Following on from my recent post about the challenges of upgrading power grids to meet net zero ambitions, in this post I will set out the issues relating to the supply of critical minerals for the energy transition. This issue is creeping up the industry’s agenda. Supply chain cost increases in the aftermath of the Russian invasion of Ukraine made many wind projects uneconomic, and led people to look more closely at how supply chain constraints might impact the transition and the ability to meet policy objectives. (Note: on these posts the notation “MT” refers to metric tonnes.)

Availability of critical minerals will be a major limiting factor in the energy transition

While the recent report from the International Energy Agency, Electricity Grids and Secure Energy Transitions makes some sensible recommendations for optimising current resources, such as standardisation, some fall in the “easier said than done” category such as diversification of supply chains. Of course, this is desirable, but the natural distribution of mineral resources is often far from diverse. The IEA also recommends encouraging “sustainable” supply chains which carries risks and is likely to make supplies more expensive (and in some cases is impossible as I set out in a recent blog on scope 3 emissions).

“Should electricity grid development fail to accelerate in line with the APS [Announced Pledges Scenario] – with more limited investment, modernisation, digitalisation, and operational changes than envisioned – there would be a significant risk of stalled clean energy transitions around the world,”

– IEA, Electricity Grids and Secure Energy Transition

The technologies underpinning the energy transition rely heavily on critical minerals. According to the IEA, an offshore wind turbine depends on nine times more minerals than a comparable gas-fired power plant, and an EV uses six times more critical minerals than an ICE vehicle. It’s not just power grids that require large amounts of copper – wind, solar hydro and geothermal generation all rely on copper as well as nickel, silver and rare earths. Nuclear power plants depend on uranium for fuel (which I will discuss in a forthcoming post), while nickel alloys are a key component in their cooling systems as well as being used inside the pressure vessel. EVs rely on a range of critical minerals for battery components, and also require rare earths for motor design and copper for wiring.

