In a recent post I outlined some of the challenges facing Hinckley Point C – the flagship next generation nuclear project in the UK. Various commentators have suggested that new nuclear in the UK has missed the boat since the deployment of renewables combined with the problems with the new EPR technology means that there will be no nuclear renaissance in the UK. There are good reasons for agreeing with this assessment, particularly given the problems with Flamanville, but the question is whether this is true for all new nuclear projects, or just super-large ones such as Hinckley Point.

Small successes

Since the first commercial nuclear reactors were developed in the 1950s, they have become progressively larger in order to capture economies of scale. This has resulted in enormous multi-GW facilities with long and complex construction requirements and astronomical capital costs. The combination of high complexity and high cost drives economic risk and makes these plants difficult to finance, raising the need for subsidies and government guarantees.

However, at the opposite end of the spectrum is a proven small-scale nuclear technology – work on nuclear marine propulsion began in the 1940s, with the first nuclear-powered submarine, USS Nautilus, being launched in 1955. In the UK, Rolls-Royce pressurised water reactor (PWR) technology has powered nuclear submarines since 1966. Nuclear power is also used for surface ship propulsion, for example in US aircraft carriers and Russian ice breakers.

Source: Rolls-Royce

In recent months there has been a lot of excitement in the UK about the prospect of small-scale nuclear, and the government is keen to pursue the idea having funded a number of studies into the technology and has devoted £250 million in the latest budget to finance a competition to identify the best prospects.

SMR landscape

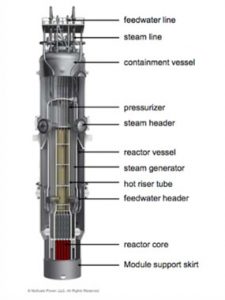

| Small modular reactors (SMRs) are defined by the International Atomic Energy Authority as nuclear fission reactors with an output below 300 MW. They are manufactured in factories rather than being built on site, and are designed to be modular with larger plants being constructed from multiple modules. Most SMRs are being developed using one of four technologies: light water reactors (LWR), fast neutron reactors (FNRs), graphite-moderated high-temperature gas-cooled reactors and molten-salt reactors (MSRs). The main focus is on advancing LWR designs as they are seen to have the lowest technological risk, being similar to conventional nuclear plant. |  Source: NuScale |

A small number of SMRs are currently in operation around the world: small reactors have run a remote site at Bilibino in Siberia since 1976, with the excess steam supplying a district heating system (graphite moderated boiling water), and there are also small reactors operating in China (PWR), Pakistan (PWR) and India (PHWR). China is currently building two 250 MW high-temperature gas- cooled reactors.

The World Nuclear Association has a comprehensive outline of the state of SMRs worldwide and the technologies under development on its website.

Benefits of SMRs

SMRs are seen to have a number of potential benefits over traditional large-scale nuclear facilities:

- Manufacture – SMRs can be manufactured off-site, and delivered already fuelled and sealed. Their small size and simpler design means build-times will be significantly shorter and construction risk reduced. The forging capabilities needed to build the pressure vessels are similarly reduced, potentially a major benefit in the context of the issues with the Flamanville pressure vessels. There is also scope for “mass” production.

- Financing – SMRs are forecast to cost US$25 – 200 million per unit, versus US$5-15 billion for a traditional reactor. Maintenance costs are also lower for SMRs, as they have fewer moving parts making cheaper and more reliable to maintain and operate. The reduced complexity and technological risk will bring down the overall risk profile of projects, and the shorter construction time will reduce the time to positive cash generation, making them more attractive financing prospects.

- Safety – SMRs are specifically designed to be simpler to operate than conventional nuclear plant, with more passive operations (ie reduced scope for human error). Remote shut-down procedures and power-independent cooling systems (using natural convection and gravity) mean reactors should remain safe even under severe accident conditions.

