In July, National Grid published its 2018 Future Energy Scenarios, with the following headlines:

- Capacity could increase from 103 GW today to between 189 GW and 268 GW by 2050, with the more decarbonised scenarios requiring the highest capacities. Up to 65% of generation could be local by 2050.

- High levels of intermittent and inflexible generation will require high levels of new flexibility, and there may be some periods of oversupply. Interconnectors and electricity storage will play a key role in easing this.

- The changing generation mix also means new ways to maintain system balance will have to be found.

The scenario framework has changed again, for the second year running, moving from a focus on Prosperity/Green Ambition to Level of de-centralisation/Speed of de-carbonisation, to reflect the falling costs of de-carbonisation technologies.

The speed of de-carbonisation axis is driven by policy, economics and consumer attitudes, whereas the level of decentralisation axis indicates how close the production and management of energy is to the end consumer, moving up the axis from large scale central, to smaller scale local solutions.

The Future Energy Scenarios are produced by National Grid as a marker of potential outcomes to understand their impact on the gas and electricity networks operated by the company, and to facilitate long-term planning. They do not therefore represent what National Grid thinks will happen, or what it would like to see happen, so should not be seen as predictions. They do however provide some insights into the outcomes the system operator is evaluating, in terms of future network planning.

National Grid sees de-carbonisation and de-centralisation as the key themes for the future of the GB energy systems

De-carbonisation

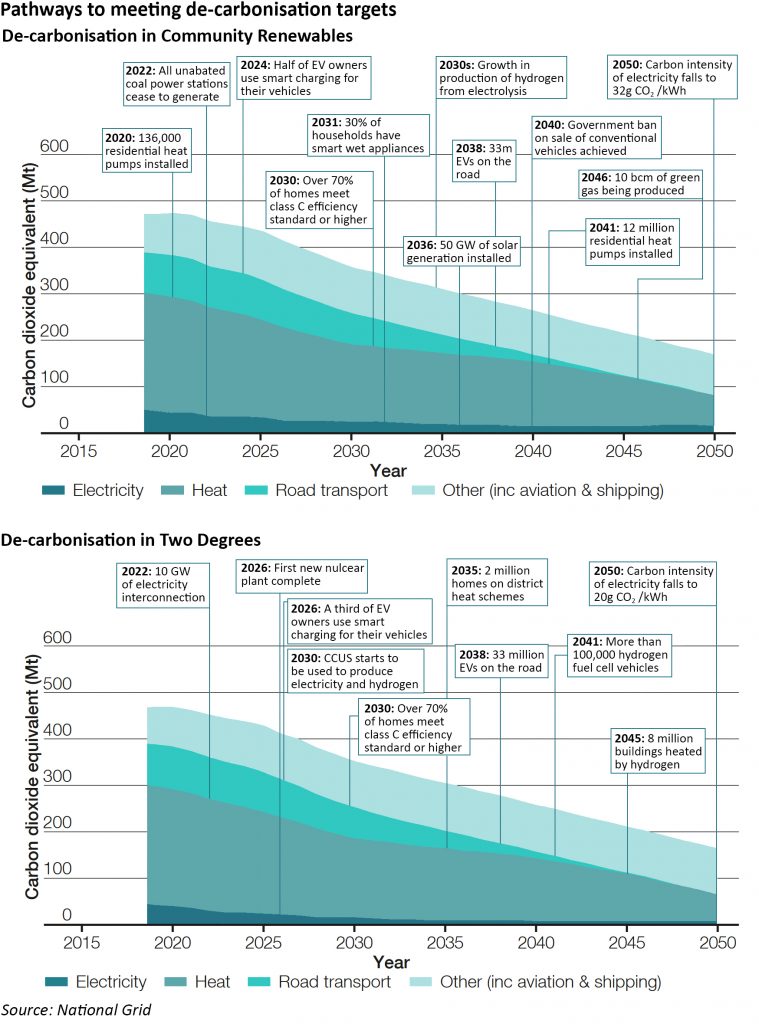

National Grid presents two scenarios in which 2050 targets are met, and illustrates the pathways taken to compliance in each case:

The Community Renewables scenario sees the greatest amount of load-shifting by domestic consumers, with high take-up of EVs and smart appliances, alongside high levels of renewable generation – there could be 60 GW of onshore wind in this scenario, which National Grid has said is at the top end of possible capacity assuming re-powering existing facilities with the latest technology.

