In the last few weeks there have been a number of announcements by the Government and others on the challenging subject of the de-carbonisation of heat. Heating and cooling currently accounts for nearly half of UK energy consumption, and around 50% of UK emissions from heating are associated with space heating and hot water in domestic buildings.

“The decarbonisation of heat is arguably the biggest challenge facing UK energy policy over the next few decades,”

– Ofgem

Role of technology

Over the past 20 years, a number of technology trials have resulted in the development of a range of low carbon heat technologies, each of which has its advantages and disadvantages.

Heat pumps

The domestic Renewable Heat Incentive (“RHI”) is a government-backed incentive scheme designed to encourage UK homes to install renewable heating systems, including heat pumps. There are several types of heat pumps, which all use the same basic principle of extracting heat from a natural source such as the ground or air, and concentrating it to obtain a higher temperature. This heat is usually then applied to water for space heating and hot water.

As heat pumps transfer rather than produce heat they are more efficient than traditional heating systems, however they generally operate at a lower temperatures than boiler systems so benefit from the use of larger radiators or under floor heating.

Heat pumps are often thought of as a “fit and forget” technology since they require little maintenance and eliminate the need for fuel deliveries required by other types of domestic heating. Heat pumps can provide both space and water heating, thus significantly lowering fuel bills, however they are expensive and difficult to install, require larger radiators that conventional central heating systems, and may not be suitable in all properties.

