Legend has it that when a great fire broke out in Rome in 64 AD, Emperor Nero played music (unlikely to be an actual fiddle since those were not invented until the 11th century). The moral of the story is that Nero was both an ineffectual leader and indifferent to the suffering of his people. It is tempting to cast Ofgem as a modern-day Nero, fiddling with the retail price cap while suppliers collapse into bankruptcy all around them.

The tinkering in question emerged on Friday, when the regulator launched five separate consultations on the price cap:

- Consultation on the potential impact of increased wholesale volatility on the default tariff cap

- Consultation on the process for updating the default tariff cap methodology and setting maximum charges

- Consultation on the true-up process for COVID-19 costs

- Consultation on reflecting prepayment End User Categories in the default tariff cap

- Consultation on Energy Company Obligation scheme allowance methodology in the default tariff cap

Reponses are being sought by 17 December, with any changes to take effect in the next cap period beginning on 1 April 2022.

However, this has been eclipsed by the news that Bulb Energy has become the 26th and by far the largest supplier to fail this year, and will enter special administration imminently.

Consultation on the potential impact of increased wholesale volatility on the default tariff cap

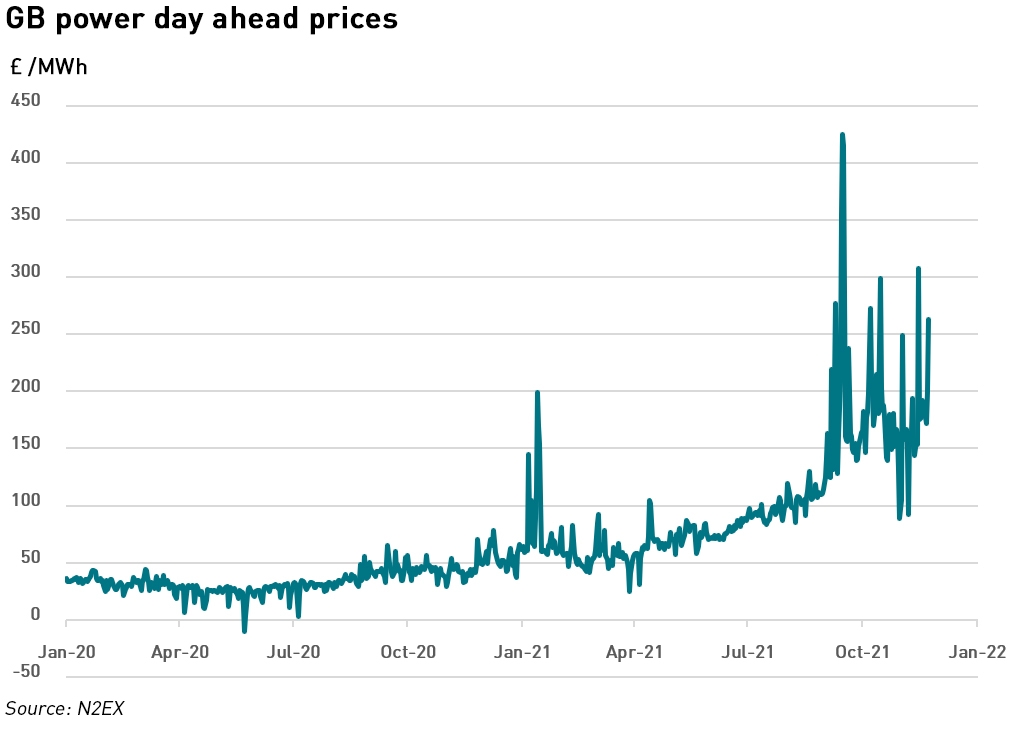

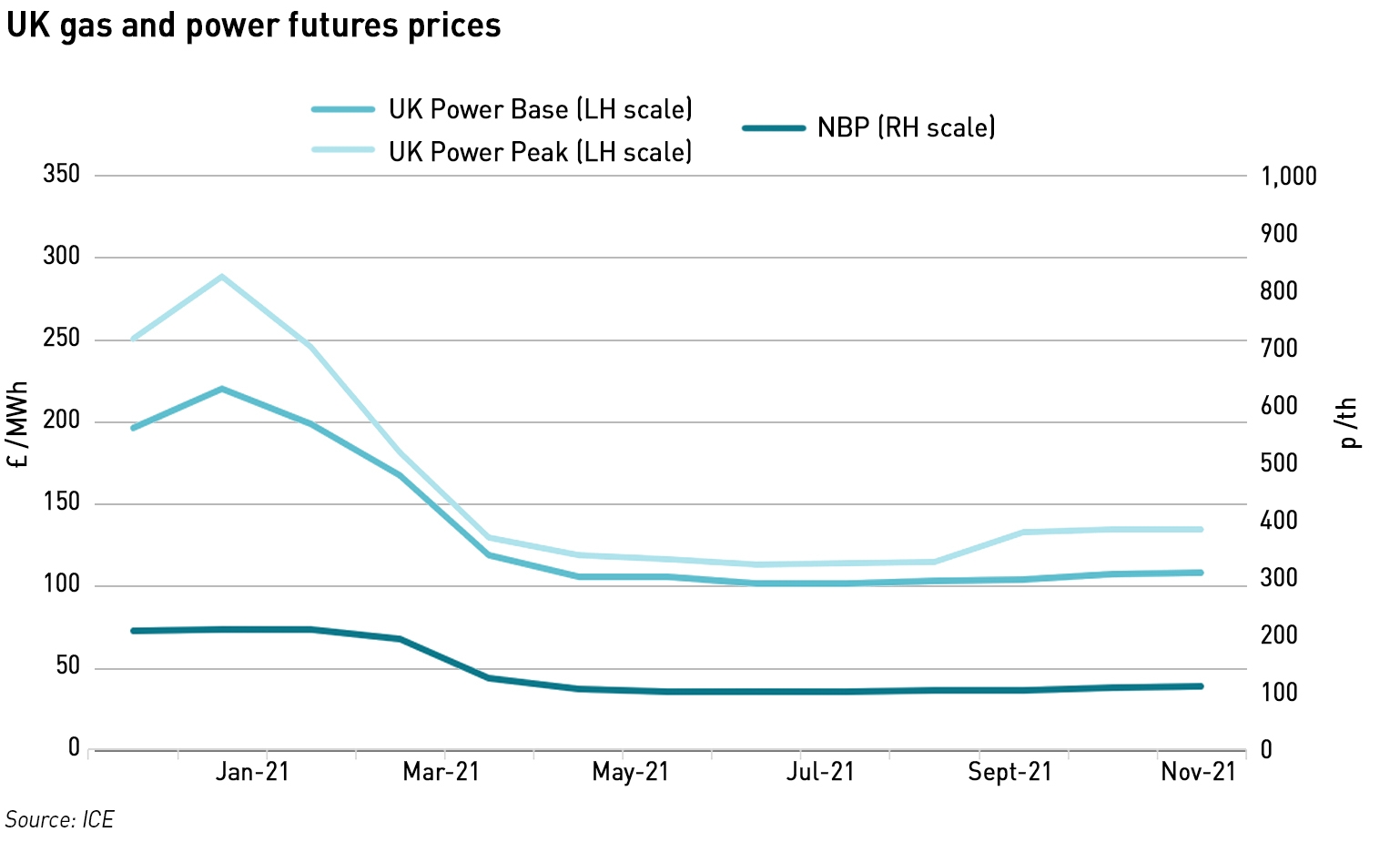

Clearly the main issue with the price cap is the pace at which wholesale prices have risen since the last re-determination, forcing 26 suppliers out of the market since the beginning of the year, the latest being Neon Reef and Social Energy Supply which both ceased trading on 16 November, and now Bulb, the seventh largest supplier, which annouced it would enter special administration yesterday. Bulb’s collapse has been described as the largest supplier failure since the demise of TXU Energy almost 20 years ago.

“The scale and pace of the rising wholesale prices observed in recent months is unparalleled in the GB energy market. The additional costs and uncertainties facing suppliers are likely to be beyond what is accounted for in the cap in the existing methodology,”

– Ofgem

Ofgem considers the main reasons that the current cap methodology are failing to be properly cost-reflective are:

Shaping and imbalance costs: the costs of refining hedging positions when converting from less granular forward contracts to more granular products closer to delivery, and the costs of imbalance are likely to be higher in current market conditions; and

Unexpected SVT demand: it was never envisaged that the capped default tariffs would be the cheapest in the market, so suppliers are seeing a much large number of customers on their standard variable tariffs (“SVTs”) – with more being added each month as fixed price contracts end – which represents a material deviation from their reasonable expectations when implementing their forward hedging strategies.

