I didn’t really go out on a limb in my last post when I predicted that energy markets would continue to make headlines this year – the last few days have seen a lot of people wondering what on earth is happening with gas prices as LNG diversions hit the news.

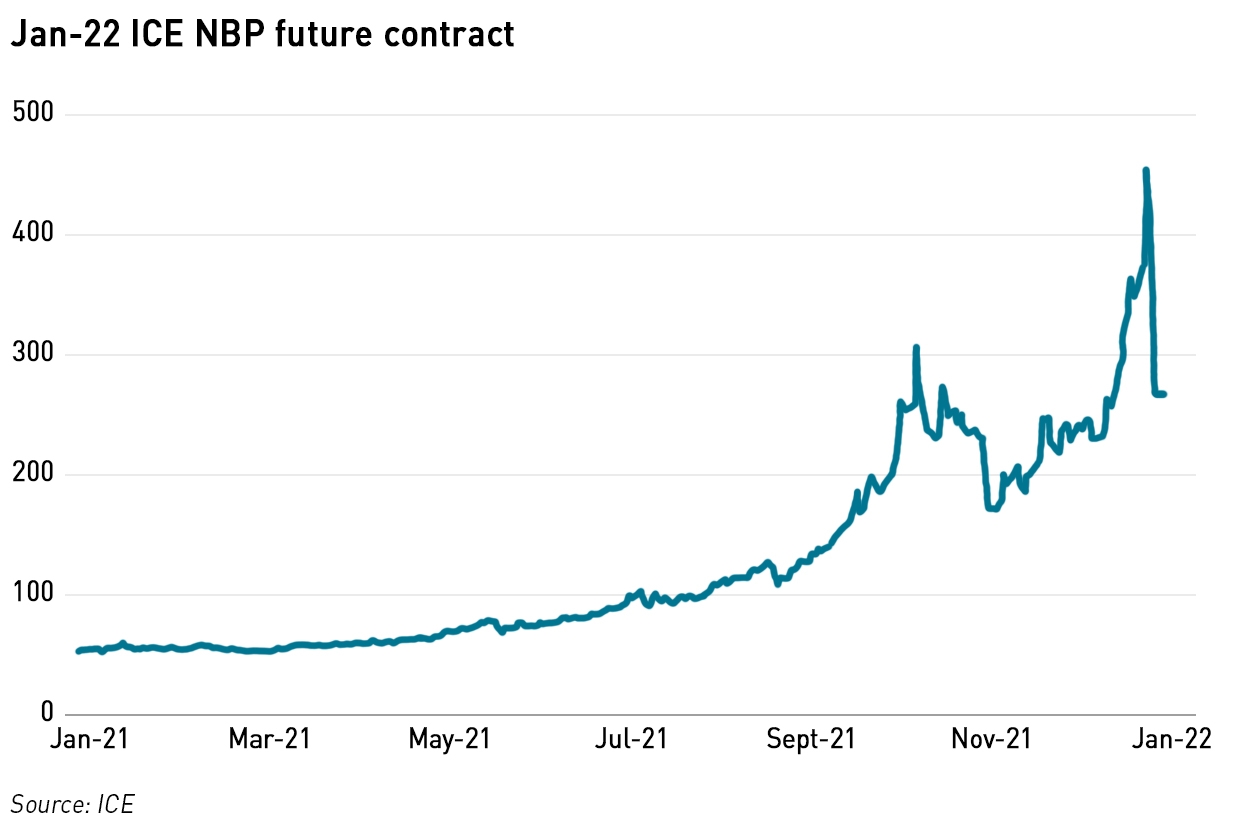

Gas prices have been on quite a journey this year, rising to record levels in the autumn, leading to Government support for the fertiliser industry when high gas prices brought the carbon dioxide supply chain to a halt. (A by-product of fertiliser manufacture is CO2, which is widely used in food supply chains, from powering the stun guns used in animal slaughter, to providing the dry ice used in food transportation, to carbonating fizzy drinks.) The run-up to Christmas saw gas prices soar, only to undergo a significant reversal. So what’s going on?