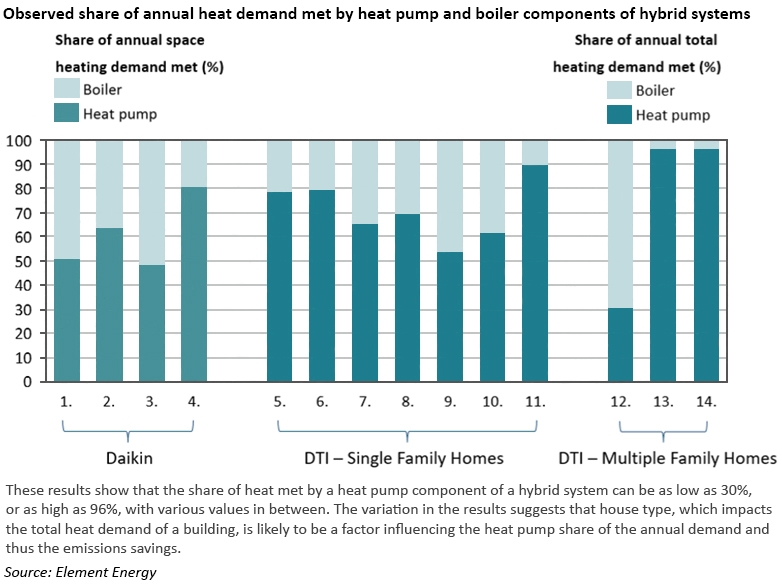

Hybrid heat pumps

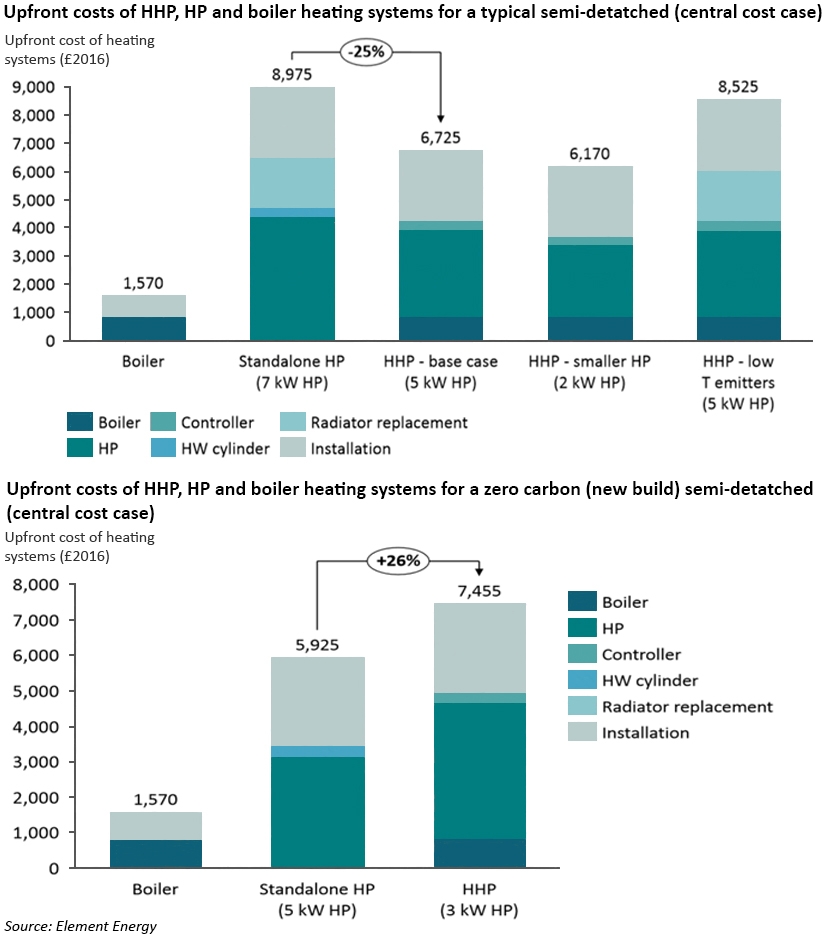

Element Energy carried out a study for the Government on the potential use of hybrid heat pump (“HHP”) systems in the UK’s long-term de-carbonisation of domestic heat. For the purposes of the study, a HHP system was defined as one combining an electrically-driven heat pump with a gas boiler, along with a dedicated controller.

As shown in the chart below, for a typical semi-detached house, HHPs and standalone HPs are £5,000-£7,500 more expensive than gas boilers, however hybrid heat pumps are £450-£2,800 less expensive than standalone heat pumps. The savings are mainly due to the ability to avoid placing existing radiators when installing HHPs, as well as the ability to reduce the rated capacity of the heat pump component in the HHP case compared to the standalone HP case. Additional savings can be realised by choosing to provide hot water with a combi boiler, thus avoiding the cost of a hot water cylinder required for water heating by the heat pump.

In the case shown in the chart, the cost differential between the HP components of the HHP in the base case and the ‘smaller HP’ case is only £555, for a 2kW system versus a 5kW system. This is because cost per kW value used for heat pumps below 5kW capacity was significantly higher than the equivalent cost for heat pumps above 5kW. However, there was only one data point for the smaller heat pumps – it is possible that the costs would fall as more sub-5kW heat pumps enter the market.

For highly efficient new builds, on the other hand, the study found that hybrid systems may not bring upfront cost benefits over standalone heat pumps, since suitable radiators are installed as part of the initial construction, and the overall heating requirement would be lower due to higher levels of energy efficiency.

