In July 2020, National Grid published its 2020 Future Energy Scenarios (“FES-2020”), its annual update on the four scenarios describing what it sees as the “credible pathways for the future of energy over the next thirty years.” They are not intended to be firm predictions, rather a set of plausible scenarios based on different assumptions of consumer and policy attitudes towards the energy market with a view to net-zero ambitions.

The impact of covid-19 was not included in the 2020 modelling as it emerged too late in the process. It will be considered next year, but it is worth noting that the FES look over the long-term, and covid effects might not be relevant over the time horizons under consideration.

The main conclusions from FES-2020 are:

- Reaching net-zero carbon emissions by 2050 is “achievable”, but immediate action is required across all key technologies and policy areas alongside full engagement across society and end consumers. Power sector emissions need to be negative by 2033 and at least 40 GW of new capacity added to the electricity system in the next 10 years for the net-zero ambition to be met. The amount of natural gas burned without abatement would need to halve by 2038 and the input energy required for heating homes would be just a quarter of what is currently required;

- Hydrogen and carbon capture and storage (“CCS”) are required for net zero with industrial scale demonstration projects needed this decade. Hydrogen would need to provide between 21% and 59% of 2050 end-user energy needs, with a minimum of 80 TWh of hydrogen to de-carbonise the shipping and heavy road transport sectors;

- The economics of energy supply and demand fundamentally shift in a net zero world, so markets must evolve to provide incentives for investment in flexibility and zero carbon generation. At least 3 GW of wind and 1.4 GW of solar would need to be built every year from now until 2050, with zero marginal cost generation providing up to 71% of generation in 2030, and up to 80% in 2050. Vehicle-to-grid services could provide up to 38 GW of flexibility from 5.5 million vehicles;

- Open data and digitisation underpin the whole system thinking required to achieve net zero, a key requirement to navigating the increasing complexity at lowest cost for consumers. By 2050, up to 80% of households smart charge their EV and up to 45% actively provide V2G services. As many as 8.1 million homes would need to actively manage heating demand with residential thermal storage and load shifting, and there could be over 8 million hybrid heat pumps shifting demand between hydrogen and electricity systems by 2050.

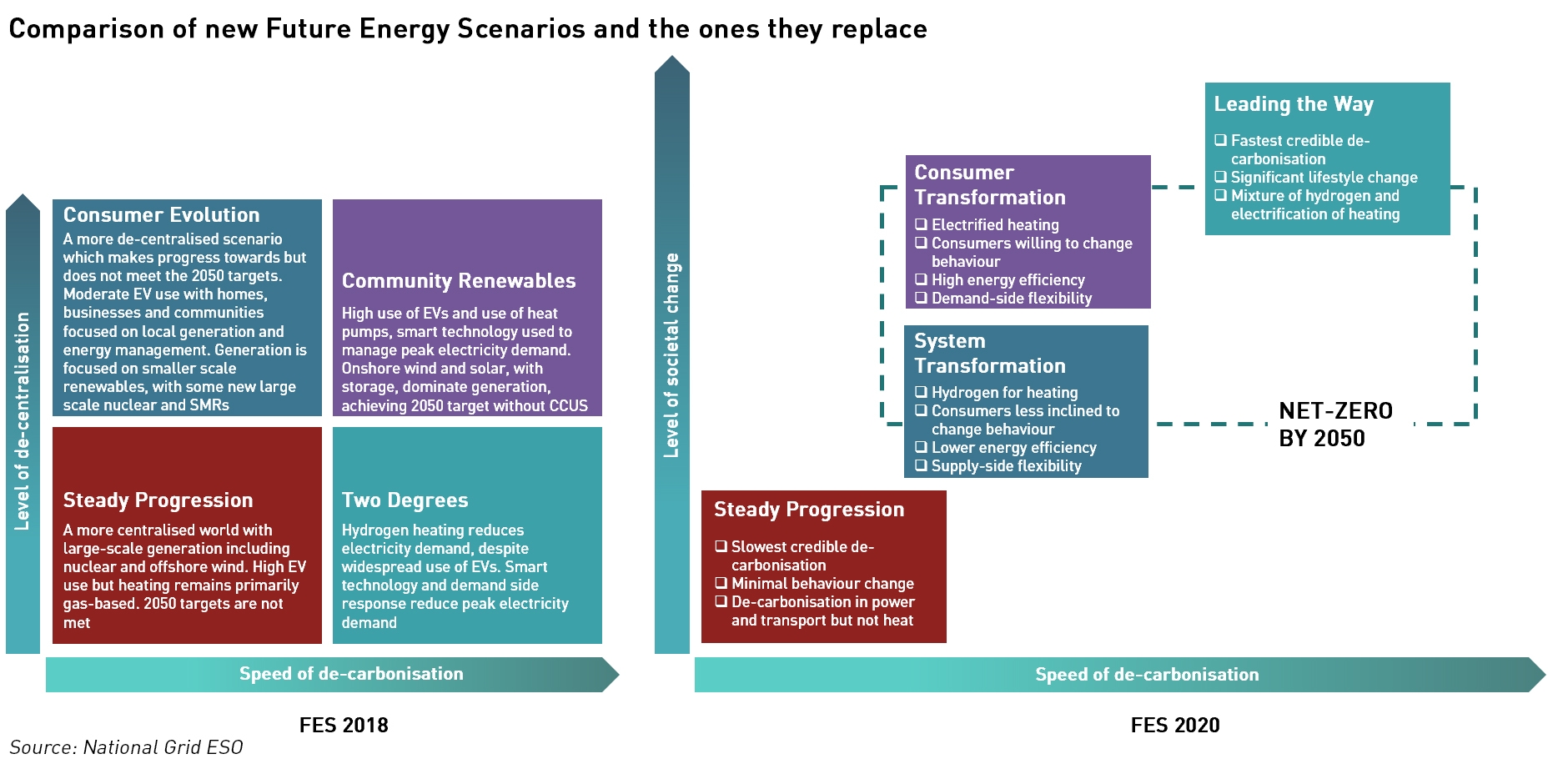

The scenarios have changed since FES-2019, and as described in the chart below, however there are some common themes in the overall messaging: CCS and bioenergy with CCS (“BECCS”) are both seen as key contributors to net-zero; and de-carbonisation will make energy balancing increasingly difficult making demand-side response (“DSR”) more important, with optimisation of EV charging, including vehicle-to-grid services, and hybrid heating systems.

Technological drivers for net-zero: bioenergy, CCS and hydrogen are key

CCS and BECCS are seen to be key enablers of the net-zero scenarios – in fact, bioenergy contributes as much as 10% of electricity demand by 2050, and when paired with CCS would deliver the negative emissions needed to fully de-carbonise the economy. It remains to be seen how realistic these outcomes would be: as I have described before, there are currently no large scale CCS projects in operation anywhere in the world that do not rely on hydrocarbon fuel production or processing for their economics. In a net-zero world, where there are no hydrocarbon fuels, CCS is likely to require significant subsidies in order to be economically viable.

Bioenergy with CCS is even more challenging as the bio-fuels need to be sourced. Currently, bioenergy contributes about 7% of primary energy demand in the UK, and recent increases in use have driven up imports of biomass from around 11 TWh in 2008 to 40 TWh in 2017.

Making bioenergy add up from an emissions perspective is far from straight-forward when the round-trip energy consumption is taken into account: wood needs to be harvested, chipped, dried out and transported even before it reaches the power stations which would need to be fitted with CCS technology. Then there is the question of the land use and competing with food crops, and the ethics of land-use conversion in regions where food crops are important for feeding local populations.

