A few months ago I wrote a series of posts about the critical minerals needed to support the energy transition and promised a similar look at uranium. Client work has been keeping me busy, but here, finally, I will cover the topic in a small series of posts. I will start with the nuclear fuel cycle, going on to looking at mining and enrichment, followed by fuel production and then geopolitical risks.

Nuclear is increasingly recognised as an important enabler of net zero

Nuclear power does not produce carbon dioxide emissions in operation, and as it lacks the intermittency that characterises a lot of similarly zero carbon renewables, it is increasingly seen as a key enabler of the energy transition. New projects are being developed across the world, and the lives of existing reactors extended.

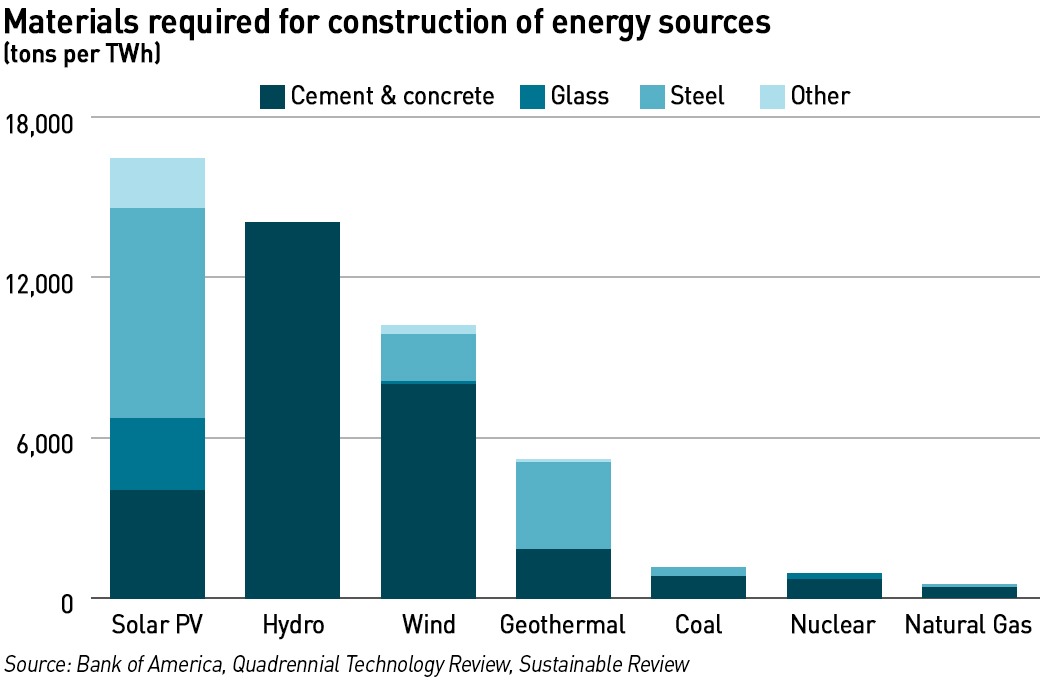

I have long been ambivalent to the introduction of intermittent renewables – while I rejected the arguments that they are cheap, I had no particular objection to their inclusion in the electricity generation mix. But since researching the materials requirements for renewable generation, I have formed a view that they represent an inefficient use of both capital and mineral resources, and are ultimately likely to prove unsustainable in all senses of the word.

I believe that sustainability is important. We should seek to use resources efficiently and minimise waste. We should seek to minimise our impact on the environment, whether that is by not littering or by choosing the most effective forms of energy. And to this end, I do not believe that intermittent renewables, and in particular wind power, satisfy these criteria when the full life-cycle and supply chains are taken into account.

As I described previously, some of these choices may be taken out of our hands – communities living in resource-rich regions may object to the mining and processing needed to provide the minerals needed for these technologies, given the adverse impact on their local environments, and the social, labour and human rights abuses that can accompany these activities.