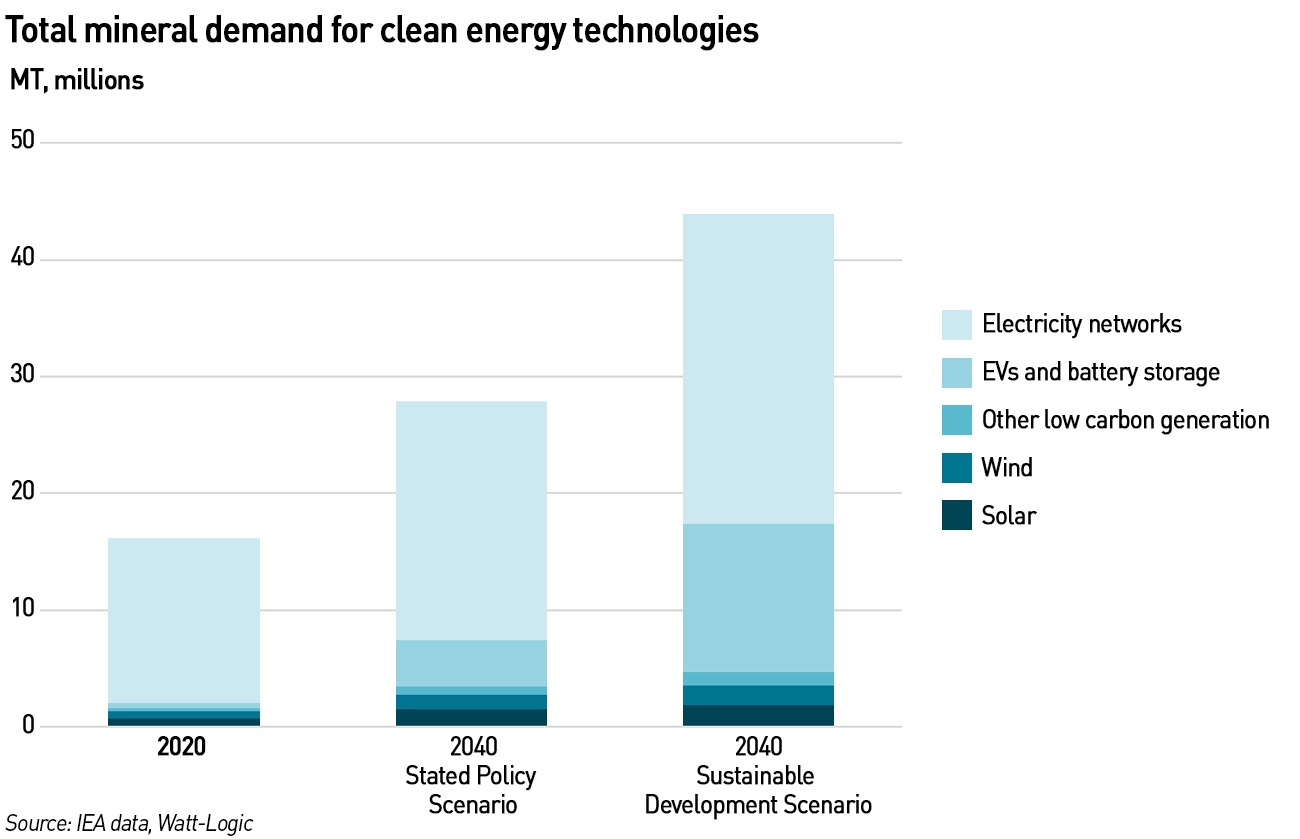

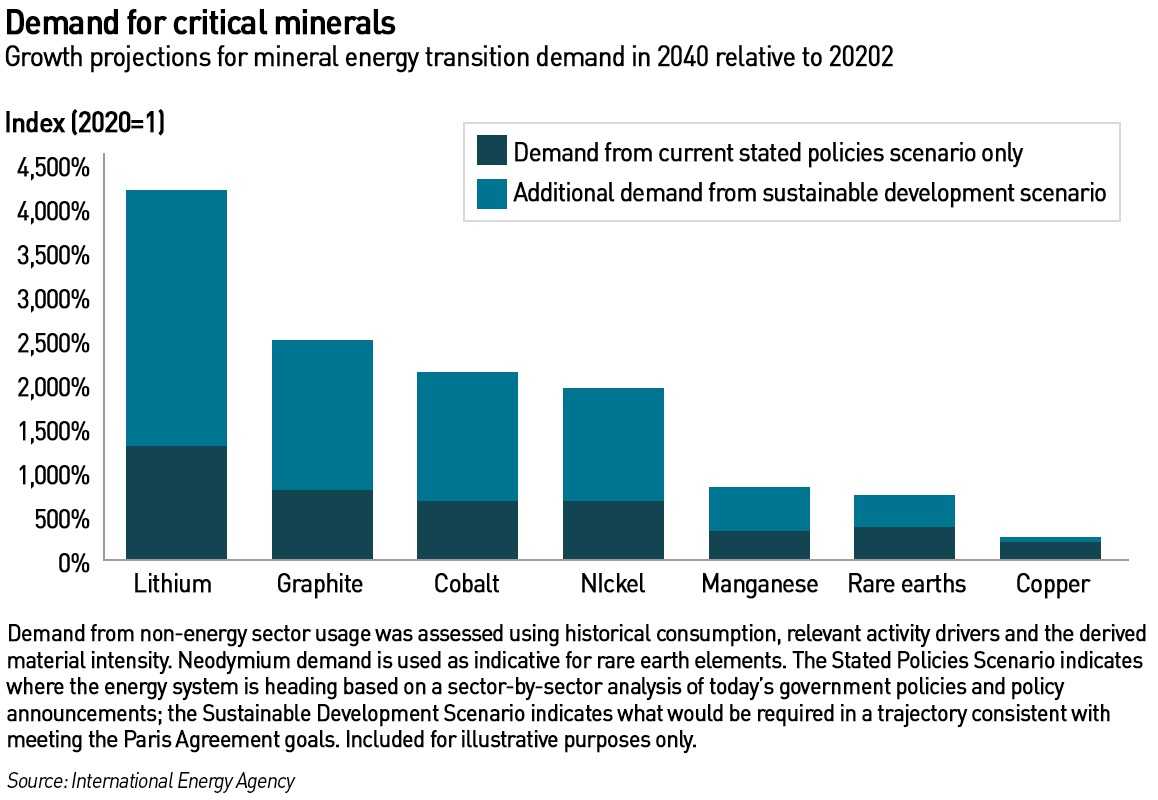

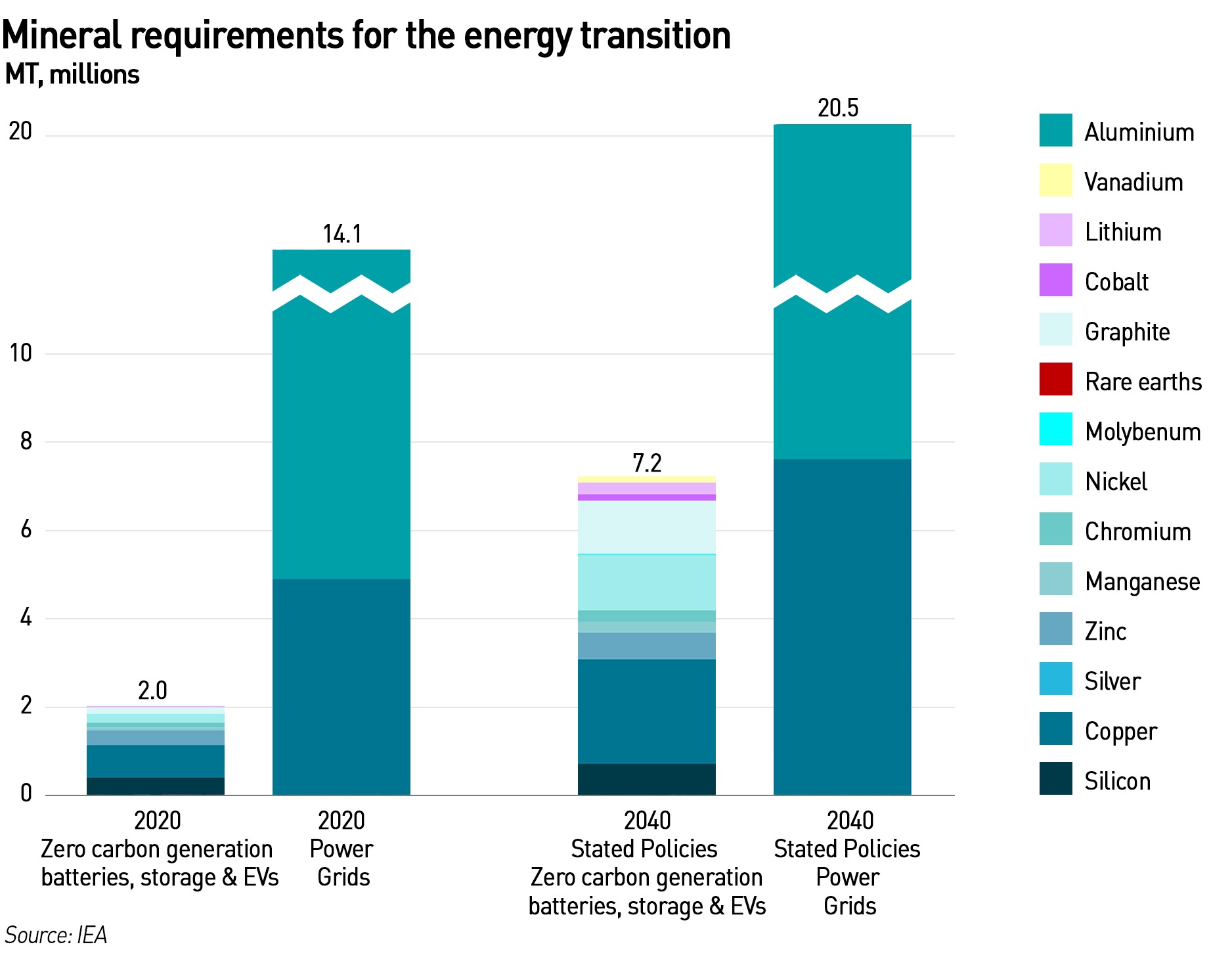

Far and away the largest source of new mineral demand will come from grid infrastructure, such as power lines and transformers. Taken together, the need for critical minerals will double between 2020 and 2040 based on the stated policies of governments, and quadruple in the IEA’s Sustainable Development Scenario. In both scenarios, EVs and battery storage account for about half of the mineral demand growth from clean energy technologies over the next two decades – mineral demand from EVs and batteries is predicted to grow tenfold in the Stated Policy Scenario and over 30 times in the Sustainable Development Scenario by 2040. By weight, mineral demand in 2040 is expected to be dominated by graphite, copper and nickel, with lithium experiencing the fastest growth rate – increasing by over 40 times in the Sustainable Development Scenario. The shift towards lower cobalt chemistries for batteries will limit growth in cobalt demand, as it is displaced by nickel.

Electricity grids dominate current mineral demand from the energy sector, accounting for 70% of demand. Although their share is falling as other technologies experience rapid growth, they will still dominate in 2040. Demand for copper in electricity grids is expected to grow by 55% by 2040, while aluminium demand is predicted to rise by 40%, in the Stated Policy Scenario.

Mineral demand from low-carbon power generation (excluding nuclear) is expected to increase from 2.0 MT in 2020 to 7.2 MT in 2040 in the Stated Policy Scenario. This is currently dominated by wind and solar PV, and they will continue to form the bulk of resource demand for renewable generation – the requirements for hydro, biomass and geothermal are much smaller.

Accessing critical minerals will not be trivial

There is currently no unified definition of “critical mineral” although many countries (as well as the EU) have developed critical mineral strategies aimed at ensuring the necessary access to those materials they deem to be critical. But there will be many challenged in achieving these goals, including access to capital and expertise, the location of deposits and mines, the adverse environmental and social impact of mining, particularly on indigenous communities, resource nationalism and the risk of cartel formation, and trading risks including high levels of cyclicality, high price volatility and risks of market abuse by traders.