A niche for bio-fuels could be found in the transport sector for shipping and aviation, where fuels need to have high energy densities. In the FES, National Grid assumes aviation will depend biofuels, while shipping would use hydrogen instead, in the form of ammonia.

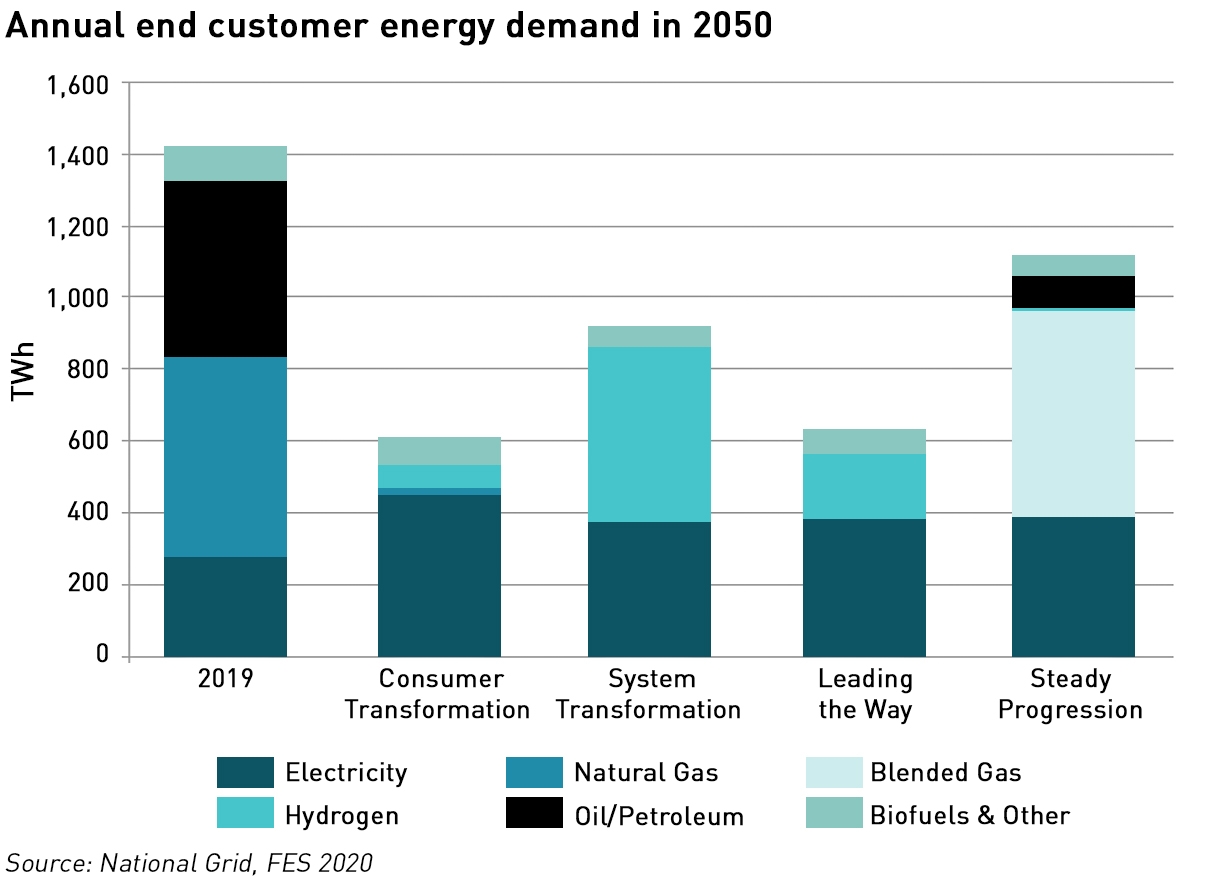

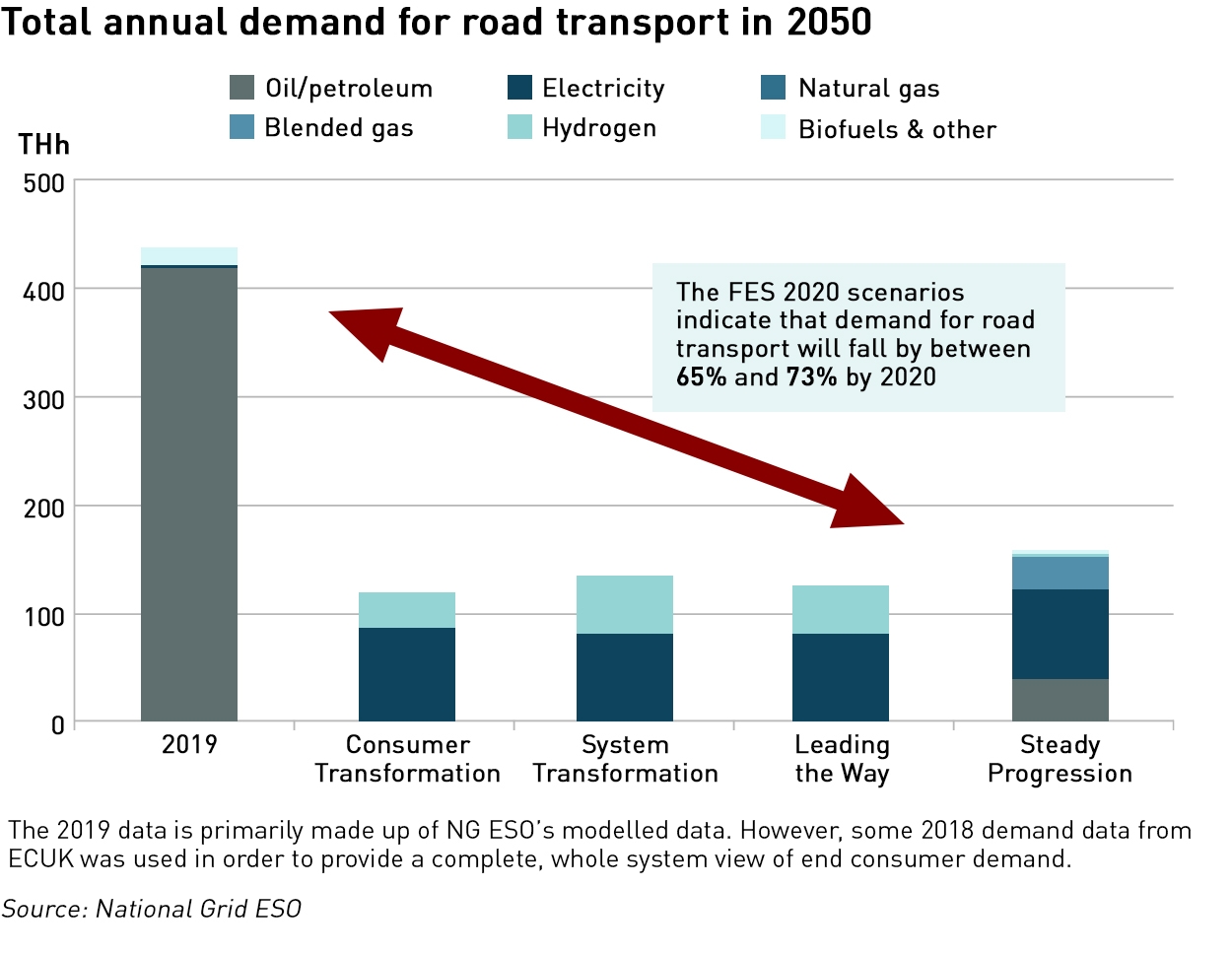

Levels of natural gas supply are expected to remain broadly similar to today in the System Transformation and Steady Progression scenarios, but fall away significantly in the Consumer Transformation and Leading the Way scenarios. In Consumer Transformation and Leading the Way, natural gas use is driven down by high levels of electrification and the use of hydrogen produced from electrolysis. In System Transformation, there is a shift in end-user consumption from natural gas to hydrogen, but as the hydrogen is produced from methane rather than electrolysis, the overall use of natural gas does not fall.

