Despite the disruptions to the energy sector as a result of the pandemic, the Government remains committed to its 2050 net zero carbon target. The problem, as I have noted before, is that there are currently no technological solutions to achieve this – carbon capture and storage (“CCS”) is seen as a key enabling technology, yet there are no large CCS projects currently operating anywhere in the world that do not rely on hydrocarbon fuel production for their economics.

In a net-zero carbon world, one could imagine a greatly reduced requirement for hydrocarbons (there may be an ongoing requirement for them as a feed-stock but presumably use as a fuel will be all but eliminated). This suggests that without heavy subsidies or a technological breakthrough, CCS will not play a significant role.

An obvious route would be to expand the use of nuclear power. In high level terms, nuclear power is a proven technology that produces zero-carbon electricity. The major drawback is cost – the capital costs of new nuclear reactors are so large that they are beyond the reach of commercial organisations and rely on state support for financial viability. This is also true of small modular reactors (“SMRs”) which, although they individually have lower capital costs, will require expensive fabrication processes to be developed which have so far proved to be too large and risky for the financial markets to fund.

The Government is therefore faced with some difficult choices: there is pressure to pursue hydrogen as a means of de-carbonising hard-to-reach sectors such as heating and transport, and to support CCS trials. There is also pressure to provider greater levels of support to nuclear power, both in terms of large reactors and SMRs. In this post I will explore the current nuclear options facing the Government, and whether this is an area that should be awarded greater levels of state support in order to further the zero carbon agenda.

The prospects for new large nuclear power stations

A damning report underlines the issues with EPR technology

Regular readers will be familiar with my views of large nuclear in the GB market. I continue to be bearish on the European Pressurised Water (“EPR”) technology being developed by EDF at Hinkley Point C, and proposed for Sizewell C and Bradwell B. The route to market for the EPR has been long and difficult.

The first project at Olkiluoto in Finland saw yet another delay to the troubled, over-budget plant, having its previous commissioning date put back by a further 11 months. The reactor was already over 12 years behind schedule and three times over its original €3.2 billion budget. The flagship EPR at Flamanville in France has also suffered delays and cost over-runs, and a recent audit by the Cours des Comptes, the French public spending watchdog described it as a “failure” with “huge” financial consequences for the French nuclear industry.

“It is not only an exceptional documentation of the failures and mishaps of project management, engineering and huge financial consequences, it is foremost an unprecedented illustration of the total absence of state oversight,”

– nuclear industry critic and independent consultant Mycle Schneider, writing in the World Nuclear Industry Status Report 2020, published in September

The reactor is billions of euros over budget, a decade behind schedule and EDF’s latest start-date of 2023 may yet be pushed back due to the impact of the coronavirus. According to the auditors, the firm’s current €12.4 billion estimate of the construction cost is unreliable, and a further €6.7 billion may be needed before it enters service. Olkiluoto and Hinkley Point C also come in for criticism and even the two completed EPRs in Taishan, China are described by the auditors as showing “insufficient profitabilty”.

The audit report states that construction at Flamanville began when only 10-40% of the necessary assessments had been completed, and that EDF had estimated it could build the reactor in 54 months when the average lead time to complete reactors at the time elsewhere in the world was 121 months. It said it needed 5 million hours of engineering when it would actually require 22 million hours.

The UK Government should take note of this report in deciding whether to support EDFs other EPR projects.

ABWRs would be a better bet

There is a credible alternative to the EPR: the Advanced Boiling Water Reactor (“ABWR”) project mooted for Wylfa Newydd in Wales. ABWR technology was developed in Japan and South Korea, and two ABWRs were running successfully in Japan before the mandatory shutdown of all Japanese reactors after the Fukushima disaster in 2011. These had been built on time and on budget and had a respectable if short record in use.

I continue to be a supporter of this technology, and despite Hitachi’s withdrawal from the project, this is actually a lower-risk prospect from a technology perspective than most if not all of the other large-scale projects on offer for the furtherance of the net-zero ambition.

Hitachi’s withdrawal might have been the final blow for the project, but the Government has kept hope alive by extending the deadline for a decision on the planning application to the end of the year to allow time for the remaining developers to explore other options for the scheme.