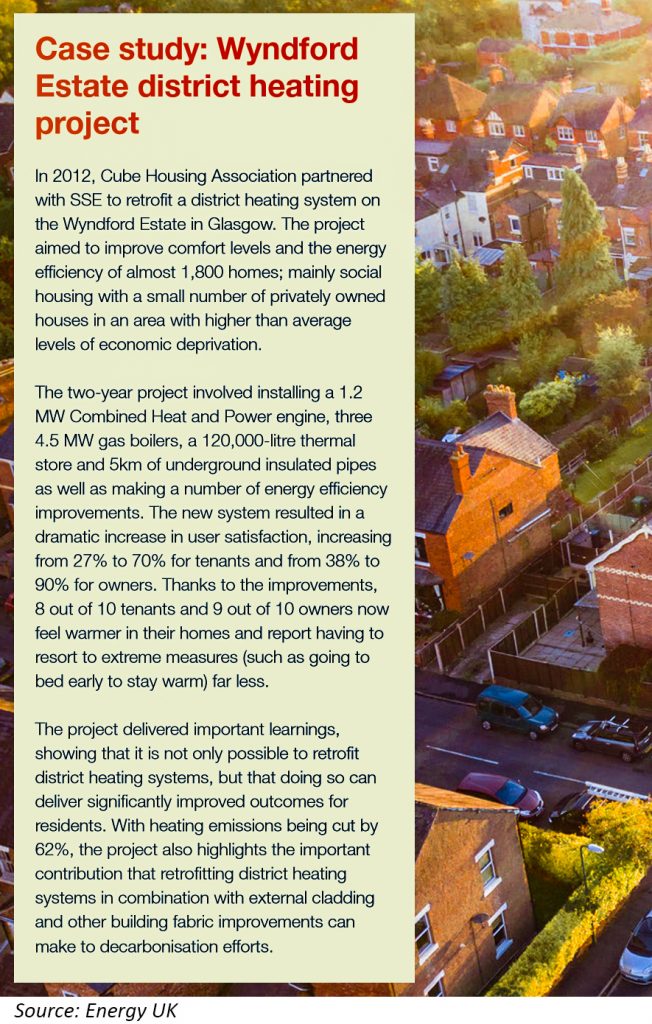

District heating

The Government has announced a new scheme for consumers and non-domestic users including schools, hospitals and councils to participate in a heat networks project, beginning in the autumn. The £320 million Heat Networks Investment Project, is a key party of the Government’s Clean Growth Strategy, and will offer grants and loans to both public and private sectors for networks serving two or more buildings.

The Government has announced a new scheme for consumers and non-domestic users including schools, hospitals and councils to participate in a heat networks project, beginning in the autumn. The £320 million Heat Networks Investment Project, is a key party of the Government’s Clean Growth Strategy, and will offer grants and loans to both public and private sectors for networks serving two or more buildings.

Heat networks distribute heat through insulated pipes from a central source to a variety of different customers. For residents in flats, heating costs could be as much as 30% lower on a heat network than alternatives such as individual gas boilers. There are already a number of successful heat network projects already operating in the UK such as one in Sheffield which burns 12,000 tonnes of municipal waste each year as the main fuel source for its network. Or Southampton’s main energy centre which has over 45 energy users ranging from over 1,000 residential properties, a hospital, university, shopping centre, police headquarters and BBC studios.

.

.

.

.

Energy efficiency

Energy efficiency is an obvious place to start when it comes to the de-carbonisation of the heating sector, however it is an area that has seen a number of false starts, with initiatives coming and going and struggling to gain traction with homeowners. According to a report published in September 2017 by Frontier Economics energy efficiency measures save the typical dual fuel household £490 per year, yet the energy saving potential in UK homes has not been fully realised.

The UK Energy Research Centre found that cost-effective investments in residential energy efficiency and low carbon heating over the next 20 years could reduce energy demand by 25%, which would equate to £270 per year for a typical household at 2016 prices.

Frontier Economics proposed three “ambitious and achievable targets” to improve the energy performance of UK buildings:

- From 2020: all new homes will be built to the Zero Carbon Homes standard – to prevent homeowners and tenants being locked into unnecessarily high energy costs over the lifetime of the buildings.

- By 2030: all the homes of low income households and all homes in the rented sector will be retrofitted to an Energy Performance Certificate (EPC) rating of C (on a scale from A to G) – making an important contribution to reducing fuel poverty.

- By 2035: all other homes will achieve a C rating – maximising the economic and social benefits of meeting binding climate change targets in the most cost-effective way

The report suggests that public investment underpinning these targets would require around £1.7 billion per year up to 2030 – broadly in line with the levels seen in 2012 and 2013. The report also proposes linking the Stamp Duty paid when buying a home to the property’s energy performance, rather than just to the purchase price. This could be revenue-neutral for the Treasury and has been proposed before but not adopted.