“Hydrogen has great potential to provide zero or low carbon energy to help the UK achieve net zero by 2050. But before UK consumers can really tap into hydrogen’s potential to decarbonise heating and transport, the challenges of zero carbon production and transportation at scale must be met,”

– FES-2020

Although hydrogen produces no carbon emissions at the point of combustion, there are still emissions arising in its production, storage and transportation to the point of combustion. Very little hydrogen exists as a free element, not bound with other elements such as oxygen, so it needs to be separated out from these other compounds – typically methane or water – before it can be used. Not all hydrogen production methods are zero carbon, so CCS will need to be deployed alongside hydrogen production in some cases.

The production of hydrogen also involves efficiency losses: in the System Transformation scenario, producing 591 TWh of hydrogen will require 736 TWh of input energy. Current efficiency rates are around 73% for methane reforming and 70% for electrolysis – National Grid assumes this will improve to around 80% for both technologies by 2050.

Finally, hydrogen has much lower energy density than traditional fuels, which has implications for its transportation and storage.

The consumer perspective – major behaviour changes will be needed for net zero

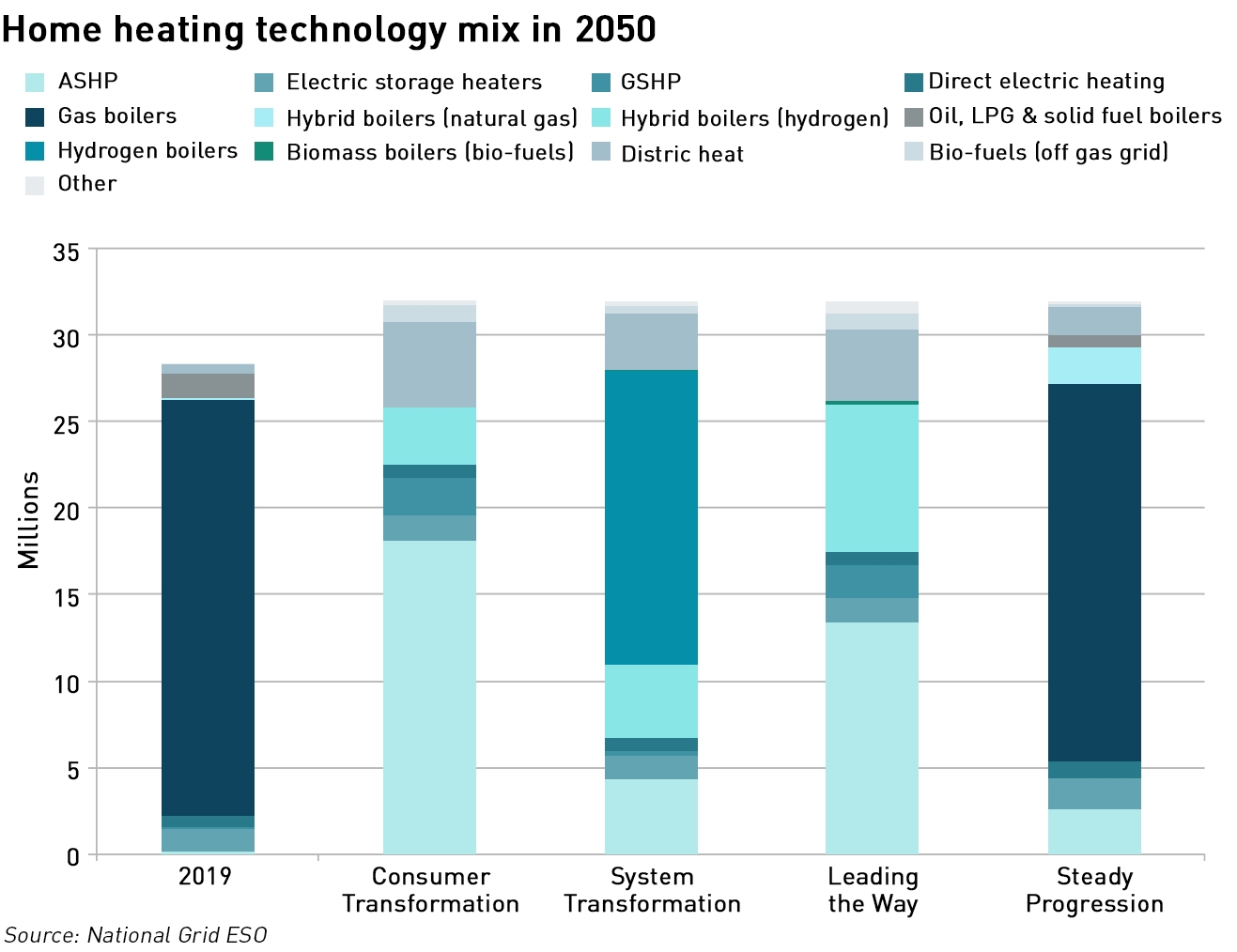

The net-zero scenarios require significant changes in consumer behaviours, with annual household demand needing to fall by between 35% and 58% in order to achieve this target.

These reductions would be achieved through a combination of high levels of insulation and the use of electric heat pumps, and methane would no longer be used for heating or cooking.

“De-carbonising the residential sector will require co-ordinated behavioural change at an individual level. This means encouraging consumers to upgrade their homes’ insulation, to choose energy efficient technology and to operate appliances ‘smartly’ – when electricity is in least demand,”

– FES-2020

“Our modelling assumes changes to nearly every home in the UK,”

– FES-2020

National Grid assumes that almost every home in the country will need to change the way it is heated in the net-zero scenarios, with only the types of change varying between the scenarios. A huge deployment of heat pumps is predicted, alongside other technologies such as hydrogen and district heating. National Grid also expects domestic appliances to be more efficient, and run “smarter”, turning up or down in response to market signals.

This is likely to require a change in the way electricity is supplied and managed, since it would be unlikely that consumers would actively manage their systems to the degree required. A move to energy as a service with service providers bundling supply with appliance management would be most likely to deliver the necessary flexibility.

The scale of this change cannot be under-estimated. According to National Energy Action, 4 million British homes – that is 14% of the total – is currently in fuel poverty. About 4.5 million families live in private rented accommodation, with a similar number living in social housing, meaning that almost a third of British householders do not own their own homes. 15% of the population lives in flats with only 24% living in detached houses.

That National Grid chooses to illustrate the level of change required using a “typical suburban house” is interesting, possibly reflecting a common misconception among policymakers that energy consumers are middle-class home owners with a high degree of autonomy over their energy choices, when in fact the challenge is significantly more complex:

- People living in poverty will be unable to afford to install better insulation or purchase more efficient appliances;

- People living in homes they do not own will be unable to make changes to insulation or methods of heating;

- People living in flats or terraced housing may be unable to install heat pumps due to lack of space or restrictive covenants in property leases.

The other important thing to note is the potential dis-connect between the suggestion that appliances should be operated “when electricity is in least demand”, which is overnight, with fire service advice against leaving running appliances unattended either by being out of the house, or asleep.

