Current high gas prices combined with a period of low wind output in September have re-awakened concern about security of supply, including among the general public – today my doctor asked me if he was going to be able to charge his car when needed this winter! Business Secretary Kwasi Kwarteng has been forced to repeatedly reassure the public that gas supplies will not run out:

But can we be reassured or is security of supply in the energy market genuinely at risk for the first time since the 1970s?

European gas storage facilities filling but much depends on the weather

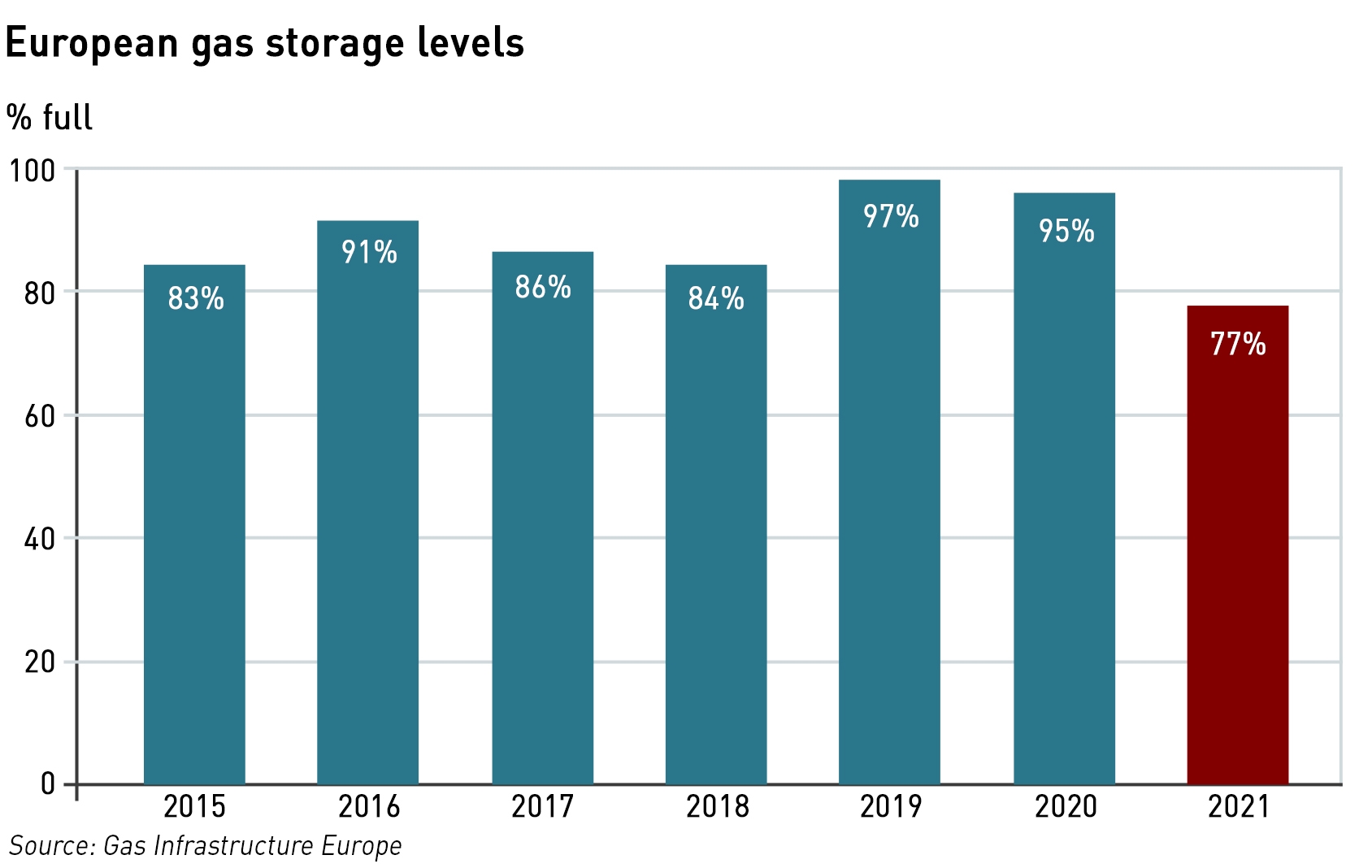

European gas inventories are slowly recovering from a low of just under 30% in mid-April to 77% in mid-October. While the April levels were some way above previous lows, typically summer injections would have been higher, and inventories remain below historic norms for the time of year.

