On 25 July, Ofgem launched a consultation as part of its review of the Secure & Promote licence condition. Secure and Promote was introduced in 2013 to improve liquidity and market access for small and new entrant electricity suppliers.

Small suppliers face a number of challenges in their electricity procurement – typically they do not have their own sources of generation and therefore rely on the wholesale markets for both procurement and hedging of their electricity needs. Small companies with limited trading history face challenges in securing suitable credit lines for trading, with onerous collateral obligations putting pressure on working capital. The smaller volumes required and more granular shape, can also be challenging for small suppliers as they may require volumes that are below standard clip sizes.

Over-the-counter electricity trading is generally carried out under the terms of an applicable Master Agreement such as an EFET, or a Grid Trade Master Agreement. These can be time consuming to negotiate and must be entered into on a counterparty by counterparty basis. Small suppliers were finding it challenging to negotiate such agreements with larger market participants, for whom such small business was generally a low priority.

Various studies suggested that these challenges were crating barriers to entry for new suppliers, prompting Ofgem to introduce Secure and Promote in order to widen market access for smaller suppliers and new market entrants.

Liquidity has improved but is concentrated in the market-making windows

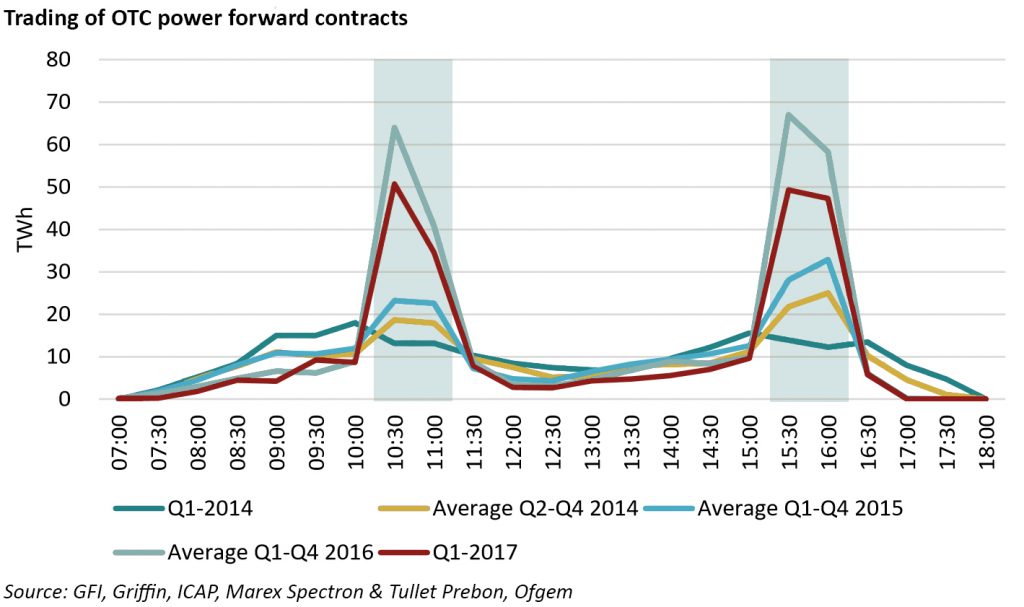

The Secure and Promote obligations require large the five largest integrated utilities to make a market (ie offer to buy and sell) a range of electricity products over different tenors, with subject to certain constraints on the maximum permitted bid-offer spread, as noted above. The market-making requirement applies during two “windows”: 10:30-11:30 am and 3:30-4:30pm.

Ofgem’s analysis shows an increase in the volumes traded in during the market-making periods, as seen in the chart below.

