The energy landscape is an increasingly confusing one for consumers – with new entrant suppliers going out of business, the introduction of price caps, and the on-going controversy over smart meters. The latest issue is the fuss suddenly being made about so-called “surge pricing” by which suppliers are apparently going to hike prices for consumers at times of high demand such as Christmas and Easter. Many of these problems have their roots in a number of myths about the industry that are believed by the public and in some cases by policymakers. In this short series of posts, I will explore some of these myths and why they are taking energy policy in the wrong direction.

Myth #1: Energy supply is a lucrative business with the Big 6 suppliers earning billions in excess “profits”

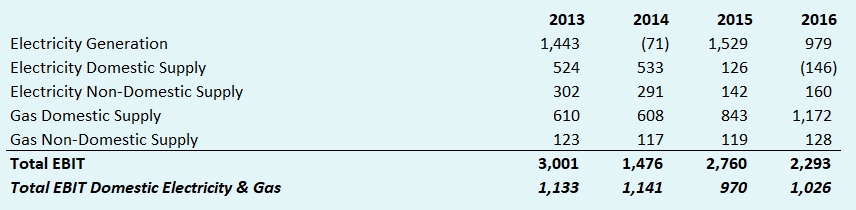

This myth has gained traction since the Competition and Markets Authority carried out an in-depth investigation into energy supply businesses and found that the domestic customer detriment due to overcharging by suppliers was around £1.4 billion per year over the period 2012-15 under once analysis approach, and around £720 million/year over the 2007-14 period using a different method.

“For far too long older people, hard-working families and those on low incomes have been subject to rip-off energy tariffs,”

– Theresa May, Prime Minister

As I have described before, this figure is inconsistent with the Consolidated Segmental Statements by the Big 6 – reports that are prepared by their external auditors based on guidelines issued by Ofgem, that must reconcile with the suppliers’ audited accounts. Aggregated data for the Big 6 suppliers are shown in the table above and indicate that the only way that over £1 billion of excess profits could be earned would be if reported profits in the non-domestic segments including generation were in fact earned from domestic end users (or the figures are completely wrong/distorted in other ways). This could be the case, but neither the CMA nor Ofgem has said they believe this is happening, nor taken any action to prevent it.

The latest bills breakdown published by Ofgem (also based on the Consolidated Segmental Statements) show that retail electricity supply is a loss-making activity for the Big 6:

Although margins on gas are healthy at 10%, the margin for dual fuel customers is 4.83%, which is reasonable but hardly a goldmine.