Accessing capital and technical expertise

Developing new mines requires significant amounts of capital and technical knowledge and experience. The mining sector is currently dominated by a handful of very large companies who, along with smaller players and possibly even new entrants, will need to gear up operations to deliver the huge increases in output that will be necessary to support the energy transition. Finding the money, skilled workers and other resources will be challenging. According to the International Renewable Energy Agency, IRENA, the top five mining companies control 61% of lithium output and 56% of cobalt output. Opening a mine and separation plant can cost from US$ 500 million to US$1 billion, depending on the location, element, ore grade, and a variety of other factors.

Fred Sveinson, a professional mining engineer with more than 40 years’ experience in exploration, development, construction, operation and financing of mining projects has described the process for opening a new mine. He says there are three key components to building a mine: a competent, experienced management team; financing; and a technically sound and economically feasible deposit.

In a normal market, financing will be available to proven management teams which can exploit even marginal deposits. A feasibility study would be carried out and a Life-of-Mine plan developed. A post-tax internal rate of return of about 20% to 30% would be considered positive, combined with a capital payback period of two to three years with a mine lifetime of five to ten years.

The key components for actually building the mine are engineering, procurement and construction management. The construction phase requires building roads, rail, air-strips or ports to access the mine plus the services such as water, sewage and power which can be particularly challenging as mines are often located in remote areas. It is also necessary to build crushing and processing plant, a tailings storage facility, and permanent waste storage areas, particularly if the waste is acid generating.

