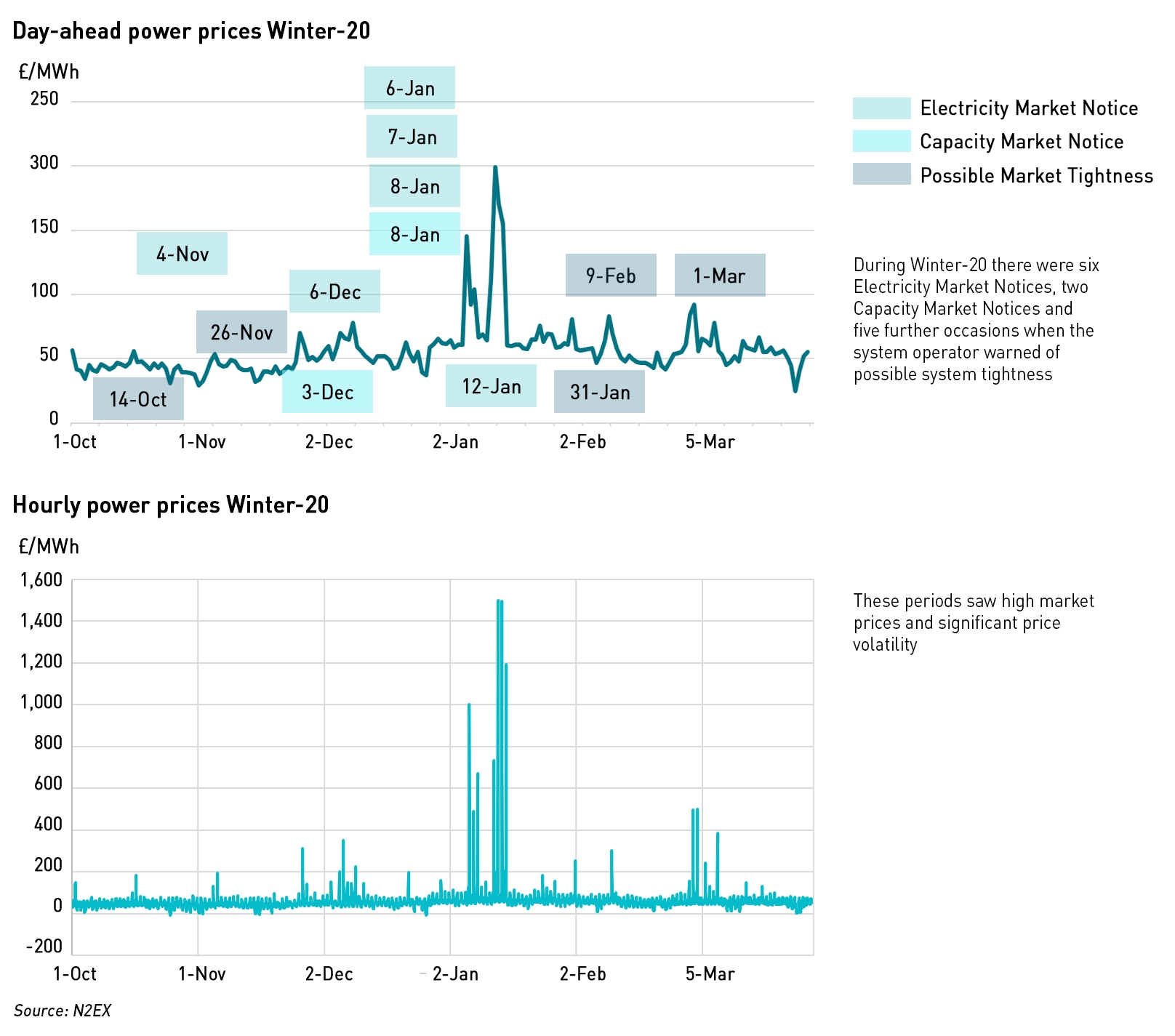

Winter 2020 was a bumpy ride in the GB electricity market. Electricity Margin Notices (“EMN”) (the new name for a “NISM” – Notice of Insufficient System Margin) were issued six times, there were two Capacity Market Notices (“CMN”) (following one on 15 September just before the start of winter) and on a further five occasions National Grid ESO tweeted about possible system tightness. As expected, prices were spiky and volatile across all near-term time periods, and generators were able to capture significant upside in the Balancing Mechanism (“BM”).