Arguably even more striking than the assumptions around domestic heating are those underpinning transport – National Grid appears to believe consumers will accept massive reductions in mobility in order to secure the net-zero targets with even the Steady Progression scenario seeing a dramatic reduction in the energy consumed in transport:

National Grid’s scenarios assume falling car ownership, and in the more ambitious scenarios, a transition to autonomous vehicles that are not owned by the users, and greater use of public transport, as well as greater use of cycling and walking.

Of all the modelling assumptions, this seems to be the least likely to be realised. The recent attempts by councils to re-design roads in the so-called “Green Transport Revolution” have been met with stiff resistance, and the related “Low Traffic Neighbourhoods” (“LTNs”) are creating significant social tensions, as many believe they shift traffic and pollution from more affluent areas to more deprived areas. Voters and road users are also enraged by the installation of new cycle lanes that have reduced road capacity for cars and trucks, thereby increasing congestion, while the usage of the new cycle lanes is extremely low, and new research suggests that pollution has increased as a result of these schemes, even in the LTNs themselves.

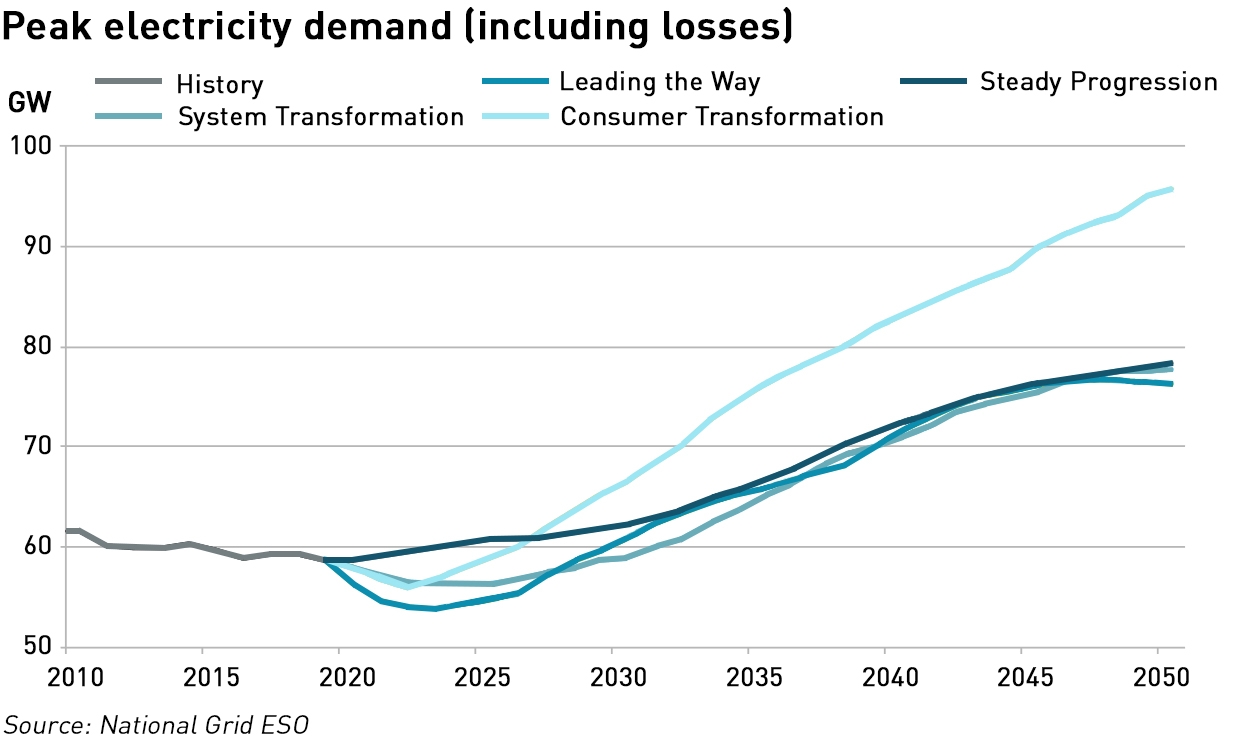

The size of the electricity system will increase as electrification takes hold

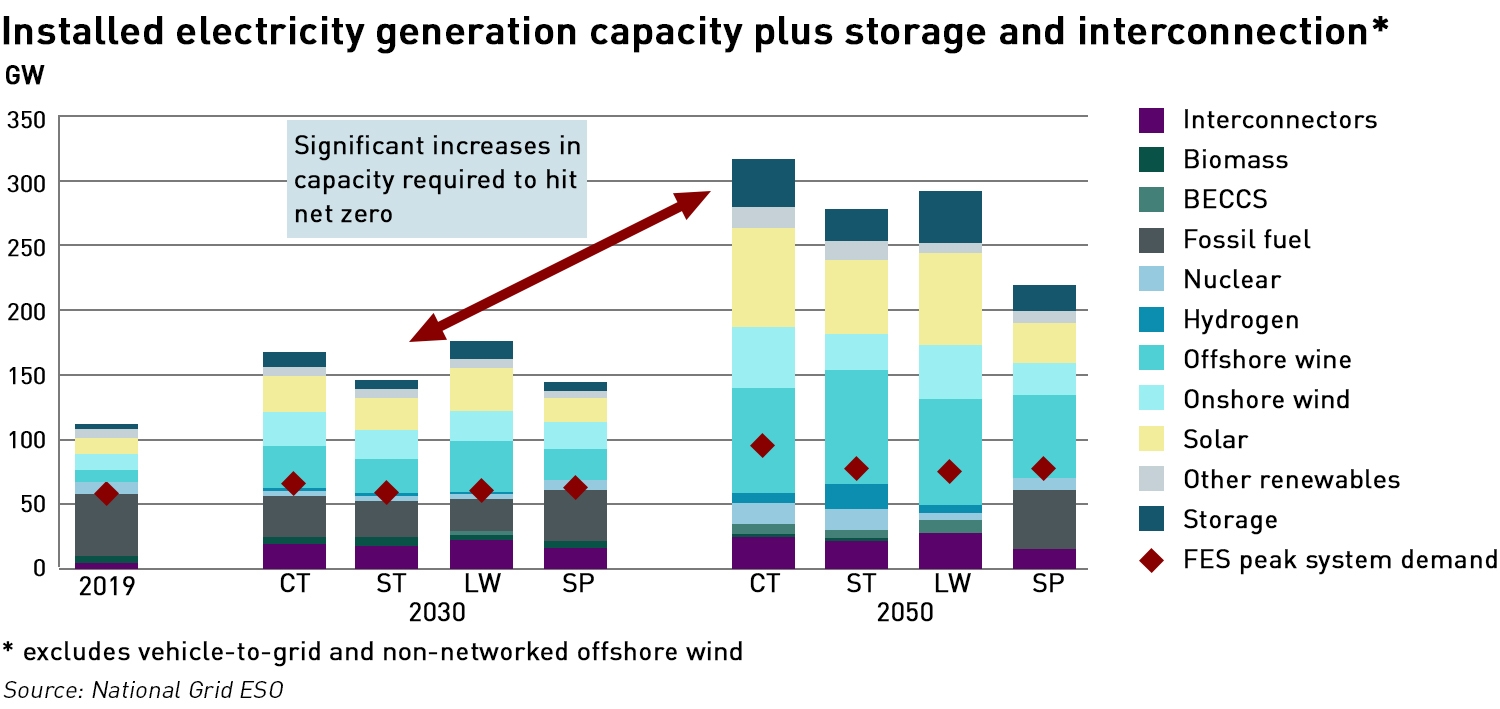

National Grid assumes that overall electricity capacity will grow in all scenarios with the largest increase in the more electrified world of the Consumer Transformation scenario which sees 2.8 times the total generation capacity in 2050 as there is today. The proportion of renewable generation rises in all scenarios, including Steady Progression, as the assumed reduced cost of wind and solar and increases in electricity demand lead to increased use of these technologies. National Grid assumes sufficient generation capacity is in place in all scenarios to achieve a security of supply standard of no more than a 3-hour loss of load expectation.