The question is whether there will be enough gas to meet demand this winter. This depends on a number of factors: pipeline flows from Russia, European production, LNG imports and demand levels. National Grid’s Winter Outlook for gas sees margins more or less the same as last year, with lower demand for electricity generation due to the development of more renewable generation.

“If low volumes of LNG are delivered to the UK this winter, then we would expect the shortfall against demand to be made up from imports through the European interconnectors and domestic storage, as was observed last winter,”

– National Grid Gas Winter Outlook

However, this analysis might be optimistic. My feeling is that the electricity market outlook is itself on the optimistic side, with the potential for more gas-fired generation in times of low wind conditions and, in particular, lower nuclear availability (see below). A cold winter, with cold, still weather at the end of winter similar to what was seen earlier this year, could challenge National Grid’s assumptions. According to analysis by Wood Mackenzie, weather dynamics will be key to gas security, not just in Europe, but also in Asia and Russia, with supplies from Russia effectively balancing the market (to the extent that is possible).

Under normal winter weather conditions across the northern hemisphere, Europe should not have issues in meeting gas demand. While storage levels may only reach 78% of capacity (87 bcm) by the end of October, a record low, and LNG imports limited due to strong Asian demand, a rebound in UK and Norwegian production, together with stronger exports from Algeria and Azerbaijan, will increase winter pipeline supply compared with the summer. High gas prices are also driving fuel switching from gas to coal and oil in electricity generation, and curtailing some energy-intensive industrial demand.

Assuming Russia uses all of its existing pipeline capacity, including Nord Stream 1, Yamal-Europe, TurkStream and the routes through Ukraine up to the ship-or-pay contractual levels, Europe will need around 58 bcm of gas from its inventories to meet demand. This would leave around 29 bcm of gas in storage by the end of March, below the 5-year average but comfortably above historic lows. Therefore under normal weather conditions, security of supply would be assured and gas prices would begin to ease by the end of the winter.

However, a cold winter in both Europe and Asia could mean there is insufficient gas available to meet demand, unless more gas can be shipped from Russia. Cold weather could boost heating demand in Europe up to 20 bcm, while a cold Asian winter could add up to 10.5 bcm of LNG demand across China, Japan, South Korea and Taiwan, diverting those volumes away from Europe. There would be a risk that all the gas in European storage would be consumed, leaving Europe wholly dependent on higher flows from Russian, above existing pipeline capacity, clearly threatening security of supply.