At the same time, the Treasury is re-evaluating the regulated asset base (“RAB”) funding model to support private investment in new nuclear reactors, and may move towards a model that involves the Government securing some “upside” from its support for these projects, possibly by taking equity stakes. The Government reportedly offered to buy a third of the Wylfa Newydd project prior to Hitachi’s withdrawal, although a deal was not agreed. A white paper outlining the Government’s thinking is expected next month.

The prospects for small modular reactors

The other option for nuclear is at the other end of the size scale: small modular reactors. Britain is a leader in mini-reactors for powering submarines, and there are hopes that the technology can be leveraged to provide power for a wide range of static power applications. The idea is that the reactors would be small, modular to allow mass production efficiencies, and easily portable, able to be installed on site.

The hope is that Britain could become a major exporter of the technology, creating thousands of jobs in the process – an even more attractive prospect in these depressed covid-times, and, if an appropriate funding model can be developed, potentially more interesting than investing in large-scale projects given the greater side benefits.

To that end, the Government is apparently considering deploying up to £2 billion of taxpayer money to support the developing industry. (The developers of large nuclear projects also claim wider job-creation opportunities, but SMRs are a more reliable prospect in that regard since the lower capital costs make for easier investment decisions.)

SMRs can also be operated more flexibly than traditional nuclear reactors, making the a good fit for an increasingly flexible electricity system, although in truth there is room for both technologies if the electricity system were to move away from thermal generation.

“You need both, they are complementary. The attraction of SMRs is economies of volume: having lots of them which are cheaper to build – and that’s why ‘modular’ is key – but they don’t each generate so much. For traditional, big plants the attraction is economies of scale: they are expensive to build as it’s done on site, but they produce more at a lower price once up and running,”

– Tom Greatrex, chief executive of the Nuclear Industry Association

The major challenges facing SMRs are the high capital cost of developing the production processes for SMRs and the high levels of regulation around the nuclear industry, where it takes years to secure regulatory approval for new nuclear technologies. (Although this is not a new technology per se, its use in a new context means it is treated as such.)

According to Tom Samson, head of the UKSMR consortium, believes it will take a decade to get the SMR into operation and believes the cost will potentially exceed £2 billion, and require government support to drive through regulation and a commitment that another five SMRs will be ordered, each costing £1.8bn. That means that absent development problems, the start-up costs would exceed £10 billion. Overall, some 16 sites could be developed by 2050.

“This is not a new type of fuel or reactor, this is based on existing technology and there are no insurmountable challenges. But we need a commitment to a new fleet of SMRs so we can get the supply chain involved,”

– Tom Samson, head of the UKSMR consortium

Last November, the Government awarded the UK SMR consortium, which is led by Rolls-Royce and includes Assystem, BAM Nuttall, Laing O’Rourke, National Nuclear Laboratory, Atkins, Wood, The Welding Institute (TWI) and Nuclear AMRC, £18 million in matched funding to further develop the initiative.