The existing cap methodology assumes that shaping and imbalance costs will represent the same proportion of direct fuel costs in any given cap period, and that suppliers can forecast the number of customers that will be on the standard variable tariff, so they broadly know how much energy to buy. The past year has seen significant increases in wholesale prices, particularly at shorter timeframes, with significant spikes in imbalance prices. Smaller suppliers are disproportionately exposed to imbalance prices due to limitations on being able to hedge their shape risk (due to the small volumes they need to trade).

Another potential additional cost to suppliers arises from the shape of the forward curve which is strongly backwardated (meaning shorter-term contracts have higher prices than longer-term contracts). Prudent hedging strategies would see suppliers increasing the proportion of their expected demand that is hedged as they get closer to delivery, but in backwardated markets this becomes more expensive (this strategy is considered prudent due to volume uncertainty). The current cap methodology assumes the costs associated with the shape of the forward curve, whether in backwardation or contango, will net out to zero over time…this may be the case, but it ignores the impact of significant changes in the shape of the curve within cap periods.

Off-setting these effects is the cost of the CfD levy which is inversely proportional to wholesale prices: when wholesale prices rise, the CfD levy falls.

Ofgem says it intends to bring forward wider-ranging changes to the cap methodology, but in the meantime, it is minded to increase the wholesale additional risk allowance.

Consultation on the process for updating the default tariff cap methodology and setting maximum charges

While the Domestic Gas and Electricity (Tariff Cap) Act 2018 places no limit on the frequency with which the price cap can be adjusted (other than that it must be reviewed at least every six months), Ofgem constrained itself by introducing fixed six month review periods into gas and electricity supply licences. In this consultation, the regulator is seeking to amend these licences in order to enable it to update the cap more frequently, in special circumstances which it considers would be “rare and would have high impacts without urgent action”.

The tests for these conditions being met are:

Rare: how foreseeable it may have been for suppliers to identify the event as a risk and have actively managed it, which takes account of the scale of the event relative to historical levels. This which would include the recent rise in wholesale gas prices;

High impact without urgent action: whether the event leads or may potentially lead to irreversible effects on the energy market or could have systemic consequences, for example the risk of significant market exit by efficient suppliers. Also, events where there are concerningly large impacts on customers, particularly those in vulnerable situations. The required materiality for a “within-period” cap level adjustment would be larger than that required for a normal adjustment for a forthcoming cap period.

Any “within-period” adjustment would only apply for the remainder of the period and not be retrospective.

Of course, this amendment to supply licences is necessary, but the real question is why Ofgem did not envisage a situation where more frequent revisions might be necessary and place this sort of limit on its powers in the first place. Ofgem has the statutory powers to change the cap as often as it wants, but it deliberately limited itself when it amended supply licences to require suppliers to abide by the cap. While frequent changes to the cap level would be un-desirable, introducing greater uncertainty to suppliers in managing their businesses, no supplier would prefer the certainty of a loss-making situation in the current market conditions. By restricting itself in this way, Ofgem has made it difficult for the statutory objectives of the cap to be met, and is therefore failing in its legal duties.

Consultation on the true-up process for COVID-19 costs

In February Ofgem introduced an adjustment in the cap to account for the estimated additional bad debt costs as a result of covid. This initial estimate, referred to as a “float” was intended to be adjusted with a true-up once the final costs are fully known. This consultation sets out Ofgem’s proposals regarding this true-up.

Ofgem is proposing to implement a cumulative bad debt charge approach to calculate any additional covid-related bad debt costs and is seeking information from market participants in order to determine the extent of these costs:

- Ofgem proposes to calculate the increment relative to the same months before covid, using data from October 2018 to March 2019 for the winter baseline and April to September 2019 for the summer baseline;

- Data would be gathered on payment type and tariff type;

- The first true-up in cap period nine (October 2022- March 2023) would consider the bad debt charge costs for cap periods four, five and six (April 2020 – September 2021) which will be treated as the main cap periods affected by covid;

- Ofgem also proposes to gather bad debt charge data for twelve months after these periods, to account for any provision movements, which means gathering bad debt charge data on cap periods seven and eight (October 2021-September 2022).

