The energy retail sector has once again been in the news with the big energy companies raising prices – British Gas announced an average 5.5% increase, followed by EDF with a more modest 1.4% rise. Both companies linked the price rises to increasing wholesale and policy costs, with Ofgem citing similar pressures when it raised the prepayment meter limit earlier in April.

While Ofgem is consulting on the structure of the wider energy retail price cap proposed by the Government, analysis by Aurora Energy Research has found that policy costs will push up household electricity bills by almost a third by 2025, leaving Ofgem “little choice” but to repeatedly raise its price caps in future.

While Ofgem is consulting on the structure of the wider energy retail price cap proposed by the Government, analysis by Aurora Energy Research has found that policy costs will push up household electricity bills by almost a third by 2025, leaving Ofgem “little choice” but to repeatedly raise its price caps in future.

Payments to low-carbon technologies are expected to double to £15 billion, meaning the average contribution to policy costs will grow to £206 by the middle of the next decade – quarter of total spending on power.

Despite gains in energy efficiency and the proposed reduction in network returns through the proposed RIIO-2 price controls, the typical annual bill is forecast to reach £810.

“This will mean that, under the price cap model, Ofgem will have little choice but to allow repeated increases in energy prices for the foreseeable future,”

– Aurora Energy Research

Pressures for smaller suppliers: Flow Energy to exit the market….

Many new entrant suppliers attempt to grow market share through price competitiveness, but face procurement challenges due to their size, and may lack the resources to keep on top of the complex sets of regulatory obligations they face (I recently prepared a paper for a new entrant supplier outlining their obligations under various policy initiatives, which was both long and surprisingly difficult to prepare due to a lack of any single comprehensive source for such information providing the operational details needed for compliance).

It therefore comes as no surprise that some new entrants have been struggling. After a period of calm following the exit of GB Energy in 2016, Brighter World closed in January followed within days by Future Energy. Now we have seen the exit of Flow Energy, which has sold itself to Co-op Energy for £9.25 million, in a deal that (if approved by both companies’ boards, and subject to a revised supply agreement between Co-op and Shell) will combine Flow Energy’s 130,000 customers with Co-op’s 320,000, which includes 160,000 customers acquired following the collapse of GB Energy.

The future of Flow Energy had been a matter of some speculation, with a statement from the company highlighting strengthening “headwinds facing challenger suppliers”, citing the prospect of widespread price regulation, and the significant number of new entrants pursuing aggressive pricing strategies as presenting particular challenges.

“The response of the “big six” energy suppliers to Government policy developments is considered likely by the Company’s management to be, in many instances, to lower their standard variable tariffs. This would lead to an erosion of the differential between the prices challenger suppliers are able to offer and the tariffs being offered by the big six.

The Board believes this would be likely to have a significant adverse impact on consumers’ propensity to switch suppliers. In addition, the recent very cold weather, while beneficial to earnings given the Group’s hedging strategy, also increases the peak funding requirements of the business. This arises as the revenues from the additional energy consumption are recovered through the direct debit cycle over the next 12 to 18 months, while the supply costs of the additional energy consumed are paid for by Flow Energy in the short term,”

– Flow Group

…..while Iresa is banned from taking new customers

At the same time, another small supplier, Iresa, has been banned from taking on new customers for three months and may not increase direct debits or ask for one-off payments during the period, or until noticeable improvements are made in its customer service. If Iresa does not improve its customer service over the next three months it risks losing its licence.

The company is required to extend call centre opening hours and bring down the average call waiting time to below five minutes – the current time is estimated to be over half an hour. They are also required to call customers back by the end of the next working day if requested and to respond to all emails within five days (as well as clearing the backlog of emails that currently exists). Ofgem has also required Iresa to draw up a plan to identify and help vulnerable customers, including building a priority services register to allow such customers immediate access to help.

The company is also under investigation for other failings, with concerns over unexpected increases in direct debit demands, an inability for customers to log complaints, and the firm not having a system to identify and manage potentially vulnerable customers. Ofgem is examining whether Iresa gave sufficient notice to customers facing financial difficulty that debt repayments were being taken out of their accounts.

The company is also under investigation for other failings, with concerns over unexpected increases in direct debit demands, an inability for customers to log complaints, and the firm not having a system to identify and manage potentially vulnerable customers. Ofgem is examining whether Iresa gave sufficient notice to customers facing financial difficulty that debt repayments were being taken out of their accounts.

Doug Stewart, chief executive of Green Energy UK commented that energy companies should be stress-tested to ensure they are capable of operating in a challenging retail environment:

“Iresa is one of a number of small suppliers to succumb to an energy market which is not working. How many more energy companies have to go bust using Ofgem’s recently introduced ‘safety net’ before there is some sensible stress testing of energy suppliers? Ultimately it is the consumer that pays when an energy company goes bust, although the energy companies pay the upfront costs of creating a fund these costs eventually get passed onto the consumer. We need to be looking carefully at the cause of these failures, before we have another Carillion on our hands.”

He went on to add that while the Big 6 are under pressure to change their operating practices, they may end up being the only suppliers willing to take on the customers of failing challengers.