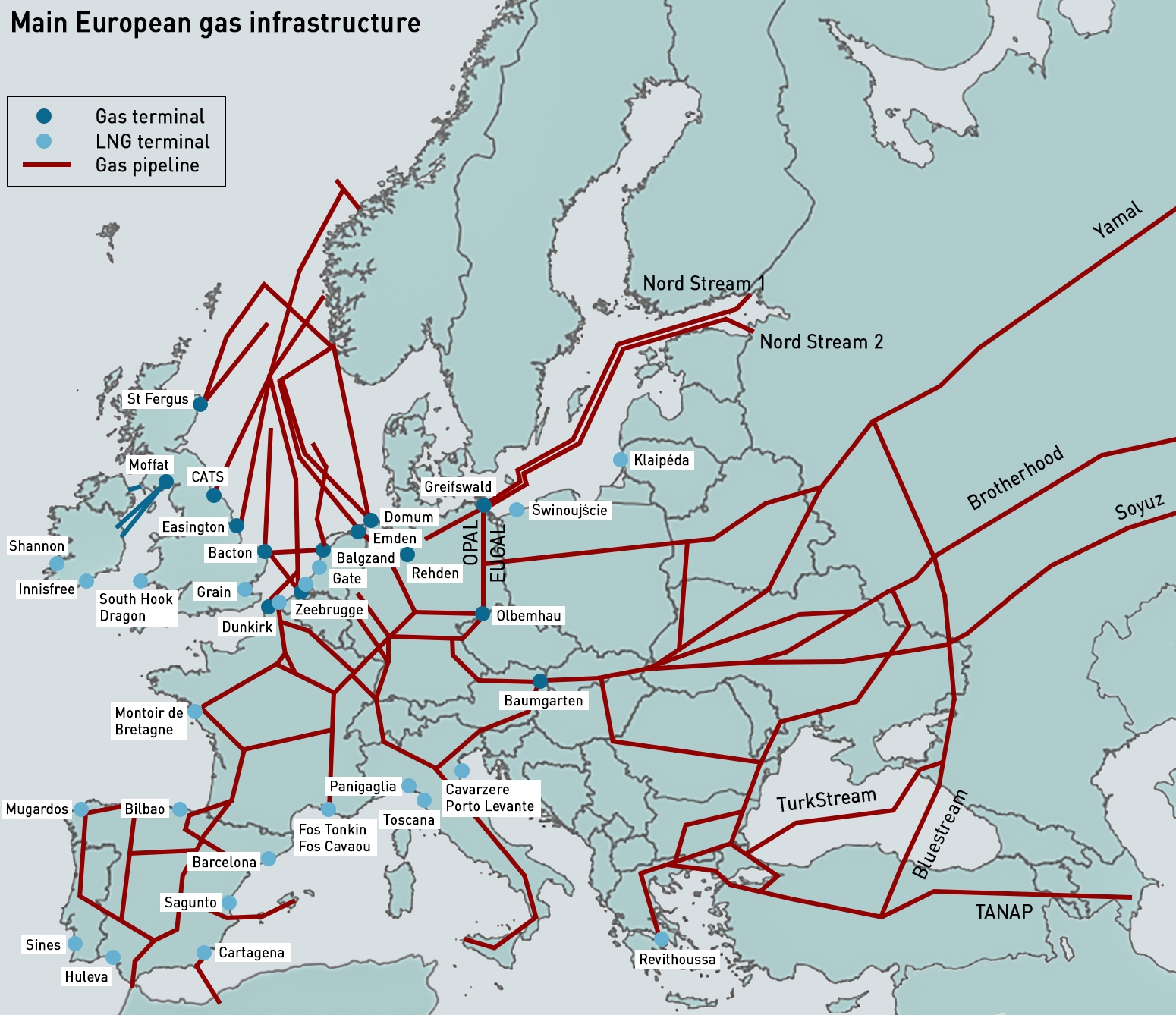

Analysis from the Oxford Institute for Energy Studies (“OIES”) in 2018 indicated that existing pipeline capacity (ie excluding Nord Stream 2 and TurkStream) was highly utilised with little space capacity at peak times. Since then Gazprom has changed its approach to shipping logistics, reducing its volumes through the Ukraine and using the Yamal pipeline through Belarus as the swing route. Its contract with Naftogaz in relation to transit through Ukraine, secures a fixed volume of gas (on a ship-or-pay basis – see box below) but at lower levels than in the past. Increasing those volumes above the contracted level (40 bcm /year) will incur additional transit fees and is the least economic option for Gazprom.

Nord Stream 2 could provide some respite, potentially delivering up to 12.5 bcm through the winter (although the OIES suggests flows would be limited to 5 bcm), but its opening remains uncertain and any gas on that route could materialise too late to stabilise the market in cold weather conditions. Europe would also need flows throughout winter from the 12 bcm of available capacity via Ukraine above the current ship-or-pay agreement, but so far Russia has ruled that out.

Last week Russian president, Vladimir Putin asked ministers to explore options to deliver more gas to stabilise European markets, but there is no guarantee that this will materialise, since any such move would need to be on “an absolutely commercial basis, taking into account the interests of all participants in this process”. (This paper by the OIES provides an excellent summary of Russian gas flows into Europe and how the dynamics are changing both in response to political tensions and the development of new pipelines.)

“The big bounce in Russian gas production in 2021 has proven to be insufficient to meet the simultaneous spikes in demand at home and abroad. Russian gas output has risen robustly and has been close to its maximum productive capacities but the necessity to fill the depleted domestic gas storage facilities in Q3 2021 limited the availability of Russian gas for Europe when it was most needed,”

– Vitaly Yermakov, Senior Research Fellow OIES

But even with additional pipeline capacity being available (and setting aside the political and economic tensions around transiting additional gas through Ukraine), Gazprom needs to have the gas available to export. Russian storage levels are also lower than normal and cold weather would boost local demand meaning that Gazprom would only have enough gas to provide additional exports through Nord Stream 2 or Ukraine but not both (although higher deliveries through both routes has never been likely). Exports to Europe could be limited to 106 bcm through the winter.