Broadening the role of nuclear power

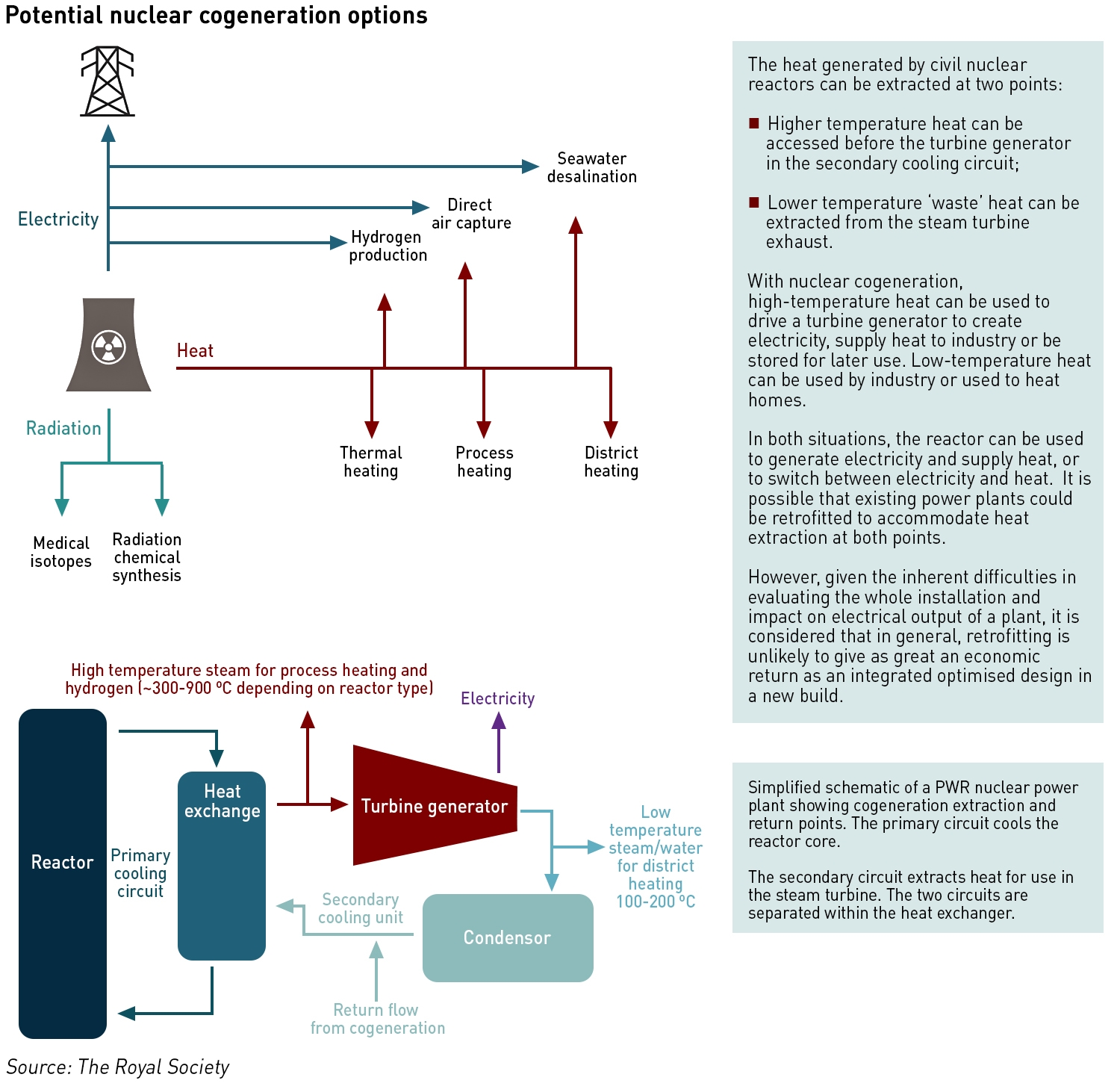

A policy briefing published in October by the Royal Society, Nuclear cogeneration: Civil nuclear energy in a low-carbon future outlines the need for more flexibility from the nuclear generation fleet, and suggests a co-generation model using either low temperature heat for district heating and/or or high-temperature heat for industrial applications including the production of hydrogen.

The Government has identified district heating as an important route to de-carbonising heating, but currently only around 2% of UK heat demand is met this way. Several countries already use nuclear cogeneration for district heating, and the Royal Society’s analysis suggests there may be 50 urban areas which could be suitable for SMR-powered district heating, although, “public opinion and acceptance of nuclear reactors being sited close to population centres would need to be examined”.

Nuclear energy in the UK is currently only used to generate baseload electricity – reactors work best if operated at a constant full capacity, and can encounter problems when ramped too often as seen with the Brockdorf reactor in Germany. As noted above, an electricity system that is increasingly dependent on intermittent renewable energy gives rise to the need for more flexible dispatchable assets, particularly as a low-carbon world pushes thermal plant out of the mix. Cogeneration could facilitate this by enabling switching between electricity generation and the provision of low carbon heat.

“Nuclear energy has the potential to help the UK to achieve net-zero carbon emissions by 2050, not only through the generation of low-carbon electricity but by more fully utilising the generated heat. This could support the UK taking a ‘whole systems’ view of future energy production and use by addressing difficult to decarbonise energy demands,”

– Royal Society

The report highlights SMRs as being of particular interest, their modular nature allowing plants to be tailored to the specific needs of regional or industrial clusters. Next generation of SMRs – known as Advanced Modular Reactors (“AMRs”) – are expected to generate temperatures in excess of 600°C which is what some of the hardest to de-carbonise industrial processes require. It could even potentially be used in the notoriously difficult steel industry.