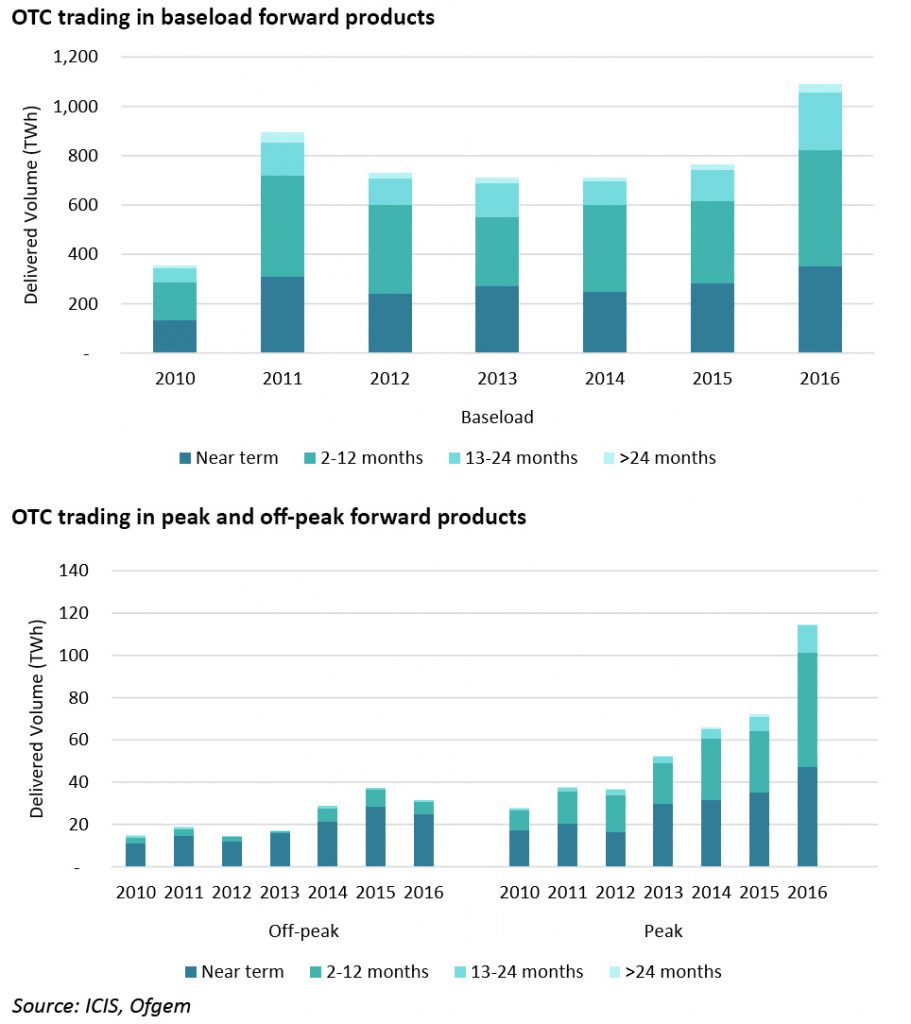

Overall, since the introduction of Secure and Promote in 2013 there have generally been slight increases in the volumes of all contracts traded. The less liquid peakload products showed 206% increase in the volume of longer-date products traded, compared with a 71% increase in comparable baseload products. Offpeak products continue to be traded mainly in shorter tenors.