So the European market is particularly vulnerable to a cold winter, and if that cold weather extended across Russia and Asia, there would be a real risk of supplies being insufficient to meet demand, resulting in curtailments, and prices rising even higher than recent record highs. Should this happen LNG would be diverted from Europe and the UK to Asia, and National Grid’s assumptions that pipeline gas from Europe will be enough to meet demand may prove to be incorrect.

Structural vulnerabilities in the power market makes security of supply less assured

National Grid ESO’s Winter Outlook sees a capacity margin of 3.9 GW, or 6.6%, lower than the 4.3 GW or 7.3% it anticipated in its early outlook published in July with a loss of load probability of 0.3 hours, up from 0.1 hours in the early outlook. The reasons for the deterioration are changes to the generation mix with slightly lower gas-fired generation and the IFA outage which has removed 1 GW of interconnector capacity since the early outlook.

Unfortunately National Grid ESO has left its nuclear forecasts unchanged, which it explained in the early outlook was based on average availability over the past 3 years. This may be optimistic: as these assets age their reliability is rapidly declining. Right now, EDF has two reactors on planned maintenance, and five on un-planned outages, with seven reactors operating at normal full load. The winter outlook assumes a de-rated capacity of 5.4 GW for nuclear this winter (versus base case installed capacity of 7.1 GW, with a 75% de-rating factor). The reactors currently on un-planned outages have a combined capacity of 3.4 GW representing 2.6 GW of de-rated capacity or two thirds of the capacity margin.

“There may be some occasions when we see exports to continental Europe, however this is unlikely to be during peak times and should GB experience some tight/stress periods, we would expect GB prices to escalate and interconnectors to import,”

