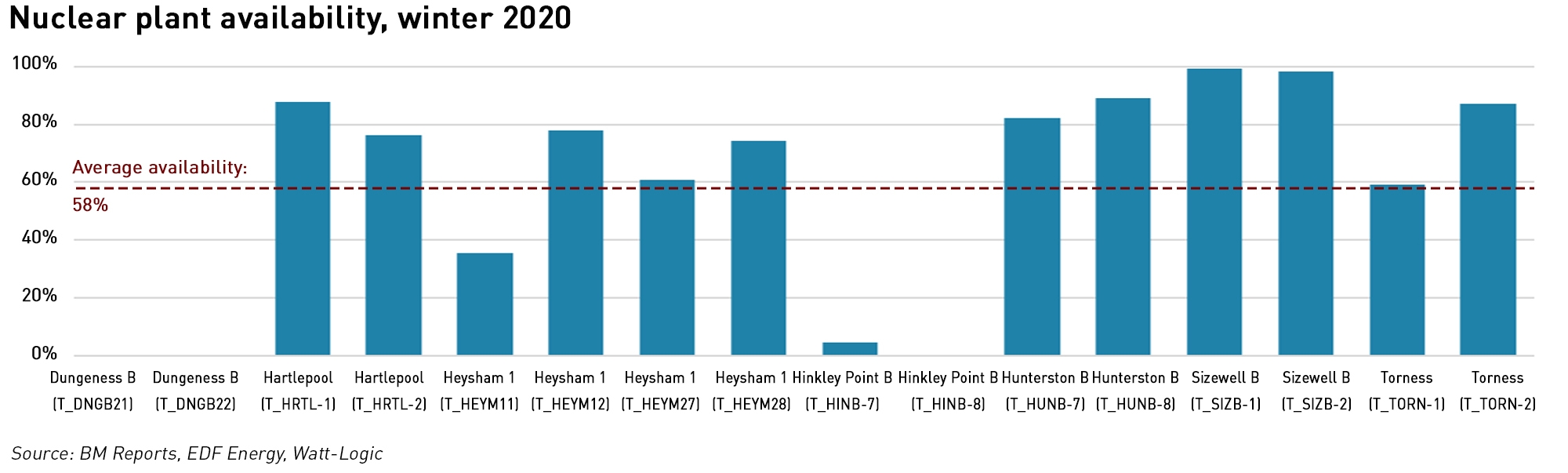

Low nuclear availability added to the capacity issues in the GB market over the past winter, and as the fleet ages and new nuclear is further delayed, these problems are set to become more acute.