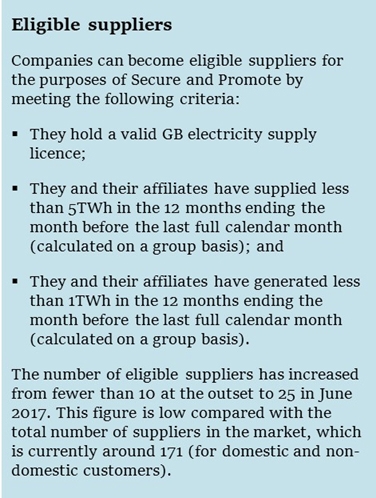

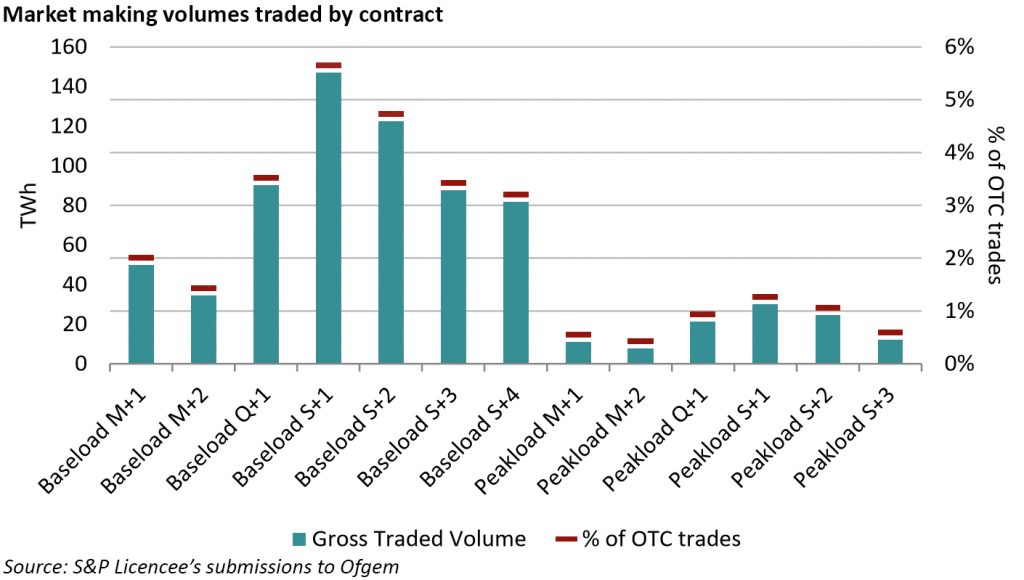

Liquidity in the market-making windows is concentrated in baseload products, and still represents a relatively small fraction of the overall volumes traded, in part because only eligible suppliers may participate, and there are relatively few of these (see box).

There has been no discernible impact on short-dated trading executed either OTC or on-exchange.