In the Two Degrees scenario there is rapid growth of interconnection (assumed to be zero-carbon for the UK), alongside large new nuclear plant, which together with use of CCS with gas-fired generation sees almost complete de-carbonisation of electricity generation by 2050.

De-centralisation

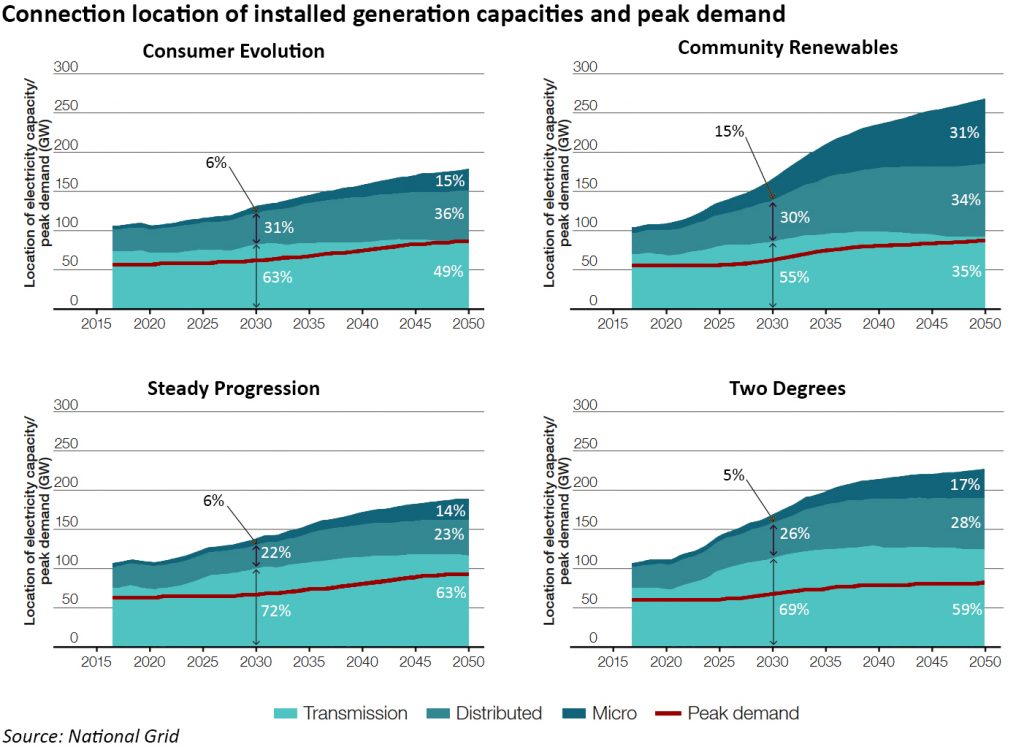

De-centralised generation is generation that is located close to consumers. In the de-centralised scenarios, there are more small scale intermittent generators connected to the medium and low voltage networks, requiring a larger amount of installed capacity to mitigate against the effects of their intermittency. Currently, there is 103 GW of generation capacity on the system, comprised of 73% transmission-connected, 23% distribution-connected and 5% micro-generation.

Low levels of transmission-connected generation has implications on balancing the transmission system given the low levels of flexibility of baseload generation such as nuclear.

As the network becomes more decentralised, power flows become more complex and potentially more volatile. In the past, power flowed from remote large generators through the transmission system, down though distribution networks to the consumer, however with de-centralisation this changes in a number of ways depending on the weather.

National Grid describes this with the following example: on cold windy nights there would be no output from solar panels in the south of England while small wind farms in Scotland could be generating significant amounts of electricity. However on still, sunny days, the opposite could be true, so although neither type of generation is connected to the transmission system, the transmission system is still needed to move power from to point of production to the point of consumption. This is an important observation in the context of Ofgem’s current consultation on transmission charging. Power flows can also change quickly as weather conditions change.

The grid must also be balanced, and operated within allowable frequency tolerances, which means that the majority of supply at a particular moment might be produced by solar generation in the south, with frequency reserve coming from gas plant in the Midlands.

