and port costs.

In a tight market, JKM prices rise relative to TTF and attracts cargoes into Asia from further afield, that is from supply sources with longer voyages and a higher variable costs of delivery. The most expensive incremental supply that can be diverted to Asia is generally the reload of European cargos. However, when the market is long, US production needs to be shut in to balance the market, and Henry Hub prices act as a floor for both TTF and JKM with pricing dynamics driven by the variable costs of liquefaction and shipping.

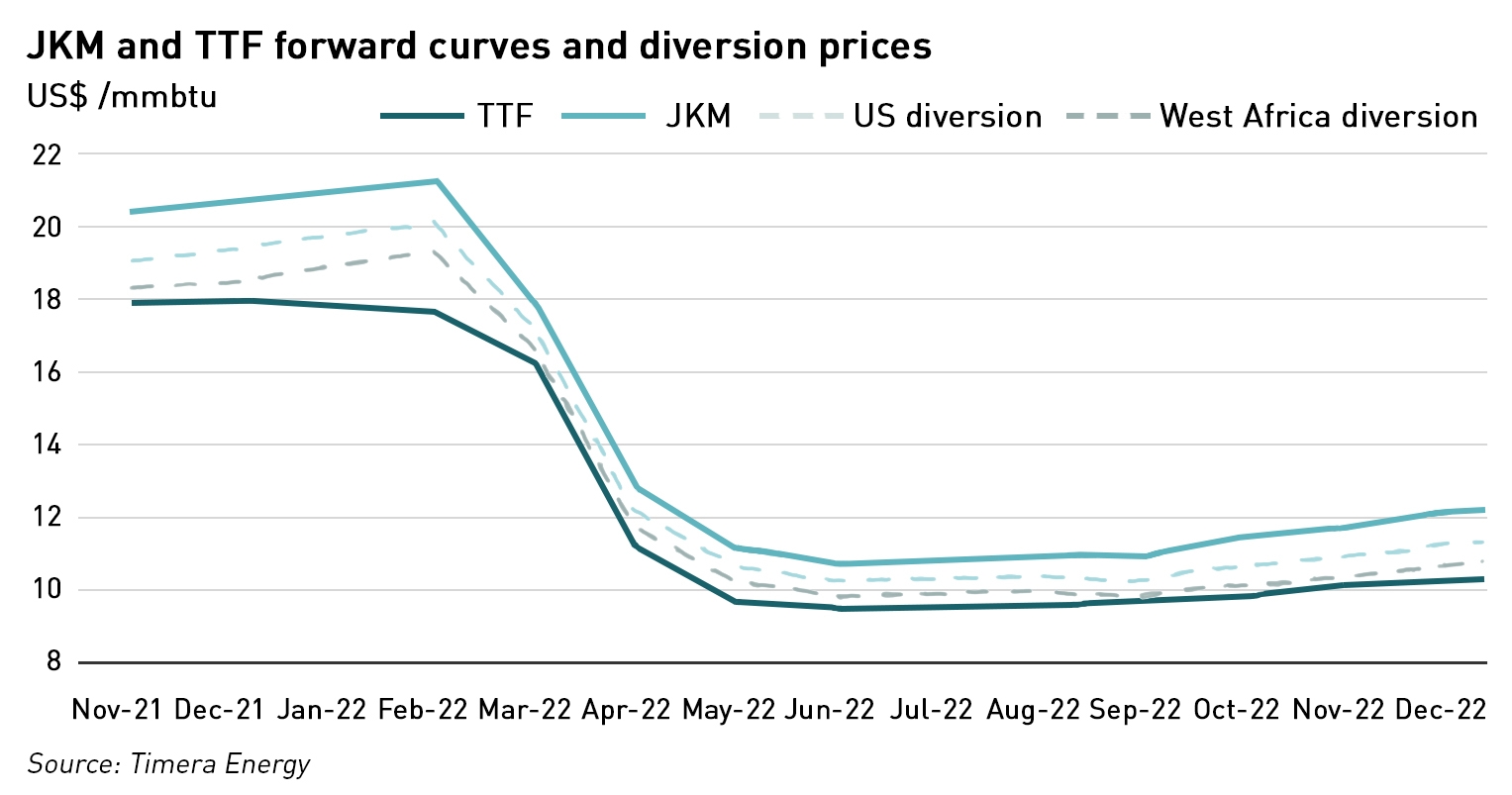

The chart indicates that despite European prices being high, Asian prices are higher. The dashed lines on the chart show the diversion costs for West African and US supplies – if these diversion prices are above the TTF price then it is more profitable to send cargoes to Asia. The diversion curves are calculated based on the JKM price less the incremental round trip costs to divert a cargo from Asia to Europe.