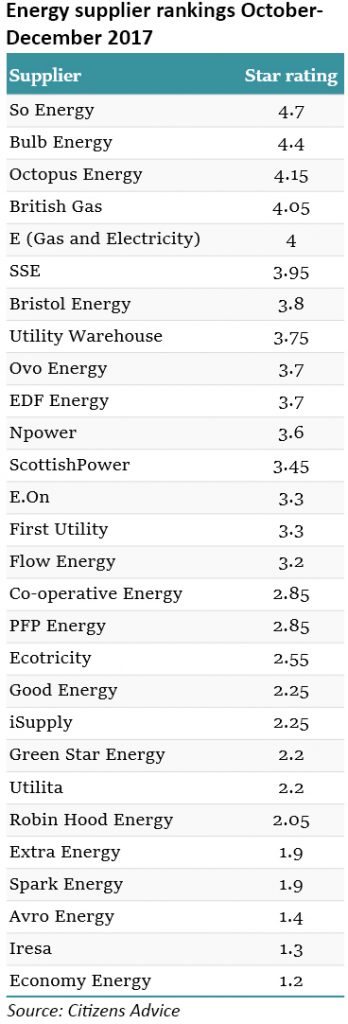

Stewart is not the only one to call for tougher regulation of new entrant suppliers. Citizens Advice also believes it is too easy for firms to set up and start serving customers before they have the systems and processes in place to deliver good customer service, with its latest quarterly ranking of energy suppliers showing a number of new and smaller suppliers at the bottom of the table.

Economy Energy is the worst performer with a score of just 1.2 stars out of a possible 5 for its customer service between October and December, with Iresa and Avro Energy also occupying the bottom positions. So Energy came top with a score of 4.7 stars, followed by Bulb Energy and Octopus Energy.

“The performance of some smaller energy suppliers raises serious questions for the companies themselves, and shows why Ofgem needs to get tougher on licensing…Ofgem also has an important duty in protecting customers from companies which don’t provide appropriate levels of customer service. The regulator must now take action and tighten the rules for new companies becoming suppliers,”

– Gillian Guy, chief executive of Citizens Advice

Ofgem has indicated that it is considering a review of its approach to awarding supply licences during 2018/19.

Is a state-owned supplier the answer?

During the last General Election, the Labour Party proposed re-nationalisation of the energy industry, while in Scotland, the devolved government is actively exploring the creation of a state-owned energy retail supplier to provide low-cost renewable energy to Scottish consumers.

A study by consulting firm EY outlining the strategic case for the new Scottish energy company highlighted a number of challenges: a state-owned energy company would not be eligible for subsidies under EU state aid rules and would therefore need to be commercially viable without such support in a market where pre-tax margins are limited. The study states that while other socially-minded suppliers exist, so far they are all loss-making, so it remains unclear whether such models are economically sustainable:

There are existing socially minded suppliers in the market who are focused on promoting their social values as a way of engendering trust amongst customers and encouraging them to switch their energy supply. These suppliers may typically owned by a local authority or housing provider. Examples of socially minded suppliers include Bristol Energy, Robin Hood Energy and Our Power. These suppliers aim to provide energy to customers at lower prices by;

- Not paying dividends to shareholders

- Finding more efficient ways to operate

- Generating their own power

- Reinvesting any profits to further benefit customers and their communities.

As many of the socially minded suppliers are relatively new to the market, it is not yet apparent how sustainable these lower prices are or to what extent these suppliers have been able to reduce costs. Each have reported losses, £7.7m in 2017 for Bristol Energy, £2.5m in 2016 for Robin Hood Energy, and £0.9m for Our Power in 2015.

On a more positive note, the report found that if a Scottish energy company was able to offer competitive pricing, it would be “well positioned” to develop a sufficient customer base – positive brand awareness as a public sector initiative could persuade disengaged customers to switch, and could encourage greater take up of energy efficiency measures by consumers.

The report outlines possible business models for a state-owned energy company, concluding that either a white-label arrangement with another supplier providing the main operational functions as well as being the source of the energy supplied, or a full-service licenced supply model (possibly under a “Licence Lite” arrangement) could be feasible.

In the first instance, the state energy company would lose some control over both operations and pricing, but would be a lower-cost prospect with lower operational risk, while under the second alternative, the company would have full control but would face significant set-up costs and operational risks.

Delivering either model without subsidy in a low-margin environment would be a significant challenge, however, the Scottish government is so far undeterred (possibly hoping that in a post-Brexit world, it would not be prevented from propping up a loss-making energy business).

The environment for energy retail continues to evolve, and further changes are likely. Recent experiences indicate the importance of sensible regulation, and while measures to increase competition are generally welcome, there should be processes in place to ensure new entrants have the basic operational capabilities to operate effectively in the market.

The proposed retail price cap is likely to further disrupt the market, and how well smaller suppliers will be able to compete in that context is unclear. It is unsurprising that at the opposite end of the market, the Big-6 is re-organising itself and consolidating certain operations. It may still be the case that scale is a key to long-term success in this market.

Leave A Comment