A 2017 Parliamentary Research paper identified a number of barriers to implementation of efficiency measures including:

- Misaligned incentives – in the private rented sector, the financial reward for installing efficiency measures is realised by tenants rather than landlords through lower energy bills, meaning there is no direct financial incentive for landlords to install energy efficiency measures in their properties;

- Hassle – the installation of energy efficiency measures can be disruptive, which in the industrial and commercial sectors has cost implications;

- Lack of prominence and information – for many households and non-energy intensive businesses, saving energy is not a priority. Householders prioritise the comfort and value of their homes and do not seek information about energy saving opportunities;

- Poor return on investment – energy efficiency measures are less attractive to businesses when payback periods are longer than for business growth projects;

- Low consumer confidence – confidence in energy efficiency measures has been eroded by instances of poor quality installation under Government-supported programmes, and discrepancies between advertised and realised performance;

- Difficulty accessing finance – lack of finance for the up-front cost of efficiency measures, which is often high, can be a barrier to their installation.

Around 7 million new homes are expected to be built by 2050 – one-fifth of the country’s housing, while this provides opportunities for the implementation of energy efficient and low carbon technologies, it also means that the majority of housing that will be in use in the 2050s has already been built and so retro-fitting will be needed.

Concerted policy efforts would be needed to overcome these barriers and deliver the available building efficiency gains. Attention should also be given to the issues of poor pre-construction forecasting of building energy performance, to avoid incurring expenditure on un-successful measures and further eroding public confidence.

Improvements in energy efficiency could be supplemented with technologies such as Building-integrated PV. BIPV has the potential to reduce the energy consumption of buildings by around a quarter and has already been deployed on some high-profile buildings such as the Dubai Frame.

Role of gas

80% of the UK’s 26 million homes use gas for heat. According to National Grid, in order for the de-carbonisation of heat to be successful, around 20,000 homes will need to switch to a low carbon heat source every week between 2025 and 2050, requiring a mix of solutions, including reducing the carbon intensity of the gas system through use of hydrogen and/or bio-methane, electric heat pumps, combined heat and power (“CHP”) facilities and district heat networks.

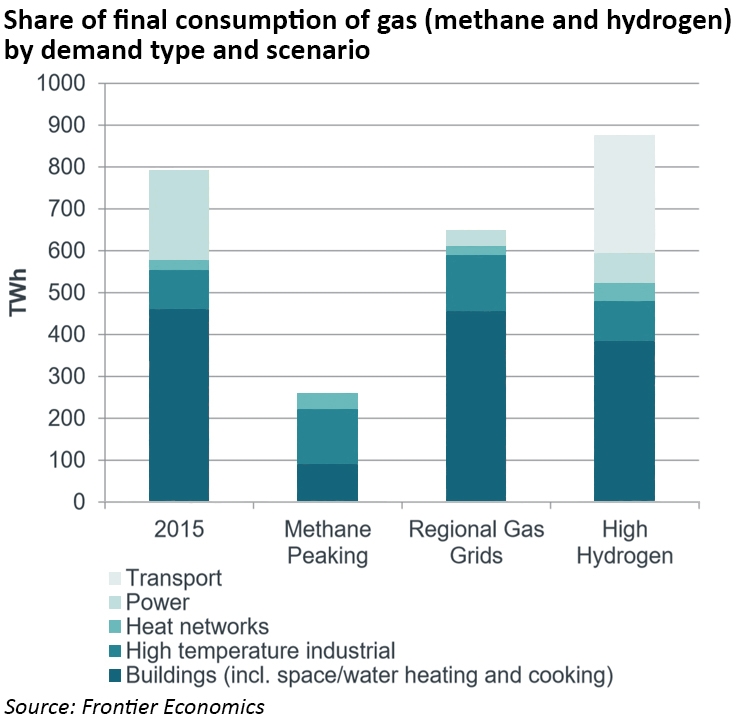

As part of its wider research into heat decarbonisation, BEIS commissioned Frontier Economics to objectively describe challenges likely to be associated with a low carbon gas system. Frontier Economics developed three scenarios for 2050 gas use:

- High Hydrogen: involves the conversion of all gas supply to hydrogen. In addition, most of road transport switches to use electric vehicles powered by hydrogen fuel cells (alongside some use of plug in electric vehicles), significantly increasing total national demand for gas. Overall, transport demand makes up almost a third of total hydrogen demand under the scenario. End use in buildings is predominantly made up of the use of hydrogen boilers that are not dissimilar to today’s gas boilers.