In just 3 days this year, EDF was paid more in the BM than in the whole of Q3 last year, at one point earning £4,000 /MWh – 70x the average winter 2020 day ahead power price of £55 /MWh. According to analysis by Hartree Solutions, the six biggest earning power stations in the BM in January were all CCGTs with EDF’s West Burton B plant earning £8 million on 8 January when both an EMN and a CMN were issued.

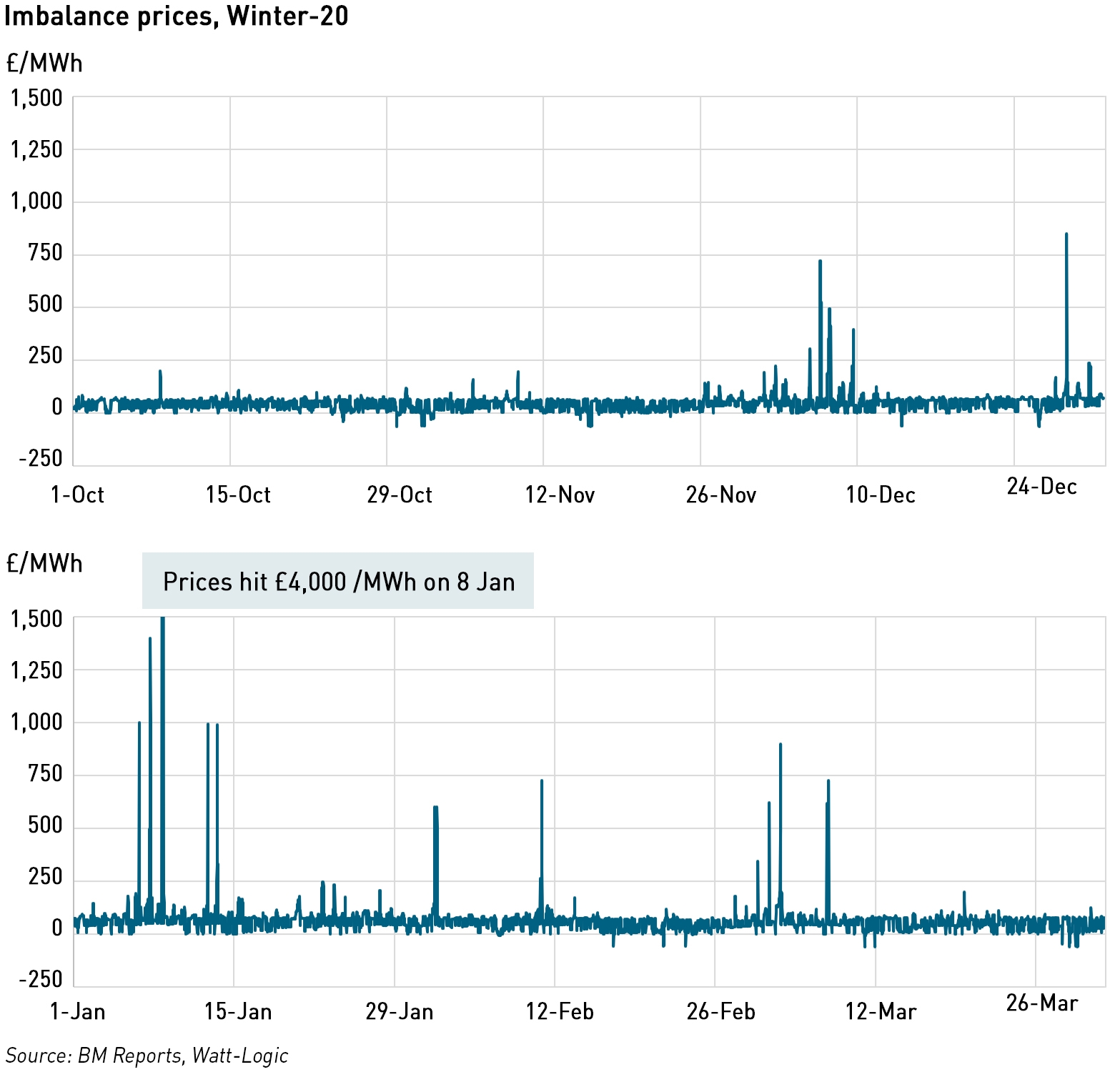

Market participants with imbalances faced significant price risk with Imbalance Prices also seeing significant spikes, reaching £4,000 /MWh on 8 January which was the tightest day of the past winter. This exposed particularly smaller firms which can struggle to hedge their full shape risk in the forward markets.

Why was the market so tight in winter 2020 and was it a one-off or part of a wider trend?

There are two opposing schools of thought on this. One view is that NG ESO wants to make EMNs less rare: if market participants are to be encouraged to develop necessary capacity, then there need to be signals to suggest it is needed. If ESMs are only issued rarely, then the market might conclude there is ample capacity.

The other perspective, which I favour, is that we are heading into a period of structural under-capacity. The market is responding to the Government’s deadline of October 2024 for the closure of all remaining coal plant, and the aging nuclear fleet is seeing declining reliability even where lifetime extensions have been granted. The beleaguered next generation nuclear facility at Hinkley Point C has had it’s opening date pushed back again, this time to June 2026 (and another hike in the costs), means that the nuclear replacement programme will not be available to fill the gap.