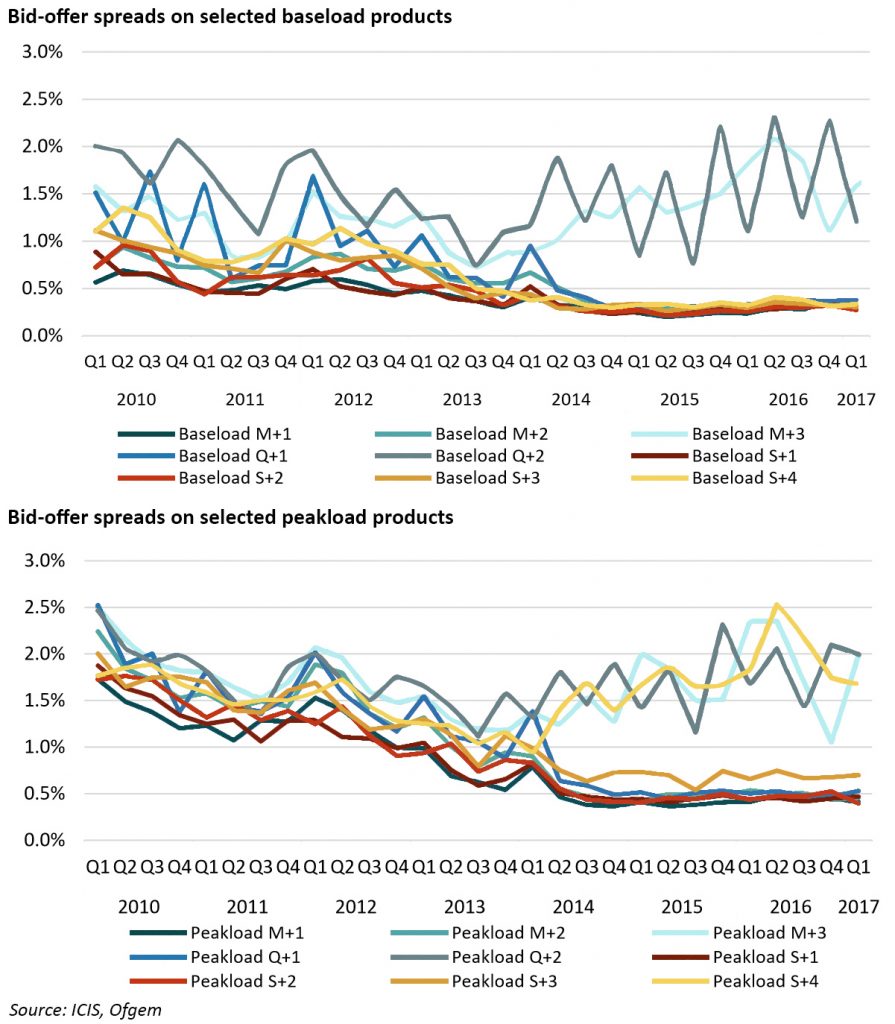

Bid-offer spreads have narrowed during the period, which is generally an indicator of improved liquidity, although part of this trend is as a direct result of the MMO which sets a mandatory 0.5% spread on certain products.

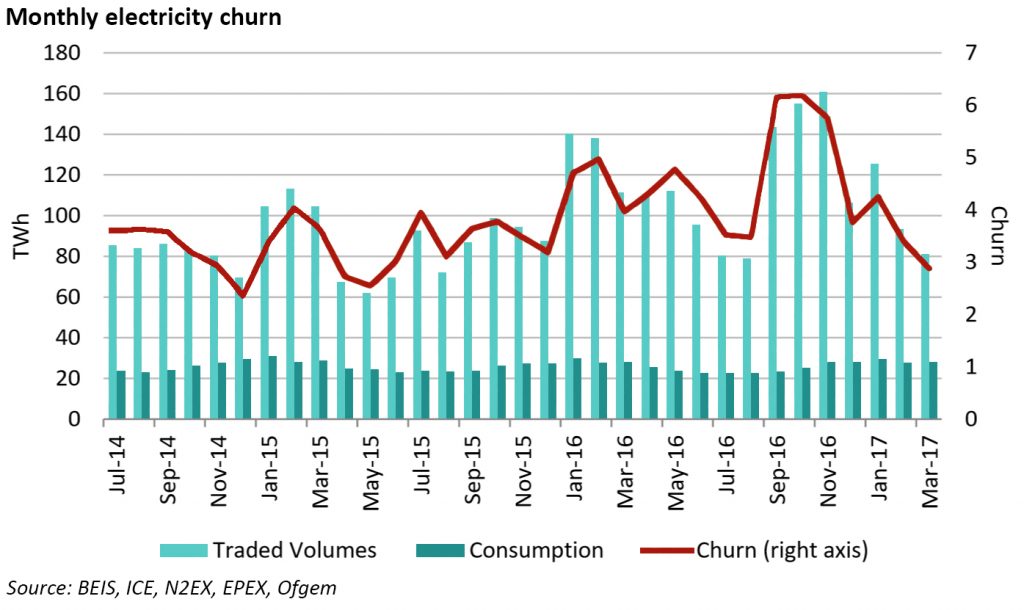

Another measure of liquidity is churn – the number of times a unit of the underlying product is traded prior to delivery. There has been a slight increase in churn since the introduction of Secure and Promote, but it has also become more volatile. The electricity market is still significantly less liquid than the gas market, where churn regularly exceeds 20 times.

Secure and Promote rules allow the large utilities to withdraw from making a market if they develop a net position of 30 MW or more on a product in the window. This volume limit is being met more often, increasing from 32 times in Q2 2014 to 515 times in Q4 2016. A similar cap applies to price changes of ±4%, which has also increased in frequency from 28 times in 2015 to 117 times in 2016.