At the same time, distribution-connected generation is not visible to the transmission system operator further increasing the complexity of balancing and managing the grid.

Electricity demand is expected to rise significantly driven by the electrification of transport and heating

The pathway to the de-carbonisation of transport is already emerging with the availability of electric vehicles (“EVs”). National Grid expects this trend to continue, with as many as 11 million EVs by 2030 and 36 million by 2040. However smart charging and vehicle-to-grid technologies could see the increase in peak electricity demand limited to as little as 8 GW in 2040. EV-related tariffs are staring to appear, and current trials of virtual power plants connecting domestic batteries could be a sign of things to come.

The de-carbonisation of heat is seen as a key requirement if 2050 targets are to be met, however the pathways here are less clear, with the debate only just beginning. In its scenarios, National Grid has identified a number of ways to achieve the de-carbonisation of heating, and believes that up to 60% of homes could be using heat pumps by 2050, with green gas, smart heating technologies and improved building energy efficiency contributing. Alternatively, a third of homes could be heated by hydrogen in 2050, with low carbon district heating, hybrid heat pumps and micro combined heat and power all playing a part.

“…consumers may change their car every 3 to 5 years, but are unlikely to change their boiler more than once in a 10 to 15 year period. Many boiler replacements take place following a breakdown as a distressed purchase, so there is less opportunity to consider changing heat sources.”

National Grid expects that minimum demand on the electricity transmission network will move from early in the morning to around 2pm on a summer weekend day, as happened for the first time in March 2017, driven by the growth in distribution-connected solar generation. The speed of this change is scenario specific.

Electricity supply will rise to meet higher demand and be increasingly de-centralised

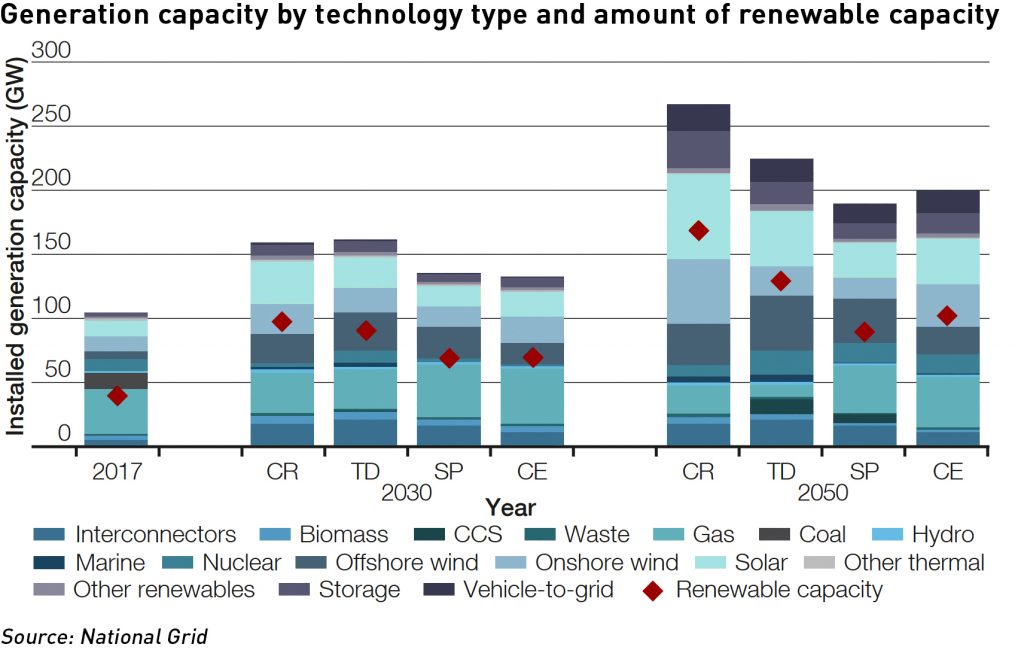

All scenarios see high levels of generation growth, with the highest levels in the 2050 compliant scenarios, and higher levels of de-centralised electricity than today. Offshore wind grows strongly in all scenarios, as does solar capacity, although the range across the scenarios is larger for solar than for wind. Greater levels of flexibility are required in all scenarios, and CCUS features in two of the scenarios.