There were also some more specific events last winter which may not be part of the wider trend. Last year the bankruptcy of Calon Energy forced its two large CCGTs (2.3 GW in total) into mothballs, although recent developments suggest they could be brought back into use ahead of next winter, and there was an extended outage from 8 December until 9 February on the BritNed interconnector which added to the capacity shortage.

“For one week in mid-February, wind farms generated nearly 40% of Great Britain’s electricity, keeping electricity prices low and reducing carbon emissions. However, two weeks later wind power had almost disappeared, providing just 7% of weekly generation and leading to higher prices,”

– Ed Birkett, Senior Research Fellow, Energy and Environment, Policy Exchange

Of course, the weather did not help – January and February in particular saw the weather alternating between cold and still periods with low wind output and high demand for heating, and storms where the temperature was notionally higher but still felt cold, driving heating demand.

What does last winter’s tightness means for the market?

The next few years will see less coal and nuclear running, and while more renewable generation continues to be built, solar makes a minimal contribution in the winter, and high pressure weather systems with low temperatures and little wind are actually quite common at that time of year.

But while lower capacity margins increase the chances of blackouts it does not make them likely as NG ESO has plenty of reserves to call on in addition to the capacity market. That in itself does not mean all is well – my sense is that for the next few years, we will see periods of significant market tightness in winter, with corresponding price spikes and volatility.