But then we must answer the question of how we will make our energy supplies cleaner if not through renewables. The answer is through increased use of nuclear power, which not only has zero carbon dioxide emissions in use, its high energy density means very large amounts of electricity can be generated from small geographic sites, with minimal requirements for additional grid infrastructure – large units of generation fit perfectly with power grids since this is what grids were designed to accommodate. Intermittent renewables such as wind and solar have very low energy density meaning much more land is required to generate equivalent amounts of electricity, and their dispersed nature means more wires, transformers and other grid equipment is needed to connect them up. Nuclear is fundamentally more efficient than intermittent renewables.

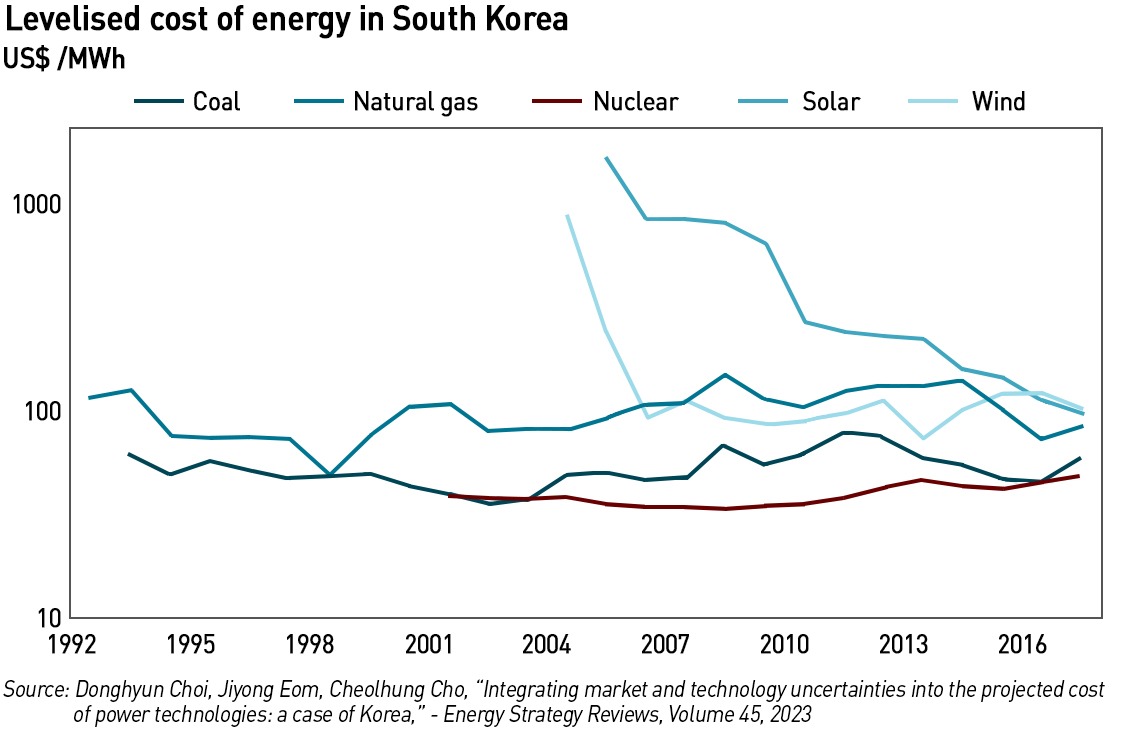

Of course many people believe nuclear is too expensive. There are two ways to define “too expensive” – one is that it costs too much and the other is that it costs more than it should. In the west the latter is true. This article contains a comprehensive analysis which shows that very clearly – newbuild nuclear in South Korea is cheaper than all of the other alternatives. Nuclear regulation in the west and the mindless pursuit of ALARP is inflating costs un-necessarily.