Development of the mine itself depends on whether it is underground or open pit, with underground mines typically using smaller equipment, which tends to make them more expensive to operate. The grade of ore that can be mined is a function of operating costs – the lower the operating costs, the lower the grade of ore that can be mined.

The crushing and processing facility is constructed based on the testing to understand the mineralogy and determine the best approach to recovery of the metals and the treatment or management of tailings. A lack of sufficient metallurgical testing up front has caused the failure of a number of projects. Most deposits require one or two stages of crushing to provide a feed to the grinding circuit of one quarter inch to half inch size, although with semi-autogenous grinding, the ore feed can be six inches. Conventional grinding will reduce this ore to fine powder.

Once the ore is ground to the prescribed size for optimum mineral recovery, the recovery process itself can begin. This depends on the metal type:

- Gold and silver can be recovered by gravity for the free gold/silver followed by cyanidation of the lower grade ore to make doré bars – a metal bar which includes 50-75% pure gold or silver which require further refinement before the metal can be used. Doré bars are neither ore nor bullion, but simply metal bars with a high gold or silver content. Alternatively, after gravity, a flotation step can be used to produce a lower grade concentrate that is shipped to smelters elsewhere for final processing.

Froth flotation works by exploiting the hydrophobic properties of gold molecules. The ore is ground into a very fine powder which is mixed with water to create a slurry. Surfactants are added to increase the gold’s hydrophobicity. The mixture is placed into a large tank filled with distilled water. Air bubbles are pumped into the tank and the water is agitated. The water repels the gold into the air bubbles, which rise to the top creating a bubbly golden froth which is skimmed and collected, and later condensed into metallic gold. The tailings and waste material sink to the bottom of the tank.

- Base metal and polymetallic ores typically use differential flotation – a flotation process which seeks to float out a single mineral to produce concentrates which are sent to smelters

- Heap leaching is used for lower grade precious metal and copper deposits, where the ore is crushed to a size that liberates most of the economic metals and does not have to be ground. Heap leaching eliminates the need for a grinding circuit, flotation and/or large cyanide tanks, reducing capital and operating costs. The crushed ore is trucked or conveyed to a leach pad where an impervious liner collects the leach solution from the heap, which is sprayed with cyanide as each layer of ore is placed.

Tailings from all of the processes must be deposited in a suitable tailings storage facility near to the plant, with a dam and often lined, or dried and stacked, or deposited underground after thickening, or after it has been made into a paste. If cyanide is used, then residual cyanide in the tailings stream must be destroyed prior to leaving the plant.

Building a mine typically takes 10 or more years from discovery to extraction with a huge amounts of capital deployed from the high-risk exploration stage through to building the mine.