I am currently working on a post that explores the analysis published recently by Professor Gordon Hughes of the University of Edinburgh, which indicates that, contrary to popular belief, the costs of wind generation are actually rising and not falling. Most UK wind farms are structured as separate corporate entities known as Special Purpose Vehicles (“SPVs”) and as such they are required to file their accounts at Companies House. Professor Hughes examined these accounts in order to ascertain the actual capital and operating costs of wind projects in the UK, and his findings contradict the almost universal belief that windfarm costs are falling.

“Far from falling, the actual capital costs per MW of capacity to build new wind farms increased substantially from 2002 to about 2015 and have, at best, remained constant since then…the operating costs per MW of new capacity have increased significantly for both onshore and offshore wind farms over the last two decades.”

– Professor Gordon Hughes, School of Economics, University of Edinburgh

His analysis suggests that these projects will require significantly higher wholesale electricity prices in order to operate economically on a merchant basis once their subsidy periods expire and that absent these rises, windfarms are likely to close at the end of their subsidy periods. As renewable generation has a near-zero marginal cost of production, the mechanism by which wholesale prices would rise to the levels required would be through the introduction of materially higher carbon prices.

Electricity is already expensive, and with 4 million homes in fuel poverty, there would seem to be little scope for raising prices further (and indeed, de-carbonisation of heating will naturally push prices higher due to the higher cost of hydrogen or other non-methane based modes of heating).

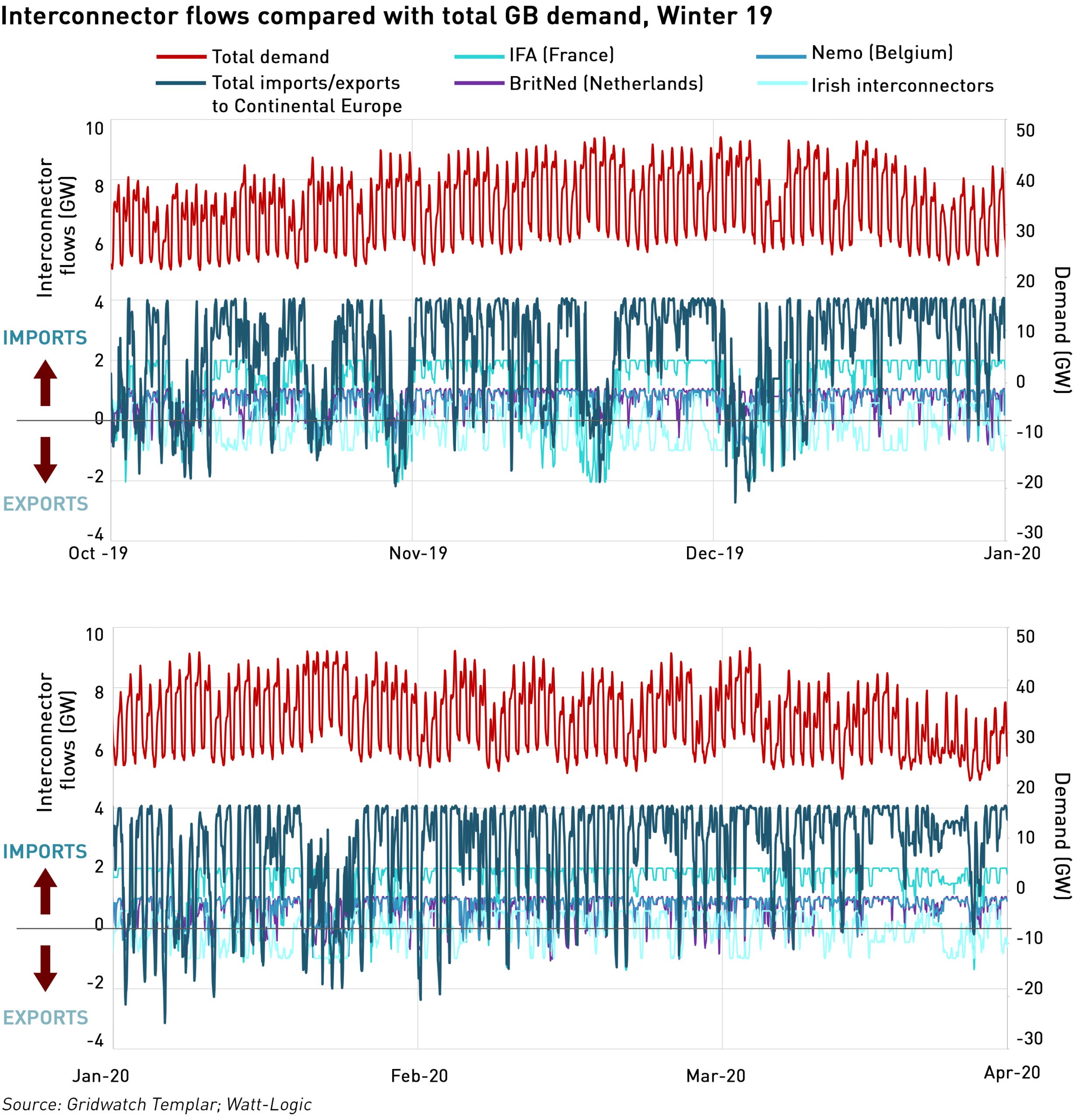

Interconnectors are also expected to play a larger role than they do today. Even if Britain retains access to European electricity markets post Brexit, this assumption is problematic. I have illustrated the high weather correlation between most of the markets with which Britain has or plans to have interconnection, with the result that weather-related electricity demand will rise in these markets together.

Currently, during periods of high GB winter demand, the country often exports electricity: Britain exported electricity to Continental Europe during 13% of the hours with the top 5% of demand since the beginning of last winter, while exports accounted for 16% of all hours over that period. (Considering Winter 19, which was less affected by covid-19 effects, Britain exported electricity to the Continent in 18% of all hours and 12% of the hours with the highest 5% of demand.)

A key reason for these patterns is that the French electricity system is more temperature dependent than the British system due to the dominance of electric heating. The move away from gas heating in the UK could narrow this gap, but the extent to which it does will depend on how much heating is electrified rather than concerted to hydrogen or off-grid solutions.

Finally, National Grid sees nuclear power declining in all scenarios, reflecting the anticipated retirements of aging reactors and the lack of support for new-build. The new investments announced recently as part of the Government’s 10-point plan are too low to materially change these assumptions.

