Following close behind Myth #1 about the profitability of the energy supply business, comes Myth #2, that the retail price cap will see the end of “rip-off tariffs” and save money for consumers. I have already written a number of posts on the price-cap subject, since I believe they are likely to do more harm than good. In this post I will explore in more detail the reasons why the cap is unlikely to save money for consumers.

Myth #2: The retail price cap will save money for consumers

In 2016, the Competition and Markets Authority (“CMA”) found that 70% of Big 6 customers were paying standard variable tariffs which are more expensive than other deals available in the market, and recent figures from Ofgem suggest 12 million households remain on default tariffs despite the availability of better deals.

With switching rates remaining stubbornly low and a high proportion of consumers being considered “disengaged”, the Government has introduced a cap on the amounts suppliers may charge with their standard variable /default tariffs. The Domestic Gas and Electricity (Tariff Cap) Act 2018 received Royal Asset and passed into law on 19 July.

“The Government wants markets to thrive and we continue to promote competition as the best driver of value and service for customers. The Government is prepared to act, however, where markets are not working for all consumers, and the energy market is a clear example of this.

Last year the Competition and Markets Authority found that customers of energy suppliers were paying £1.4 billion a year more than they would be in a truly competitive market. Vulnerable and low-income customers are more likely to be on the most expensive standard variable tariffs,”

– Greg Clarke, Secretary of State for Business, Energy and Industrial Strategy

Ofgem must now develop the cap methodology with the following objectives:

- protect existing and future domestic customers who pay standard variable and default rates;

- create incentives for holders of supply licences to improve their efficiency;

- set the cap at a level that enables effective competition for domestic supply contracts;

- maintain incentives for domestic customers to switch to different domestic supply contracts;

- ensure that holders of supply licences who operate efficiently are able to finance activities authorised by the licence.

As noted in my previous post on the myth of supply business profitability, the Big 6 suppliers earn an average margin of 4.83% on dual fuel bills – on an average standard variable dual fuel bill of £1,172, this margin is £57 per year. It is difficult to see how the £100 per year savings promised by the Conservatives when they launched their price cap plan can be realised.

This will make it challenging for Ofgem to determine the appropriate level for the cap: to meet objective (v) above, suppliers will need to be profitable, but the market response to the cap as set out below will make it hard to meet objective (iv). Arguably, incentives to improve efficiency already exist since margins are low, but the Big 6 suppliers are restructuring and shedding jobs to try to cut costs further. Ofgem’s room for manoeuvre is very limited.

What next for energy bills

“Victory for consumers as cap on energy tariffs to become law,”

– UK Government press release

With the price cap expected to come into force by the end of the year, a number things is likely to happen:

Smaller gap between best and worst tariffs leading to lower rates of switching

The first is that suppliers use higher priced tariffs to subsidise cheaper tariffs. If they are unable to generate sufficient income from their more expensive tariffs their ability to offer cheaper tariffs will fall, so the gap between the best and worst tariffs will narrow, penalising those consumers that do actively switch provider. As a result, switching rates will decline, as the benefits of switching become too small to justify the inconvenience.