New entrants lured by the prospect of easy money find the going tough

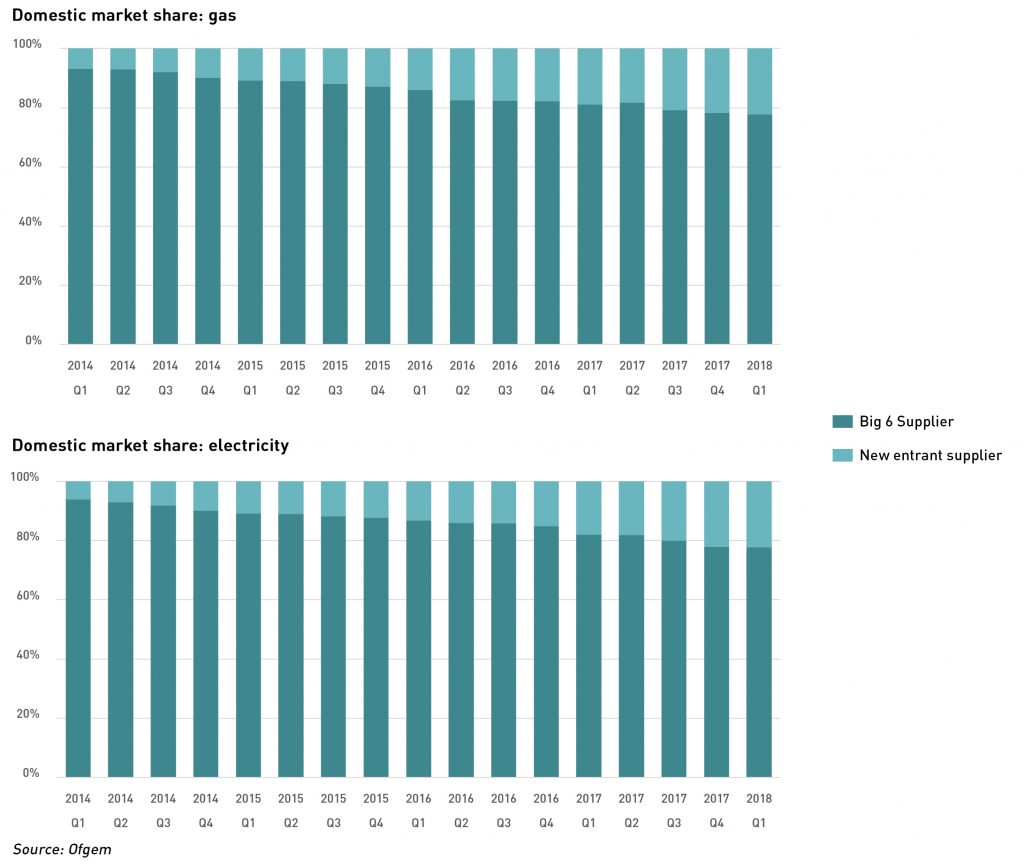

The problem with this myth is that new entrant suppliers are encouraged to come and take market share from the Big 6, however setting up a functioning supply business is hard. Gas and electricity are largely commoditised, so new entrants must either identify a particular consumer preference such as local or green energy, or they must compete on price, but since margins are low (and negative for electricity) it is challenging to develop a successful low-cost supply model.

This is illustrated by the growing number of suppliers that are going out of business, most recently Iresa, which had faced a number of operating restrictions from Ofgem due to poor customer service and high levels of complaints, and finally closed its doors last month. So far this year, five small suppliers have exited the market: Brighter World and Future Energy both closed in January, followed in April by Flow Energy, and National Gas and Power, which supplied the non-domestic sector had its supply licence revoked in July after becoming insolvent.

The next failures are on the horizon with reports that Gen4U has had all of its trading contracts cancelled and has withdrawn its tariffs from the market, and Electraphase, which appointed administrators on 6 August.

Trying to force switching

Since the CMA identified low switching levels as a sign of market disfunction, Ofgem has been exploring ways in which switching can be stimulated for disengaged consumers. This has meant that suppliers will be required to share the data of such consumers to the Disengaged Customer Database (with all of the privacy concerns that go alongside such as scheme), and has been considering ways in which these customers can be incentivised to switch supplier, for example by allowing other suppliers to target them (which is highly likely to make both the original supplier and prospective suppliers breach the General Data Protection Regulation, so it’s hard to see how the scheme could be legal).

Consumer group Which? has also found that 80% of consumers are likely to either opt out or ignore any communications arising from the scheme, limiting its effectiveness.

“Consumers should vote with their feet. Switching suppliers will always help consumers to get the best deal,”

– Claire Perry, Energy Minister

In February, Ofgem trialled the “Active Choice Collective Switch” initiative, in which 50,000 inactive consumers were provided with a calculation of their savings if they switched to an alternative tariff determined by “an Ofgem-appointed consumer partner organisation”. The role of the consumer partner is to:

- negotiate a price competitive, ideally market-leading tariff;

- calculate the saving each customer could make and let them know what it is;

- provide online and phone routes to switch to the new tariff and/or conduct a wider search comparing tariffs across the market.

Ofgem is yet to report on the outcome of this trial, but the Sunday Telegraph reported this week that almost 13,000 customers were encouraged switch to a new entrant supplier that is “unable to pay its bills”. According to the newspaper, SSE sent over 176,000 letters to customers part of the trial, of which 12,917 encouraged customers to switch to Electraphase, which trades under the name E-phase, and which, as noted above, has recently gone into administration.

