The Big 6 energy suppliers have all raised the prices of their standard variable tariffs recently. E.On kicked off with a 2.7% increase, followed by EDF Energy with 1.4%, npower with 5.3%, Scottish Power and British Gas both with 5.5%, and SSE with 6.7%. They all blamed rising wholesale prices and policy costs.

“The costs all large and medium energy suppliers are facing – particularly wholesale and policy costs which are largely outside our control – have unfortunately been on the rise for some time and we need to reflect these in our prices,”

– Simon Stacey, Managing director of domestic markets at npower

In the face of price increases by large suppliers, consumer switching continues to increase with a 4% increase between March and April, in line with last year’s record number of 5.5 million electricity customers (one in six).

The figures published by Energy UK which published these figures show small and mid-tier suppliers benefiting at the expense of the larger companies:

- 34% were from larger to small and mid-tier suppliers

- 11% were from small and mid-tier to larger suppliers

- 31% were between larger suppliers

- 23% were between small and mid-tier suppliers

Smaller suppliers facing challenges despite switching successes…

Despite their success in growing market share, smaller suppliers still face a number of challenges. Several have failed in recent months, and there are calls for tighter regulation to ensure new entrants have the necessary infrastructure to cope with the customers they acquire. This week Ofgem announced that minnow Iresa had failed to meet customer service improvement targets and may face an indefinite ban on taking on new customers, increasing direct debits or asking for one-off payments until these targets are met.

Iresa now has until 27 June to make its representations in response to Ofgem’s initial findings, after which the regulator will decide whether to take further action, which could result in the company losing its supplier licence.

Ofgem is also investigating whether energy suppliers Economy Energy and E (Gas and Electricity) and consultancy Dyball Associates – have broken competition law, and has issued a “statement of objections” in which it alleges that between January and September 2016, the companies had an agreement that prevented the two suppliers actively targeting each other’s customers through face-to-face sales.

The companies shared details about their current customers, while Dyball facilitated the arrangement by designing, implementing and maintaining software systems that allowed customer lists to be shared, and recruitment of each other’s customers to be blocked.

Ofgem said its provisional view was that these arrangements prevented, restricted and distorted competition amongst energy suppliers, and would now consider any representations from the companies before deciding whether competition law has in fact been broken.

Mid-sized supplier Utility Warehouse is also being investigated by Ofgem to see whether the company has breached rules in the way it manages customers who are in debt, and in particular whether it has appropriate repayment options for indebted customers in place. It also includes whether they are installing pre-payment meters appropriately as a means of recovering debt from customers, particularly when they install them under warrant.

…while defensive consolidation among the Big 6 faces regulatory scrutiny

Last month the Competition and Markets Authority (“CMA”) opened a full-scale investigation into the proposed npower-SSE merger after previously suggesting the tie-up could lead to higher consumer energy bills.

SSE is the second largest of the big six by customer numbers, and npower is the smallest – together they would have 11.5m customers in the UK, and be almost as large as British Gas, the market leader.

The merger of the companies was announced last year, in the face of increasingly stiff competition from new challengers – there are now about 60 energy suppliers in the UK, with just over 20% market share. This is a key motivator of the proposed merger, and also one of the reasons the companies do not believe their deal threatens competition:

“There are now 60, not six, suppliers in a market in which competition is stronger than ever….this is not a case of six into five; it’s more like 60 into 59. And, as a result of this merger, one of those 59 will offer a completely new model that combines the resources of established players with the agility and innovation of an independent supplier,”

– Alistair Phillips-Davies, CEO, SSE

The deal is also complicated by a proposed asset swap between E.On and RWE, owner of npower’s parent company Innogy, under which E.On would acquire a third of the merged SSE-npower entity. The Telegraph reported that Innogy is expecting the CMA to require it to divest its stake and before the Eon-RWE deal completes. It could also waive its rights to take up two seats on the board of the merged company.

The blame game

The Big 6 companies are not the only suppliers raising their prices. In March, Opus Energy wrote to its customers with news of a 7.5% price rise, which it blamed on non-energy costs including network and policy costs:

The Big 6 companies are not the only suppliers raising their prices. In March, Opus Energy wrote to its customers with news of a 7.5% price rise, which it blamed on non-energy costs including network and policy costs:

“Non-energy costs cover the cost of transporting your energy to you and provide support for Government initiatives and interventions in the energy industry, such as climate change policies”

Igloo Energy increased prices by 3.2% in April, however it blamed increases in wholesale prices, while Bulb Energy raised priced by 2.8%. First Utility, PFP Energy and ENGIE have also raised prices since the beginning of the year.