Reserves are geographically concentrated, often in less developed nations

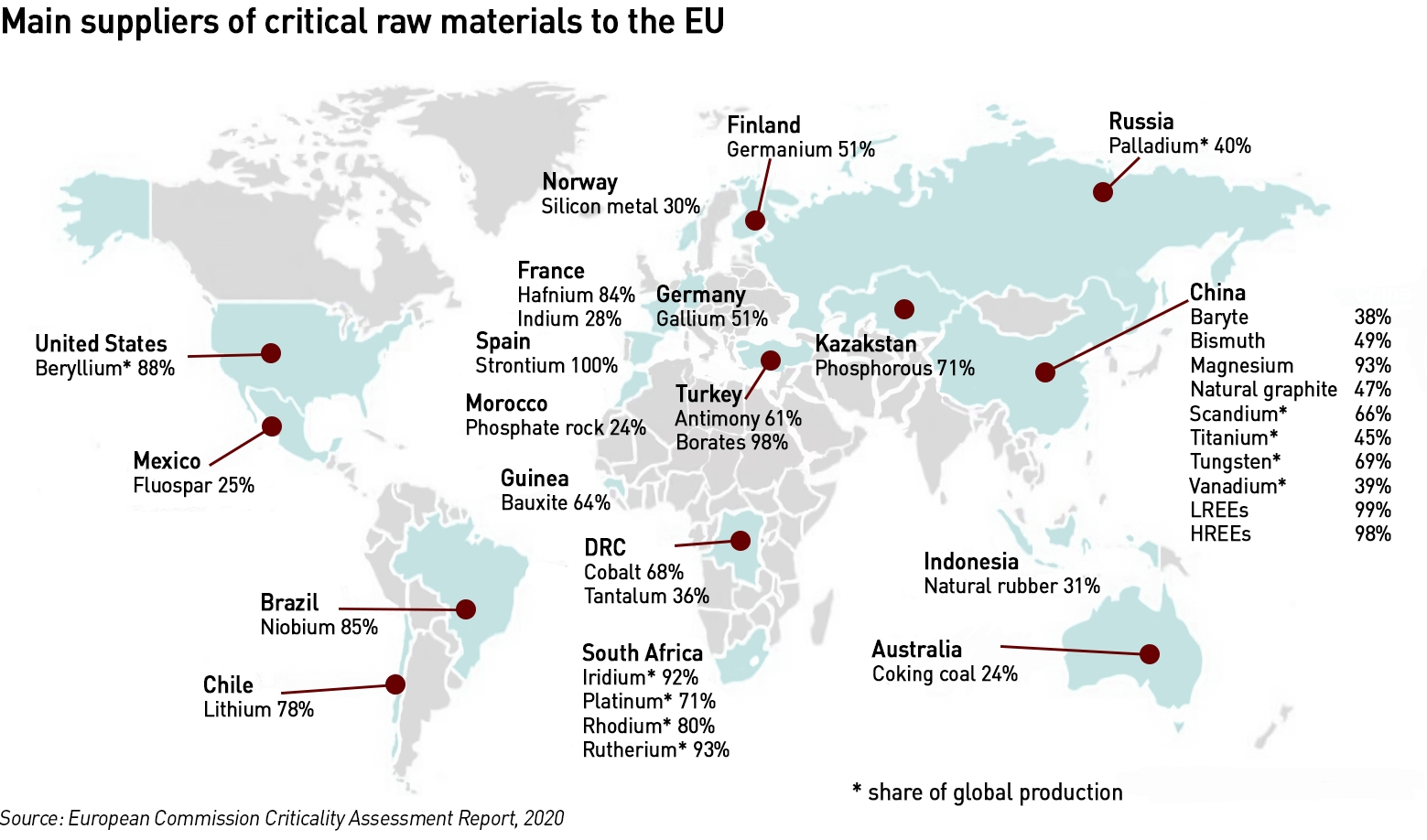

Second is the issue of where these minerals are located. They tend to be very geographically concentrated, for example, more than 70% of platinum is mined in South Africa; 70% of cobalt is mined in the Democratic Republic of Congo; more than 60% of natural graphite in China; almost 50% of nickel in Indonesia; almost 50% of lithium in Australia and almost 50% of the rare earth metal dysprosium is mined in China. Mineral processing is even more concentrated, and is dominated by China, with a 100% share of global refined supply for natural graphite and dysprosium, over 90% for manganese, 70% for cobalt, almost 60% for lithium and around 40% for copper.

This concentration is exacerbated by the efforts of foreign firms or governments to own and control mineral assets and operations. Chinese firms have equity stakes in lithium projects in Australia and Chile, a rare earth deposit in Greenland and cobalt operations in the Democratic Republic of Congo, Papua New Guinea and Zambia. Research found a 2% to 14% increase in the share of global cobalt production and an 11% to 33% increase for cobalt intermediate materials when accounting for the equity stakes of Chinese firms. Foreign mineral assets are also owned by American, British, Canadian, Japanese, Korean and other companies. China is also among the top importers or critical minerals. It is the world’s largest importer of raw or unprocessed nickel, copper, lithium, cobalt and rare earths.

Huge swathes of minerals are to be found in less developed nations where there are difficulties with access to capital and skilled labour, which in some cases have been resolved through massive Chinese investment, particularly in Africa. Less developed nations typically have weaker governance structures – the majority of minerals are extracted in countries categorised as either extremely unstable or unstable in the Worldwide Governance Indicators, which measure the quality of governance across six major dimensions, including governmental accountability, political stability and absence of violence, government effectiveness, quality of regulation, rule of law and control of corruption. Political or social unrest in producing countries, including coups, labour strikes and civil wars, all present risks to mineral supplies.

Corruption in mineral supply chains a significant risk according to the National Resource Governance Institute cited in the IRENA report, with the possibility of corruption at all points in the extraction value chain. Corruption risks are particularly high in the award of mining rights where officials may face pressure to compromise on environmental and social measures and due diligence more broadly, to accelerate approvals. Opaque tax structures incur significant revenue losses for governments, where unfair pricing arrangements and tax avoidance strategies by large multinationals can lead to substantial revenue losses for host governments. Research indicates that multinational enterprise tax avoidance results in losses of around US$ 600 million per year in corporate income tax from mining sectors for Sub-Saharan African countries.

The growth in critical mineral demand could trigger geopolitical conflicts over ocean sea-beds, which hold some of the largest estimated mineral deposits on the planet. Some countries such as Norway have already initiated deep-sea exploration within their exclusive economic zones or extended continental shelves. However, these areas often overlap between neighbouring countries, triggering disputes over resource ownership and extraction rights. There is also the prospect of deep-sea mining in waters outside any country’s jurisdiction. This is regulated by the International Seabed Authority, created by the United Nations Convention on the Law of the Sea, however, its regulatory framework remains incomplete, with member countries holding opposing views on how to proceed.

Environmental and social concerns make securing a just energy transition more difficult