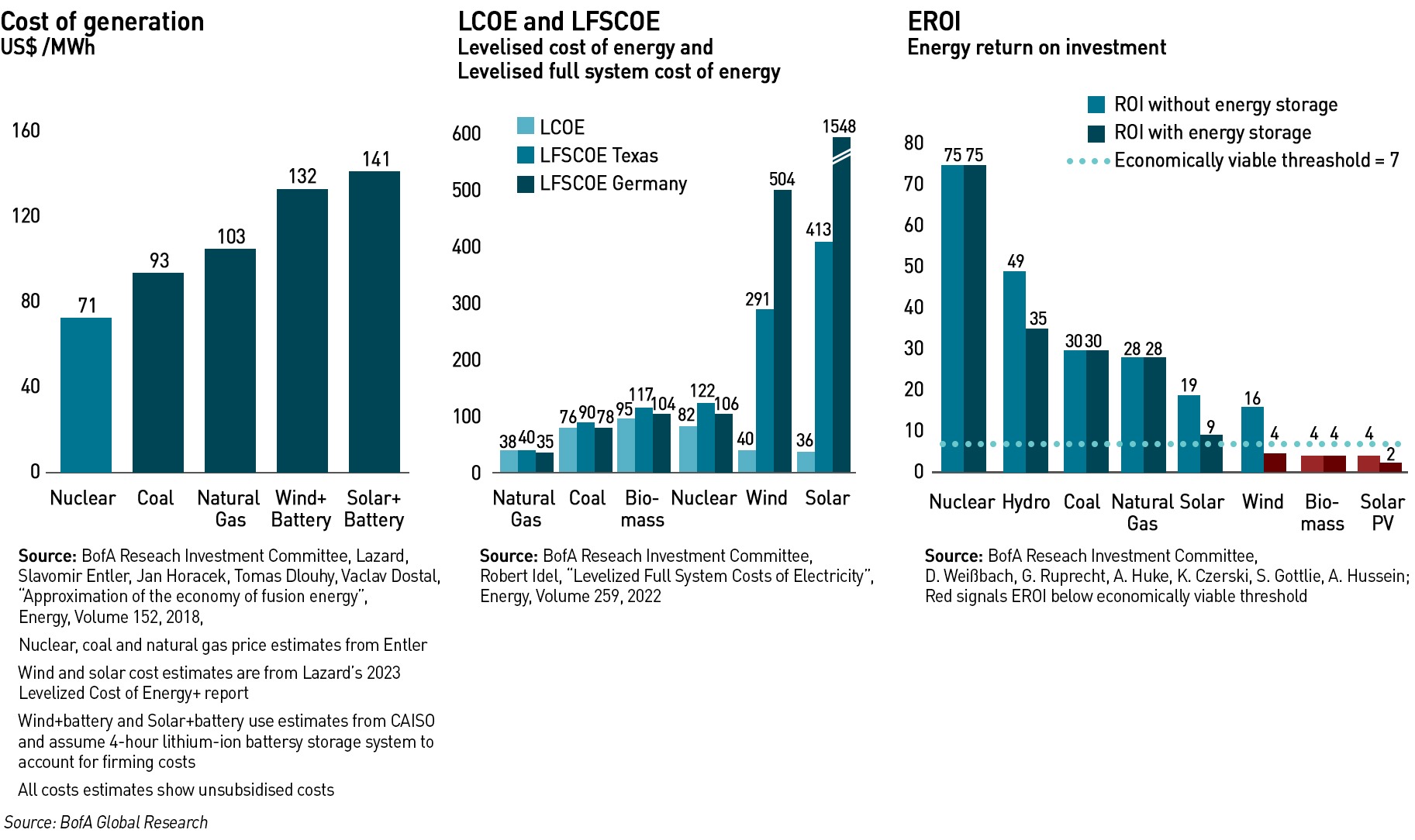

Appropriately regulated, nuclear can be cost competitve with other generation technologies when the full cost impact to consumers is taken into account. Even in the west, nuclear is cost competitive compared with off-shore wind when full costs are taken into account, as this analysis from Bank of America demonstrates. Nuclear also has the best EROI (energy return on investment)

Strong demand for uranium

Nuclear power currently provides about 10% of the world’s electricity, and 18% of electricity in OECD countries.

The International Atomic Energy Agency (“IAEA”) has materially increased its forecasts for nuclear power in recent years – in both its high and low case scenarios, the Agency now sees a quarter more nuclear energy capacity installed by 2050 than it did as recently as 2020. In its high case scenario the IAEA expects nuclear installed capacity to more than double by 2050 to 890 GW, and in its low case, capacity increases to 458 GW.