US LNG is typically the source of marginal supply given its large volumes and relative flexibility – the chart shows the US diversion curve reconverging with TTF prices during 2022, which is consistent with the forward market pricing in a more balanced market in 2022 as supplies recover to meet demand.

Gas market tightness unlikely to ease until well into 2022

The decline in demand in 2020 amounted to a drop of 2.1% – the largest fall since the financial crisis in 2009 – resulting in a sharp reduction in drilling and capital investment across the industry, leading to an unprecedented decline in worldwide output. Production fell by 3.1%, the largest decline since at least the 1970s. Production has remained depressed even as global economic activity has recovered, with prices rising as traders believe there will be insufficient production to meet demand by the end of the year.

Rising prices send a strong signal to the industry to boost production and are providing the cash flow to finance a major increase in output. This should support strong growth in 2022 and 2023, but ramping back up takes time. Before the pandemic, both global production and consumption had increased at a compound rate of roughly 3% per year for around a decade.

In the meantime, the markets will have to make do with lower supplies, and widespread gas-to-coal switching is expected in power markets, and even gas-to-oil where oil-fired generation exists (the UK no longer has any large-scale oil-fired power stations, however it has a fair amount of small-scale embedded diesel generation typically under 20 MW in size).

The market is expected to return to balance by the end of 2022, with prices reverting to long-term average levels.

How vulnerable is the UK?

The Government has been at pains to stress that there is plenty of gas around and there will be no supply disruptions through the winter. Today, Kwasi Kwarteng made a statement to Parliament on the state of the UK gas market, saying:

“We have sufficient capacity and more than sufficient capacity to meet demand, and we do not expect supply emergencies to occur this winter. There is absolutely no question, Mr. Speaker, of the lights going out, or people being unable to heat their homes. There’ll be no three-day working weeks, or a throw-back to the 1970s. Such thinking is alarmist, unhelpful and completely misguided.”

He was also able to announce that Norwegian production will ramp up from 1 October to increase exports into the UK. Bizarrely he also stated that the UK is still too reliant on fossil fuels and should develop more renewable generation, apparently failing to understand that low wind output is the reason for the doubling of electricity prices in the last couple of weeks on top of the doubling over the past year. Congratulating himself and the Government on the renewables roll-out while those renewables are currently failing to deliver has a certain irony.