– National Grid ESO Electricity Winter Outlook

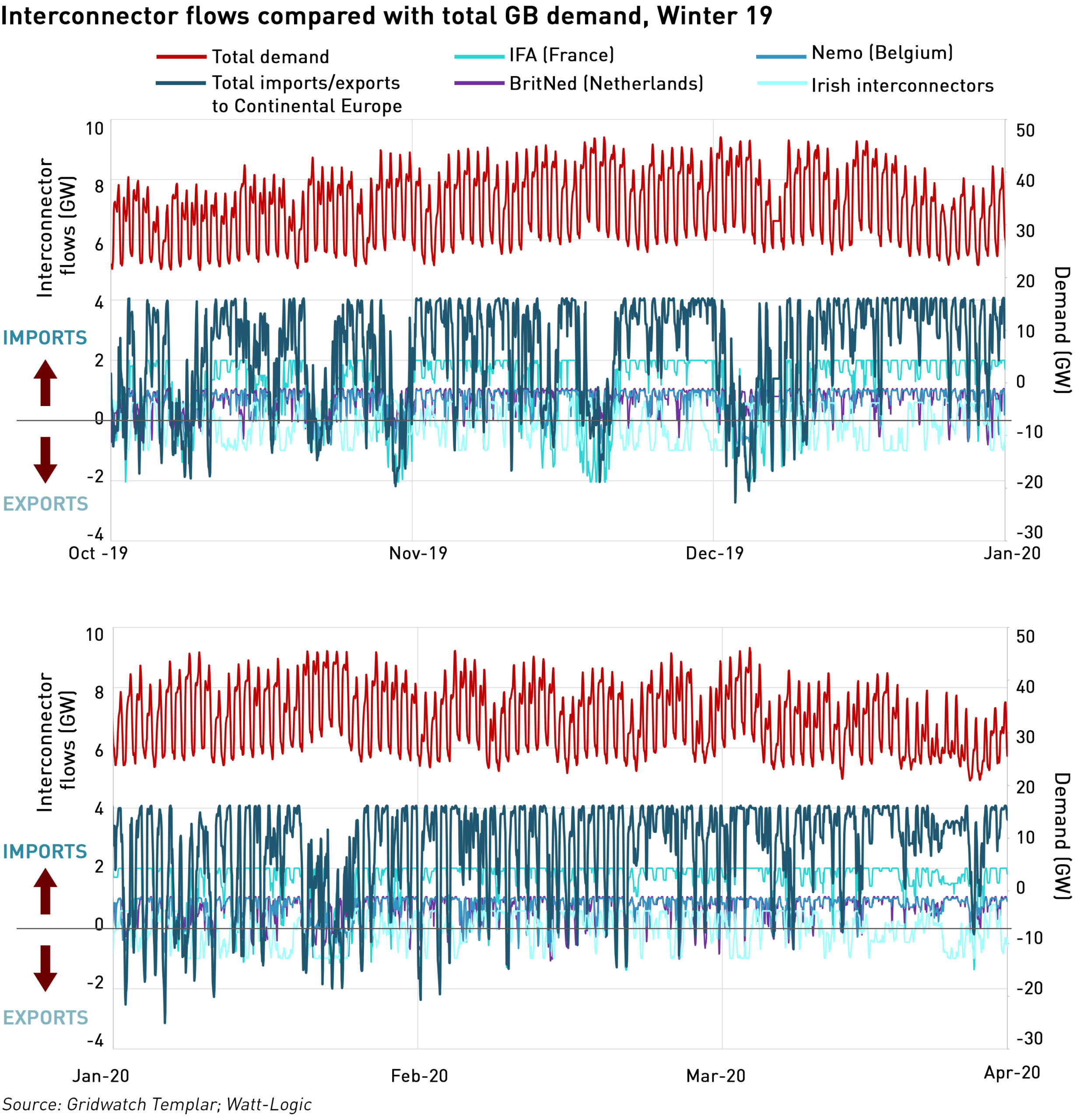

It wouldn’t take much for the remaining margin to be used up by a higher level of outages in the thermal fleet, another interconnector outage, or even a higher than expected level of exports. National Grid ESO seems confident that interconnectors will be importing when needed, but my analysis of flows in Winter 19 showed Britain was exporting in 18% of all hours and 12% of the hours with the 5% of highest demand. In other words when demand is at its highest we actually export in almost one out of every eight hours.

The risks this represents were highlighted on 9 September, when National Grid ESO undertook emergency actions to support consumers in Ireland. The GB system operator reported in its weekly Operational Transparency Forum, that the Single Energy Market (“SEM”) in Ireland was in an amber alert status and had requested additional flows from GB, which were available, albeit at high cost. Eirgrid bought approximately 3 GWh of SO to SO trades throughout the day, preventing load-shedding in the SEM.

These actions raised initial estimates of GB system management costs to £39 million from around £27 million, with about £12 million to be paid by the Irish market to cover these additional costs.

It wouldn’t take much for security of supply to be called into serious question this winter.

French threats are unlikely to translate into a security of supply issue

In addition to the geopolitical risks inherent in the gas markets, a political spat has arisen with France which is threatening to cut off its energy exports to the UK and is urging the rest of the EU to follow suit. For electricity, this would in theory affect the 3 GW of interconnectors with France (1 GW of which is currently unavailable due to a fire at the Sellindge sub-station in Kent), the 1 GW link with the Netherlands and the 1 GW link with Belgium. For gas it would affect pipelines with Belgium and the Netherlands. In addition there are both gas and electricity interconnectors between the UK and the Republic of Ireland, but for these the UK is generally an exporter.

Clément Beaune, who is a close ally of the French president, Emmanuel Macron is calling for action on energy because he is unhappy with the access French fishermen are getting to UK waters following Brexit. The French are claiming that the UK is acting in breach of agreements made between it and the EU. Last week, Jersey declined permits to a third of French boats applying to fish in the island’s waters, as they had failed to provide evidence of operating in the relevant areas. The UK approved 12 of 47 applications, while Jersey approved 95 out of 170 applications.

“We defend our interests. We do it nicely, and diplomatically, but when that doesn’t work we take measures. The Channel Islands, the UK, are dependent on us for their energy supply. They think they can live on their own and badmouth Europe as well. And because it doesn’t work, they indulge in one-upmanship, and in an aggressive way,”

– Clément Beaune

Under the trade and co-operation agreement between the UK and EU, the EU could take unilateral measures “proportionate to the alleged failure by the respondent party and the economic and societal impact thereof” in case of a dispute with Jersey. Jersey is also being accused of failing to provide French fishermen with appropriate access to its waters, and the island, along with its neighbour Guernsey, is dependent on imports of electricity from France.

In theory, the EU could also take unilateral measures affecting the energy supply to the rest of the UK. But all member states would need to agree to the move, and any such action would have to be considered proportionate, since the UK would have the right to take the EU to arbitration. A more likely approach is for the French persuade the EU to appeal to an arbitration tribunal itself, rather than seeking to take action to cut off the UK’s energy supplies.