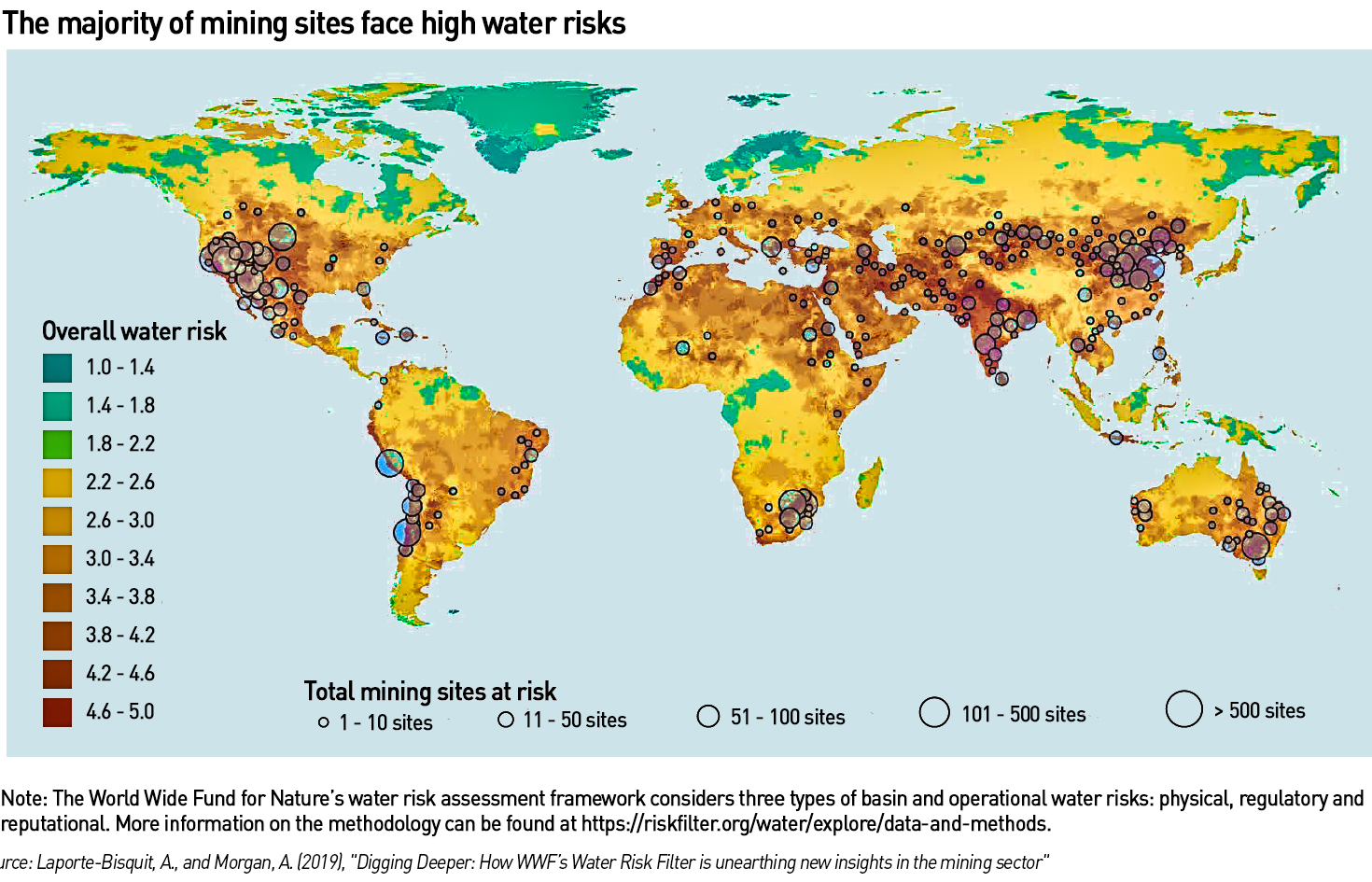

Thirdly there are social and environmental concerns. According to the IRENA report, around 54% of energy transition minerals are located on or near indigenous peoples’ land, which necessitates robust and early community engagement – a failure to do this, and ensure that the benefits of these resources are shared equitably is leading to protests which in some cases are causing mine closures. Over 80% of lithium projects and more than half of nickel, copper and zinc projects are located in the territories of indigenous peoples. In addition, more than a third of these mineral projects relevant to the energy transition are on, or near, land that faces a combination of water risk, conflict and food insecurity, another source of complaints by local and indigenous peoples.

The mining of critical materials has been associated with land loss, displacement and human rights abuses against indigenous communities. Poor labour conditions have been persistent across the industry, which lacks adequate social protection and labour laws in many places. These challenges are exacerbated by small-scale and artisanal mining, which is often characterised by hazardous working conditions, low wages and a lack of social protections.

Extraction industries are also environmentally harmful. The metals and mining sector is responsible for 10% of global greenhouse gas emissions, with aluminium and steel industries being major contributors due to the energy intensity of the smelting processes. Mining activities can be harmful to landscapes, for example, causing deforestation, soil erosion and pollution both by blasting materials into the atmosphere and through contamination of soil and water sources. Critical material extraction can also exacerbate water stress since it often requires large quantities of water. About half of global copper and lithium production is in highly arid areas, creating competition between mining and agricultural industries and the need for adequate supplies for human consumption.

Resource nationalism and the risk of cartels

The high concentration of mineral production raises concerns of market collusion and cartel-like behaviours including the formation of actual cartels. Historically, there have been numerous attempts by producer groups and governments to influence mineral markets through collusion. In the early 20th century, there were active producer cartels in the aluminium, copper, nickel, steel, zinc and lead industries, several of which were created in the 1930s in response to low prices during the Great Depression.

The 1960s and 1970s saw another wave of cartelisation, particularly in the metals markets, covering bauxite, copper, iron ore, tin, tungsten and uranium. Many of these attempts were short-lived due to disagreements between cartel members, the non-participation of major producers, or disruption due to mineral substitution or innovations in supply and demand technologies.