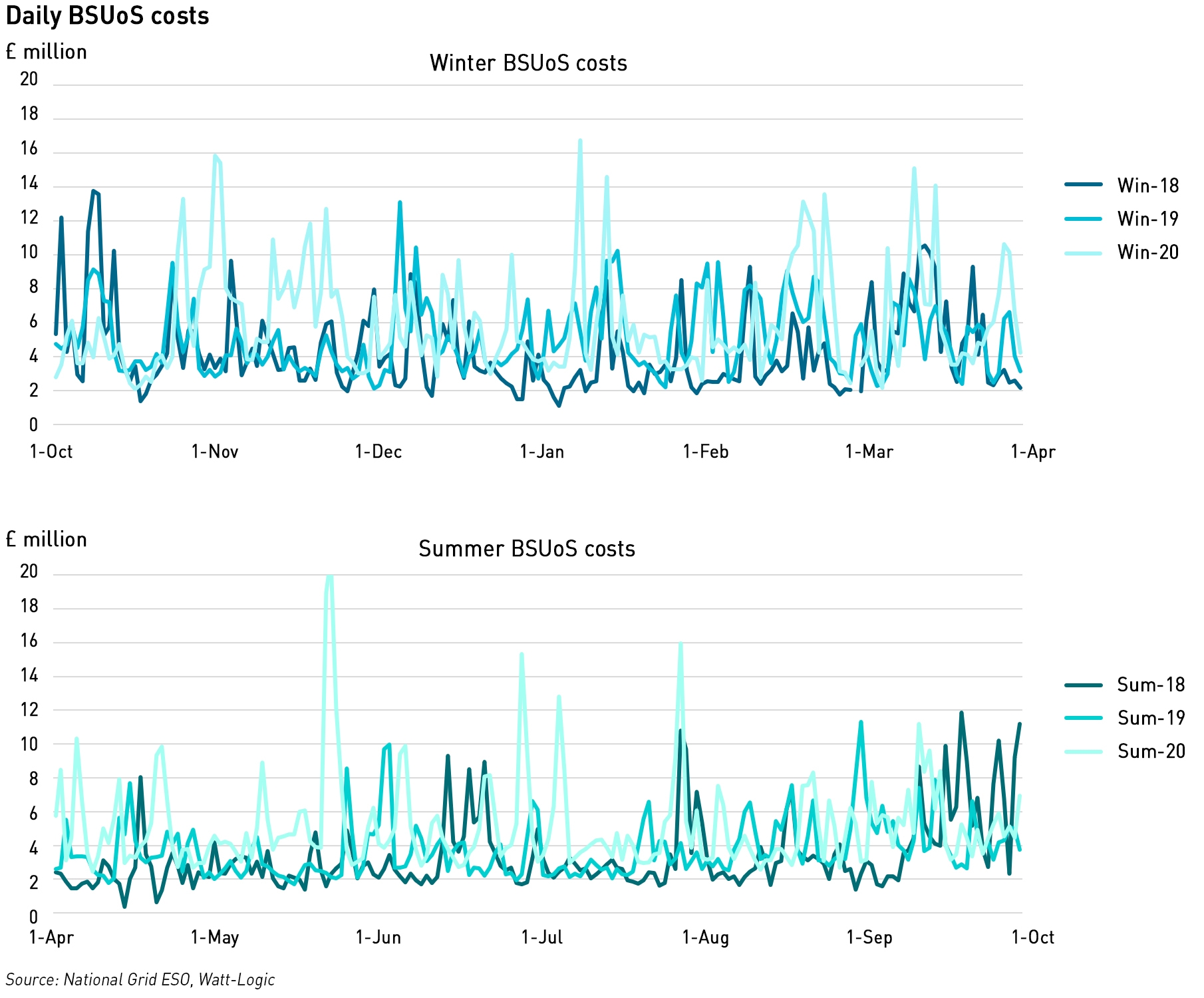

At the same time, there will be low system demand in the summer, due to the increasing contribution of solar power, with more periods of negative prices. And across the year, I expect balancing costs to rise sharply, as was seen last summer when low system demand saw balancing costs rise sharply.

The other important trend is that of electrification. The Government is pushing hard for electric vehicles to replace petrol and diesel cars and vans, and is looking at ways to encourage the uptake of heat pumps as an alternative to gas heating. Either of these in isolation would have a major impact on electricity system demand, with electric heating driving higher use of electricity in winter – some 78% of British homes are currently heated with gas, so the potential impact on the electricity system of electricifation could be very material.

Although some of the capacity issues last winter might have been one-offs, the reality is that dispatchable generation is being increasingly replaced with intermittent renewable capacity, while demand is set to grow significantly. This means that although the specific drivers may differ in future, the overall outcomes may be remarkably similar, and winter 2020 may indeed provide an insight into a new market paradigm.

If this is the case, then market participants will need to find ways to manage these very different winter and summer dynamics.

Thanks for the informative post.

While changes to grid supply is worrying, I thought we saw this coming a long time ago? Is there something uniquely unexpected in how the market is developing?

We definitely saw this coming, but the past few winters before win-20 were much milder. Win-20 saw much more sustained cold weather coinciding with low wind output.

NG ESO’s priority is to keep the lights on, it doesn’t really have a particular mandate on cost other than to try to minimise costs where possible, within the SQSS framework. In practice this means taking the lowest cost actions available at the time to balance the system…if market prices experience short-term spikes that isn’t really an issue for ESO. But it’s a big issue for market participants that have to manage that volatility.