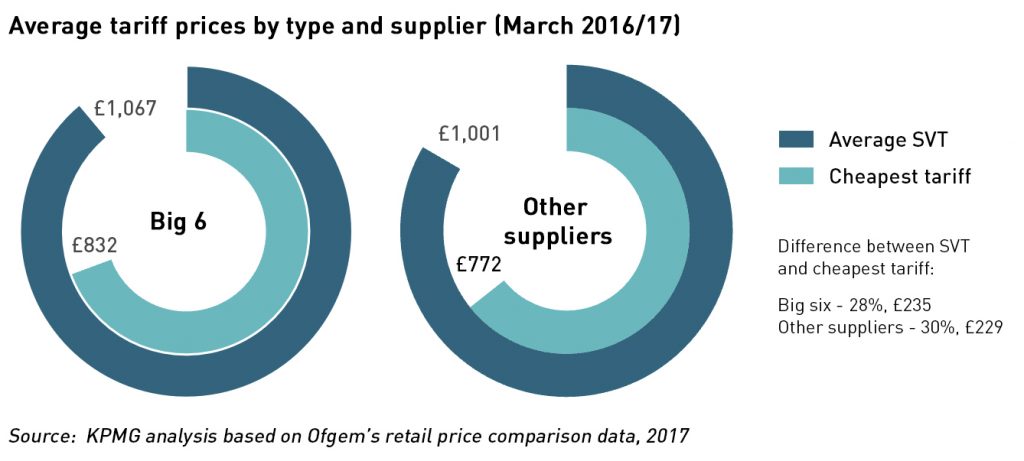

A 2017 report by KPMG suggested as much. It found that the difference between standard variable tariffs (“SVTs”) and fixed-price tariffs was already narrowing in anticipation of the cap’s introduction – not by reducing SVTs but by increasing average fixed-price tariffs. Between early 2016 and April 2017, the gap reduced from more than £300 to less than £150, and according to the most recent data published by Ofgem (December 2017), the gap was down to £134.

“A price cap, whether relative or actual, will lead to many of the best deals disappearing, prices finding a higher level and a growing market of disengaged customer,”

– Stephen Murray, MoneySuperMarket

The Ofgem data also illustrate that the Big 6 suppliers are not alone in applying cross-subsidisation between tariffs:

Reduced profitability for suppliers is changing the competitive landscape

Secondly, as suppliers are not actually making huge profits on their supply businesses, it will be difficult to set the cap significantly below current price levels, so savings will not be significant. If the average value of the cap exceeds £57 per year, it will make the entire sector unprofitable. Suppliers may try to avoid supplying certain consumer groups, and some may face financial difficulties – this month saw the news that E.On was cutting 500 staff as a result of the price cap, while Centrica expects to cut 4,000 jobs, and SSE is exiting the supply business altogether.

“[The price cap will be] potentially putting at risk the billions in investment and jobs needed to renew our energy system,”

– Lawrence Slade, CEO of Energy UK

The KPMG report also found that innovation in the sector was likely to fall as supplier profits are eroded by the cap, and investor confidence could suffer, as evidenced by the drops in the share prices of the listed energy suppliers on news of the cap.

When California introduced a retail price cap in 2000, it ended up bailing out one of the largest suppliers, acting as the sole buyer of electricity on behalf of utilities, and providing rebates to consumers that agreed to cut consumption, all at a cost of billions of dollars.

Smaller suppliers are expected to be less impacted by the cap since the requirements to recover energy policy costs are linked to customer numbers – suppliers with fewer customers are therefore able to offer lower tariffs excluding policy-related costs. On the other hand, smaller suppliers are more exposed to wholesale price risk as hedging on small volumes is difficult and they are often constrained by their generally weak credit status.

If there is a market shift that results in the Big 6 having a smaller market share than non-Big 6 suppliers, there would need to be a change in the rules around policy cost recovery. The Government seems committed to recovering these costs through bills rather than through general taxation, but there will be a point at which the current method becomes unsustainable if the larger suppliers find themselves unable to offer competitive tariffs or recover all of their costs within the cap regime.

Frequent cap increases as fundamental price drivers continue to rise

Thirdly, the underlying drivers of price increases are not likely to reverse any time soon, meaning that the cap will need to be frequently re-adjusted to keep pace with costs that are outside the control of suppliers, as it has been doing with the safeguard tariff cap on pre-payment meters.

Wholesale energy prices have risen significantly this year, and have been a key driver of price rises announced by many suppliers in recent weeks, not just the Big 6. Day ahead gas prices have risen from 55p/therm at the start of the year to 62p/therm, a rise of 13%, while electricity prices have increased from £46.06 /MWh to £58.27 /MWh over the same period, a 21% rise. While larger suppliers can implement hedging programmes to manage this risk, it is difficult for smaller suppliers to do the same primarily due to volume and credit constraints, and no suppliers can do anything to manage the costs of network charges and environmental/social costs.

The Office for Budget Responsibility calculates that environmental levies will more than double between 2016/17 and 2022/23, increasing from £5.2 billion to £12.8 billion. This does not include the £11 billion cost of the smart meter programme.