In addition to producer clubs, there have been several international commodity agreements involving both producers and consumers, such as the International Tin Council which governed the tin market from 1956 until its collapse in 1985 (see below). These agreements aimed to stabilise the tin market by establishing a buffer stock system that would allow producers to store excess supplies during periods of oversupply and release them during periods of shortages. This system kept tin prices artificially high for several years, thereby encouraging substitution of tin with aluminium, especially in the drinks can industry.

Trading risks: high cyclicality, price volatility and abusive market practices

Like many other commodity markets, the markets for critical minerals are highly cyclical, exhibiting a classic boom-and-bust pattern. This pattern tends to arise when lead times for delivering new supply – in this case new mines – are long, meaning it takes a lot of time to respond to increases in demand. Anticipatory investments can cause periods of excess supply, dampening prices, while delays to the development of new supplies creates shortages and price spikes. These risks are increased when demand changes rapidly, either as a result of wider economic concerns forcing a contraction in activity, or periods of economic growth boosting demand. The energy transition introduces new demand pressures into the sector, although these are overlayed onto existing economic dynamics, which is why (as I will explain in later posts) some critical minerals have experienced demand reductions and even supply gluts in the past couple of years.

Mineral and metals markets are also prone to market manipulation in the traded markets by both cartels and rogue traders, primarily because the markets are small with relatively low liquidity, and high price volatility. Low liquidity provides opportunities for market participants to attempt to develop market cornering positions which can restrict supply and cause price spikes. According to the IRENA report, there were at least 15 cases between 2000 and 2010, where competition authorities discovered attempts to form private cartels in mining and primary metals. In the 1985 tin crisis, the tin market collapsed when the International Tin Council, a cartel which tried to manipulate the price of tin by restricting exports from producing countries and buying tin on the open market, ran out of money to fund its positions. Tin trading was suspended and did not resume for 44 months.

In 1996 a trader at Sumitomo Corporation accumulated a large copper position in order to control the copper price and recoup previous losses. By November 1995 he controlled almost 100% of the London Metal Exchange (“LME”) warehouse receipts. The extremely tight physical market resulted in a huge price backwardation, leading to complaints from other market participants, and an investigation uncovered the unauthorised trading. When the position was revealed, the market crashed, causing Sumitomo and other market participants to suffer heavy losses – US$ 2.6 billion in the case of Sumitomo. The trader was later convicted of four counts of forgery and fraud, and sentenced to eight years in prison, however he was not charged with market manipulation. Sumitomo was fined by various regulators and paid over US$ 150 million to settle charges of copper price manipulations. The company sued various investment banks for assisting the trader in his illegal trading, and received around US$ 500 million in damages.

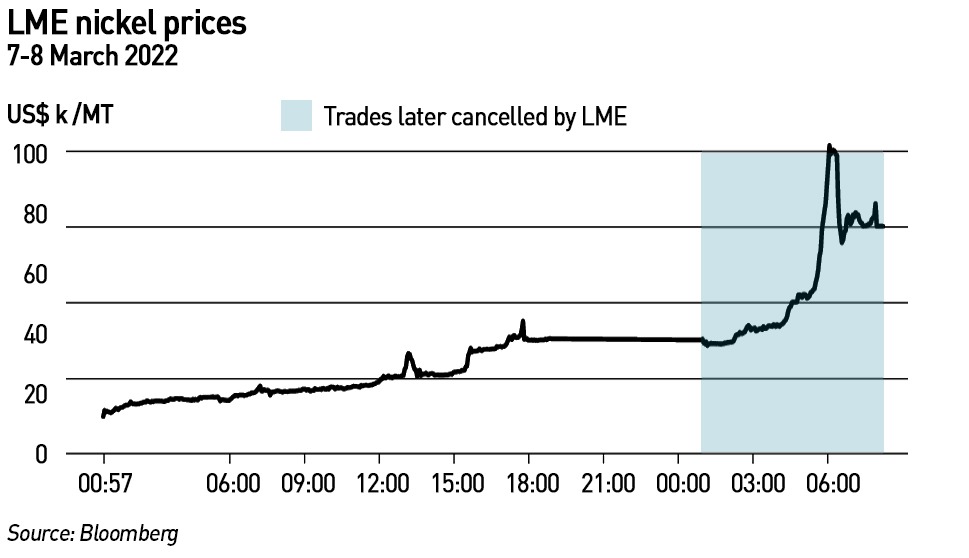

In March 2022, the LME suspended nickel trading after prices surged by over 250% in just two days as a result of a short squeeze, where a Chinese trader built a large short position in the expectation of a correction in nickel prices which had been rising as a result of the post-covid recovery and Ukraine war.

The trader built his position both on exchange and through OTC deals, with subsequent reports suggesting that only one-fifth of his total nickel exposure was built through exchange trading. The trader intended for his huge short position to drive the LME nickel price down, but at the same time, other market participants including Volkswagen, Glencore and JPMorgan, entered into large long positions which drove prices higher. When the trader tried to cover his short, the price went up even further.

Having allowed nickel prices to surge by around 250% in just two days to an all-time high of US$ 101,365 /MT – more than double the previous close – LME suspended all nickel trading and retroactively cancelled US$ 3.9 billion of transactions made before the suspension when nickel prices stopped reflecting the underlying physical market. Had it not done this, sources suggested to the press that the trader would have owed the exchange around US$ 15 billion. While LME’s decision to suspend the market and cancel the trades was later challenged in court, the challenge failed, although following the crisis the LME contract lost its benchmark status, and it took several months for prices to stabilise.