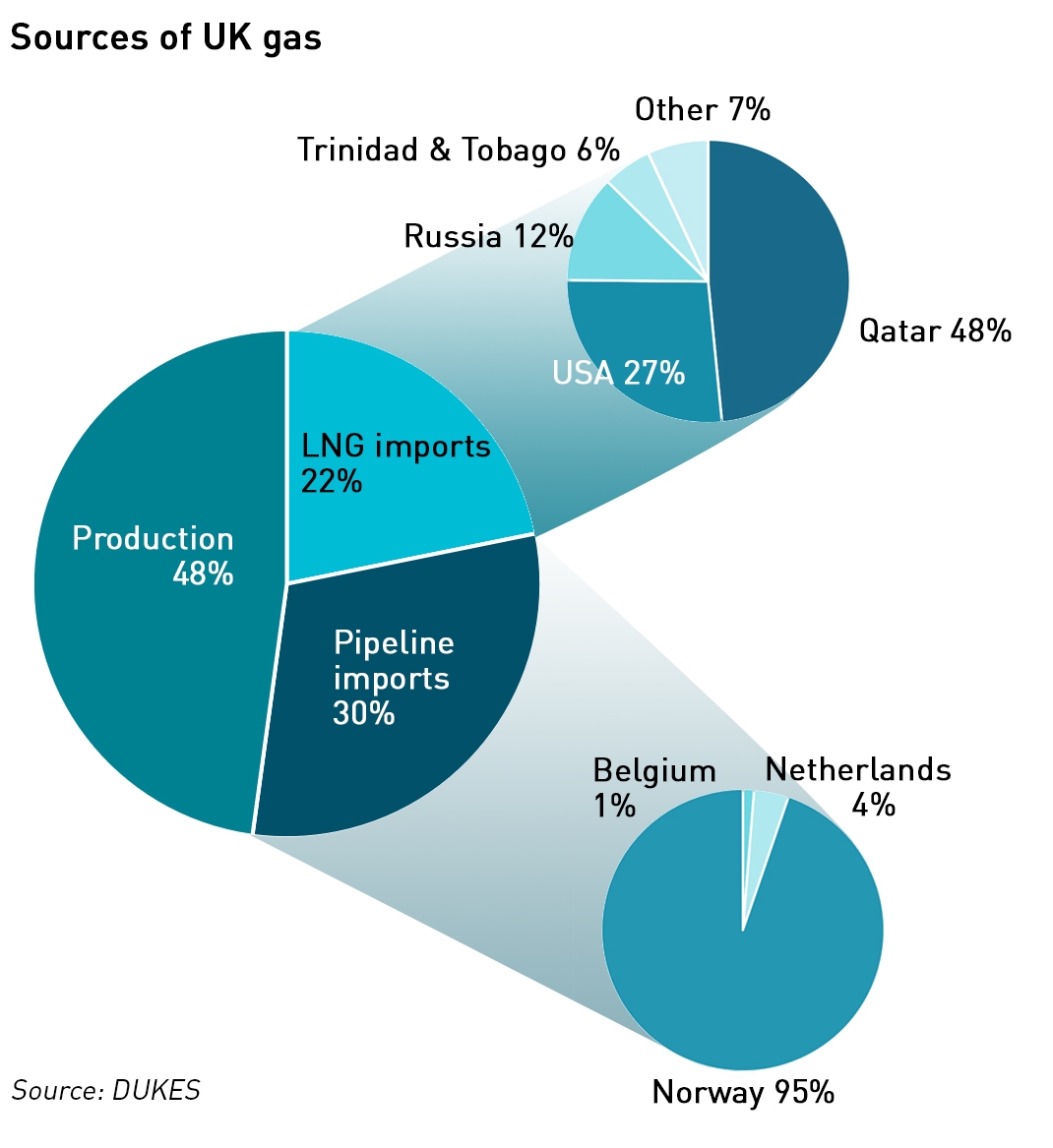

However his arguments on gas supplies have more basis in reality. Almost 50% of the gas we use comes from domestic production which is insulated from global supply and demand pressures, and new discoveries in recent years mean there are reasons for optimism around the future of the UKCS.

However his arguments on gas supplies have more basis in reality. Almost 50% of the gas we use comes from domestic production which is insulated from global supply and demand pressures, and new discoveries in recent years mean there are reasons for optimism around the future of the UKCS.

30% of the gas we use comes through pipeline imports, and of this 95% is from Norway, under long-term agreements. Norway is clearly a highly reliable partner, so these supplies can be considered secure subject to temporary operational constraints. Another 22% of our supplies comes from LNG, which, when taken with our pipeline imports from Continental Europe means that about a quarter of our imports are subject to global pricing dynamics.

The security of this supply is more precarious because very little, if any, of the UK’s LNG deliveries are under firm contracts. A study currently being conducted by UKERC and the Oxford Institute for Energy Studies into the role of LNG in UK gas security suggests that the only long-term contract is between Centrica and Qatargas – a five-year agreement signed in January 2019 for up to 2 million tons a year. However the details of the contract are unclear, and it is possible that supplies could be diverted in a tight market. It also should be noted that the transit time for a cargo from Qatar to the UK is two weeks.

A government study into the UK’s security of gas supplies in 2017 found that:

“The modelling shows that even where there is an extreme shock to global LNG markets, GB demand can be met if GB consumers are willing to pay for it.”