Prices had been ramping through December driven by cold weather in both Europe and Russia, and rapidly declining storage levels. NBP day ahead prices reached 440 p/th on 22 December before falling back to 254p/th on Christmas Eve. Nuclear outages in France, and low wind output across the Continent increased pressure as gas generators ramped up to fill the gap.

LNG heading towards Europe but poised to re-divert

Prices have since eased on the news that at least 15 LNG tankers are heading to Europe from the US, but with the weather turning milder this is not necessarily a definitive move – if European prices move below the Asian JKM market, those cargos could still re-divert back to Asia.

Some cargoes appear to have committed to Europe: one tanker, the 177,000 Bcm Marvel Crane, loaded at Cameron LNG in the US, and was originally heading for the Panama Canal before diverting across the Atlantic, with an expected delivery at South Hook on 30 December. It is now heading for Sagunto in Spain, and is expected on 8 January. The 174,096 Bcm Hellas Diana left the Corpus Christi liquefaction terminal in Texas in mid-November, headed for China, and is now in the Panama Canal, apparently heading for Europe. Similarly the 173,644 Bcm British Achiever left Freeport in the US in early December and was off the coast of Brazil when it re-directed to the Netherlands, and is now expected in Rotterdam on 10 January.

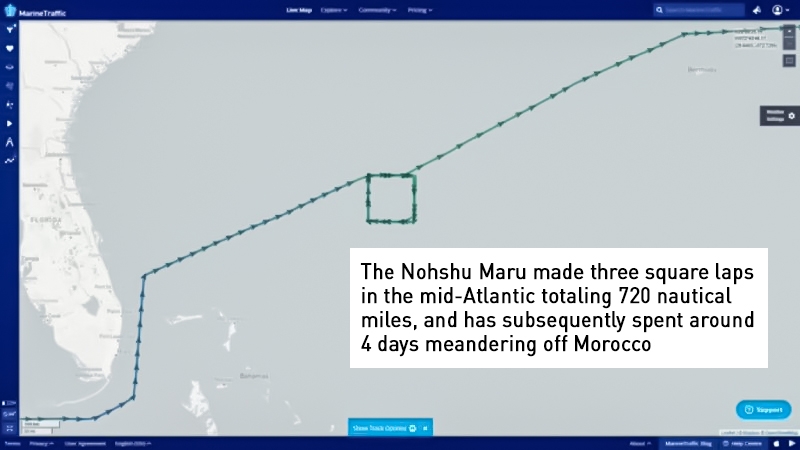

There are also two tankers in the eastern Mediterranean, the 173,400 Bcm Maran Gas Vergina and 174,000 Bcm Minerva Chios which both turned away from Asia and returned to Europe, but now seem poised to turn back to Asia. The 177,300 Bcm Noshu Maru left Ingleside in the US in mid-December with an initial destination of Japan. She diverted to the Atlantic, and then made three square “laps” before taking a position off Morocco where she has since remained. Her new official destination is Gibraltar, but given her current position, she could divert around Africa, avoiding Suez Canal fees, and head on to Asia.