How far will western countries be willing to go to deliver their energy transitions?

Western countries – governments, investors, businesses and the public – face a moral dilemma which is scarcely recognised at the moment. Most have ambitious de-carbonisation targets, and strong commitments to “save the planet” and address the “climate emergency”. There are also moves to force companies to ensure their supply chains, both upstream and down-stream are both de-carbonised and ethical, for example through scope 3 emissions reporting and other Environmental, Social and Governance (“ESG”) metrics.

But these objectives are likely to be conflicting, as I highlighted in a previous post. Wind turbine manufacturers require rare earth magnets, which are almost exclusively supplied by China. Yet China has a poor record on both environmental protections and labour conditions. 45% of the polysilicon used in solar panels is produced in the Xinxiang province of China where there are widespread allegations of abuses of the Uighur population, including forced labour including in industries relevant to the energy transition. China as a whole supplied 85% of the world’s polysilicon. Water disputes are erupting in South America as the mining sector consumes water that is needed for human consumption and agriculture. And mineral extraction is an inherently polluting activity, causing contamination to air, earth and water. These issues often affect indigenous communities the most, exacerbating other historic wrongs.

Mining is dangerous both for the miners and for those living nearby both mines and mineral transportation centres, and there are issues with the treatment of waste which is often highly toxic. Countries with weak governance structures are more likely to face problems with illegal or inappropriate dumping of waste. For example, in the Cerro Chuño region of Chile, the United Nations estimated that by 2021 12,000 people had been affected by toxic mining waste, some of them losing their lives.

This is not only an ethical issue; it is an economic risk. In many of these countries, probably with the exception of China, there are risks of social unrest, labour disputes and hostile state action that could disrupt supplies – recently a large copper mine in Panama was forced to close over some of these concerns. Failing to ensure equitable treatment of local communities is not just unethical, it means that the supply of minerals critical to the energy transition may be restricted.

There are also questions about relative harms. Few people have given any thought to the question of whether polluting water sources in order to prevent or limit climate change is actually desirable, not least because the science behind the ability of policy actions to actually prevent or limit climate change is tenuous: we could succeed in de-carbonising but fail to limit climate change. People living in low-lying countries fear rising water levels and demand action on climate change, but those living in mineral rich areas demand clean water and uncontaminated air and soil in order to live healthy lives. So far there has been little attention paid to these trade-offs, although there are beginning to be calls for cleaner extraction technologies using less water. But delivering progress in these areas will be difficult as it involves not only identifying commercially and technically viable solutions, but ensuring they are implemented in places where governance may be weak.

.

In forthcoming posts I will explore the specific challenges associated with the main minerals required for the energy transition.

Critical minerals series

Following on from my post about the need to secure critical minerals for the energy transition, in this post I look at copper and aluminium…

Continuing my series on critical minerals, in this post I will look at some of the main metals required for lithium-ion batteries: lithium, cobalt and nickel…

In this next post in my series on the critical minerals required for the energy transition, I look at graphite and manganese….

In this final post in my series on minerals critical to the energy transition I look at rare earth metals.

Great article. It supports my view that we have spent too little time considering the question of “how” the transition will happen at a detailed level. We all know the why and the what. We now have a monumental struggle to deliver.

Many of our best project professions are retiring and we need to develop the next generation urgently. Thank you for showing some of the examples of where this expertise needs to be created.

Transition from fossil fuels to what?

Certainly it will not happen with weather dependant sources of electrcity generation.

Big Nuclear !

In the words of Jack Devanney (Gordon Knot Soc.)

All solutions have consequences.

No Nuclear Energy, no nuclear waste; No burning of fossil fuels no accelerated global warming.

BBC Radio 4 this morning announced Westminster’s decision to push on with Sizewell C.

More importantly at the end of the bulletin I welcome reference to two more sites; North Wales (Wylfa) & Cumbria (Moorside).

Both are part completed projects firmly established; no further planning, no nuclear licencing, existing infrastructure in place etc.

Hopefully the latter will NOT follow the Hinckley/Sizell projects (massively over time, over budget).

There other reactor designs out there that need to be considered subject to a thorough cost v risk analysis.

Barry Wright, Lancashire.

The sanctimonious ESG-led investment advocates thought it would be so easy to demonise fossil fuels. Once they start to consider the impact on the environment, water supplies, indigenous populations and so on their heads will explode.

Ironic that the loudest advocate for ESG investment is a company called BlackRock.

As anyone who has made it past the first chapter of an elementary economics textbook will tell you: a surge in demand that is not met by an increase in supply will send the price through the roof.

I believe something like this is already happening in the offshore wind business.

Great overview of the mineral supply chain and the challenges that today way beyond just extracting and processing the materials. Any sane Western govt wouldn’t want to be involved with many of these regimes.

I just finished reading this and the four associated articles – all of which are outstanding.

The pessimist in me wonders; could this become the background to World War III…?

On a lighter note, please can I thank you Kathryn for putting such high-quality analysis in the public domain free-of-charge. We are lucky to have you.

Thorium reactors have huge potential one has just been completed in China.