“Climate change is a big driver, but so is security of energy supply. Many countries are extending the lifetime of their existing reactors, considering or launching construction of advanced reactor designs and looking into small modular reactors (SMRs), including for applications beyond the production of electricity,”

– Rafael Mariano Grossi, Director General of the IAEA

The World Nuclear Association expects global demand for uranium for nuclear reactors to climb by 28% to 2030 and nearly double by 2040 as governments around the world ramp up nuclear power capacity to meet net zero targets, with additional uranium mines being needed to meet this demand.

Global nuclear capacity was 391 GW from 437 units at the end of June 2023, with another 64 GW under construction. Capacity is expected to rise by 14% to 2030 and by 76% to 686 GW by 2040, with new plant, the re-opening of Japanese reactors closed after Fukushima, and life extensions for existing reactors all contributing to this growth. As a result, demand for uranium is expected to rise from 65,650 this year to 83,840 tonnes by 2030 and 130,000 tonnes by 2040.

According to Ted Jones, the Senior Director for National Security and International Programs at the Nuclear Energy Institute, Central and Eastern Europe is “probably the hottest market” for nuclear power at the moment. These are countries with energy intensive economies that currently rely on coal for much of their power generation. They have also been wary of relying on Russian energy even before the invasion of Ukraine. The Czech Republic, Poland, Romania, Bulgaria and others are looking to buy plants that are already in operation as well as developing new projects of both conventional designs and small modular rectors.

Another driver of interest in nuclear is from the tech sector where the growth in Artificial Intelligence is causing huge increases in energy consumption – Google has seen its greenhouse gas emissions increase 48% in five years as a result. According to the Wall Street Journal, the owners of around a third of US nuclear power plants are in discussions with tech companies to provide electricity to the new data centres they will need to meet the demands of the AI boom. The newspaper cites sources that claim Amazon Web Services is close to a deal with Constellation Energy to buy electricity directly from a nuclear plant on the East Coast, and in a separate deal in March, the company purchased a nuclear-powered data centre in Pennsylvania for US$ 650 million.

At the moment these deals are focusing on existing reactors, but there are also some deals looking at new-build plant. Last year Microsoft signed a deal with Helion Energy, a private US nuclear fusion company with a view to receiving electricity from its plant in about five years’ time (although as this is a fusion plant, that schedule could be ambitious).

Sources of uranium for nuclear reactors

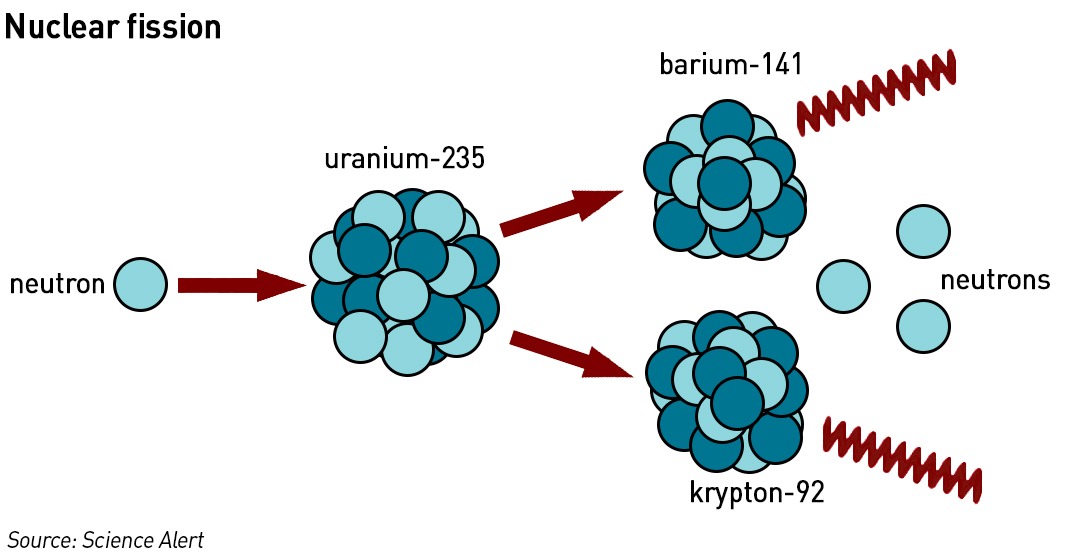

Nuclear reactors are powered by fuel containing fissile material. The fission process releases large amounts of energy and for this reason the fuel must be held in a robust physical form capable of enduring high operating temperatures and intense neutron radiation. Fuel structures must maintain their shape and integrity over several years within the reactor core, without leaking fission products into the reactor coolant.