One thing the French seem to be overlooking in making these threats is that fellow EU member, Ireland, depends on the UK for its energy, as was illustrated by events on 9 September. It hasn’t been mentioned publicly, but in theory, the UK could counter any move by the EU to cut exports to the UK, but stopping UK exports to the EU, including to Ireland. It would also be a move which could potentially harm the French – France depends on electricity for heating, and in cold weather, tends to import electricity from its neighbours, including the UK. Being a net exporter is of little comfort if in times of high demand you are an importer, and the French could end up harming their own self-interest with such a move.

On balance, I’m not inclined to see this as being a particularly likely outcome, but that does not mean that the Government should ignore the situation. Depending on other countries for security of supply carries geopolitical risks that need to be taken into account.

This winter will be the tightest for some years

Electricity margins have been steadily declining in recent years, something which has been widely predicted in the markets, and which is now being realised, translating into significantly higher and more volatile prices. Key vulnerabilities around the nuclear fleet and low wind conditions could significantly erode what is now a pretty slim capacity margin, meaning that the risk of load-shedding is higher than it has been for years, even decades. National Grid ESO likes to repeat its confidence that “the lights will stay on”, but these assertions are getting less credible with each winter – it wouldn’t take much to get into difficulties.

The gas markets are a different story, and in normal circumstances the idea of load-shedding would seem far-fetched. But covid has created a global gas shortage which could not have been predicted. The system operator seems confident that supplies are no worse than usual, but this may be somewhat complacent – if the winter is cold both in Europe and in Asia then Europe could run short of gas, and the UK would not be immune to that effect, or its consequences.

The weather is currently warmer than normal, but there is talk of snow by Hallowe’en, with bookmakers offering odds of 2-1 that this will be the coldest winter on record. I’m not really sure why this is suddenly big news since the Met Office does not seem to be forecasting weather that is unusual for the time of year, and my (generally reliable) weather app is not showing anything particularly exciting for the next month.

The odds are that the winter will pass without security of supply dramas – although pricing dramas are an entirely different matter – and that there will be enough capacity to meet demand. But there is no room for complacency, and while after this winter we can expect gas markets to recover, the GB electricity market has a few tight winters ahead before things improve.

Russian gas contracts

Traditionally gas supply agreements between European buyers and Gazprom were long-term (up to 25 years) agreements priced against a historic average prices of a basket of fuel oil and gasoil indices, typically with some time lag. They also include “take-or-pay” and “ship-or-pay provisions”. In a take-or-pay agreement, the buyer agrees to either accept a minimum volume of gas, or pay a penalty equivalent to having purchased those volumes. Ship-or-pay is the corresponding obligation on the seller which must either deliver the minimum volume or pay the customer the value of the gas it should have delivered (so that the customer can replace the gas elsewhere).

Typically these provisions have some embedded time flexibility, so in years where demand is low, such as during 2020 when covid depressed demand, buyers can reduce their volumes below the take-or-pay level provided they make up the difference in subsequent years, up to an agreed time limit. These additional volumes are known as “make-up gas”.

These contracts worked very well in the past when European gas hubs were immature and gas was generally priced with reference to alternative fuels such as oil, but as the European hubs matured and liquidity grew, oil-indexed pricing began to expose European buyers to basis risks between the oil-indexed price at which they bought gas and the gas-indexed price at which they sold it. For an extended period, hub prices traded at a discount to oil-indexed prices, forcing Gazprom’s customers to buy at a loss, at a time when demand had fallen and the downward flexibility in the gas contracts was not enough to manage the lower volumes needed.

This created real financial pressures for European gas buyers, who began to re-negotiate their long-term contracts with Gazprom, forcing it to accept a degree of hub-gas indexation in its contracts. Gazprom introduced hub indexation for the first time in 2010, when a 15% spot component was included in the pricing formula in its contract with E.On.

Various arbitration panels the forced Gazprom to extend partial hub indexation to other contracts, but it was never required to introduce full hub indexation. There have been suggestions that Gazprom might be unwilling to enter into long-term contracts on a fully hub-linked basis.