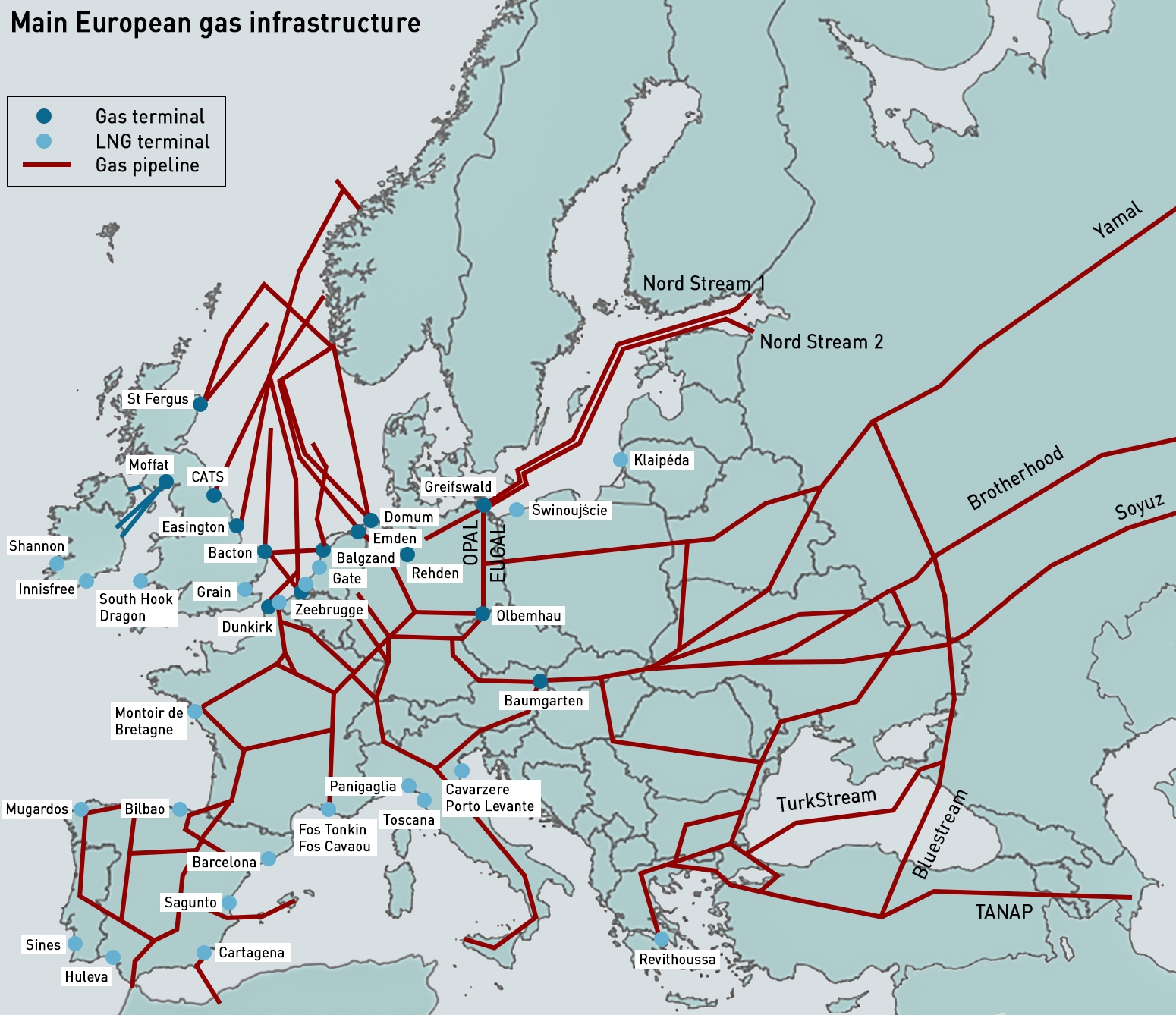

Meanwhile volumes of Russian gas into Europe have declined as the Yamal-Europe pipeline has seen reverse flows, with gas flowing from Germany to Poland at Mallnow. Similarly, nominations are down at the Velke Kapusany entry point on the Slovakian border with the Ukraine.

Some commentators believe that these reduced flows are further evidence of Russian political pressure aimed at securing approvals for Nord Stream 2 to open, but others point to Russia’s record levels of exports to Europe this year, and the cold weather in Russia last week. Russia certainly would like to see the Nord Stream 2 pipeline open for business, but it is unlikely that this would mean more gas coming into Europe – it would simply divert the transit route away from Ukraine.

