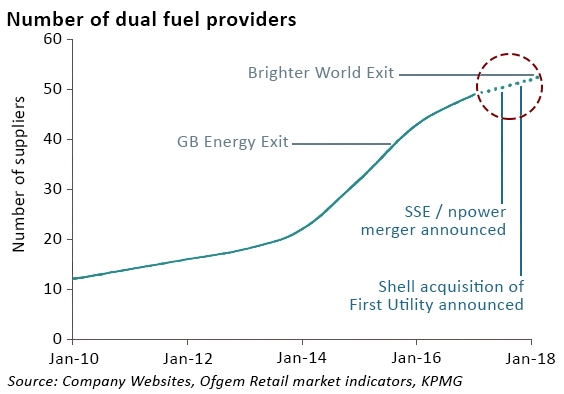

The collapse of GB Energy in November 2016 was seen by many as the start of a market correction, with other small independent suppliers being seen as vulnerable to rising prices and higher volatility. In the event, 2017 was quieter than expected – market prices and volatility both stabilised, and there were no further exits until the closure in December of Brighter World Energy.

Meanwhile independent suppliers continue to perform well in customer surveys. The annual market review by consumer group Which?, a survey of almost 9,000 customers, the highest-rated company was Utility Warehouse. Flow Energy, Octopus Energy and PFP Energy also scored well, while npower was at the bottom of the table, along with Spark Energy and Extra Energy. Spark Energy in particular saw a marked deterioration over the year, dropping from 12th place the year before. Of the Big Six, EDF Energy and EON were rated highest, with average scores, while Scottish Power and British Gas were in the bottom five with npower.

Brighter World claimed that it was not forced to close, but decided to cease trading because it felt the market has changed so dramatically in the last two years, it no longer had a sustainable business model. As a white label supplier, the company was unable to innovate on tariffs and struggled to differentiate itself in a highly competitive market. On closure, it passed its customers on to council-owned Robin Hood Energy whose tariffs it was re-selling.

Despite this, the GB market now has a record number of domestic retail suppliers, with the number of new entrants continuing to rise -independent suppliers now have approximately 18% market share, up from 5% in 2013. However not all new entrants are small start-ups – 2017 saw a number of large utilities and oil companies targeting the sector. Which begs the question: is size important for success in the retail energy market?

How vulnerable are small suppliers?

Speaking at the Energy UK conference in November 2016, Peter Atherton of Cornwall Energy, suggested the number of suppliers could fall from more than 50 to as few as 15 due to rising wholesale prices and other costs imposed upon energy suppliers.

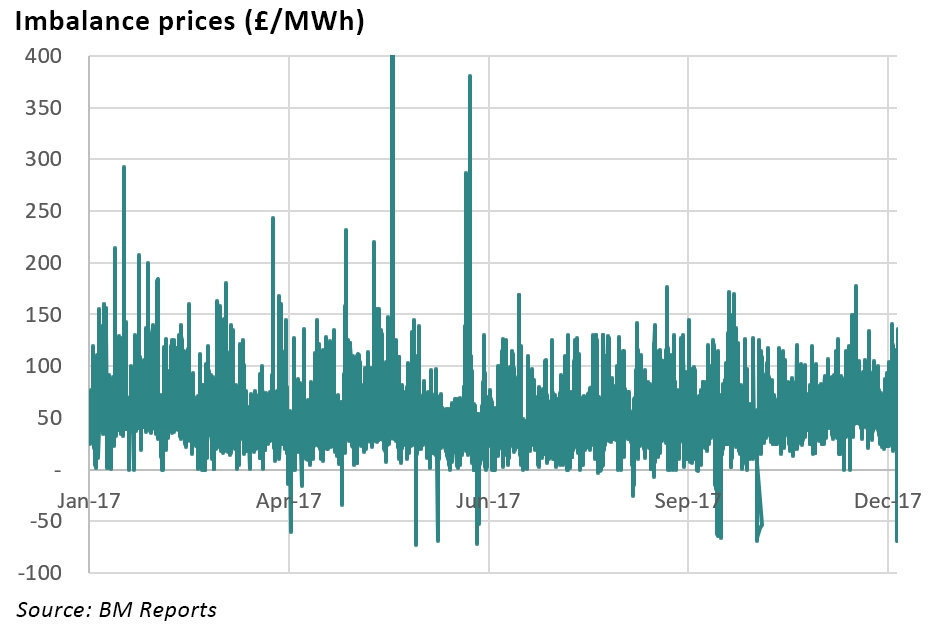

Despite regulatory interventions such as the Supplier Market Access rules, small suppliers still find it challenging to hedge their forward price exposures – their smaller size requirements make it difficult for them to accurately hedge their expected volume profiles, leaving them exposed to imbalance prices, which can be highly variable.