Where does this leave the competitive landscape?

While smaller suppliers are finding the market increasingly challenging, the Big 6 are also feeling the pressure, which is emerging in three ways:

- firstly, all of the larger energy suppliers (and many smaller ones) have been increasing their prices, most recently British Gas announced its second increase in its standard variable tariff this year;

- secondly, the larger suppliers are in the midst of various corporate re-structurings and/or mergers and divestments in order to better position themselves in the face of difficult market conditions;

- and thirdly, the larger suppliers are exploring new business avenues such as energy services, distributed energy and the connected home segment.

In addition, several larger non-energy companies are targeting the sector, and are more likely to be successful than the many smaller new entrants (that are also often start-ups).

Energy supply is a complex business, but few people understand this and why current energy policy is driving costs higher and service lower.

The basic energy supply business involves procurement of energy in wholesale markets (gas and electricity or the fuels for the generation of electricity for vertically integrated suppliers). This involves managing volume risk as well as price risk, since participants in the wholesale markets must maintain balanced positions every day for gas and every half-hour for electricity. Having an imbalanced position exposes the supplier to imbalance prices which cannot be hedged and which can vary from a few pence to thousands of pounds per kWh.

Suppliers must also pay a share of the transmission and distribution network costs incurred in the delivery of energy to their customers, which are growing due to the effects of de-carbonisation. Suppliers are also required to recover the costs of various environmental and social policies through bills, such as the costs of renewables subsidies, and the smart meter roll-out.

All of this makes the administration of the supply business highly complex, requiring sophisticated billing systems – something suppliers have generally done badly. Despite the complexity, this has been an own-goal which has allowed successive governments to place the blame on suppliers for rising costs, on the basis of their inefficiency and profiteering, rather than the pressure created by energy policy.

“This latest price hike is another slap in the face for energy customers who are already feeling the pinch and can’t see any real difference in the service they’re receiving. We would urge the nine million customers affected by the Big Six price hikes to take back the power by switching to a better deal, as they could save over £400 a year,”

– Alex Neill, Managing Director of Home Products and Services at Which?

The problems experienced by new entrant suppliers such as Iresa demonstrate the difficulties of running a supply business very well. Iresa positioned itself as a low-cost supplier in order to win customers, however it simply did not have the systems in place to cope with the customers it acquired, leading to large numbers of complaints and restrictions being placed in its operations by Ofgem. Eventually it simply collapsed.

It is tempting to conclude suppliers must either be large (due to legacy positions or entry from other markets), or very small with modest growth aspirations, neither of which looks like the sort of competition the Government seems to want in the industry.

Where next for retail market regulation?

There are now calls on Ofgem to tighten the rules for new entrants as the barriers to entry are considered to be too low, while at the same time, the Government believes the market is insufficiently competitive and has introduced a retail price cap as a means to prevent the Big 6 suppliers from exploiting their dominant market position.

The reality is that retail energy supply is not a lucrative business, and that while barriers to entry are too low, barriers to effective operation continue to be too high. Setting up the operational systems needed to service new customers is not cheap, and new entrants still struggle to manage price risk despite initiatives such as Secure & Promote making them vulnerable to swings in wholesale and imbalance prices.

The steps needed to fix this are unlikely to happen (such as recovering policy costs through general taxation rather than bills; and an end to the narrative from the Government that suppliers are profiteering at the expense of ordinary consumers), which places Ofgem in a difficult position trying to stimulate competition while ensuring that new entrants have adequate resources to operate effectively.

Ofgem will almost certainly introduce new licence conditions for suppliers, possibly around capital adequacy, and resourcing. This may stimulate some much-needed be consolidation among the smaller new entrant suppliers, as those that do not meet these new requirements will need to either find new investment or join with a larger supplier – failure to do so would lead to the withdrawal of their licence and the allocation of their customers to another non-Big 6 supplier.