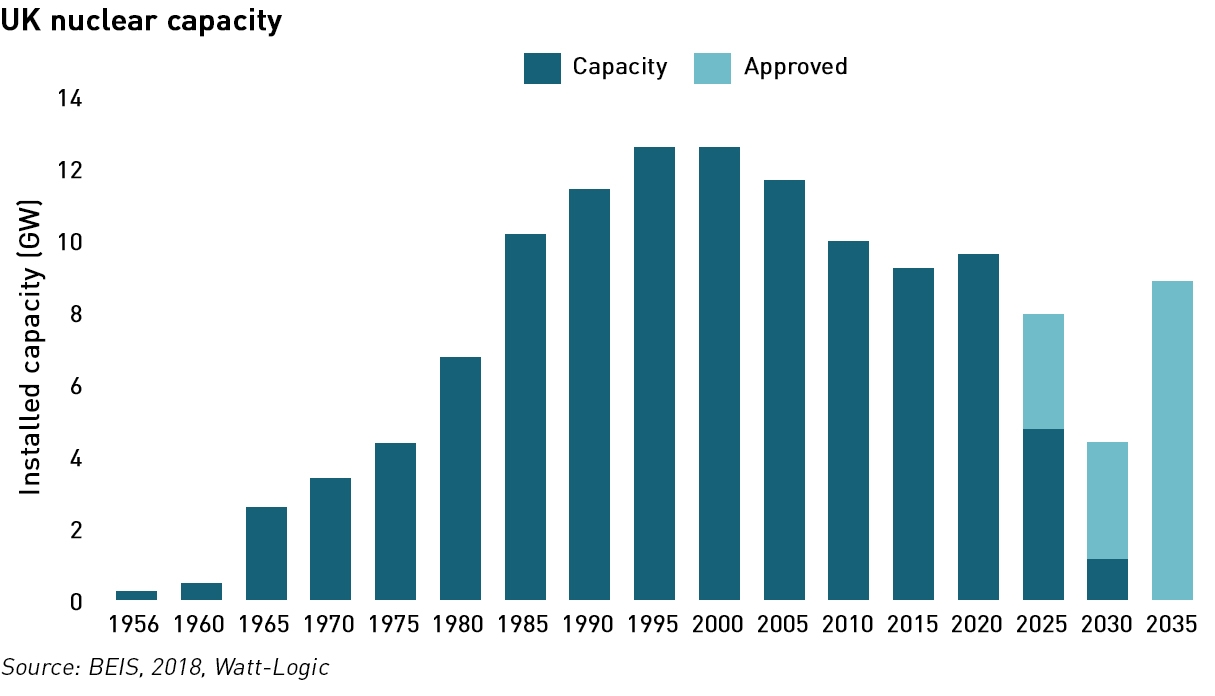

Since the first commercial nuclear power plant anywhere in the world opened at Calder Hall at what is now the Sellafield plant in west Cumbria in 1956, nuclear power has formed an important part of the British energy mix, peaking at 17% of installed capacity in 1994 at 12.7 GW. Plant numbers peaked at 18 in 1988.

But now the fleet is aging, and with just 7 nuclear power stations left after the recent closure of Dungeness B, the sector is struggling to meet the gap made by the exit of coal. Just one new nuclear power station, Hinkley Point C, has received approval since the last of the current reactors, Sizewell B, was approved in 1987.

Dungeness B in Kent, which has been offline since 2018 for maintenance, will not restart and run until 2028 as planned, despite significant investment in attempting to bring it back to service this summer. Even as late as April EDF has been hoping to get the plant re-started.

“The station has a number of unique, significant and ongoing technical challenges that continue to make the future both difficult and uncertain. Many of these issues can be explained by the fact that Dungeness was designed in the 1960s as a prototype and suffered from very challenging construction and commissioning delays. Major investments have been made to repair and upgrade the station over many years, including more than £100million in this current outage. A number of significant technical risks still remain,”

– EDF Energy

The newest nuclear plant on the system, Sizewell B in Suffolk has recently been forced off the grid for extended maintenance. The station went offline on 16 April for planned maintenance and had been due to return to service at the end of May, but it will remain closed until the end of August as repairs are needed to some of the stainless steel “thermal sleeves”, which form part of the mechanism that inserts control rods into the reactor core to shut it down. If these sleeves become too worn they can loosen and obstruct the control rods, although an EDF spokesperson said they “provide no significant nuclear safety-related function”.

Calder Hall

The 196 MW Calder Hall facility was the first nuclear power station in the world to produce electricity for domestic use, supplying the town of Workington, 24 km away. Designed to last 20 years it operated for 47 years before closing in 2003. Although the plant was promoted as a cheap source of electricity that was “too cheap to meter”, it’s low capacity meant it produced relatively little electricity, being primarily intended to produce plutonium for the country’s nuclear weapons programme.

The station had 4 Magnox reactors – the first two began operating in 1956, the third in 1958 and the fourth in 1959. The reactors were of the gas-cooled graphite-moderated type, using carbon dioxide, each weighing 33,000 tonnes. To generate electricity, the reactors ran eight 3,000 rpm turbines, four located in each of the two turbine halls. The turbines were 75m long, 25m high and 20m wide. The site also included four hyperbolic 90m high concrete cooling towers.

According to the British Nuclear Group, in its 47 years of operation, Calder Hall generated enough power to run a three-bar radiator for 2.85 million years.

The age of the fleet is creating problems with availability – only Sizewell B had almost full availability over the winter – each of the other reactors had periods of unavailability. Usually, planned maintenance is scheduled for the summer when high solar generation and low demand depress prices, so when nuclear power stations are offline during the winter it is either a forced outage due to safety concerns, or because a fault has developed which forces the plant offline.

Indeed, in addition to its announcement last week to close Dungeness B early, EDF has also indicated in the past few days that safety issues at Torness in Scotland and Heysham 2 near Lancaster could force both plants to shut years ahead of their planned 2030 closure dates.