A much more flexible energy system will be needed

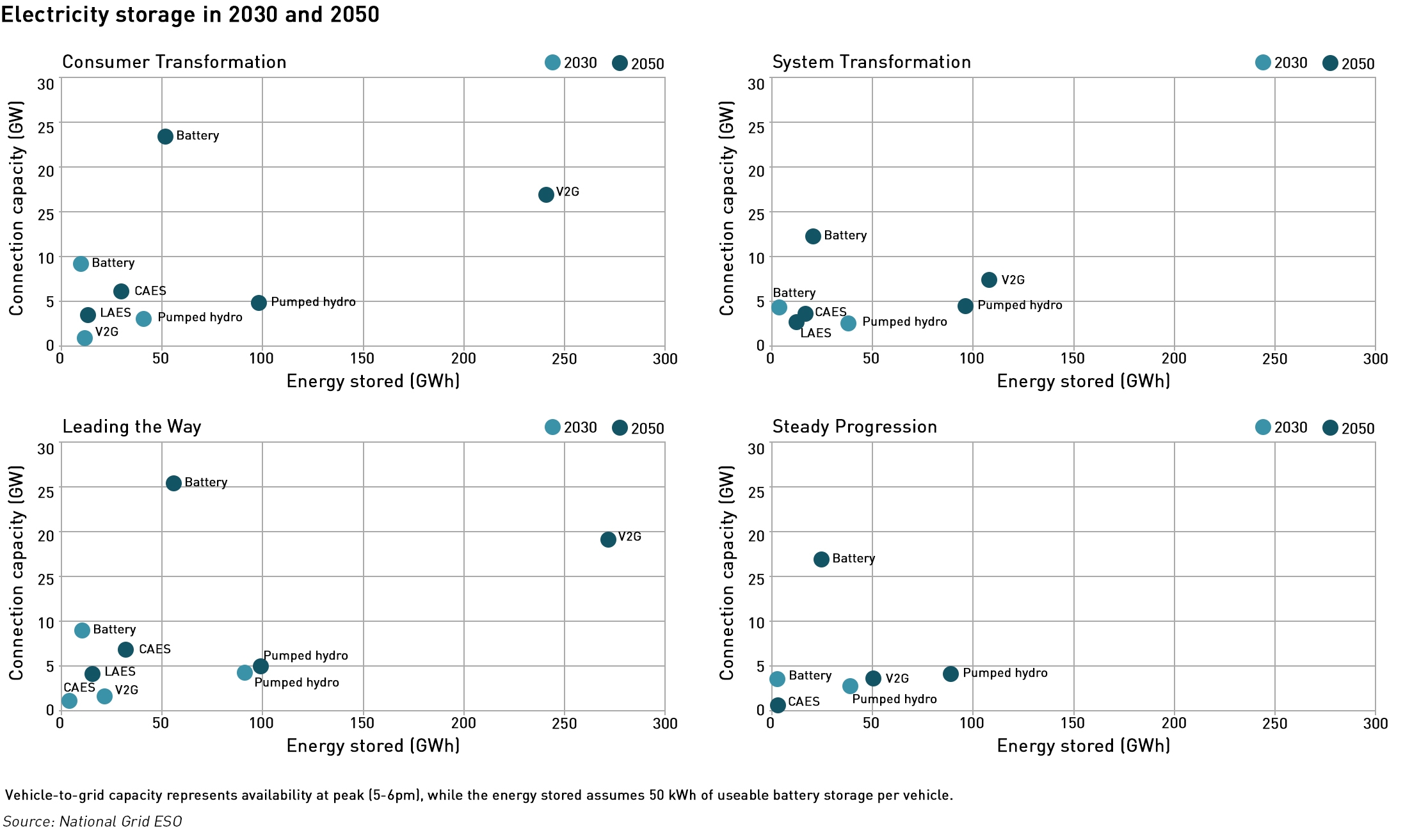

As a result of increased reliance on renewable energy sources, flexibility on both the supply side and the demand side would become more important. Fossil fuel use is phased out to meet de-carbonisation, and with them goes a significant amount of energy storage capacity. Even if hydrogen replaces methane in the gas network, its lower energy density means that the energy content of linepack will fall. National Grid expects interconnector imports to reduce the need for storage, but as noted above, this may not be realised at times of need.

Flexibility will be needed not only to meet demand spikes, but also to minimise renewable generation curtailment in low-demand periods. At the system level, excess renewable generation could be used to produce hydrogen through electrolysis. At the domestic level, National Grid sees an increasing role for smart appliances in conjunction with time-of-use tariffs, with load shifting from appliances remaining low in the 2020s due to the need for manual scheduling, but subsequently rising significantly once white goods are developed that can respond automatically to price signals from the 2030s.

National Grid believes that smart appliances could shift up to 11.4% (or 1.5 GW) of peak appliance and lighting electricity demand in the Leading the Way scenario by 2050. This outcome is most likely in an “energy-as-a-service” model with minimal consumer input, and care will be needed to reduce the fire risks associated with operating appliances when left unattended (for example at night when prices are low).

Thermal flexibility offers real opportunities for residential demand-side-response. Key heating hours in winter coincide with peak system demand, but heating systems can be flexed by taking advantage of the thermal capacity of buildings. Heating can be turned off for limited periods of time without any difference in comfort levels being discerned since the fabric of buildings retains heat for a period. In addition, the development of phase-change thermal storage materials can offer the potential for thermal storage over longer periods.

One feature of domestic heating that does not feature in the scenarios is the use of air conditioning. Air conditioning demand in the UK has been growing in recent years, and even the domestic segment has seen growth as people familiar with air-conditioned shops and offices are less inclined to swelter at home in hot weather.

If the covid-related growth in working from home continues beyond the end of the pandemic, demand growth for domestic air conditioning could accelerate, and where home-owners are installing entirely new heating systems, they may well look at air conditioning at the same time. This would change the domestic electricity demand dynamic – in countries where domestic air-conditioning is already more common, peak summer electricity demand mirrors that in the winter as cooling load is significant.

National Grid believes that electric vehicles will be a major source of flexibility with over 50% of households smart charging their EVs in all scenarios in 2050, and significant amounts of V2G participation in some scenarios, although after 2045 this could fall in the high societal change scenarios as autonomous vehicles replace privately-owned EVs.

EVs are a major part of the Government’s green energy policy with £1.3 billion of investment in EV charging infrastructure being announced in the recent 10-point plan, but there are real questions over the availability of the mineral resources to meet this demand, and the environmental and ethical issues surrounding their extraction. This could lead to lithium-ion technologies being dis-incentivised in the way that diesel has been.

A move away from lithium-ion battery technology would not necessarily undermine National Grid’s projections around EV use, since other battery technologies are available, and more sustainable approaches may be found, but it is also possible that EVs will be replaced by hydrogen-powered cars.

Hydrogen is seen as a key enabler in the de-carbonisation of heavy vehicles, and if an infrastructure is developed for fuelling heavy vehicles, it could be leveraged for light vehicles as well. Fuelling a hydrogen car takes about the same time as fuelling a petrol or diesel car, which is faster than the current EV charging times, so hydrogen cars could be popular with motorists as well. (EVs have other disadvantages such as stopping over a very short distance rather than cruising to a stop when breaking down, and being difficult to tow without causing permanent damage.)