Supplier market access rules indicate some increased market access for small suppliers

The Supplier Market Access (SMA) obligation is designed to ensure negotiation of master agreements for small suppliers is not treated as a low priority by larger market participants, and that credit and collateral requirements are fair and transparent. The rules set out detailed obligations for the negotiation process, particularly around response times, and set out rules for credit and collateral, clip sizes, product type, and pricing transparency.

Data reported under the SMA condition show variable trading volumes with eligible suppliers with the total number of trades per month continuing to be quite low at 20-40 trades per month, except in Q4 2016 where there was a significant jump in trades reflecting volatile market conditions at the time.

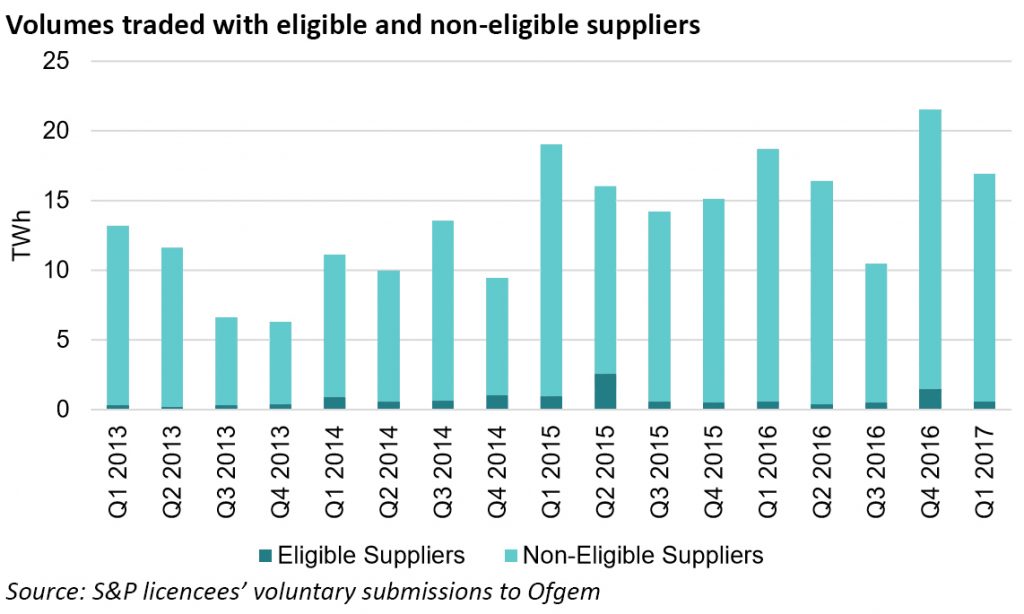

The voluntary submissions to Ofgem provide some insights into the trading of the large utilities with suppliers that are not eligible under Secure and Promote. These show a slight growth in volumes traded with both eligible and non-eligible suppliers, with increased trading in SMA products, although the amount of trades in non-SMA products has fallen slightly. Ofgem notes in its consultation document that the variability in volumes reflects some seasonality and the lumpier demand of smaller suppliers.

As the data are provided on a voluntary basis they may not give the whole picture, however the suggestion is that Secure and Promote has resulted in improved market access for small suppliers in general, and the benefits are not restricted to eligible suppliers.

“The increasing trend in both the volume of trade with small suppliers, and in SMA products traded with both eligible and non-eligible suppliers since Secure and Promote was introduced suggests that small suppliers have had greater access to the wholesale market. This may be due to greater price transparency for these products in the market, or due to improved trading relationships with the large generators,”

– Ofgem.

Large utilities oppose Secure & Promote….

The perceived success of Secure & Promote depends on who is asked. The large utilities bound by the market making obligation are generally negative about the requirement, arguing improvements in liquidity are marginal and that liquidity outside the windows has dried up, indicating a broader unwillingness of traders to make markets “naturally”, and a reluctance of new traders to enter the market. The reduction in liquidity outside the windows has been identified as a potential dis-incentive for financial institutions from participating in the electricity market – since 2015 a number of large investment banks including Barclays Capital, Deutsche Bank and Merrill Lynch have all closed their energy trading businesses.