Work will need to be done to secure public support for siting nuclear reactors close to communities, but there is precedent for this as existing nuclear facilities are also located close to communities whose residents often have jobs at the plants.

.

The phrase of the moment in energy seems to be “build back better” and the net-zero target is still firmly on the agenda. This will cost money and the Government will need to choose where to spend its limited financial resources. Nuclear power is one of the strongest candidates for this investment, but the time has come for the Government to commit, which so far it has been reluctant to do.

Nuclear power is a tried and tested technology, far more so than CCS or hydrogen (although nuclear could be used to support hydrogen), and it would make sense for the Wylfa Newydd project to be supported and for the seed investment for SMRs to be found. The longer these decisions are delayed, the higher the costs are likely to be as the clock runs down on the 2050 target. Nuclear power is expensive, beyond the reach of most private companies, and therefore it is in need of state support. That support should be forthcoming.

“…According to Tom Samson, head of the UKSMR consortium, believes it will take a decade to get the SMR into operation and believes the cost will potentially exceed £2 billion…”

This is from the 2020 Edition of the IAEA ARIS publication: ‘Advances in Small Modular Reactor Technology Developments’, in respect of GE Hitachi’s BWRX-300 SMR. Note: the design was ‘lodged’ with our BEIS in 2018:

12. Development Milestones

2017 Conceptual design started

2018 BEIS funded Mature Technology Evaluation the UK ONR

2019 Pre-application activities initiated with the US NRC

2020 Combined Phase 1 and 2 Vendor Design Review initiated with CNSC in Canada

2022 First construction permit applications expected to be submitted

2024 Start of construction for first unit expected

2027 Commercial operation of first unit expected

And the UK OCC for an NOAK, made under licence in the UK (say by 2030) would be £587 million. Pro rata, that would have an OCC of £6.26 billion for 3,200 MW, compared to thew £20 billion for Sizewell C.

It would be good to know what Tom Samson thinks about all of this.

Hi Kathryn…..thanks for a great informative article.

Waving my local flag yet again.

Hopeful that Heysham 3 be included as one of the 16 possible UK sites.

I believe a licence for a 3rd nuclear facility adjacent to Heysham 1 & 2 is in place.

The existing Heysham Energy Gateway offers a robust supergrid connection close by.

I believe the UKSMR consortium has set up its HQ in west cumbria

Encouraging to learn the area is becoming a key location for SMR development.

Finally do you have a view on a likely outcome on the part complete Moorside nuclear facility ?

Barry Wright, Lancashire.

I’m sure the public have no concept of the scale of the wind farms required to equal that of a thermal super generator.

Imagine 300 sq. km of Morecambe Bay populated with some 125 wind turbines.

With a total output of approximately 30% more than a single 600 mw generator.

The latter operates 24/7 delivering carbon neutral energy over 2 years subject to breakdowns.

Just 50% of Heysham 2 capacity which powers 2 such units.

Intermittency of output, zero inertia & non synchronisation all create major problems for National Grid.

Finally the visual impact of wind farm sites both on & off shore are not everyone’s cup of tea.

My sense is that Moorside is dead, and the technology (AP 1000) is also pretty untested – there are a couple in China and one being built in the US.

This article has more and also mentions NuScale is developing some 60 MW SMRs in the US.

I agree that the public has no idea about the relating output of different generating technologies, and how much more wind would be needed to achieve net zero (and how hard/expensive it will be given the “easy” sites are already taken).

Apologies to everyone for responding so late to the comments – my email system decided they were all spam! I’m trying to re-educate it!

Mmm. Not sure, but my recollection is that the final stages of a big steam turbine have the water at below 100°C… A minor detail in an otherwise excellent article.

Also there are other advantages to SMRs. If small enough the surface to volume ratio can be enough to support entirely passive emergency cooling under SCRAM scenarios, eliminating huge swathes of safety equipment.. and type approval can reduce dramatically the cost of commissioning. It is not clear wither why SMRS should be more expensive to run. The cost of running a nuclear set is almost all in maintenance. (apart from interests on capital)/

Does anybody out there have any idea of the likely MW capacity of SMR’s ?

Barry Wright Lancashire.

SMRs are defined as being below 300 MW but what the typical size would be isn’t clear yet as far as I know.