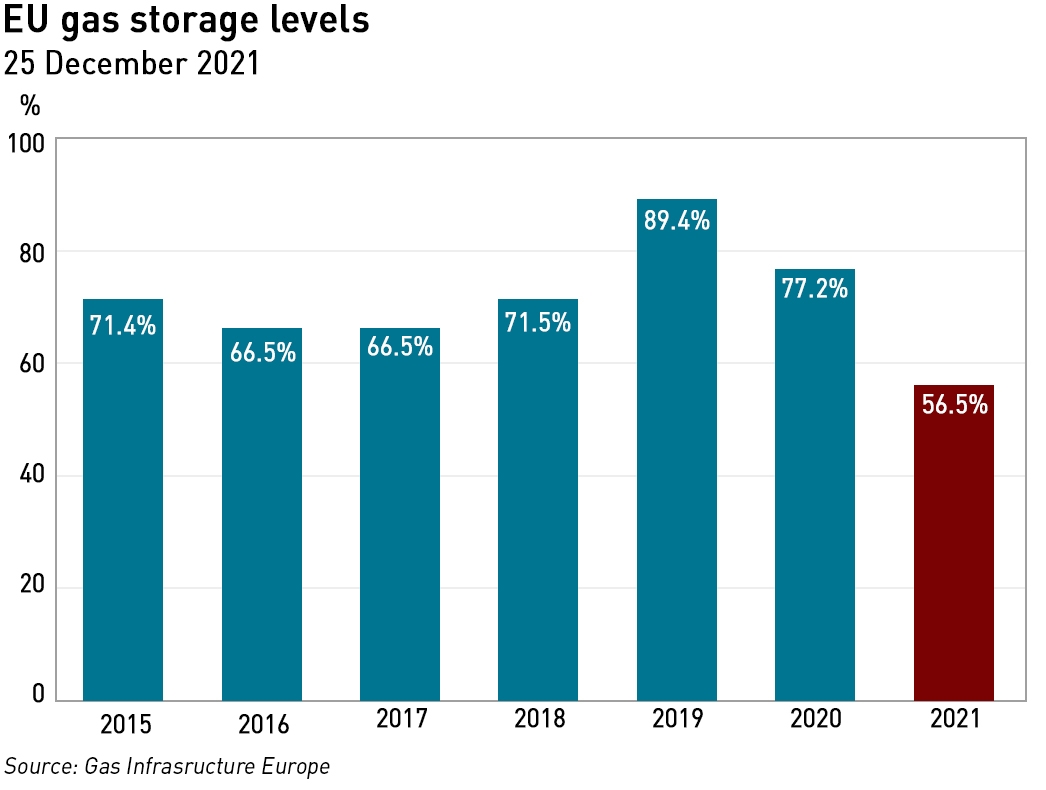

Gas storage levels are continuing to deplete, and are now at levels more typically seen at the end of January. Storage withdrawals are also not uniform, with some countries withdrawing at rates which are not sustainable. Much will depend on the weather in the coming weeks – if the weather continues to be mild and prices in Europe remain at current levels then currently un-committed LNG cargos may well re-divert to Asia, which will see prices shoot up again on the next cold spell.

Growing concerns over rising energy bills prompt talk of Government support

Concerns over surging prices prompted British energy companies to warn of disaster and urge the Government to intervene, with claims that energy bills might treble without intervention. Some suppliers are offering fixed price deals at close to £3,000 for the coming year. Calls for VAT relief on energy bills (something I have been proposing since September) are now more widespread, but are unlikely to be enough since VAT on energy is only rated at 5%.

“This has now moved from an energy supplier crisis to a cost of living crisis,”

– Martin Young, analyst at Investec

There is now talk of a £20 billion fund which would allow suppliers to avoid passing higher wholesale costs on to consumers in the short term. The idea is that suppliers would repay this loan over the next decade, slowly adding the costs on to energy bills so consumers see the impact over 10 years rather than immediately. While the idea of insulating consumers from this price shock is reasonable, I do not believe that this is the correct mechanism – suppliers should not have to subsidise consumers in this way. Any such fund should be in the form of a grant not a loan, with the Government recovering the costs through general taxation. A better approach in my view would be to remove green levies from energy bills.

“This is a national crisis. Wholesale gas and power prices have increased to unprecedented levels over the last three weeks, creating an extremely difficult operating environment for every business in the industry,”