- Methane Peaking: describes a system where hydrogen is not available and where the cost of producing low carbon methane (both nationally and internationally) rises sharply as production increases. The resultant scarcity of low cost low carbon gas means that its use in the energy system is focussed on supplying high-temperature industrial processes, where few low carbon substitutes are available, and for meeting peak heat demand via hybrid heat pumps.

- Regional Gas Grids: involves the separation of the existing national grid into a multiple separate pipeline grids. About 70% of total gas demand met from hydrogen; the rest is met by low carbon methane. Buildings end-use remains similar to today, with methane or hydrogen boilers used to heat water and provide space heating. The electrification of transport creates localised grid reinforcement issues, which creates new demand for the deployment of distributed electricity generation using fuel cells or micro-CHP.

“The overarching conclusion from this model development work is that none of the scenarios implies a radical reinvention of the market and regulatory structures currently in place. While significant regulatory changes may be required, for example to facilitate greater coordination between energy vectors, many aspects of the market and regulatory framework could remain similar to those in place today.”

The key conclusions of the study were:

- Upstream production could be built around a competitive commodity market and the scale of gas production plants is relatively modest (for example, around 500 MW for steam methane reforming units), and the capital required for low carbon gas production may be smaller for natural gas production today.

- Pipeline gas networks could remain regulated natural monopolies with the role of gas networks remaining largely the same as today across all three scenarios.

- Storage should be able to operate competitively, although some intervention may be desirable for security of supply reasons, storage as a service will not differ markedly from what we see today.

- Changes in end demand may stimulate the creation of new retail propositions, particularly where end use technologies span both gas and electricity (as for hybrid heat pumps, fuel cells and micro-CHP in the Methane Peaking and Regional Gas Grid scenarios). Energy suppliers might develop retail services that offer lower cost energy services in exchange for the control necessary to optimise the consumer unit’s operation.

- Greater coordination at the system operator level across the gas and electricity sectors may be desirable – as the end use technologies span gas and electricity networks there will be greater interaction between the two markets which may unlock potential efficiencies, like new mechanisms for network congestion management.

- The gas transport system may be more complex – alongside pipeline systems, all also envision the potential road transport of gas. The system operator role at the distribution network level may need to expand to accommodate injection into their networks from distributed anaerobic digestion plants in the Methane Peaking and Regional Gas Grids scenarios and from electrolysis plants in the High Hydrogen scenario.

However, while market and regulatory models may not need to fundamentally change, the infrastructure and technologies used across the value chain would be radically transformed in the transition to a low carbon gas system, with issues arising in the following areas:

- Managing technology uncertainty – there is a large degree of uncertainty over which is the best scenario to pursue, given limited information on the feasibility of some key technologies, future relative costs and consumer preferences, as well as the potential for disruptive technologies and unforeseen events. Investment in demonstration will be required in the near term for hydrogen systems, hybrid heat pumps and syngas production. Whichever scenario is pursued, roll out of capital investment will be required from 2030, after which point changing strategy would be most difficult and costly if High Hydrogen is pursued, given the need for a new pipeline system.

- Co-ordination requirements and policy risk – investors across the value chain need confidence there is long-term political will to tackle the emissions externality and decarbonise the gas sector. There will be a significant need for co-ordinated policies to ensure a smooth transition to a lower carbon gas system whichever scenario is chosen, including a greater degree of co-ordination between the gas, electricity and district heating sectors. There is also a need to develop appropriate incentives such as CfDs and cap/floor arrangements.

- Consumer experience and protection – in all scenarios, the technologies consumers can choose from will change, with heat pumps, hybrid heat pumps and hydrogen appliances all potentially being used. Successful de-carbonisation of heat will rely on consumer support, so measures to incentivise consumers and avoid excess costs, as well as protecting vulnerable customers will be important.

Adding hydrogen to existing natural gas networks

A trial at Keele University will assess the feasibility of adding hydrogen to the gas network to reduce carbon emissions. Current regulations restrict the amount of hydrogen in the gas network to 0.1%, owing to the naturally low levels of hydrogen of the North Sea gas – the HyDeploy project aims to blend up to 20% hydrogen into the current natural gas network without disrupting current appliances.