Effective competition in the energy markets will not come from dozens of minnows, but from a smaller number of companies with the heft to challenge the Big 6 over the long term.

Energy myths series Myth 1: Energy supply is not a goldmine and life is tough for new entrants Myth 2: The retail price cap will not save money for consumers Myth 3: Smart meters will not save money for consumers Myth 4: Renewable electricity is not cheap |

Hi Kathryn,

Thanks for the article; I’m looking forward to the rest of the myths. I recently read an interesting proposal by Stephen Littlechild that would seek to give new entrants greater clout and impose greater competitive pressure on the Big Six.

He suggests the Big Six suppliers be invited to transfer to a subsidiary company 10% of their total existing customer base, then sell this subsidiary to one or more new entrants (with a suitable number of caveats, for example customer opt-outs). This approach would stimulate competition and give new entrants a better opportunity to prove the merits of their prices and customer service.

https://www.eprg.group.cam.ac.uk/wp-content/uploads/2018/01/S.-Littlechild_DailyTel_10Jan18.pdf

I’m not sure about this idea – surrendering customers is very different to surrendering assets, and when Lloyds TSB customers were forced into TSB many were unhappy. If customers were allowed to opt out, many would have done, and GDPR (which wasn’t in force during the TSB spin-out) requires active opt-in, so allowing suppliers to pass customer data to third parties without explicit consent would probably violate data privacy laws.

I think the real problem is this: most suppliers (not just the Big 6) offer sweetheat deals to new customers that are cheaper than the deals available to existig customers – one type of customer subsidises another. If the ability to earn higher margins on the “worst” tariffs is reduced or removed, there will be tariff convergence, the difference between best and worst tariffs will narrow, and switching will become irrelevant.

If the Big 6 are disporportionally penalised they will either exit the GB supply business, or become loss-making and run into financial difficulties, potentially requiring bail-outs (as happened in California). At which point, the current means of environmental policy cost recovery would have to change and either smaller suppliers would have to take more of a share, or the costs would be removed from bills altogether (my preferred option).

I don’t know if this is actually a zero-sum game, but I think it’s probably not far away – the costs of supplying end consumers are high and largely outside the control of suppliers, meaning that switching, caps and so on can not reduce costs on a market-wide basis.

A more meaningful intervention might be to make it easier for smaller suppliers to hedge wholesale price risk. Secure & Promote is limited since larger suppliers cannot be forced to take unreasonable credit risk. There might be a way for a guarantee scheme to be implemented for smaller suppliers, funded by industry levy, to allow them to hedge efficiently. I’ve no idea if the numbers stack up, but removing barriers to hedging without exposing individual market participants to excess risk could be helpful.

It is often overlooked that domestic consumers are the most volatile demand segment. Demand from industrial and commercial customers for process use, lighting and air conditioning of shops, offices and warehouses is much less seasonal or weather dependent than demand from households. Streetlighting demand is a low risk supply aside from winter rush hours. Big 6 suppliers will benefit from large customers who will reduce demand during triad periods, reducing the risk of exposure to high price, high volume demand for the supplier. precisely the converse of the small supplier, who will find domestic demand soaring and no triad protection. Worse still, some of the “green” customers will have their own solar panels, reducing visible demand still further during sunny summer days when prices are likely subdued.

Assembling a less volatile, easier to hedge customer portfolio is hard for the small firm. Those who indulge in portfolios of green generation investment are also doing themselves few favours, other than as a marketing ploy. Their windfarms are likely to be lower average capacity factor onshore efforts, which will tend to produce when there is likely a general surplus of power and lower prices, while they will be left having to buy in precisely when their own assets aren’t generating anything meaningful and wholesale prices are high, so they offer no useful hedge.

Many smaller firms have survived initially because they established themselves close to a market peak, and chose not to pay out on forward hedging, thus putting them in a strong position to undercut the heavily hedged Big 6 in periods of falling wholesale price trends (as in the two years or so after Miliband called for a price freeze ahead of the 2015 election). Of course, when the market turns, they are rapidly exposed. Long forward hedges require substantial collateral if they are not natural hedges from a suitable generating portfolio – which is itself a substantial capital investment.