Ofgem proposes using a cumulative bad debt charge approach for determining the amount of additional bad debt costs. This involves comparing suppliers’ bad debt provisions, and changes to the bad debt provisions during all periods impacted by covid, with the baselines. Ofgem will also collect data on the administrative costs and working capital costs associated with these additional bad debts, which were not included in the float, but which should be recoverable by suppliers.

Consultation on reflecting prepayment End User Categories in the default tariff cap

End User Categories (“EUCs”) categorise gas customers by different usage patterns and payment type. When the cap methodology was developed in 2018, there was only one EUC relevant to the cap, but since then a unique EUC has been created for domestic prepayment meter customers. This new EUC has an impact on both the wholesale cost and network cost components of the cap, which Ofgem considers significant enough to warrant an adjustment to the cap methodology for these customers.

Consultation on Energy Company Obligation scheme allowance methodology in the default tariff cap

The Energy Company Obligation (“ECO”) is an energy efficiency scheme that places legal obligations on larger energy suppliers (ie those with 150,000 or more domestic customers, and an annual supply of electricity of 300 GWh, and gas of 700 GWh) to deliver energy efficiency measures to domestic premises to help reduce carbon emissions and tackle fuel poverty. The scheme began in April 2013, and has been amended a number of times. The latest version of the policy, ECO3, began on 3 December 2018, and is due to end on 31 March 2022. The Government has indicated its intention to legislate for ECO4 with a view to its commencement on 1 April 2022.

Ofgem proposes to use the latest figures from BEIS in determining the relevant costs of ECO4 for the next cap period – the draft legislation has yet to be published, but as the costs are material, Ofgem will need to use an estimate based on BEIS forecasts for inclusion in the cap. Any mis-alignment that emerges once the legislation is finalised will be recovered through subsequent cap adjustments.

What next for Bulb Energy?

Over 3.7 million households have now seen their supplier go bust this year, with the largest of these, Bulb, exiting the market yesterday. Bulb’s size means that instead of entering the Supplier of Last Resort (“SOLR”) process, a special administrator will be appointed, as set out in the Energy Act 2011. In common with many of the other failed suppliers, Bulb attributes its closure to the combination of high wholesale prices and the price cap which is preventing suppliers from recovering these higher input costs from consumers.

Bulb has been teetering on the brink of bankruptcy for some time. According to Sky News, the process had been delayed by Sequoia Economic Infrastructure Income Fund, which has an outstanding secured loan of around £50 million to Bulb’s parent company Simple Energy (which will also enter administration) – apparently the Fund had demanded the repayment of the loan prior to Bulb being placed into administration, a clearly unrealistic prospect.

Bulb has been seeking finance and/or a sale for the past few months, with various parties including Octopus Energy, Ovo Energy, Shell Energy Retail and Centrica, expressing varying degrees of interest, although some believe the interest was a pretext for getting access to the data room for market intelligence purposes rather than being indicative of any genuine intent to buy the company.

The special administration process for energy companies

The process for appointing a special administrator was set out in the Energy Act 2004 (as it applies by virtue of the Energy Act 2011), and allows the Secretary of State or Ofgem to apply to the courts for an energy supply company administration order, if statutory tests for insolvency are met.

The energy administrator is required to continue to supply gas and electricity to the failed supplier’s customers until the company is rescued, sold, or its supply activities transferred to other suppliers. The administrator is required to conclude the process as quickly and effectively as reasonably practicable.

The Act allows the Government to provide grants and/or loans to finance the company’s activities in administration – there are provisions for these costs to be recovered either from the company, or, if that is not possible, through an industry levy. Taxpayers should not ultimately foot the bill for energy supply company administration, although any attempt to impose additional costs on suppliers particularly on top of the record RO mutualisations this year, will be difficult for the market to absorb.

As most of its consumers are currently loss-making, it is not in anyone’s interests to take on the customer book until market conditions improve, which means it is likely to remain in administration for some time, being essentially propped up by the state. According to the FT, one Government figure has accepted that taxpayers will end up having to pay hundreds of millions of pounds to support Bulb through the administration process and beyond, covering the gap between the high wholesale prices and the price cap.