– Nigel Pocklington, Chief Executive, Good Energy

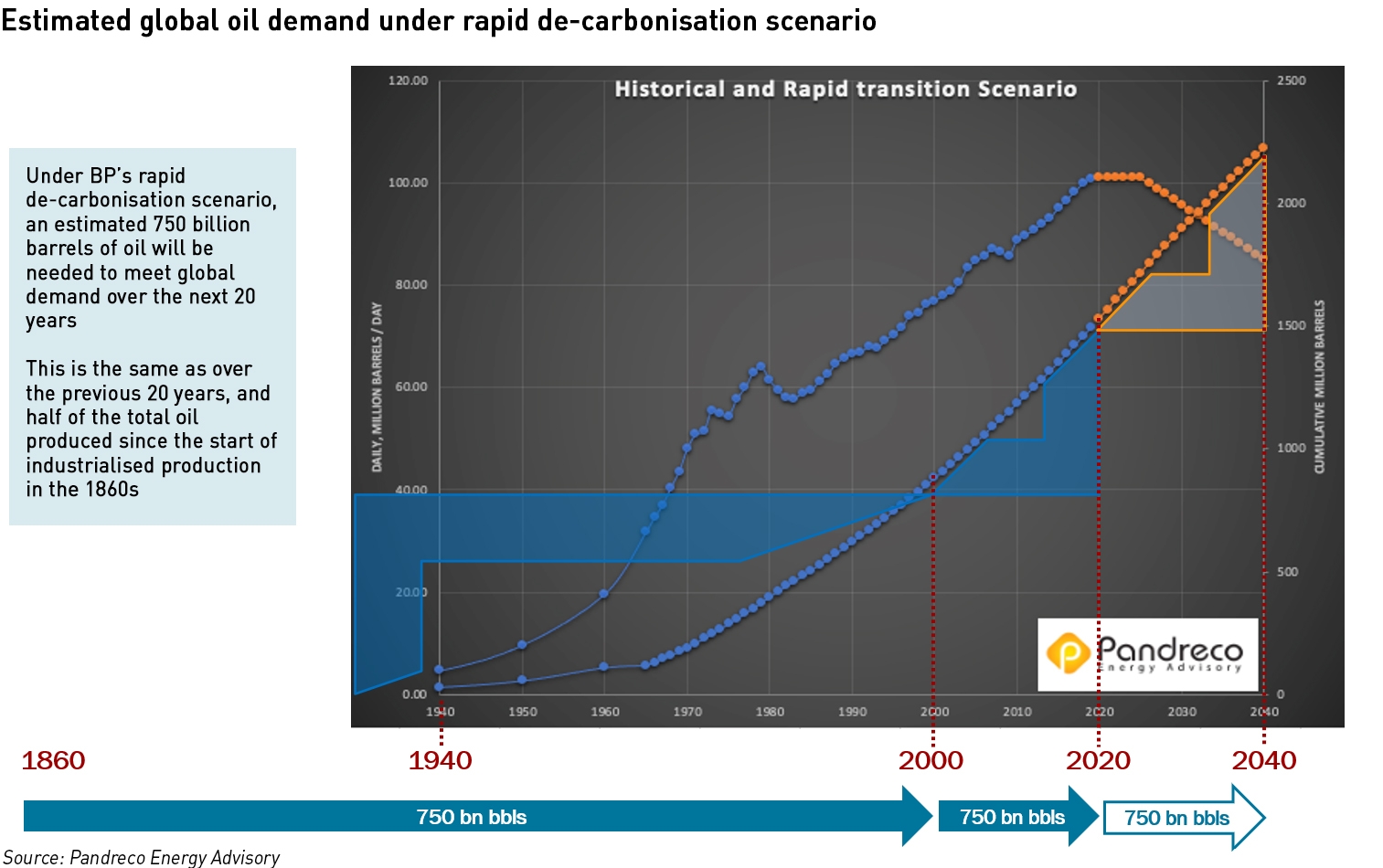

Calls for a windfall tax on North Sea production have also re-surfaced. I am much less keen on this idea. 2021 saw the lowest levels of oil and gas discoveries in 75 years, and while some may see this as good news, signalling a move away from fossil fuels, it is actually very bad news: analysis by Richard Norris of energy advisory firm, Pandreco highlighted that even on rapid de-carbonisation scenarios the global economy will require the same amount of oil over the next 20 years as was produced in the past 20 years – 750 billion barrels, so declining E&P activity will mean that oil and gas become more expensive, threatening economic output. High oil prices correlate with economic recessions.

There is a temptation to respond to the current crisis in gas markets by asserting that this makes a transition away from fossil fuels more pressing. But this is not the correct conclusion to draw from the crisis – bull runs in commodities markets occur when supply does not keep pace with demand, for whatever reason. That this is currently happening in gas is to a certain extent irrelevant – it can happen in any commodities market including any energy source which replaces gas in the future. The correct lesson isn’t that we need to transition away from gas, but that we need to give more thought to strategic energy supplies and whether and how consumers should be insulated from the effects of these supply and demand imbalances when they arise.