Interesting. And of course Dungeness B now not coming back.

Hi Kathryn….thanks for recent informative postings, both of which in my mind are linked.

(Tight Margins & Demise of Coal Power)

The rundown of coal power & tightness of margins comes as no surprise.

I remember travelling across the Pennines on the M62 from Lancashire on frosty still mornings under blue sky’s. At the M62/A1 intersection looking East along the Aire valley Ferry Bridge, Eggborough, Drax with adjacent coal mines always struck me as a neat power production model. Below each stack the mighty 500MW generators collectively delivering 20% of national demand 7/24/365 at that time. The post burn ash was used in the production of thermal blocks for the construction industry.

A tidy productive process.

I fully support green targets but in my opinion we need to extend the time scale. There has been insufficient emphasise & resource directed at carbon capture & storage (CCS) which could have favoured extending the life of many perfectly good coal plants. Interestingly Drax is currently pursuing this technology with Mitsubishi deploying old oil & gas wells etc. for safe storage of the waste substance produced.

There are many, many initiatives swirling around energy development in the UK. Hydrogen is likely to play a large part. Blue hydrogen produced from processing natural gas needs a CCS facility. The chemical giant Ineos is doing much on this at their huge Cheshire plant.

In summary I feel more support in the development of (CCS) should have been forthcoming & maybe an extension of

10 years to the life of many 1st class dependable coal power stations would have helped to bridge the gap.

Barry Wright Lancashire.

Hi Barry – yes indeed, the two posts are linked (and had to be published together as some technical problems meant I had to stop publishing for a bit).

I completely agree about the timeframes for green targets and that there hasn’t been a coherent plan that ensures the right technological progress is made to support a proper functioning of the market through the transition. We now have a situation where every form of generation is subsidised, system balancing has become significantly harder and more expensive, and a bit of cold weather sends prices soaring in winter while sunny weather sends them negative in summer.

On CCS though I think it’s better in theory than in practice. There are only 2 power stations fitted with CCS, both coal plants and both have suffered a lot of technical problems. CCS for CCGTs hasn’t been invented yet – the technical problem is harder and the parasitic loads make it uneconomic even if it could be made to work.

If it was up to me, I would build a couple of ABWRs (my next post is an update on nuclear) – these could be built in around 4 years once permits etc are granted and could even open before HPC given the latest delays there. I would then run nuclear in baseload in winter, possibly with some turned off in summer, and use renewables for the rest, backed up with gas for the time being. That would mean that at times renewables would have to be curtailed, but I don’t actually have a problem with that, particularly in the absence of seasonal storage.

I would spend my subsidy money on technologies that are known to work (ABWR) rather than holding out for something that might never be technically or economically feasible.

Hi again……always room for nuclear in the mix IMO, shame the Anglesy project was shelved.

I agree, ABWR’s are the way forward, even allowing for a possible Chinese involvement.

Currently viewing the HPC build on BBC2 brings it all back.

A very apt description of the Heysham 1 build was dubbed “Watch Making By The Ton” at the time.

Re your reference to permits, I’m sure these are in place for a Heysham 3 build at some point.

A Rolls Royce partnership are already on site developing their Small Modular Reactor (SMR) programme.

The Heysham energy gateway awaits (a big plus) offering an established robust connection to the 400v super grid.

Digressing:

The nationalised CEGB were never permitted to use gas for electricity generation. It was considered a refined fuel that could be used directly in most applications. Come privatisation the gloves were off, OCGT’s arrived on the back of a truck erected, commissioned & delivering income within 2 years. In the meantime the build continued at the exhaust end to create the final CCGT installation. Little wonder the dash for gas became the norm. However gas remains a finite resource which continues to be consumed at an alarming rate.

I still feel that far more R&D should have been directed at CCS & storage years back, just a small part of the many millions spent on renewables over the period.

Fingers crossed the gas continues to flow.

Which prompts me raise the point of interconnections & pipelines crossing mainland Europe post Brexit, or am I just an old scaremonger ?

Barry Wright Lancashire.