All scenarios see a greater role for interconnectors than today, with gas only declining in the more de-carbonised scenarios after 2030. In 2050, the most de-centralised and de-carbonised scenario, Community Renewables would have around 40% more installed generation capacity than the least de-centralised and de-carbonised scenario, Steady Progression, however both will be dominated by wind generation in 2050 with a significant contribution from nuclear.

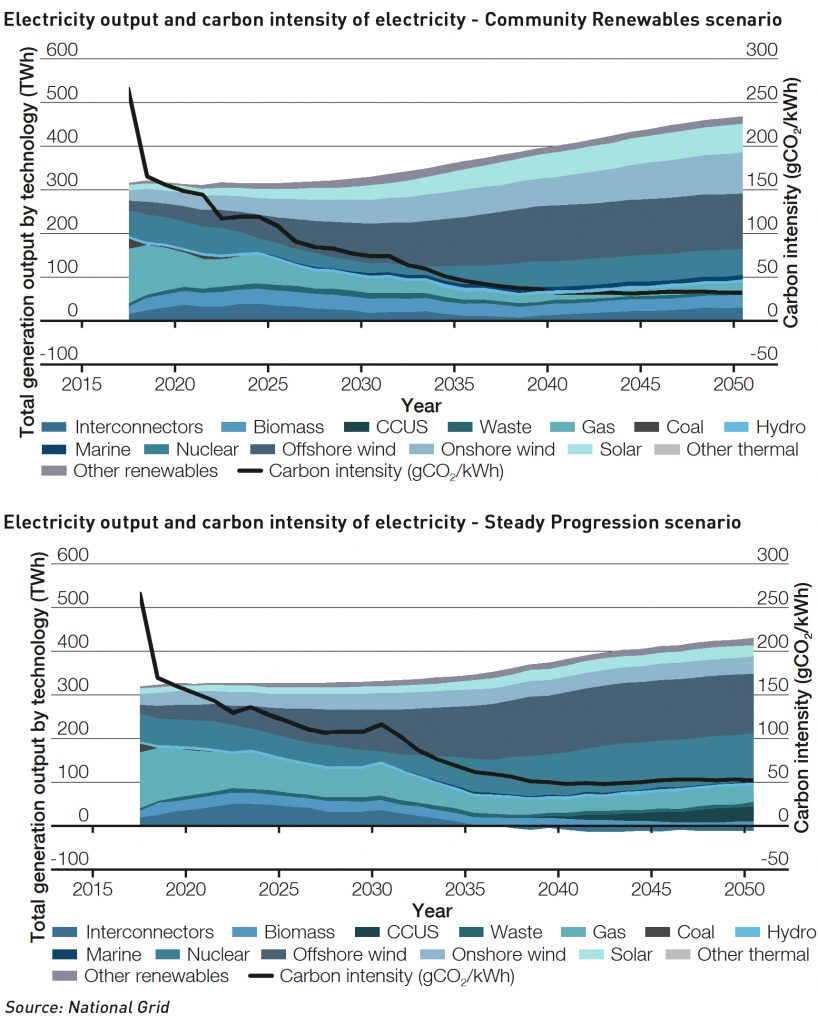

The fall in carbon intensity of the electricity system across the two scenarios to 2050 is interesting, falling to 32gCO2 /kWh in Community Renewables and 52gCO2 /kWh in Steady Progression. In 1990, the carbon intensity of the electricity system was 718gCO2 /kWh in 1990 which fell to 529gCO2 /kWh in 2013 and then to 266gCO2 /kWh in 2017.

The 2050 targets require a fall in greenhouse gas emission to 80% of 1990 levels, which for the electricity system alone would mean a drop to 148gCO2 /kWh, although the Climate Change Committee recommended a target of 50gCO2 /kWh in 2030 to support to economy-wide target.

National Grid expects the supply of electricity, rather than demand, to become an increasingly important driver of when electricity is used (through time-of-use tariffs, smart appliances that respond to price signals etc). This will result in more complex energy flows across the networks and increased challenges in balancing and system management.