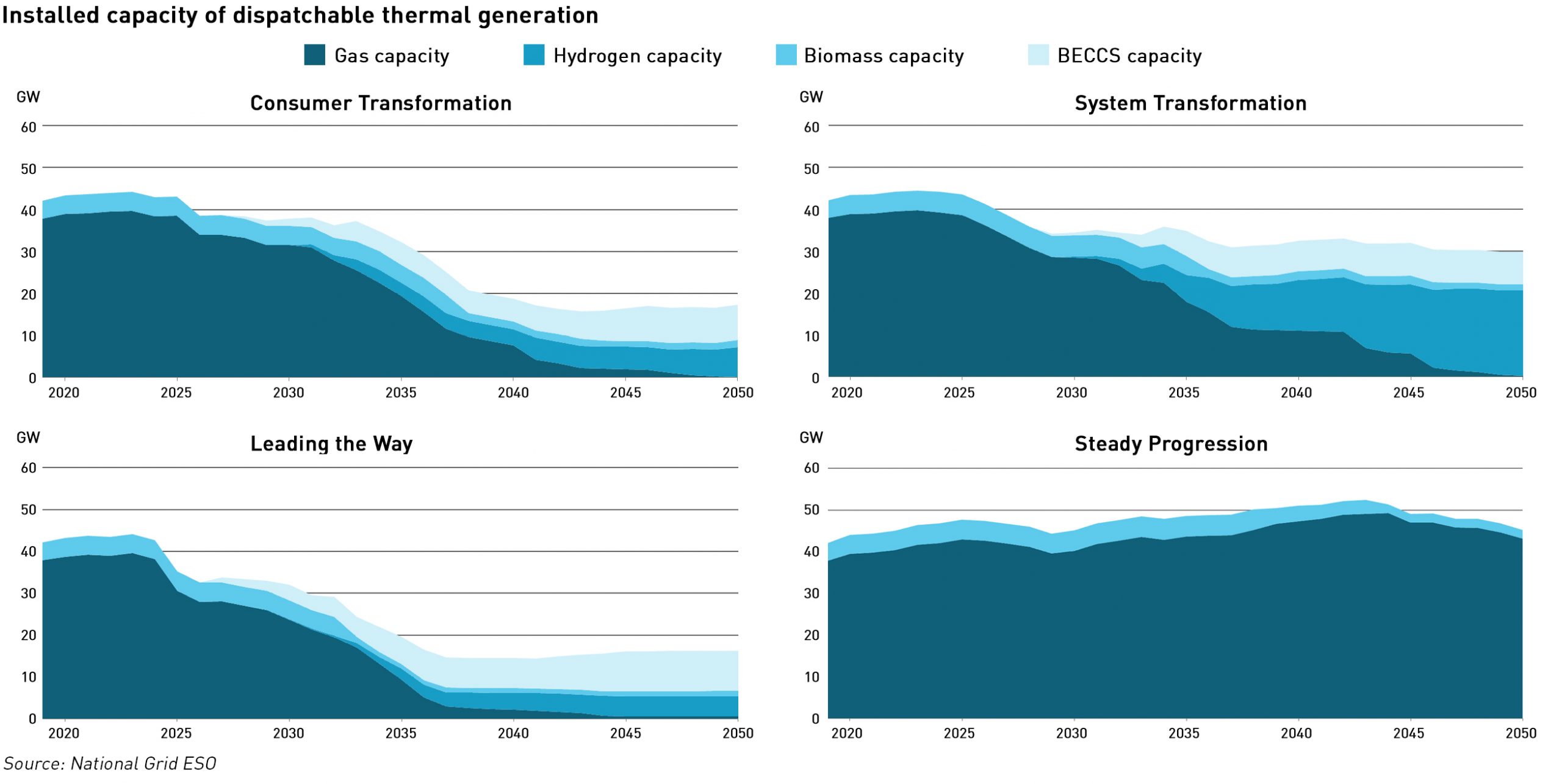

While flexibility will need to rise in an increasingly renewables-dominated world, the net zero scenarios see significant reductions in the availability of dispatchable electricity generation, with only the Steady Progression scenario maintaining current levels. In the Consumer Transformation and Leading the Way scenarios the amounts of installed dispatchable generation capacity fall to half current levels, driven by the elimination of gas-fired generation. The net zero scenarios all rely for generation flexibility on technologies that do not currently exist, specifically hydrogen and biomass with CCS.

“We assume a combination of policy and market change to support the required level of investment in flexible generation capacity with low annual running hours,”

– FES-2020

New technologies and massive behavioural changes needed for net-zero

National Grid described its Future Energy Scenarios as representing the “credible range of uncertainty” rather than predictions of the future energy pathways. It does not present the counter-factual of maintaining the status quo – even the Steady Progression scenario involves significant change both in system design and consumer behaviour to today. The FES document also does not assess the costs of the scenarios, although these have subsequently been published and will be the subject of my next blog post.

Even setting aside the issue of cost, there are significant doubts as to the achievability of any of the net-zero scenarios. There is an assumed reliance on technologies which are unproven, currently uneconomic or yet to be developed, alongside a revolution in home heating and transport, with a massive reduction in personal mobility.

Even if some of the changes that have emerged due to covid persist, particularly in relation to increased working-from-home, it is unlikely that this would deliver the transport reductions required, and inevitably domestic electricity demand would increase, not just for heating and lighting over more hours in winter, but also the possibility of cooling in summer, which is not factored in to the scenarios at all.

The disconnect between running smart appliances at times of low demand/low prices and fire safety advice will need to be addressed. Appliances are a major contributor to domestic fires, despite a century of development – the next 30 years would need to see a step change in safety as well as smart functionality to overcome this.

And there is an implicit assumption that communications technologies have sufficient bandwidth and coverage to enable smart energy technologies across the entire market. Not only must smart meters work properly in all homes, but telecoms connectivity must allow for meters and smart appliances to receive signals that enable optimised running.

The gap here is also significant, and consumers will not be keen to buy smart appliances that might reduce their ability to use available bandwidth for work or leisure. On top of this, the security issues must be addressed – the nascent market for smart products is already plagued with security gaps, with many smart doorbells, thermostats and other networked home technologies allowing hackers to access the entire domestic network via the router.

There is a great deal of talk from politicians, policymakers and market participants about Britain’s net-zero ambitions, but the long-promised energy White Paper, which ought to start setting out a concrete policy roadmap is yet to appear. The prospects for hydrogen are being hugely hyped, alongside pressure to ban the sales of traditional boilers and conventional cars. But real progress remains slow: despite all the noise around net-zero, the basic first step of removing coal from the generation mix is yet to happen – already this winter coal has contributed as much as 8% of demand at times.

The 2020 Future Energy Scenarios provide a window on what a net-zero world might look like, and it’s very different from the one we see today. The idea that such a large gap can be bridged in just 30 years seems fanciful.

This blog post was co-authored by Adam Porter

Hi Kathryn, I have just put this on Paul Homewood’s site ‘NOT A LOT OF PEOPLE KNOW THAT’

[ Paul, have you seen this – Kathryn Porter’s forensic take apart of National Grid’s 2020 Future Energy Scenarios (“FES-2020”)

http://watt-logic.com/2020/12/10/fes-2020/

See also –

Prof Gordon Hughes showing the costs of wind generation are actually rising and not falling…

https://www.ref.org.uk/Files/performance-wind-power-uk.pdf

Both are well worth reading. ]

Keep up the good work of getting the truth out there,

regards

john

Thanks Kathryn. Its very worrying, science and engineering are being silenced by the mob – politicians responding to social media fuelled popular opinion are over-ruling the sober decision making that would have been previously made behind closed doors. What frightens me is that experienced grid engineers are forced to give credence to these scenarios and feel unable to speak up. Clearly none of these plans will ever be realised, but I fear serious damage will be done in the vain attempt to meet unachievable targets. Indeed I feel damage has already been done e.g. we already have an excess of wind power on the grid, solar PV is simply not appropriate for the UK, and wood pellet biomass is a crime against nature.

As a genuine question – is it time to consider installing a backup domestic diesel/petrol generator given that future blackouts are increasing likely ?