Industry observers have long questioned how Bulb could afford to offer some of its tariffs – it had previously claimed that its variable tariff was 18% cheaper than those offered by the Big 6, but its last available accounts for the year to 31 March 2020 showed the company made losses of £63 million and had a £55 million loan facility due for repayment on 31 December this year. The company attracted criticism last month when it made significant increases to the direct debit payments it collected from customers, with some increases being as much as 80%. At the time Bulb denied it was treating its customers as a bank, but it’s hard to avoid the conclusion that this was a last ditch attempt to finance itself through the current market crisis.

Bulb had been popular with consumers, generally offering good customer service and 100% renewable electricity tariffs and 100% carbon-neutral gas tariffs – although such claims are now under investigation for greenwashing, since many consumers believe these relate to 100% of the energy they receive at all times of the day, every day of the year, which is not currently possible.

The proposed changes to the price cap are too little, too late

The five price cap consultations issued by Ofgem on Friday give the appearance that the regulator is busy working to address the crisis facing the market, but not only is much of this “busywork” (there is an impressive amount of duplication in the pages and pages these consultations run to), there is little of substance, and some of the problems it is trying to solve are self-inflicted.

“When the country’s seventh-largest supplier fails, serious questions must be asked about the state of the market and how it’s regulated,”

– Gillian Cooper, head of energy policy for Citizens Advice

It is astonishing that Ofgem chose to place limits on its powers to amend the price cap by restricting itself to six-monthly cap periods when it adjusted the gas and electricity supply licences in order to impose the obligation to abide by the cap on suppliers. This was incredibly short-sighted, and reflects the assumption, admitted recently by former Ofgem head, Dermot Nolan, that they had simply never envisaged a situation where the default tariffs were the cheapest in the market, or, presumably that they would become loss-making within a cap period.

“The much bigger issue for customers is that when the current price cap period ends, these companies are going to have to get back the money they are now losing. You can’t expect companies to carry on supplying customers at a loss. Large well-financed companies who have picked up customers through supplier of last resort may well be losing money on every single one… It takes Ofgem so long to set it that it never runs with the market. You can have a situation where prices fall and suppliers are making too much money or, like now, we have higher prices than Ofgem foresaw,”

– Lisa Waters, founder of Waters Wye energy consultancy

While the Government continues to blame suppliers for the large number of failures, it needs to take responsibility for the incompetence of the regulator. Whether Ofgem is genuinely inept, or simply carries out what it believes are the Government’s preferences, the reality is that half of the suppliers that were serving the domestic market at the start of the year have now failed. Whether those failures are the result of poor management or not, that Ofgem has presided over a market where half of the suppliers have failed in under a year must also be considered a regulatory failure, and a failure of proper oversight by BEIS.

Industry confidence in Ofgem has evaporated, and few in the market believe the regulator has the capability to provide appropriate oversight to the market. My preference is for retail energy regulation to be moved to the Financial Conduct Authority, which would allow for a fresh perspective with oversight from the Treasury rather than the struggling BEIS. Whether the Government has the vision to attempt such a change remains to be seen, but perhaps the millions that will now be flowing out from the Treasury to support the special administration of Bulb will concentrate some minds. We can only hope…

The recent collapse of Bulb has highlighted the inappropriate nature of the price cap. [NB: anybody who knows how to use a Search Engine to check on Bulb knew this was coming] As a tax payer I seem to continue to be required to support lost causes. Now it turns out I’ll be indirectly subsidising my Bulb neighbours who will continue to receive tariffs at [usually] below cost. All because of the Government’s response and the large BULB customer base.

What the whole industry has learnt from this debacle is that the Price Cap is not appropriate way to regulate the market. Period.

It’s almost as though Ofgem is trying to justify their own existence, but are doing so in the worst possible and ineffective way.

Give me strength.

It is utter shambles and whilst im peeved about Bulb consumers benefitting from taxpayer support, whilst my unit rate for gas and leccy has gone up 40% since my fixed term ended, this is a total failure of regulation and as usual in our society no one will be held accountable for it and best we will be see is “lessons will be learnt” – yeah right.

I’m not sure that Bulb’s customers will receve taxpayer support – that will depend on whether the special administrator honours existing cheap tariffs or puts them onto the SVR as a SOLR would. It’s lose-lose for the special administrator – honour cheap tariffs and it will be seen as subsidising those customers but more them to SVR and it will be seen as profiting at their expense….

It is a regulatory failure but I doubt lessons will be learned.