I have some suggestions to make:

1) Small firms (and eventually, all firms) should be allowed to buy from any wholesale supplier without renewables obligations. Of course, this will in time tend to undermine uncompetitive renewables, but that is in any case a desirable outcome.

2) Market entry should encourage the development of customer portfolios that are not dependent on mainly supplying the domestic household market. Competition to the Big 6 cannot survive if they have disproportionate exposure to events such as the Beast from the East.

3) OFGEM should stop pushing its model of heavily forward hedged benchmark pricing as in their estimated customer bills, and customers should be encouraged to separate out price insurance (fixes, caps) from basic supply, which should be tethered to a much shorter term, much more transparent benchmark – e.g. average NBP price marker for month ahead gas, plus a much more transparent pricing of other costs. Banks and financial institutions are far better capitalised and able to manage portfolios of hedge risk than individual small retailers, as they are often in a much better position to find a counterparty to take some of the other side of the risk, or otherwise reduce portfolio risk. This would also leave much more room for competition on standards of service.

4) Offerers of hedge products should be required to educate their customers on the basic economics of fixes and caps,

5) Much more risk needs to be pushed upstream: it is absurd that network charges pay so little heed to the location of generating assets. This has resulted in generation being located far from demand, instead of close to it, raising transmission costs, and penalising customers who now find themselves in regions of supply deficit. The failure of wind and solar farms to provide firm, dispatchable power incurs little penalty: Helm was entirely right that intermittent supply should pay for the cost of its intermittency – not loaded onto retailer bills as balancing charges.

5) There needs to be much better education of the public. It should be forbidden for companies to advertise that they sell only green electricity unless they install smart meters that cut supplies when the wind drops. OFGEM should provide something like this widget for the NEM in Australia:

https://opennem.org.au/#/regions/sa

It shows the contribution of each kind of generation, and the average value of that contribution measured at system spot prices, with ready access to a history and data aggregated over longer periods. A small but necessary refinement would add the average estimated price achieved via CFDs, ROCs, etc. – showing clearly what subsidies are being doled out – and what taxes and levies are being raised.

Only by informing the public properly do we stand any chance of seeing proper debate as to whether we should be investing so heavily in renewables or unduly expensive nuclear, and only through winning that debate can the public hope to see lower energy bills.

Meanwhile, the government needs to work out how to reduce the subsidy bills it has committed itself to. A windfall profits tax of some sort needs to be devised at the very least: it would be easy to get the public behind it by accusing wind farms etc. of having pulled wool over the eyes of OFGEM, DECC/BEIS and the public in demanding such high subsidies – and having thus cheated, they should be penalised. Of course, it is also necessary to ensure that we retain sufficient other generation to keep the lights on – but that is another story.

I agree. I think a big part of the problem is that “competition” is seen by the Government and Ofgem as it relates to the domestic market and then SMEs – they don’t care as much about larger I&C.

Ofgem could do a lot more to educate both customers/the public and new entrants, many of whom lack experience in managing trading price risks and are buried by the dozens of regulatory obligations imposed on suppliers.

Life would be much more transparent and competition would be more effective if some of these obligations were removed – particularly recovery of environmental & social costs – and if system costs were allocated more appropriately.

So yes to Helm’s proposals on making the creators of intermittency pay for the management of it, and yes to better locational transmission pricing. Brexit might also allow for a better allocation of transmission costs between generation and demand since the EU currently caps the amount that can be charged to generators.

I completely agree about the need for better transparency and proper public debate about costs, but my belief is that successive governments have deliberately avoided this to obscure the costs of de-carbonisation. I think if the public understood the actual costs, and stopped being fed fairytales about 100% renewables, CCS and so on, there would be less support for the current direction of travel and far more support for gas, which is flexible, easy to build, has manageable capital costs, and is pretty clean (eg low particulate pollution).