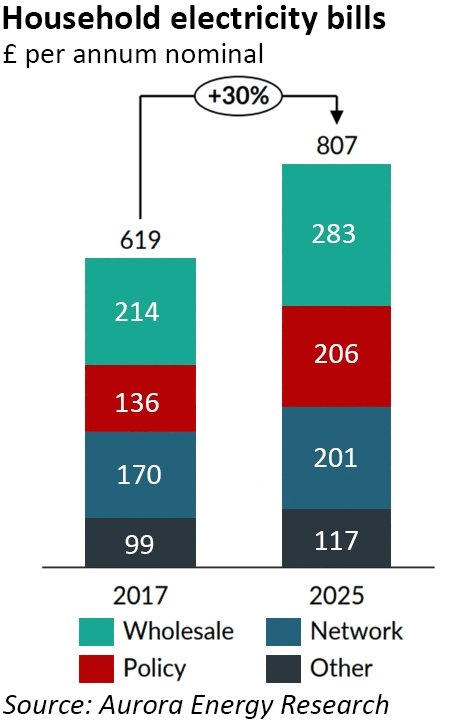

Aurora Energy Research expects household electricity prices to rise by almost third by 2025, driven by policy costs which are the fastest-growing component of bills.

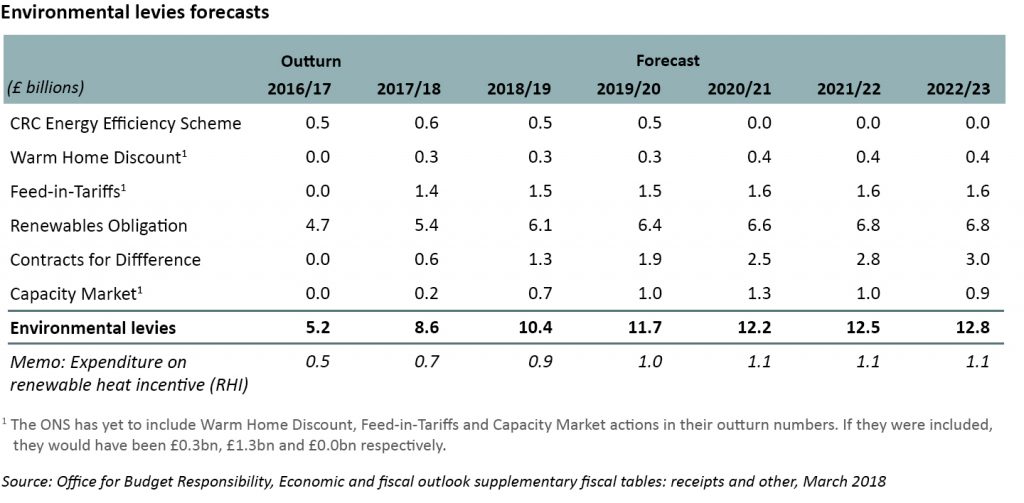

The Office for Budget Responsibility calculates that environmental levies will more than double between 2016/17 and 2022/23, increasing from £5.2 billion to £12.8 billion. This does not include the £11 billion cost of the smart meter programme.

The Government on the other hand highlights the reduction in demand resulting from energy efficiency schemes:

“The Government has put in place policies that have reduced energy bills for households, which have more than offset supporting our move to a low-carbon economy. We are driving £6 billion into making homes more energy efficient over the next ten years,”

– BEIS

The Government places the blame for price rises on supplier greed, saying in relation to the increase by British Gas:

“We are disappointed by British Gas’s announcement of an unjustified price rise in its default tariff when customers are already paying more than they need to. This is why Government is introducing a new price cap by this winter to guarantee that consumers are protected from poor value tariffs and further bring down the £1.4 billion a year consumers have been overpaying the Big 6. Switching suppliers will always help consumers get the best deal, saving £308 by switching from a default tariff offered by the Big 6,”

– Claire Perry, minister for energy and clean growth

I have illustrated previously that the £1.4 billion of excess profits identified by the Competition and Markets Authority is inconsistent with the companies’ Consolidated Segmental Statements, and the only way in which the claim could be true would be if vertically integrated operators were recording profits in non-domestic segments including generation that were in fact earned from domestic end users (or the figures are completely wrong/distorted in other ways). Given the Consolidated Segmental Statements are prepared by the companies and audited by their auditors based on guidelines prepared by Ofgem, if they are inaccurate to such a degree, there are wider regulatory and supervisory failures taking place.

However, in light of the growing impact of policy costs on bills, Aurora Energy Research has warned that Ofgem will have “little choice” but to repeatedly raise price caps in future, undermining their effectiveness in the public eye.