The HyDeploy project is led by gas network Cadent, in partnership with Northern Gas Networks, and is planning a one-year trial on Keele University’s private gas network starting in 2019. The hydrogen will be produced on-site via electrolysis, and will be mixed with before the gas enters the pipes via a special injection and mixing unit.

The Health and Safety Executive will need to provide an exemption for HyDeploy to exceed the current allowed hydrogen concentrations, and will also need to be satisfied about the safety of hydrogen before the trial will be approved. HyDeploy is currently studying how the blended gas will burn in appliances, how it will affect material in the gas network, and how to safely deal with any leaks.

Hydrogen and natural gas blends have already been successfully trialled in the Netherlands and Germany, and a similar project is underway in France, although these trials differ in some respects from the HyDeploy project due to the differences in the UK network.

Cadent is also developing a project to potentially introduce hydrogen into the gas network in the Manchester-Liverpool region. Natural gas would be converted into hydrogen through steam methane reforming, and the carbon captured and stored in depleted offshore gas reservoirs in the Liverpool Bay oil and gas fields. The hydrogen would then be supplied to a core set of major industrial customers in the area, and fed into the local gas distribution network as a blend with natural gas.

Full conversion to hydrogen

Northern Gas Networks (“NGN”) is exploring the feasibility of a 100% hydrogen system. In November, NGN secured £10.3 million of funding from Ofgem and the UK gas distribution networks to further build on the work of the 2016 H21 Leeds City Gate project which established that hydrogen conversion is technically possible and economically viable.

The Leeds City Gate project considered the possibility of building a series of steam methane reformer plants around the city, taking methane from the national gas grid and converting it into hydrogen by removing the carbon. This strategy would remove the issues around transporting hydrogen in the high pressure gas network, where a replacement of the pipes would be required. The carbon would then be stored, potentially in a disused North Sea gas field, while the hydrogen would be transported to households and businesses in Leeds.