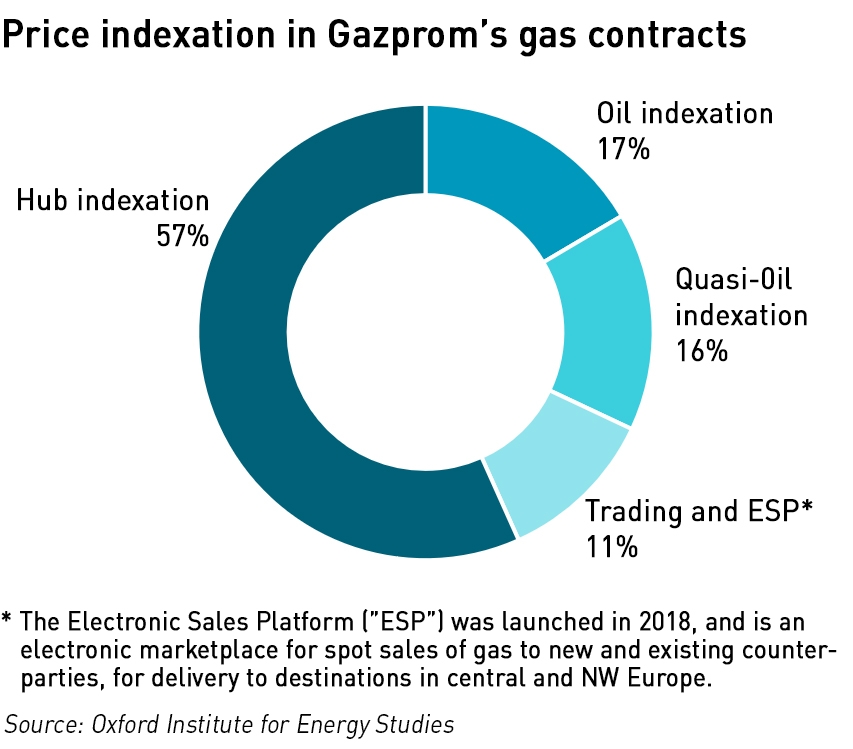

By 2019, 57% of Gazprom’s sales were hub-indexed. Recent comments by Russian president, Vladimir Putin highlight the country’s on-going preference for oil-indexation, but despite high hub prices, it is unlikely that buyers will want to return to previous pricing models. More recently the trend in new contracts for pipeline gas sales to Europe has been for shorter commitments with a transition to full hub indexation – new long-term contracts are now typically 10-15 years in length rather than the 20-25 years of legacy contracts. This also applies to other sellers such as Norway and Azerbaijan.

Europe should long ago have invested in mass district heating powered by nuclear heat only reactors

100% efficient with technically zero waste as the long life radioactive ‘waste’ just becomes long life fuel. As long as humans need warm homes the waste wouldn’t be waste but long life fuel

France alone has 170 GW thermal of reactors they built decades ago. If the UK built just half of that it would be enough to heat all homes in the UK

Heat only reactors would be at least 10x cheaper and perhaps as much aas 40x cheaper

Excellent post very informative.

I did see that Calon Energy are trying to resurrect Severn Power and Sutton Bridge power stations given the prices they can now get for electricity. There worth 1.7GW albeit we need to have the gas available to run them and i guess they would have to buy on spot market.

That’s right, I’ve seen that as well. But cleam spark spreads actually look pretty good right now, particularly in the peaks, so it should be affordable even before you look at the additional value available this winter in the BM.

My concern now is that anti fossil fuel policies in the West will leave us with short supply. Ensuring that the blame for the unpleasant consequences is placed where it belongs will be a battle given the extent of green media control.

Boris’ rumoured plans for even more aggressive targets that have not been properly evaluated only seems to spell more trouble.

Meanwhile I can heartily recommend this study of BECCS that effectively reveals is limitations and costs. The technical detail that shows they very low energy output and the whole supply chain emissions picture is very revealing. Another CCC projection thoroughly debunked.

https://www.chathamhouse.org/beccs-deployment/summary

I’m actually a bit more confident that the blame will be correctly apportioned – mainstream media are reporting all sorts of things on energy at the moment that the Government would prefer it didn’t (eg the fact that margins in energy supply are very low). I think the media’s main aim is to sell papers/clicks/whatever, so there’s less of a tendency to be ideological (except for the BBC which operates outside normal commercial considerations).

That is a really good report on BECCS. I can see the author trying hard not to be negative, but the whole thing stinks and is unlikely to be genuinely sustainable. Props to Drax for taking an obsolete business model and making it work, but the Government should not be allowing it. Sadly, since neither the Government (nor any other politicians) nor the civil servant really understand energy the problems with BECCS will only accumulate until the land use tensions become un-manageable.