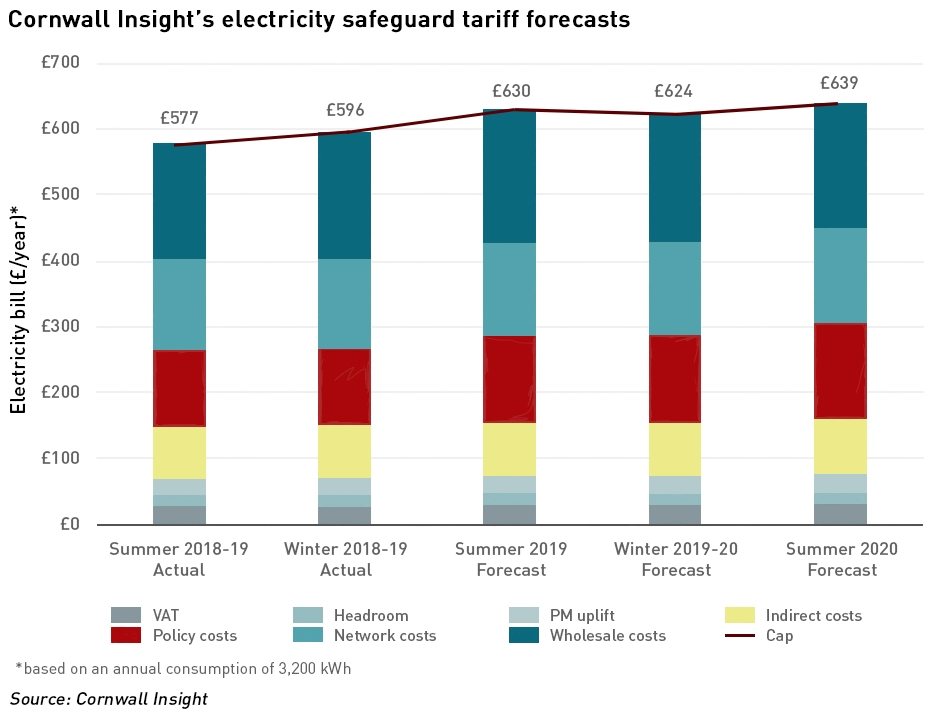

The pre-existing cap on prepayment tariffs has been regularly increased by Ofgem, most recently this week with a £47 per year increase in the safeguard dual fuel tariff for the coming winter. Cornwall Insight predicts that a further increase of £33 per year can be expected next year, driven by increases in policy costs of £16 /year, network costs of £5 /year, and wholesale costs of £9 /year.

“Household energy prices are set to continue to rise despite Ofgem’s safeguard tariff or the government’s default price cap, which is set to replace it later this year. At a constant consumption the cap is increasing at 10% year-on-year because of rising input costs to suppliers. Only if wholesale costs fall sharply will the pressure abate,”

– Gareth Miller, CEO Cornwall Insight

Any savings will be small and short-lived, and active consumers will see prices rise

The views of politicians on the energy price cap seem to be entirely divorced from reality. Energy suppliers are not in fact earning billions in excess profits and a cap that generates savings of £100 per household per year would certainly make the supply businesses of the Big 6 unprofitable. As a result the suppliers are re-organising their businesses, cutting jobs and in the case of SSE, exiting the supply business altogether.

Suppliers across the spectrum seem to be responding by increasing the cost of their best deals, narrowing the gap between the best and worst deals. This reduces consumer choice and the incentive to switch.

While some consumers on SVTs may see small reductions in their bills when the cap is introduced, those consumers that have switched supplier in the past will find the best available tariffs are more expensive. Recent increases in SVTs mean meaningful reductions are unlikely for any consumers, particularly if the date of the cap’s announcement is used as the reference point.

In addition, the absolute levels of all tariffs will continue to increase as the fundamental drivers of energy bills keep rising. Ofgem is likely to increase the cap in response, as it has done with the existing pre-payment meter cap, meaning that costs for consumers will continue to rise irrespective of the cap.