Hinkley Point B in Somerset and Hunterston B in Scotland, the first two Advanced Gas-Cooled Reactors (“AGRs”) to open in 1976, will close next year rather than in 2023 as planned due to cracking in their graphite cores which has already caused prolonged safety outages. How long the remaining four AGR plants can continue running will depend on when cracks in the graphite cores emerge, and the level at which cracking becomes a safety concern – EDF has invested around £200 million into studies to establish what level of cracking can be tolerated safely.

The two newest AGRs – Torness and Heysham 2, are not due to close until 2030 but both have already generated almost as much power in running for 33 years as Hinkley Point B and Hunterston did in 45 years, which is important because the radiation levels generation from running the plants that lead to the cracking in the graphite cores, meaning that either plant could start to develop problematic cracks earlier than expected. Once cracks emerge, they will have only three or four years of safe running left.

New nuclear is not coming to the rescue

EDF had hoped that by extending the lives of its older nuclear facilities it could bridge the gap to the next generation of reactors, but this plan is not being realised. Not only are problems with its aging fleet of AGRs bring forward their closure dates, but the next generation of reactors, beginning with Hinkley Point C is suffering from delays.

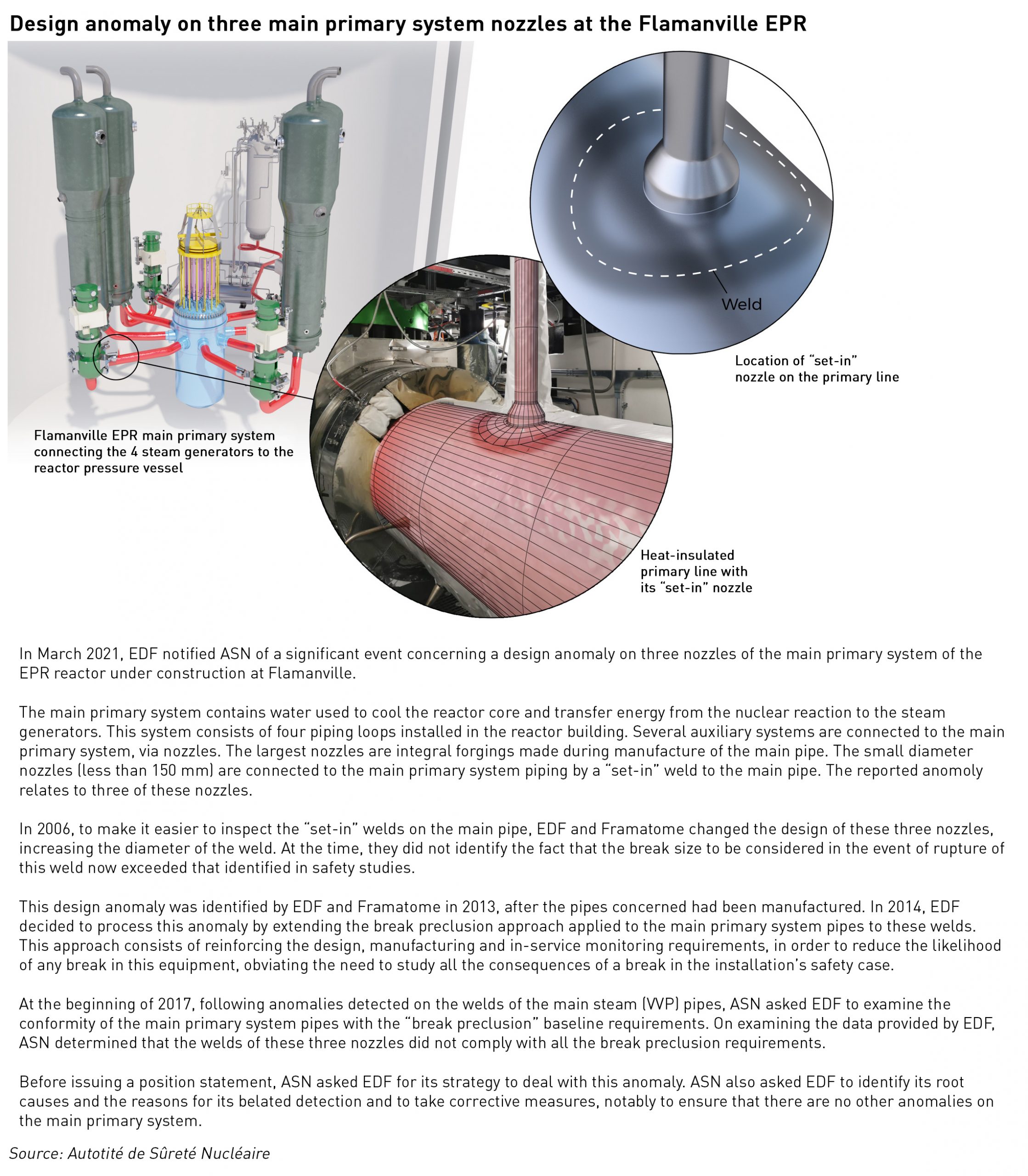

Hinkley Point C was approved after a hiatus of 25 years in the development of new nuclear in GB. The plant will have two European Pressurised Water Reactors (“EPR”), which are so-called 3rd-generation reactors being built by EDF, considered a world-leader in nuclear power. But even EDF has had a 20-year gap in successfully developing new nuclear reactors, and many of the necessary skills have been lost. The firm’s flagship EPR at Flamanville in France has been beset by technical problems and cost over-runs – in March yet more issues were discovered meaning the plant will enter service at least a decade after its first expected commissioning date. The costs have risen from an original estimate of €3.3 billion to €12.4 billion.

Olkiluoto 3, EDF’s first European EPR project is expected to be connected to the Finnish grid in October this year, 12 years later than originally planned, at a cost of €8.5 billion, three times the initial estimate. Although two EPRs have been successfully completed in China, little is known about their costs or reliability.

Although the problems at Hinkley Point C are less severe than at the other European EPRs, work is both behind schedule and over-budget, and it remains to be seen whether EDF and its partners have the depth and breadth of skills needed to bring 3rd generation nuclear facilities into successful operation. However it is pressing ahead with a second UK project, the £20 billion Sizewell C scheme and is in negotiations with the government about taxpayer support.