Time for a change

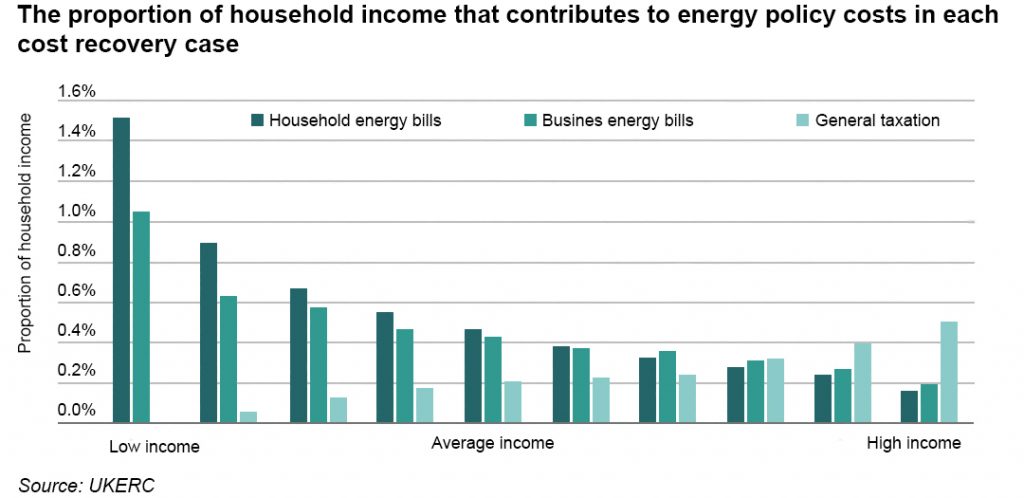

In March, the UK Energy Research Council (“UKERC”) called on the Government to recover policy costs through general taxation rather than household bills, on the basis that energy bills represent a much higher proportion of household income for low-income households – the poorest 10% of households spend 10% of their income on energy bills while for the richest 10% the figure is only 3%.

The report accepts that some policies funded though bills have helped reduce costs for consumers by lowering demand through increased energy efficiency, but points out that more than three-quarters of policy costs relate to low-carbon subsidies (the Renewables Obligation, Contracts for Difference and Feed-in Tariff schemes)

According to the UKERC, funding energy policies through general taxation would reduce costs for 70% of households – the poorest would pay nothing, saving them £102 a year, while the richest would pay an additional £410.

“Our work shows that once you consider the hidden energy in the manufacture of all the goods and services we buy, it is only fair that richer homes contribute more to energy policy costs. Low income households, who experience fuel poverty, could be exempt from these additional charges if we rethink how low carbon energy schemes are funded,”

– Anne Owen, UKERC researcher

The Government should take note of this research – recovering energy policy costs through general taxation would not only be fairer for consumers, it would also remove a big driver of energy price rises. The Government should also explore ways in which wholesale prices can become more cost-reflective, so that flexibility is valued more appropriately.

By doing so, bills would be better aligned with actual controllable costs, and energy suppliers would not find themselves trying to differentiate on prices that are largely out of their control. Capping retail energy prices is not the answer.

Thanks a lot for the post. I’ve really enjoyed reading the blog over the last year or so. I agree that recovering policy costs through general taxation may be fairer and more progressive. However, I think there is a good case to be made for them staying in energy bills – it keeps public scrutiny on the costs of decarbonisation and incentivises govt. to keep policy costs down.

Regarding cost reflectivity I think a move towards higher fixed costs in bills may be beneficial. With kWh prices reflecting average cost more than marginal cost there is an incentive to free ride on the fixed costs of providing energy, such as network and policy costs, by generating yourself and reducing your net usage. Admittedly one way of achieving this would be to recover fixed costs through general taxation, and have lower kWh rates. I do wonder whether there would be a rebound effect however – would the lower marginal rate and lower energy bills lead to inefficiently higher energy demand?

Hi Adam,

I agree it’s not clear cut – there is merit in the polluter pays argument, but the public scrutiny you mention doesn’t seem to be working: as long as the Government and energy companies blame each other, consumers will be confused and low trust in the sector will persist.

The network costs question is trickier, since a portion of these are indirect policy costs eg higher balancing costs due to renewables. I prefer the solution proposed by Dieter Helm – to make all energy firm so the generators that cause intermittency have to pay the associated costs to the network.

However, when I mention cost reflectivity, this needs to complete – self-generators that are connected to the grid need to still pay their share of network costs, since the option value of drawing from the grid when not generating still needs to be paid for. Otherwise, as you say, you get the free-rider problem.

I’m generally in favour of the Helm proposals however I can see a few risks with their implementation – for example I may have missed it but it doesn’t appear that EFP really does make intermittent generators pay for their costs to the network; they just get a lower EFP/capacity payment.