It’s hard to see how any of this can be described as a “victory for consumers”.

Energy myths series Myth 1: Energy supply is not a goldmine and life is tough for new entrants Myth 2: The retail price cap will not save money for consumers Myth 3: Smart meters will not save money for consumers Myth 4: Renewable electricity is not cheap |

I agree with your thesis here. The only way we may see some “cheaper” deals in future is some distant date when smart metering operated with ToU tariffs that some consumers are able to take advantage of – but the cost of being able to do so may be substantial, with a need to replace appliances with ones that respond to tariffs in some sensible fashion (you don’t want the cooker to die just in the middle of roasting Sunday lunch). The corollary of that is that other consumers would be on the wrong end of surge pricing, which might prove very expensive indeed. The only safeguard would be behind the meter investment in off grid generation and storage – again at great cost.

The real need for more competition is upstream. At the moment, there is none worth speaking of, with renewable generation guaranteed large subsidies and if not dispatch, then curtailment compensation, and the cheapest cost power (often coal) being excluded by quota and taxation. Only by reducing the costs of generation and transmission (by locating generation to match local demand, leaving the grid mainly to handle smaller imbalances and trips rather than long distance transmission of major slugs of power from far off wind farms etc.) can consumer bills be lowered. The retail distribution business is broken.

A good starting point would be to repeal Ed Miliband’s 2010 Energy Act that gave primacy to green interests.

Even with ToU pricing I don’t expect to see any bills going down in real terms since paying for subsidy commitments guarantees rising prices unless there is a sudden collapse in wholesale prices to offset the impact. At this stage even repealing the Energy Act wouldn’t prevent a lot of these costs, and building the new generation needed is only going to add cost if we’re committed to closing the rest of the coal fleet.

I think Ofgem’s idea of splitting domestic use into basic and additional consumption makes sense – some basic volumes would be exempt from ToU pricing to avoid harming vulnerable consumers and issues with ovens going off or being turned off to avoid peak prices. Excess consumption on things like EVs can then be charged at a higher rate. I would be surprised if super-cheap tariffs emerged because for essential consumption it would be a zero sum game.

I think that ToU would result in lower bills for a very small minority who are prepared to watch the pricing carefully (or invest in appliances that do it for them). I don’t think the investment would prove worthwhile any more that it is worth spending several hundred £s more for a fridge with an A+++ rating that has a lower internal capacity because of all the extra insulation it must fit into the 60cm appliance space in your kitchen, for the sake of saving £10 worth of electricity per year. In general, I expect ToU to result in rising consumer bills, because households come home at the end of the work day and prepare supper, switch on the TV, top up the heating, bung Johnny’s dirty games kit in the washing machine so it will be clean and dry for the morning, etc. at peak demand hours (which is of course why they are peak demand hours).

I do expect that when EVs become significant they will be on a white meter style arrangement, perhaps with a dedicated connecting cable style mandated by law. I would also expect that cars would have software that negotiated the overnight charge process with the meter, offering timing and power flexibility to the local distribution network where it is able to do so and also in the interest of good battery management. Capacity available for charging during the day will be limited, as this chart of a peak demand day shows:

https://uploads.disquscdn.com/images/9dc25c8f62d4fb76db6469410535451b5671f88fa89fd971a0c915c39f28c1ea.png

Indeed, there is a nice question as to what happens if the system succeeds in eliminating the small evening rush hour peak to that we have essentially flat demand through most of the day: would there be any spare capacity for charging EVs when we are depending on backup as in this example?

I don’t think there will be many people glued to their smart meters trying to eke out incremental savings, but various energy services might emerge where consumers set outcomes such as comfort levels, clean/dry clothes by 7am etc and the service provider programmes the home accordingly (of course the consumer still has to put that dirty kit in the washing machine ready to go when the cheaper rates start). It’s probably mst relevant with heating where the thermal capacity of the building can be used to avoid active heating during peak hours (in a world of electrified heating…).

I suppose that if the demand curve gets flattened out then new capacity will have to be built to meet any new demand if capacity margins are to be maintained, and then ToU pricing would be moot.