There are currently no other new nuclear facilities in the pipeline after the collapse of negotiations on the funding of the proposed Advanced Boiling Water Reactor (“ABWR”) at Wylfa Newydd on Anglesey. Regular readers will know that I am a big fan of the ABWR technology, which is a smaller jump from the previous generation of nuclear power stations, after four ABWR plants were completed on time and on budget in Japan before the Fukushima disaster forced them to close.

The latest delays at Hinkley Point C mean it is unlikely to begin commercial operations until mid 2026. As the Japanese ABWRs were constructed in 4-5 year timeframes, it would still be possible to get an ABWR into service in Britain before HPC is built, assuming permits and financing are expedited. Unfortunately the Government has not demonstrated the necessary will, and despite nuclear power featuring in its 10-point plan for energy, the funding commitment is woefully inadequate.

Similar issues face the much-hyped Small Modular Reactor (“SMR”) technology where the need for significant upfront capital investment in the fabrication of the reactors is a major barrier to entry.

.

I have written recently about the challenges faced by market participants last winter, with high and spiky prices and various capacity warnings. With the accelerated exit of both coal and the aging nuclear fleet and the delivery of new nuclear pushed back again, these market conditions are set to worsen over the next few winters.

The risks of blackouts are increasing, but although they remain small, they are not the only risk of tight capacity margins – in tight markets, prices rise and become more volatile, and it becomes harder for market participants to manage their price risks. This could be particularly difficult for smaller energy suppliers with no generation assets and low ability to hedge their shape risk (due to unavailability of credit), putting further stress on already stressed business models.

Interesting piece about our ageing nuclear fleet – what are your thoughts on this story https://www.theguardian.com/world/2021/jun/14/french-nuclear-firm-trying-to-fix-performance-issue-at-china-plant emerging re the EPR at Taishan and any potential implications for timelines at the other EPRs in France, Finland and Hinckley Point C? It does seem that the UK has ‘bet the farm’ on a relatively untried design that so far has been over-budget and delayed. Should they have chosen ABWRs in the first place and saved themselves a lot of potential future issues?

Interesting – I tried to seach for problems at Taishan last week and this didn’t come up (only published yesterday). My first reaction to this is that if they think there might be detectable radiation 85 miles away in Hong Kong, then there would be a serious safety issue, but I’m not sure if that isn’t just the reporter scambling for something to say.