In the 2018 scenarios, National Grid is projecting that with the increase in renewables, there may be times when supply exceeds demand in some periods, leading to new challenges in managing excess supply, and does not believe that current commercial frameworks will to be able to manage these challenges.

The FES models are now taking into account the levels of de-carbonisation in markets connected to GB, and considering that the rate of de-carbonisation may be higher in some of these markets, meaning it may not be possible to export surplus supply (and although it is not mentioned in the report, the same argument should apply in terms if imports where there is a high degree of weather correlation between the interconnected markets).

The electricity system will need to become more flexible to accommodate expected future trends

Demand side

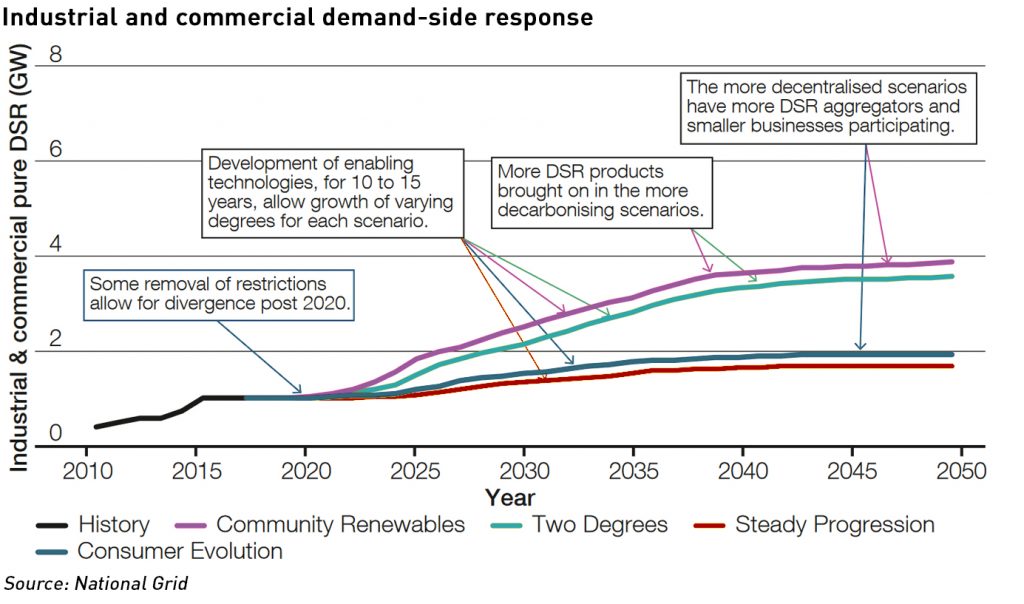

National Grid is not forecasting significant changes in the overall levels of turn-up/turn-down demand-side response (“DSR”) across its scenarios for the next few years, however after 2020 some barriers, such as the complexity of the marketplace, are expected to ease resulting in divergence between the scenarios.

From the early 2020s to 2040 National Grid is forecasting growth in enabling systems, such as communications technologies, which drive the development of DSR in all the scenarios. After this, growth is expected to decline. The most significant differentiator in DSR take-up between the scenarios is de-carbonisation – more DSR products are expected to enter the market in scenarios with higher renewable generation where businesses will earn income through providing balancing services through use of DSR, as well as being able to realise cost savings through load-shifting to cheaper times of day.

In the scenarios with lower de-carbonisation there are fewer drivers for DSR. In the de-centralised scenarios the DSR market develops to include smaller businesses and more local aggregators.

96% of the time, non-commercial vehicles are not being driven, so could be used to provide vehicle-to-grid (“V2G”) services. National Grid expects V2G participation to increase from 2% in all scenarios in 2030, to between 11-14% in 2050, increasing beyond the expected market saturation point of EVs by 2040. National Grid suggests in its report that V2G technology could deliver 8 GW of supply during times of peak electricity demand in 2040.

Modelling indicates that the level at which V2G becomes meaningful occurs at a relative low level of owner participation. Driving tends to use relatively little electricity, so in most non-commercial cases, there is significant under-utilisation of battery capacity. The models also apply de-rating factors to EV batteries to ensure comparable treatment with other forms of electricity storage.