And this is the fundamental nature of the spot LNG market – cargoes can be diverted if a buyer is willing to pay more than any other buyer. The UK can attract more LNG if it is willing to pay a premium to Asian prices.

A serious re-evaluation of energy policy is required

The most important driver of prices this winter will be the weather – a mild winter in the northern hemisphere would go some way to calming prices, as would higher levels of wind output which would reduce demand for gas in the electricity sector. Approval of the Nord Stream 2 pipeline could also see increased flows from Russia (although the amounts are a matter of speculation), easing supply problems. However, another cold winter will see gas prices rising even higher, and combine this with low wind output and electricity prices will be worse.

One of the challenges for the gas market is the way in which it is lumped together with oil and coal by environmentalists, despite being significantly cleaner. As we move through the energy transition, it is important to maintain security of supply, and the current low wind conditions are highlighting the need for other forms of generation. Unless we invest in gas infrastructure, periods of high prices such as these will see gas being substituted with oil and coal – indeed, I have recently argued that in order to maintain security of supply in GB we should extend the lives of the remaining coal plant at least until the opening of Hinkley Point C.

“That’s the tragedy right now of the supply of gas being restrained by being lumped in with coal and oil by climate activists. The outcome will be that the climate curve is slower to turn, if you don’t have enough gas to replace coal. If this continues, the consequences will be felt in either unaffordable prices for energy or in energy insecurity in the forms of lack of availability,”

– Andy Calitz, Secretary-General of the International Gas Union

It’s important that policymakers and the public remember why they want to mitigate the effects of climate change in the first place. This is not some abstract objective, the point is that climate change threatens lives and livelihoods. However, lack of energy supplies does exactly the same, and we need to take care that in seeking to avoid long-term (theoretical in the sense that the mitigating actions may have no effect) adverse outcomes, we do not create the same adverse outcomes in the short-term. Cold homes in winter are absolutely linked with excess deaths, and high prices make heating and cooking unaffordable for many. If climate change is a social justice issue, so too should be poor energy policy decisions – policymakers and activists should take note.

Very thorough and well researched piece. Kwarteng seems to be ignoring the need to economise on gas to help keep bills down. I looked at futres closes yesterday. December NBP at 194p/therm is about £66/MWh, giving electricity at £132/MWh plus say 40% of UKA at £55/tonne CO2., for a total of £154/MWh. API2 coal was $168/tonne, or about £123/tonne, giving electricity at £53/MWh, plus £50/MWh for UKA, or 103/MWh. You only need primary school arithmetic to understand that by giving our remaining coal baseload contracts and cancelling UKA for the winter you could be saving £100/MWh on 5GW while freeing up 10GW of gas, and removing the expensive bids from the balancing mechanism from coal that cover for the costs of extensive warm up etc. That’s over £2bn over the winter.

I should have added a corollary that electricity prices significantly above gas generation cost indicate electricity capacity shortages, not gas shortages. I wonder what the National Grid Winter Outlook redraft will look like.

An excellent piece, thank you.

There seems to be a spreading realisation that the obsession with Climate has hopelessly distorted energy policy. Michael Pettis (@michaelxpettis), a China economist, writes about how financial distress costs include the distraction of employees from core tasks to try and firefight the cash crisis , or even to set up new jobs for themselves. I think Climate has had a similar effect on energy policy.

BTW I’m a fan of charts and was wondering what the software for the Sources of UK Gas graphic was? It’s very nice (though the numbers on the big pie chart only add to 92%).

Sorry, that’s a typo on the chart – pipeline imports are 30% – I’ll correct it in a bit. The software is Excel for the charts and I used Photoshop for the shaded bit and the text (hence the typo!), although it’s pretty easy to do in Powerpoint as well.

There are so many problems with climate policy as far as energy is concerned. Not understanding how energy markets work and how the policies will impact them is one. Lack of transparency about costs is another (and worse, pretending to consumers that bills have been going up because of supplier profiteering rather than the truth which is policy costs). Failing to understand the trade off between guaranteed near-term hardship and theoretical longer-term hardship (which may be somewhere else / might not be preventable).

The list goes on…

Typo also still in the text… 22 instead of 30.

Thanks…if was referencing the chart when I wrote the text. Fixed now.