I did a ‘Whole of Life’ cost comparison between wind and solar plants (WASPs) and advanced nuclear power plants (NPPs) supplying the 480 TWh of low-carbon electricity proposed in the ‘Consumer Transformation Scenario’. WASPs £18.47 billion every year – FORVER!!!; NPPs £12.42 billion per year – but just for 20 years. Then there would be a hiatus in investment of some 50 years – that equates to £4.06 billion per year. That’s less then 1/4 of the cost for WASPs and that extra comes out of the pockets of every income earner. It will kill some of the poorest and underprivileged among us:

https://colin-megson.medium.com/national-grids-fes-2020-will-cost-13-21-billion-every-year-forever-ce41e7c1fdf9

I also did 2 follow up blog posts detailing the unimaginable levels of waste disposal to consider for the fibreglass wind turbine blades. I still have to come up with the solar pv panel waste figures:

https://colin-megson.medium.com/national-grids-fes-2020-what-is-the-environmental-impact-of-480-twh-per-year-from-wasps-c449f7e6b461

https://colin-megson.medium.com/national-grids-fes-2020-what-is-the-environmental-impact-of-480-twh-per-year-from-wasps-1bb3bd51a6c3

The direct confirmation that interconnects require dispatch-able power (when the wind does not blow etc…) is very interesting (and implication that fossil fuels are required then).And too the implication that if we have a more electric scenario (electric heating and vehicles) this will get worse. {Given the cube power law for wind power output then there is little or negligible wind electricity on a calm or very calm day}.

The idea of “biomass with CCS” seems limited as much of the CO2 in biomass is due to the processing and transport – as well as the loss (for decades) of tree absorption (as pointed out in one government report). So “negative emissions” seems very out of touch (and old-fashioned).

There is a possibility that hydrogen could be used in aviation,due to its lower mass/energy; especially as some advanced engines already use this – though low density will require larger fuel tanks – or shorter flights (with a bonus that taking off will be easier).

The National Grid seems to have a very limited (trammelled) and optimistic (for themselves) view of scenarios.

“3-hour loss of load expectation” if this is averaged over a year, and the country, it could mean that, say, London could have single day without electricity (for all homes, industry, transport and hospitals) once a year. This might, perhaps, be ameliorated by NG, by the use of Smart-meters to turn off power to all those running on a Green Tariff…???

The storage issue does seem to have been addressed for electricity – nor for hydrogen (which, unlike natural gas, cannot be delivered, via pipeline, from source – but must be stored, and compressed and liquefied – and occupy significant volume – WHERE?) , by NG. As far as hydrogen transportation if the same energy flow is required then the pipelines must be rated to three times the (current) pressure ( unless liquefaction is undertaken).

You do make a good point of domestic heat storage but there is still a lot of R&D required for this (especially if high temperatures are stored – with the improvements of capability and possible electricity generation). I believe that, in France (which has more electric heating than UK), hot water tanks store significant amounts of heat – which allows for a significant diurnal smoothing of electric power. Though this part solution could be advantageous in the UK it might be better to store (much more) heat in the same volume by doing so at a higher temperature; this would have the advantage of allowing it to be used, directly, for air conditioning also (see “How heat from the Sun can keep us all cool” XiaoZhi Lim , NATURE31 January 2017).

The points you make about people living in fuel poverty, or not being able to afford electric vehicles (or have access to public transport), are important and indicate NG have little understanding of their customers – or , perhaps, expecting someone with a lot of money to resolve them

The idea of more people working from home (and less need for EV, though not freight) is a scenario that does not seem to have been considered. (nor that of going nuclear)

However I do not think that the capacity problems of the internet and the limited software using it will suffer from the Smart Meters.

The Smart Metering Wide Area Network (SMWAN or WAN for short) is the name given to the communications network between the communications hub sitting on top of your electricity (“smart”) meter. It forms its own set of interlinked hubs isolated from the internet – with, I suspect, low data rates – as they use long distance radio in more rural locations. ( https://www.smartme.co.uk/technical.html )

” Ofgem have said it is reasonable for a supplier to charge for the installation of a conventional meter if a smart meter is refused.”

Read more at: https://www.smartme.co.uk/technical.html © SmartMe.co.uk

A simple Faraday cage around a ‘smart meter’ converts it into a dumb meter … so you you are in control again !

With so many different publications on future energy coming out in recent days it has been really hard trying to keep up with them. I have largely given up on the Grid’s scenarios for now, but I did note the bowdlerised version of the criticisms from the industry that they published.

https://www.nationalgrideso.com/document/177781/download

It also reveals some of the idiocies of the green zealots who have been hired by some of the companies, demanding the impossible in the interest of puritanical purity of being a zero. Some highlights:

More subsidies and regulatory fixes please! Carbon taxes to force up market prices for power!

Have they read Prof Kelly’s assessment that this is perhaps a £2 trillion item? Or real world research that tells us unsurprisingly that manufacturer claims about the effectiveness of heat pumps are rarely met, with a COP between 2 and 3 (rarely at the high end) being a typical average?

Back to FES:

Perhaps they should be looking at battery degradation costs?

That is perhaps hardly surprising given that green hydrogen made by renewables supplying electrolysis is about ten times the cost of natural gas, and blue hydrogen, made by steam reforming methane – which produces CO2 as a by-product – is around 5 times the cost, based on estimates from Timera. Another unicorn.

Yes, it’s going to hit industry really hard. More offshoring and loss of jobs. Fewer exports. Worse balance of payments as we import more (at least until we run out of credit).

Then we got the Sixth Carbon Budget, with some 38 downloads (I’ve still not managed to get a download of the main report, constantly getting incomplete versions that are deemed corrupted files). And now the White Paper, with a blizzard of technical consultations on the back of it, and a lot of green propaganda up front. The one thing I did find useful in understanding some of the BEIS thinking was the report about their model of electricity:

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/943714/Modelling-2050-Electricity-System-Analysis.pdf

Some digging around confirms that the model makes no attempt to look at the consequences for the grid and distribution – as Prof David Newberry described it it is a “copper plate model” that assumes that power can flow to wherever it is needed at no additional cost. It also is based on modelling isolated days. So as long as by assuming that we can run down our heat stores and batteries within the day we get to the end of settlement period 48 without the grid collapsing it is considered a viable scenario: the thought that cold spells with derisory renewables generation can last for days, or even weeks on end is simply ignored. The assumption that interconnectors will be able to provide us with full capacity whenever required is also implicit. There are however some glimmers – they do appear to be starting to recognise that curtailment is going to rise sharply, but by assuming we can use interconnectors to export even though it is likely that they will be trying to feed oversupplied markets at negative prices – a phenomenon we have already seen this year – they are greatly underestimating its impact.

Throughout all this work are some amazingly rose tinted assumptions about cost trends for their favoured technologies, with only the vaguest of justifications. I’ve a feeling reality will hit quite hard eventually.

I had a look at some of the issues elating to current gas storage; this is either in depleted gas fields or in salt caverns. These can, currently hold 4% of the annual gas requirement of the UK. Changing that to hydrogen would reduce this by a factor of a third i.e about 5 days worth (for same energy content). I believe other countries have larger storage capacity.

If some of this storage was used to sequester CO2 then there would, permanently, be less for the hydrogen – so there would be a conflict between the use of such stores.

And if the hydrogen were to be used as a resource for dispatchable electricity that would reduce that (gas) available for domestic and industrial use. Though I understand that Rolls-Royce have recently announced gas turbines that run of hydrogen I do not know how much this, when used to generate electricity, might affect the consumption of gas in the UK .

I suspect that 5 days storage of gas is insufficient for likely prolonged periods of calm, and at least a period of 15 days might be required (i.e. 3 times at much storage – or more if electricity usage, such as EVs, increases)