Nuclear power stations typically use uranium-235 because its atoms are relatively easy to split apart. Although uranium is about 100 times more common than silver, U-235 is relatively rare, at just over 0.7% of natural uranium. The reactors currently in operation around the world, with a combined capacity of around 400 GW, require about 67,500 tonnes of uranium each year. The factors increasing fuel demand are offset by a trend for higher burn-up of fuel and other efficiencies, so overall demand is holding steady – between 1980 and 2008 the electricity generated by nuclear power rose by a factor of 3.6 times while the uranium used only increased by a factor of only 2.5.

The world’s current measured resources of uranium that can be extracted for a cost up to three times current spot prices represent enough to last for about 90 years. As well as existing and likely new mines, nuclear fuel can be derived from secondary sources including:

- Recycled uranium and plutonium from used fuel, as mixed oxide (MOX) fuel

- Re-enriched depleted uranium tails (the process waste from uranium mills)

- Ex-military weapons-grade uranium, blended down

- Civil stockpiles

- Ex-military weapons-grade plutonium, as MOX fuel.

Military uranium for weapons was enriched to much higher levels than that for civil nuclear applications. Weapons-grade material is about 97% U-235, which can be diluted about 25:1 with depleted uranium (or 30:1 with enriched depleted uranium) to reduce it to about 4%, suitable for use in power stations. From 1999 to 2013 the dilution of 30 tonnes per year of such material displaced about 9,720 tonnes U-3O8 per year of mine production.