According to Ofgem, the large utilities also complain that the costs of complying with the Secure & Promote provisions, estimated by RWE at £3-4 million per party, are not justified by the level of participation by eligible suppliers. They also raised concerns that the price and volume caps were set too wide and too inflexibly to effectively limit their costs and risks, particularly during periods of market higher volatility, although by the same token, small suppliers would find it very difficult to manage their risks in such markets in the absence of the market-making conditions.

…but is it working for the intended beneficiaries?

Small suppliers generally believe that Secure and Promote has helped them access products more easily, both inside and outside the market-making requirements, providing associated benefits to suppliers not on the eligible suppliers list, although they would like to see it go further, with greater liquidity in forward “block” products that are more granular than peak and baseload products. Some suppliers continue to see credit and collateral arrangements as a barrier to trading.

Inability to trade forwards efficiently exposes small suppliers to both price and volume risks. Relying on short-term trading means a supplier’s costs can be volatile, a problem which is compounded if the supplier cannot trade the volumes and shape it needs and is forced to make up its shortfalls in the cashout process where prices can be even more volatile.

These risks are highlighted in analysis produced by Cornwall Insights following the bankruptcy of GB Energy in 2016, which was partly down to failures in its hedging programme:

“The best proxy hedge against volume risk on a domestic profile a supplier can manage is with “secure and promote” (S&P) products (baseload and peak), which were specifically introduced by Ofgem in 2014 to provide liquidity to new entrant suppliers often buying in small quantities. But it cannot protect against price risk over block five and six as there is very little liquidity in these products. These periods are also when within day and imbalance prices have been increasing significantly.

Structurally we should ask whether the S&P is working as it was designed to. Ofgem needs to ask if small suppliers can access short-term hedging products (a structural problem) or can they not afford to pay the prices that these products are quoted at (a commercial problem)? In addition we should be asking if the changes under P305, which has sharpened energy imbalance prices, have been exacerbating these effects on smaller suppliers. These events also raise important questions about the move to PAR 1, which will further sharpen imbalance process, in November 2018.”

It is unsurprising that the large utilities would want to push back against Secure and Promote….compliance is expensive, and ultimately it is a mechanism for increasing retail competition, which directly challenges their own retail market shares. The question is whether these concerns are outweighed by the benefits to smaller suppliers.

From the data presented by Ofgem in its consultation paper, it would seem that so far Secure and Promote has been positive for small suppliers, providing them with improved market access, and some increases in liquidity. However, the efficiency of the scheme is less clear, as it may well be that the products offered are failing to meet small suppliers’ shape needs. The question of reach is also a valid one, with only a small proportion of all GB domestic electricity suppliers having been granted eligible status – it is unclear whether those that do not have failed to meet the criteria, or have simple decided not to apply.

A wider question is whether Secure and Promote has acted as a barrier to entry for market counterparties. Although a number of banks have exited the market in the last couple of years, these steps have been part of a wider withdrawal from energy trading (including gas and Continental European power trading, some of which is significantly more liquid than the GB electricity market), and are unlikely to have been prompted by Secure and Promote in any form. There are legitimate questions about whether the degree of vertical integration in the market is still a barrier to liquidity, evidenced by low traded volumes, and particularly low levels of churn, and whether this makes the market unattractive for traders who are seen in other markets such as the NBP gas market,

The number of new entrant suppliers joining the market is growing, suggesting the barriers to entry are falling, although only a small proportion of these currently benefit directly from Secure and Promote. However, with the exception of a period of volatility in late 2016, the markets have been fairly benign…the real test would be a sustained period of volatility so see how robust the trading and risk management arrangements of small suppliers really are.

Leave A Comment