Mutualisation is really a loss for those who opted to pay a premium to a well capitalised supplier who wasn’t sailing close to the wind of bankruptcy by buying market share at loss making prices. They get to pay twice over.

That’s true. It’s also part of the reason taxpayers rather than bill-payers should pick up the bill for the special administrator since many low income and vulnerable households don’t pay income tax.

I think the burden should partly fall on the customers who benefitted from aggressive under-pricing, as well as on lenders and financers who enabled it, who should rank last among creditors.

I agree, but that undermines the Government’s entire thinking on competition which is that competition = more suppliers = cheaper prices = consumer switching = effective competition. The Government wants people to switch and is looking at forced switching of “inactive” consumers onto cheaper tariffs…the current situation ought to make it think twice but who knows. The people who really should carry the can are the shareholders and lenders, and of course Ofgem and the Government for poor market design.

The cap is of course a cap, or call option, which has a cost that is a function of the relationship between market prices and the strike price or cap level, the duration of the option, and the degree of market price volatility over the period until it expires. When it was set, it was not all that far out of the money, which is one reason why it is now so painful: the six month duration and energy policy have contrived to make it very expensive. Hedging a cap is a dynamic process unless you buy the cap in the market and your counterparties perform against it. It requires the purchase of more and more fixed price hedges the higher that prices go, adding to market demand in a self fuelling process that drives prices higher, until substantially all the volume is covered by these hedges. Then demand subsides, and coat tail speculators seek to take profits and sell. That starts to drive prices lower, in turn resulting in sales by cap hedgers. Whipsaw volatility adds to the hedging cost as hedging happens in the rear view mirror. Market capacity to supply the hedge trades is limited.

If we look back to the post Fukushima period of high gas prices we find that the extent of the problem was limited by a combination of switching, primarily to coal, and by strong market incentives to increase gas supply with governments being keen to make that happen for the benefit of their own countries. Nevertheless gas prices were extremely volatile and reached levels that were uncomfortable, particularly in Asia on the back of Japanese switching from nuclear.

Now we see efforts to restrict gas and coal supply by Western governments, ranging from disallowing and delaying new development through closing coal capacity and refusing to use it and taxing it heavily. Net zero policy is aggravating the problem. In the UK most of our LNG supply is essentially unhedged spot purchase. Even where there are fixed contracts in place it has made more money to divert volumes to Asia: China appears to be quite happy to cause high energy prices in the West while it benefits from its extensive reliance upon much cheaper coal. Secure pipeline supply has also been hit by the pandemic maintenance backlog. Nuclear capacity continues to atrophy, reducing the pool of forward producer hedge sales. Renewables on CFDs do provide some natural hedge to the market, but the baseload CFDs for Drax etc. are insensitive, being set a quarter at a time and offering no real cover against intraday volatility at times of peak demand. Renewables on ROCs have been making out like bandits: there really is a case for a windfall tax or compulsion for forward sales on these generators.

Dealing with the situation requires root and branch reform, starting with suspending injurious net zero policies. Biden’s SPR sale is capitulation, creating a weakened position instead of investing in more fossil fuel production.

I have long argued that price insurance (fixes, caps and collars etc.) should be provided entirely separately from energy supply. That would ensure that it was priced appropriately by professionals, not amateurs with no understanding of markets in OFGEM, or startup suppliers, and would entail providing customers with a proper guide to potential pitfalls. The operational within month balancing hedging should be conducted by well capitalised businesses with the relevant expertise. Smaller suppliers should be required to secure their services as a condition of licence. Basic market pricing should align with the monthly cycle of futures markets.

Do OFGEM understand what they have created? Do they need consultations to find out? They are living in a past world when electricity supply was stable and boring, which is what engineers like(and perhaps the majority of consumers). We are entering a world of ‘consumer engagement’ and an exciting computer game with lots of action with serious financial and climate change implications. .

“rare and would have high impacts without urgent action”. In this exciting game rare events historically will become frequent. With resilience decreasing both in the technical operation of the grid and over reliance on one energy source high impact events are more likely.

Are OFGEM acting for the consumer or peddling a narrow economic model?

You mention green-washing. People are being hoodwinked. 100% renewable energy claims are a little nebulous (although believed) but OVO claims specifically to supply 100% renewable power- I hope they can prove this.