Access to uranium through reprocessing nuclear fuels is limited

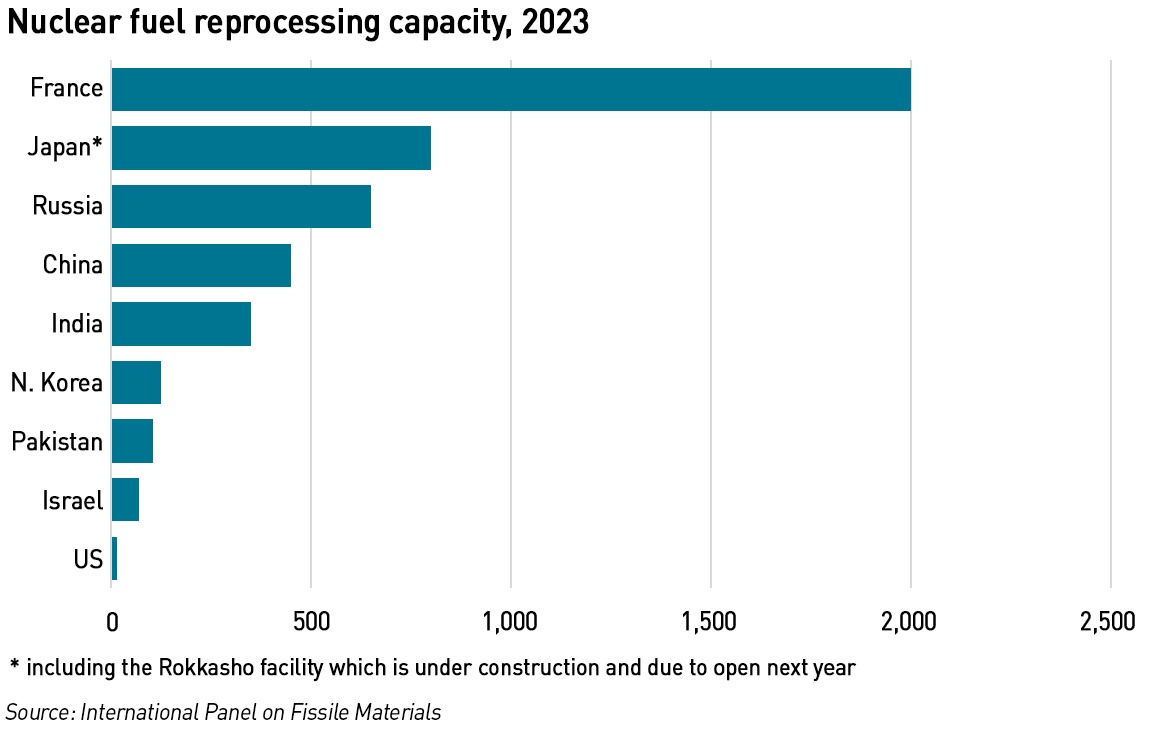

Global reprocessing capacity is limited and highly concentrated in a few countries with estimates of global capacity varying from about 2,000 tonnes of heavy metal (“tHM”) following the end of reprocessing activities at Sellafield in the UK, to 4,000 tHM per year.

France currently dominates the market with 55% of reprocessing capacity, with MOX fuel powering about 10% of the country’s nuclear output. Russia has 18% and China has 12%. However, following the opening of the 800 tHM Rokkasho plant in Japan, expected later this year, Japan will overtake Russia as the second largest recycler of spent nuclear fuel, although capacity is also under construction there and in China.

The only method of reprocessing used commercially is PUREX, or plutonium uranium reduction extraction. This process separates spent-fuel byproduct, typically combining the uranium and plutonium into a “mixed oxide fuel,” or “MOX”. However, since the process isolates very pure plutonium, there are concerns in relation to nuclear weapons proliferation, leading to extensive oversight from domestic and international safety regulators.

While there is no law banning reprocessing in the United States, the country does not currently engage in national reprocessing efforts, other than at a small facility at H-Canyon, part of the Savannah River Site in South Carolina. At the start of the commercial nuclear industry, the United States was a clear nuclear technological leader, including on reprocessing, which was carried out at the West Valley Demonstration Project in New York and the Savannah River Site in South Carolina. The West Valley plant recovered 1,926 kilograms of plutonium and 620 metric tons of uranium during its operation from 1966 to 1972. The Hanford site in Washington state housed a PUREX reprocessing facility for military applications, which operated intermittently from 1956 to 1988.

As a result of proliferation concerns, the Carter Administration issued an executive order in 1977, diverting federal funding and support away from nuclear fuel recycling, in the hope of setting a global precedent against recycling fuel, to set clear boundaries between the power sector and weapons production. In the following years, support for reprocessing and recycling flip-flopped between presidents, and this political uncertainty, along with low prices for uranium and stagnant demand, led to the lack of a comprehensive programme for spent fuel recycling in the US.

However, as with other aspects of the nuclear industry, sentiment towards reprocessing is also changing around the world, as concerns over access to uranium grow. There are now several projects evaluating the feasibility of spent-fuel recycling in the US. ARPA-E, a research agency within the US Department of Energy, has funded 12 reprocessing-related research projects through its CURIE program to research novel reprocessing technologies and 11 projects through its ONWARDS program to optimise waste from new reactor designs.

.

In the next post I will look at the supply of nuclear fuel from primary (mined) uranium.

One potentially interesting consideration was flagged to me by one of my readers, and that is the impact of electricity price volatility on the mining sector. Magnus Soederberg, Professor of Economics at Griffith University in Australia has analysed the impact of electricity prices on the valuation of listed firms that operate in the Basic Materials (metals and mining) segment. He finds that these firms lost over 5% of their value in 2023 as a result of higher electricity price volatility. Since the Basic Materials segment in Australia is valued at around A$ 40 billion so that reduction corresponds to A$220 per household, which is a substantial loss given that the average household spends $2,000 per year on electricity.

Soederberg argues that nuclear power reduces electricity price volatility and is therefore positive for the important Basic Materials sector in Australia. The increased interest in nuclear power globally would therefore reduce the upwards trend in price volatility and therefore support the valuation of these companies. The sector in Australia would benefit despite the fact that local electricity prices would remain volatile since so far Australia has failed to lift its moratorium on nuclear power, although there are growing calls for this to be reversed.