Doug Stewart, CEO of Green Energy, believes that smaller suppliers trying to compete aggressively on price are particularly vulnerable, and that “any of those at the top of the Uswitch table” of cheapest tariffs could be next to fail. He went on to suggest that a lot of new companies are also caught out by the extensive non-commodity costs they face:

“The wholesale market has been really quiet for the last six years yet prices have continued to rise, while profits have continued to go down. This is because there are a lot of policy costs that are being passed onto the industry and, ultimately, passed onto customers.”

The signals from the market relating to smaller suppliers are mixed. Independent suppliers are taking market share from the Big 6, but there are some indications of stress.

Signs of possible trouble ahead came in December when Toto Energy increased two of its tariffs by 22% and imposed a 50% seasonal direct debit charge where customers would pay 50% more in winter and less in summer. Confusingly, the company partially retreated from its price rises due to a marketing error. Utility Week drew a parallel between this price increase and the 30% rise announced by GB Energy shortly before its collapse. Good Energy also increased prices late last year, albeit at the more modest rate of 7%.

Meanwhile, Flow Energy and Spark Energy both failed to make scheduled payments into Ofgem’s fund for vulnerable customers, which may indicate cash-flow weakness. Flow Energy’s Chief Executive resigned in November following heavy customer losses, and the company’s share price has dropped to 0.5p from 22p two years ago.

Spark Energy claims to be profitable, however its most recent publicly available accounts are for the year to June 2016, so it’s unclear how well it is weathering the competitive environment.

Despite these concerns, Ofgem has not asked either company to stop taking on new customers despite failing to meet these payments.

Larger companies muscling in on the market

Engie launches home energy business

In May, French gas utility Engie announced its entry into the domestic energy market, building on its long track record supplying UK businesses. The company announced a number of innovations, including a commitment to rolling customers onto the cheapest available tariff at the end of their fixed term plan, a new tracker product, and an intention to focus on connected home initiatives. The tracker tariff is designed to keep rates aligned with wholesale prices, is being explicitly marketed as analogous to tracker mortgages.

“We think there is some space for a new player who can come up with a new model,”

– Wilfrid Petrie, chief executive of Engie UK

At the time, Engie claimed to be the largest company to enter the UK domestic energy market for over 15 years – a distinction which turned out to be short-lived.

Vattenfall buys into the market

In June, State-owned Swedish utility, Vattenfall acquired Bournemouth-based supply company iSupplyEnergy and its 120,000 customers. Vattenfall is the largest utility in the Nordic region, and has invested over £3 billion in its UK wind energy businesses since 2008. It has recently branched out into solar PV, battery storage and business to business sales.

In November, Vattenfall was granted a distribution licence, giving it the right to own and operate local electricity distribution assets anywhere in Great Britain.

Oil giant shell buys the largest independent supplier

In December, Shell overturned Engie’s status as largest new entrant, by announcing its intention to acquire First Utility, the largest of the independent suppliers with 825,000 customers. The two companies had a pre-existing partnership, where Shell supplied gas and electricity to First Utility while First Utility sold to domestic consumers in Germany under the Shell brand. The acquisition, which will be subject to regulatory approvals, is expected to close early this year.

Shell intends to double its new energy investments to US$2 billion next year:

“The biggest growth in the energy market in the coming decade will be in electricity. It’s a growing market and one that is changing quite a lot. Consumers have a lot more control over their energy in the home through digital devices and the growth of electric vehicles will bring a lot more new opportunities. It’s an exciting growth market that is undoubtedly very competitive,”

– Mark Gainsborough, vice president of new energies, Shell

The announcement in November of the proposed merger of the retail businesses of SSE and npower supports this trend for scale. Small independent suppliers have succeeded in taking market share from the Big 6, but wholesale prices have been relatively calm over the past year. This is unlikely to continue – the growing penetration of intermittent generation is likely to make prices, particularly imbalance prices, more volatile, and the non-commodity burdens on suppliers continue to grow.

Any significant period of market turbulence would put pressure on the smaller independents. Add in the prospect of price caps and it’s easy to see why some see scale as necessary to survival.

Leave A Comment