- Markets – SMRs can vary their output quickly, and so can act to balance systems with high levels of intermittent, renewable supply. SMRs are a low-carbon generation source which can displace thermal generation, in particular retiring coal plant. SMRs are also suitable for use in remote areas and can support district heating schemes.

- Non-proliferation – Many SMRs are designed to use low-enriched uranium with less than 5% enrichment, making it less desirable for weapons production.

Potential drawbacks

However, there are also some drawbacks to SMR technology:

- Lack of maturity – SMRs would need to demonstrate the same high safety standards that large-scale light water reactors have shown in over 50 years of commercial operation. The lack of track record and credible test cases is a barrier to licencing SMR projects, and is expected to lead to long (and expensive) permitting processes.

- Running costs – SMRs have relatively high running costs, with each kilowatt hour projected to cost between 15% and 70% more in fuel costs than equivalent output of a traditional large nuclear plant, due to economies of scale.

- Market evolution – The first new SMRs under development in the US are not expected to come to market until 2025. The pace of renewable deployment might make baseload generation such as nuclear largely obsolete during this timeframe, meaning SMRs would need to be economic under load-following conditions.

- Security – As with any nuclear technology, protection against theft or terrorism is important. With small reactors spread across multiple locations, security costs can be higher than for traditional large facilities.

- Manufacture – SMRs are designed to be built in factories – factories which themselves would need to be financed and built. Some commentators have estimated that between 40 and 70 units would be required to achieve break-even, which is a comparatively large amount. David Orr, head of nuclear business development for Rolls-Royce in the UK, estimates 4-6 dozen whereas former US Energy Secretary Steven Chu is more optimistic thinking cost savings would be apparent from the 10th unit.

SMRs also face the same challenges as their larger cousins in relation to the safe disposal of nuclear waste.

Chicken-and-egg problem

The potential of SMR technology has attracted a lot of interest and some impressive claims. A 2014 report from the UK’s National Nuclear Laboratory suggested the global market or SMRs could be in the 65-85 GW range by 2035, valued at £250 – 400 billion, with 7 GW of SMRs in the UK. However, there is a good deal of scepticism around these claims.

For SMRs to make economic sense will depend on their production economies of scale being realised. Whether the breakeven point is at the 7th or 70th unit is a significant difference, and a strong order book would be required in order to finance a facility that is genuinely capable of delivering scalable production. Unfortunately, the ability to secure orders generally requires a level of track record, so both customers and investors are likely to hang back and wait for results before committing themselves. This creates a chicken-and-egg dilemma, since the initial units need to be manufactured, and the production process itself needs to be tested.

The difficulty of this challenge has been reflected in the degree of scaling back by some of the early movers. In early 2014, Westinghouse announced that it had “reprioritised” staff away from its SMR project, with the CEO, Danny Roderick being quoted as saying that the problem with SMRs is not the technology but the lack of customers. In April 2014 Babcock & Wilcox announced it was cutting spending on its mPower SMR project having struggled to find customers or investors.

However, US-government funded company NuScale continues to push forward and plans to submit documentation to the Nuclear Regulatory Commission in 2016 for design review. It expects to have its first SMR in operation in the US in 2025, with plant in the UK following shortly thereafter. And just a couple of weeks ago the Tennessee Valley Authority submitted the first-ever permit application to the U.S. Nuclear Regulatory Commission (NRC) for a small modular nuclear reactor.

White hope or white elephant?

It’s easy to construct a compelling case for SMRs based on the potential benefits outlined above, but if the economics were as persuasive, there would be no need for the kind of state sponsored technology competitions currently being run by the US and UK governments and others. Even under the most ambitious scenarios, the first SMRs would not be running in the UK before the mid-2020s, at which point the market will look very different from today…a serious challenge for any investment case.

As we have seen with the significant state support needed for the next generation EPR, which is so far also technologically unproven, it seems likely that SMR will also struggle to get off the ground unless it receives similar assistance, meaning that the future of nuclear energy, in the UK at least, is very much in the hands of the government.

Leave A Comment