Supply side

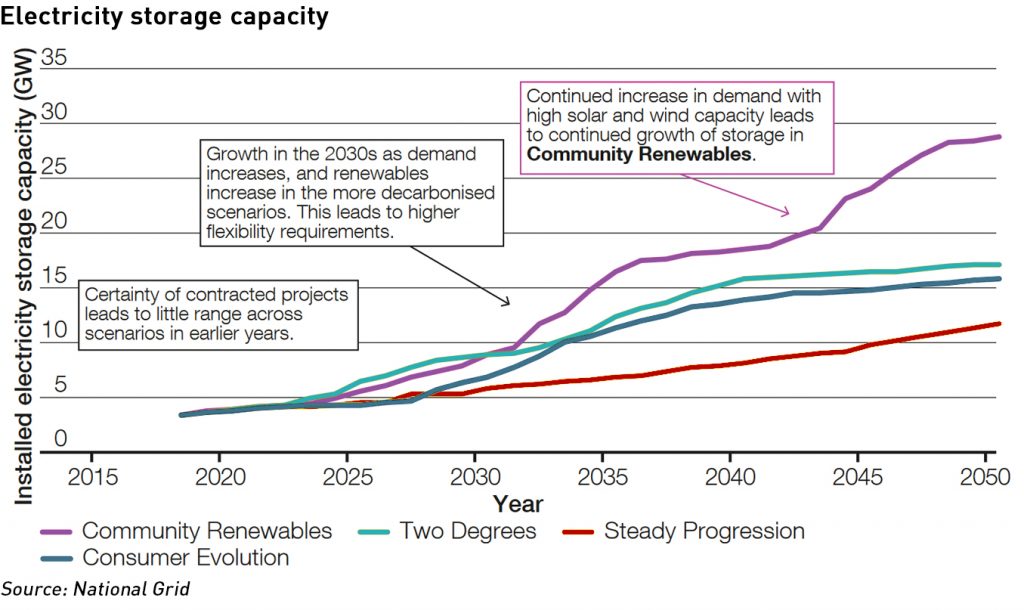

Storage and interconnector capacities are expected to grow in all scenarios, and the economics of thermal plant will rely on their ability to deliver flexibility.

National Grid assumes that storage providers will need to stack revenues from a number of sources to be economically viable. This could include arbitrage, balancing and ancillary services, and providing services to network operators. Its modelling of storage capacity and energy requirements is increasingly driven by the need for storage to absorb excess energy from inflexible or intermittent generation at times of low demand. Storage is also expected to increasingly co-locate with thermal as well as renewable generation enabling developers to sell a broader range of services.

Beyond 2030, National Grid expects to see a marked increase in electricity storage capacities in most scenarios. In some scenarios such as Community Renewables, this is driven by expected consumer behaviours, for example, co-location of storage with solar, including at the domestic level. In other scenarios the growth in storage is assumed as being necessary to support high levels of intermittent generation on the system.

This requires an implicit assumption that the necessary commercial frameworks and revenue streams will develop to support this amount of storage, which is interesting as National Grid has previously indicated that the requirement for frequency response will only be around 2 GW yet the storage scenarios all far exceed this.