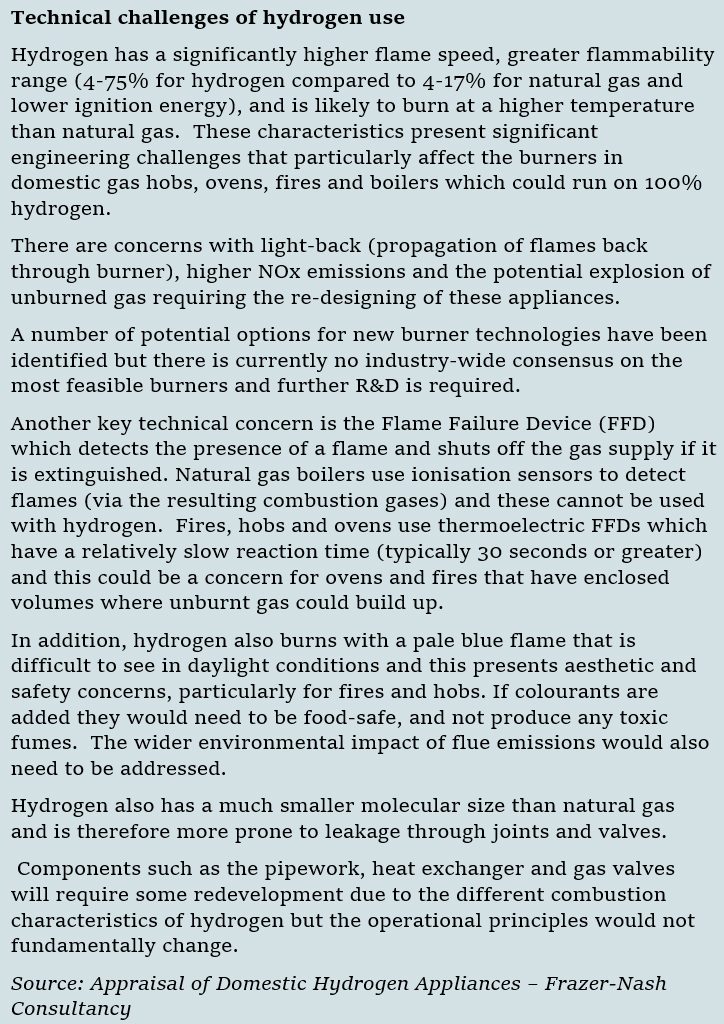

Impact of hydrogen gas on domestic appliances

A study by Frazer-Nash Consultancy concluded that adapting existing natural gas appliances to hydrogen is possible in theory, but it is unclear whether a conversion kit for the burner can be developed that is sufficiently universal to fit all different product variations. The performance of these appliances is likely to be lower when running on hydrogen since components would not be optimised for hydrogen use. In the context of a single gas changeover, the study concluded that hydrogen-ready dual-fuel appliances could be developed that would be designed with future hydrogen use in mind but capable of running on natural gas in the interim.

“Dual-fuel appliances that can interchange between natural gas and hydrogen without the need to replace components are not considered practical.”

However, the study highlighted the need for consensus on the fundamental technical challenges of hydrogen use: burner technology, flame colouration, cooking performance, flame sensors and pipework, and concluded that government intervention will be required to realise the development of hydrogen appliances.

Role of finance

Energy UK is urging the Government to provide stronger guidance to the markets to signpost the direction of travel on de-carbonisation of heating in order to stimulate the development of technologies and business models. In its report, Energy UK notes that local authorities will play a key role in co-ordinating moves to lower carbon heating, as district heating schemes are developed in more towns, and low carbon heating is installed in social housing, however current funding models would struggle to support these moves.

Property developers should also be incentivised to incorporate low carbon heating in private homes and commercial buildings, potentially extending existing Feed-in-Tariffs for small-scale generation to low carbon heating installations, with these schemes also targeting housing associations and private landlords. Innovative financing structures such as green mortgages could play a part in incentivising both energy efficiency and low carbon heating schemes, with support schemes for low income households.

Based on a 10-15 year lifespan for the average domestic boiler, there will be two or three replacement cycles between now and 2050, providing opportunities for installation of lower carbon solutions. Policies should be developed to ensure these opportunities are not missed.

Outside the domestic sphere, Energy UK believes the Government should be supporting the development of supply chains, but with a technology-neutral approach. A re-vamped Renewable Heat Incentive should seek to stimulate action from small and medium-sized business since so far only large organisations have participated in the scheme.

The de-carbonisation of heat is a challenging problem that will require a combination of technologies and strong, well co-ordinated policy support. However, despite the upbeat tone of many recent reports, most “solutions” require CCS in one form or another, and to date CCS remains an unproven technology except in the context of enhanced oil recovery, which hardly sits well with de-carbonisation goals.

The high costs of de-carbonising heat will further drive up energy prices, fuelling consumer discontent, so policy-makers would be well advised to focus on areas where consumers would benefit directly, such as energy efficiency. In the meantime, before committing consumers and tax payers to the costs of de-carbonising the heating segment, there should be a wider debate on the need for de-carbonisation and the associated costs.

Hello,

A bit late to comment on this ‘vision’ of the future.

A couple of thoughts spring to mind:-

I do not consider urgent decarbonisation ( 2050!) necessary

Very little mention of where the electrical power will come from:-

-to use electrolysis to produce hydrogen

-CHP fuelled by what- maybe hydrogen

and so the visionaries go on and on.

Thanks Kathryn for your measured comments.

Nick Perrin.

Hi Nick,

It’s never too late to comment!

I agree completely, everyone is suddenly talking about the “challenge” of de-carbonising heat, and no-one is taking a step back to ask if it’s actually necessary (even if you buy into the CO2 causes climate change theory, mitigation may be less expensive than prevention), or viable (CCS doesn’t work but just about every 2050 scenario assumes it does)…

Element Energy carried out a study for the Government on the potential use of hybrid heat pump (“HHP”) systems in the UK’s long-term de-carbonization of domestic heat. For the purposes of the study, an HHP system was defined as one combining an electrically-driven heat pump with a gas boiler, along with a dedicated controller.

Here is a link to the study for anyone who is interested:

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/700572/Hybrid_heat_pumps_Final_report-.pdf