I also have some serious misgivings about EFP calculations themselves and I would like your opinion on them. One of the examples explained that a plant that is at any time randomly on or off 50% of the time is allocated a firm capacity factor of almost exactly 50%. This just doesn’t seem right. It doesn’t take into account the fact that this binary plant is not 50% firm – it is not the same as a generator that is for sure at half capacity (or say has a very tight dist. around 50%) for example. By replacing a 50% sure generator with a binary plant you are introducing uncertainty, changing the shape of the margin duration, and therefore increasing your LOLE.

Say a more uncertain generator is a mean preserving spread of a more certain one then I would have thought they shouldn’t be valued the same, but they appear to be under EFP. The way the generation uncertainty manifests itself and consequently the shape of your margin duration curve matters for security and also has consequences for wholesale prices.

If there are problems with that toy example then I’d have thought there must be some with the real life EFP for wind, solar, and interconnectors etc.

The best way I can think of working out an EFP at the moment is if you do not want to decrease security of supply from today then the de-rating factor should be calculated by swapping out a standard reliability generator (with average qualities) and replacing it with the generator you’re trying to de-rate. Increase the capacity of that type until you arrive at the same LOLE – and that would give you your LOLE preserving de-rating factor. Given your background in finance I was wondering whether you knew of any finance concepts which could be lent to this ?

Another potential problem I see with the Helm proposals is the application of a carbon tax sufficient to meet carbon targets. Aside from how high the tax would have to go and whether marginal cost wholesale pricing (and so the carbon tax) would really work in a low marginal cost generation world, there is the potential for interconnectors to not be charged their proper amount, either not at all, as they are at the moment, or the average carbon intensity of the exporting country – in which case we offshore our emissions at the expense of domestic generation.

I’m inclined to agree with your comments about EFP – my support of the Helm proposals was in terms of the concept of placing the cost of intermittency with the creators of intermittency (an analogy to “polluter pays”). There were other of his ideas/analyses that I disagreed with, and I haven’t thought through whether his specific methodology propsals would work (eg he disappointingly failed to challenge the CMA’s assertion that the Big 6 suppliers are earning £1.4 bn of excess profits).

As far as a finance analogy goes, it’s an interesting question. It could be compared with an asset portfolio, with capacity instead of return and risk of not delivering capacity/returns. In the investment case, the objective is to construct portoflios that lie on the efficient frontier, which we could take to be the lowest risk for a given level of return. For security of supply, you need to set the required capacity and acceptable level of risk associated with the portfolio that would make up that capacity, so it’s not quite the same. There are also various exotic derivatives that pay out based on the best/worst/2nd best etc performer in an asset portfolio, so there could be something there that would translate (my background was in risk management/hedging and finance so investment strategies aren’t my forte!)

I’m against the carbon tax for a number of reasons. Setting aside my issues with the man-made-CO2-causes-climate-change hypothesis, a unilateral carbon tax makes UK electricity comparatively more expensive than on the Continent, which impacts the way interconnectors are used, and also has implications for industrial competitiveness. Even if you accept the climate arguments and see a need to curb CO2 use, I agree that the tax creates probems with exporting emissions/leakage. I don’t think the low marginal cost scenario is probematic in this respect though since the carbon tax is a fixed and not relative amount. It would be feasible (if perhaps optically difficult) for a high carbon tax to sit on top of even zero wholesale prices (and I guess negative ones too).

Yes, I have also seen the excess profits number repeated unchallenged elsewhere by other economists. I don’t know exactly how it was arrived at so can’t really comment on the number itself. Although I see from your previous blogs that it’s more than the big 6 earned in profits. I would imagine him quoting it came from respect for the CMA.

Thanks for your suggestions on finance analogies. I will bare them in mind.

I think there’s also a more subtle argument regarding economy-wide carbon taxes. Often it includes the proposition that exports would be exempt the tax to prevent an unfair disadvantage on the world market, and imports would be charged a carbon tax based on the carbon intensity of the good being imported. Assuming this is possible to do both accurately and without too much administrative burden, it creates the incentive for firms to focus more on export markets than previously as margins will likely be larger in the absence of the carbon tax – in domestic markets not all of the cost increase will be passed on to consumers and suppliers will absorb some of the tax meaning tighter margins.

There is also an energy return on energy invested (EROI) point of view to a carbon tax as it increases the effective EROI of an economy. The following paper (https://www.sciencedirect.com/science/article/pii/S0301421515300392) approaches it from a ‘peak oil’ perspective but the conclusions are similar – a move to lower EROI technologies leads to lower levels of consumption as more of the economy’s resources are used to generate the energy to power the economy – the economy is deprived of its former energy ‘subsidy’. How much depends on how easy it is to substitute energy for capital as energy gets more ‘expensive’.