In the past, governments created strategic oil reserves in order to insulate themselves from the effects of oil shocks, but as those shocks became less of a political issue, these reserves were seen as a source of cash and monetised. There is always a temptation to view insurance as an expensive luxury at times when it isn’t needed, but no-one enjoys the consequences of being un-insured. The question really is whether the cost of the required insurance is justified by the cost of being un-insured.

For example, for most people mobile phone insurance offers poor value – you do not need to have avoided a claim for very many years before the amount spent on insurance exceeds the cost of a new phone. In this case being insured makes little sense unless you habitually lose or damage phones, or would find a sudden replacement unaffordable. With energy insurance, there is also the political dimension which is the equivalent of whether it is socially acceptable for people to have to replace their phones at short notice, particularly when phone costs might have multiplied at the exact time the replacements are needed.

That is a complex calculation, and not one I’m able to make, but the issues for the Government are:

- What if anything should be done in the short term to alleviate the impact on consumers of energy price rises, and my feeling is that something does need to be done since the combined impact of higher energy costs, higher taxes and higher inflation is going to make life difficult for a large number of people;

- What if anything should be done in the longer term to minimise the impact of energy price shocks, and here there needs to be a discussion about security of supply and to what extent we can or should invest in over-capacity or enter into long-term contracts which could look expensive when prices fall.

What I am sure of is that this is not and should never have been a retail market crisis. The crisis in the retail market is purely a result of a policy choice: the retail price cap. If suppliers were able to pass on the wholesale cost of energy, there would have been minimal impact on suppliers – of course some badly run suppliers might have still collapsed, but I reject the suggestion that half of the companies in the market were badly run (and if they were then Ofgem has a lot to answer for).

So I renew my calls for the price cap to be scrapped, for VAT relief to be granted on domestic energy bills, and for green levies to be removed from energy bills altogether. This last move may well offset the effect of rising wholesale prices removing the need for a stabilisation fund. The Government is currently consulting on the future of the retail energy market – this time it needs to listen.

UK Nat Gas nearly half the price it was before Xmas today albeit still 2.43p so still up five fold on recent average price so no respite but its clearly a very fickle world when someone can afford to have a tanker load of gas just plying the oceans waiting for the jackpot to arrive somewhere in the world. Also its not going to help the situation if these tankers are just circulating around waiting for the jackpot the longer they stay at sea the less gas will be injected into countries storage over the weeks ahead. The world needs to wake up and realise that cost effective gas is an essential input to allow teh production of infrastructure to achieve net zero.

On domestic energy if we pay what it costs we might think twice about how much we use. My thermometer has been dropped from 21 to 20 this year no ones been moaning about it being too cold. My grandparents had one heated room this time of the year and you slept under a weight of blankets at night time. Not saying we want to go too far backwards but perhaps people should look at what they use.

I think the problem is that many people on low incomes cannot afford heating at all – thousands of people die each winter from under-heated homes in the UK. So while I agree – there is certainly a need for middle-class culture change – we all know people who like to swan about in shorts and bare feet in winter and just turn up the thermostat – that is not the reality for people on low incomes.

20 degrees is still pretty high for heating…we have ours set to 18.5 most of the time and don’t heat bedrooms at all unless they are being used by my sons for studying. There is also poor understanding about the costs of heating – I was speaking to someone recently with an electric under-floor system who ran theirs at 22 degrees and wondered why their bills were so high!

The other problem people forget about is damp – damp homes always feel colder than dry ones, and again, people on low incomes are more likely to also have damp homes.

The reality you describe exceeds my wildest dreams. How as a country have we become involved in such an exciting game. Perhaps with smart meter developments we can all play and as individuals bid minute for minute for our electricity supply. Perhaps with the much quoted (and strangely undefined) digital and data driven future for a modernised electricity system we could know the postcodes of those we are out- bidding. A game not just about money but about survival. A basic level of government support may well be necessary for the losers.

Unfortunately the question is how close will the future be to this dream.

Some places actually do have this – uncapped market-indexed time-of-use tariffs. It’s one of the reasons I really want to see banking-style regulation in energy – so that only people who really understand the risks can play those games.