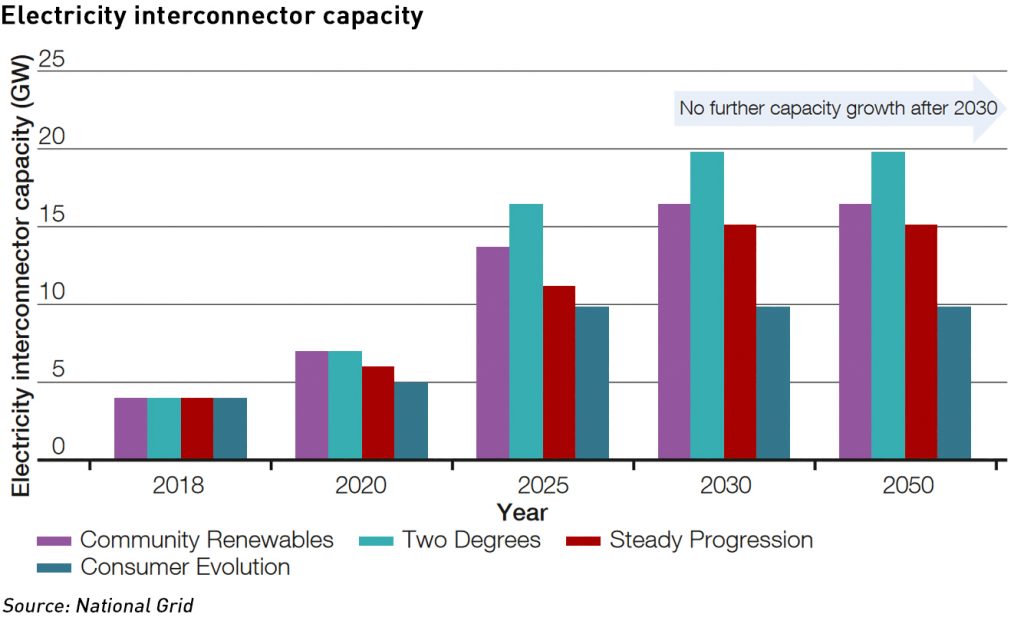

In considering the role of interconnectors, National Grid uses a pan-European dispatch model to study cross-border energy flows, together with a number of scenarios for the connected European markets. Its analysis assumes continued market harmonisation between GB and Europe following Brexit, including an assumption that GB will continue to participate in the Internal Energy Market, or similar future arrangements.

Interconnection is generally higher in the 2050 compliant scenarios, because of the need for greater levels of flexibility to balance intermittent output from renewable generation. However, in scenarios with greater de-centralisation, capacity is likely to be lower, with flexibility more likely to be provided by smaller scale projects, such as domestic storage or distribution connected thermal plant.

Consumer Evolution, as both a more de-centralised and more slowly de-carbonising scenario, sees the lowest level of capacity built, while Two Degrees has the highest. In all scenarios, no new interconnector projects are built after 2030, as prices between the connected markets converge.

National Grid expects that GB will be a net importer of electricity for most of the 2020s, as the carbon price floor will play an important part in driving imports. However, its carbon price assumptions see EU ETS prices increasing to the point where carbon pricing us no longer a driver of cross-border electricity trading. This is expected to occur in the 2020s in Two Degrees and Community Renewables, but not until the 2030s for Consumer Evolution and Steady Progression.

After the mid 2020s, Two Degrees starts to see net exports to connected markets, driven by excess supply at times from nuclear and renewable capacity. A similar trend emerges in Steady Progression in the 2030s. In the more de-centralised scenarios, there is less baseload generation driving exports , and imported electricity provides flexibility to support renewables, particularly in the Community Renewables scenario.

GB would be a net importer during times of peak demand in all scenarios, driven by high peak prices in GB at times when relatively cheap nuclear and hydro baseload generation will be available in France and Norway. While this may well be the case for Norway, analysis of actual interconnector flows suggests that GB exports to France in times of peak winter demand since the higher temperature sensitivity of the French system sees demand in France grow faster in cold weather.

It is not clear from the National Grid scenarios that electric heating is rolled out in the GB market to a degree that would change this dynamic, although in its FAQ document it says that all of its scenarios are consistent with the electricity security of supply reliability standard of 3 hours loss of load expectation per year.

National Grid sees an ongoing role for thermal generators in providing flexibility to the electricity system, and is undertaking work at the moment to understand how the combination of plant closures with increasing intermittent generation impacts the requirements for services such as system inertia and reactive power.

All the scenarios see unabated coal generation phased out by 2025 in line with government policy, with the earliest exit date in 2022 in the Community Renewables scenario, and the latest exit in 2025 in Steady Progression.

Carbon capture utilisation and storage

CCUS, as a large-scale technology, features in the two more centralised scenarios – Two Degrees and Steady Progression, where CCUS is expected to be used alongside gas-fired generation to provide low carbon electricity.

In Two Degrees, CCUS is also used with steam methane reforming to produce low-carbon hydrogen. National Grid expects the use of CCUS for both hydrogen production and electricity generation will help to build a scalable market for the technology, reaching commercial viability in 2030 in the Two Degrees scenario, with 12 GW of CCUS gas-fired generation in 2050. On the other hand, in Steady Progression, CCUS is predicted to only be used with gas-fired electricity generation, meaning the technology develops at a slower pace.