The reality is that China is simply too obscure so I generally ignore the Taishan reactors. If someone can point me in the direction of credible, externally verified data on costs and performance, them I would be happy to include them in my analysis, but in the absence of either, I don’t think we can derive any information regarding EPR technology from the Taishan plants.

The UK should never have gone down the EPR route. At the time those decisions were made, the problems at Olkiluoto and Flamanville were already well known, but in the absence of other project proposals, they bet the farm on EPR. The correct answer at that point would have been to announce that they were seeking alternatives and asking the market to put forward other projects based on other technologies – ABWRs were already running by then, so even a small amount of due diligence by BEIS (or whatever its predecessor department was at the time) would have identified this.

You make a very good point about the credibility and transparency around the Taishen data. Re Hinckley point it also seems like in the absence of any other proposals EDF leveraged a hell of a deal for HPC with various UK government-backed guarantees during construction to mitigate risk, as well as a set price for the output that was index linked from (I think) 2012 onwards that covers the first 35 years of the plants lifespan. Whatever your views on new nuclear it seems on paper to have been a terrible deal (from a cost perspective) that politicians at the time thought ‘well, I’ll be gone by the time it starts generating therefore not a problem for me’.

Perhaps one of the biggest clues was that the Chinese decided very early on after the completion of the first reactor that they weren’t going to build any more EPRs. They obviously expected technical and economic problems based on the experience of building the pair the committed to.

And what about the serious problems at the new EDF power stations in Taishan, China?

https://www.telegraph.co.uk/business/2021/06/14/fears-radiation-threat-edf-nuclear-plant-china/

Also New Scientist and Mail about to publish.

And in France via Press Assoc:

https://www.lepoint.fr/monde/epr-de-taishan-un-probleme-qui-tombe-mal-pour-edf-mais-aussi-pour-la-chine-15-06-2021-2431006_24.php

This looks like a reasonably balanced overview of the Taishan situation:

https://www.reuters.com/world/china/what-happened-chinas-taishan-nuclear-reactor-2021-06-15/

It also refers to “frequent” minor safety issues at the plant. I would tend to agree that the current situation isn’t particularly dramatic, and that the real concern relates to moving the goalposts from a regulatory perspective rather than actual danger. While I do believe that European safety standards are unduly strict following Fukushima – EDF’s in-service reactors would not have been certified under the current regime despite running for decades without any major issue – standards should not be subject to ad hoc change just to keep a reactor running.

Not only falling capcity in the UK of course. As Timera pointed out

Put in simple terms, Germany needs to replace 8 GW of nuclear (closing by end of 2022), 15GW of coal and 14GW of lignite capacity (most of which will now likely close by the mid 2020s). The majority of these units have been running at relatively high load factors i.e. orders of magnitude more GW of wind & solar capacity is required to replace it, given lower average load factors (& even lower derating factors).

“Germany’s current policy framework is flirting with major power market disorder across the next 2 – 3 years”

And that will echo to the UK via interconnectors. Not that they are the only one of course. There are plenty pf closures in the offing, even if France has extended its nuclear deadline by a decade.

I don’t think Germany will close its coal that fast. It now has its coal closure auctions, but the TSO still has the right to keep them open for system reasons, and is exercising that right so far. The TSO holds the get-out-of-jail-free card which I think will make the difference, but they are right to say the policy flirts with disaster.

PS Sorry for taking some time to approve your comments – over the weekend I migrated from shared hosting to a VPS and couldn’t make changes to the website until the migration was completed (at least, I could but they might have been lost…)

Your comments regarding nuclear availability of the winter are not really correct. The units come off for all sorts of reasons – statutory (regulatory) outages, refueling outages, even on load refueling requires a drop in output for a short period of time. You’ve also included in your 58% figure 2 stations which were never really expected to generate much at all, and so compared with their declared availability the 58% figure is very misleading, as it suggests the units were offline for 42% of the time either for a safety reason or because there has been an equipment failure, which is not true.

If you can explain more why those stations were offline in winter absent a safety concern or equipment failure then that would be helpful. Otherwise, it is not typically the case that operators do not make their plants available in winter, particularly when they can see a lot of other plant is unavailable (eg the 2 Calon CCGTs and then BritNed). My understanding was that planned outages are scheduled for the summer when there is reduced need for them to run, and lower returns from doing so.