The question is whether these assumptions have been developed by examining the current state of CCUS technology and drawing realistic conclusions about the progress of the technology or whether a top-down approach has been taken, where the technology is assumed to emerge because without it the 2050 targets would be difficult to meet. The latter case can be described as the “wishful thinking” scenario, where the existence of a need does not actually mean a particular solution will emerge to address that need, particularly not in a way that is commercially viable. The technology for CCUS with gas is far less developed than for coal, and so far CCUS with coal has not proved to be economic unless a value can be attributed to the CO2 extracted, which to date has been limited to enhanced oil recovery, which is inconsistent with de-carbonisation ambitions.

What does it all mean?

While it is tempting to join with commentary along the lines of “National Grid expects [insert dramatic headline]”, it is important to keep in mind that these scenarios outline possible rather than predicted future outcomes – as system operator, National Grid needs to explore the ways in which the energy systems it manages may change over time, in order to develop operational responses to those changes that allow it to continue to meet its statutory obligations. This means that the scenarios reflect potential outcomes for which National Grid may need to plan in future, rather than its opinion of what the future is likely to look like.

However, it is interesting for market participants to understand something of National Grid’s reasoning and the range of scenarios it believes are possible. National Grid devotes significant resources to modelling these scenarios and welcomes input and feedback from the industry, and its thinking in these areas will inform its development of the balancing and ancillary markets that form a critical part of the business case for many emerging energy models.

Another interesting question is in terms of relative cost, something National Grid is only just starting to explore. It has so far developed initial cost projections for the two 2050 compliant scenarios, Community Renewables and Two Degrees, which apparently indicate that in 2050, the costs for these scenarios are broadly similar overall, with the contribution of the electricity generation, industrial, commercial and residential energy demand (including heat) and transport sectors is also being comparable. The actual level of these costs has not been provided.

It would be useful for market participants and policymakers to understand the costs associated with the different scenarios, and in particular the difference between Steady Progression and Community Renewables being at the extremes of the range of predicted outcomes. This would enable an assessment as to whether the expected additional cost of the Community Renewables scenario was justified in terms of the projected improvement in carbon intensity (which, rightly or wrongly is a key driver of energy policy). It would also give the public some insights into the expected costs of energy policy in general, which might lead to pressure for different outcomes.

I love it when they say things like ‘large scale storage will need to be developed.

Yeah, and cats will need to be belled, too.

Wow all this technical and comercial complexity of the alternative scenarios (and without costings yet) to address a political ambition to cut CO2 emissions makes me wonder if National Grid are really saying ‘ do you really need to do this?’.

The only way I see any of this being achieved will be by dictatorial Government to try and make it work. With the fiascos of current (and earlier) Gov. initiated projects I recon this would go the same way. The Gov may try and use this information as a ‘pick and mix’ perhaps.

Leo what do you think?

Nick.

From the speech of Angus Taylor, Australia’s new energy minister:

Price gouging by distribution and transmission businesses has been a result of over-engineering and over-investment in the networks and being given a regulated rate of return on their investments, and what a business this is. Convince the regulator that you need to invest and your returns are guaranteed. Most hardworking small business people would weep at the way this works. Small business and people never get these sorts of guarantees. All of that is paid for by the electricity consumers in the marketplace and it’s unacceptable. The regulatory process needed to change and it’s changing with our reforms to the limited merits review. In practise, what this means is it’s much harder for distribution and transmission businesses to over-engineer and overinvest with the guaranteed return. At the wholesale generation level, there’s enormous potential for strategic pricing in the marketplace or price gouging in the vernacular.

All I see is NG taking advantage of the regulatory process by cooking up endless assets for which it would seek an enhanced return as they would be “high risk”, unproven ventures. Aside from that, I see a load of nonsense in what they write. Have they forgotten London Bridge, Battersea and Lots Road or even Grain and Kingsnorth and Didcot in favour of wind farms in the middle of the North Sea or the Scottish Highlands? Of course, that is another fiction in the same mould. Lots of interconnectors in which they hold financial interest. Lots of grid connection assets for different forms of generation and storage. Lots more transmission to make it all work.

I’d set Angus Taylor on them.