People are becoming increasingly concerned about the mineral requirements for the energy transition and how these will be met.

In October, the International Energy Agency (“IEA”) published a report entitled Electricity Grids and Secure Energy Transitions in which it sets out the grid-related challenges to the energy transition. It identifies regulatory reform, planning reform, increased grid investment and development of supply chains and workforce skills as the steps necessary to enable these challenges to be overcome.

“To achieve countries’ national energy and climate goals, the world’s electricity use needs to grow 20% faster in the next decade than it did in the previous one…Reaching national goals also means adding or refurbishing a total of over 80 million kilometres of grids by 2040, the equivalent of the entire existing global grid,”

– IEA, Electricity Grids and Secure Energy Transition

The main recommendations were as follows:

Regulatory reform: regulation needs to be reviewed and updated to both better use existing assets and the deployment of new infrastructure. Regulation needs to incentivise the investments necessary to keep pace with changes in electricity demand and supply. This requires addressing administrative barriers, rewarding high performance and reliability, and spurring innovation. Regulatory risk assessments also need to improve to enable accelerated buildout and efficient use of infrastructure.

Planning reform: grid planning processes need to be better aligned with wider long-term planning processes by governments. New grid infrastructure often takes between five and fifteen years to plan, permit and complete, compared with one to five years for new renewables projects and under two years for new EV charging infrastructure. Stakeholder and public engagement are key both to inform scenario development and to ensure public acceptance – the public needs understand the link between grids and a successful energy transition.

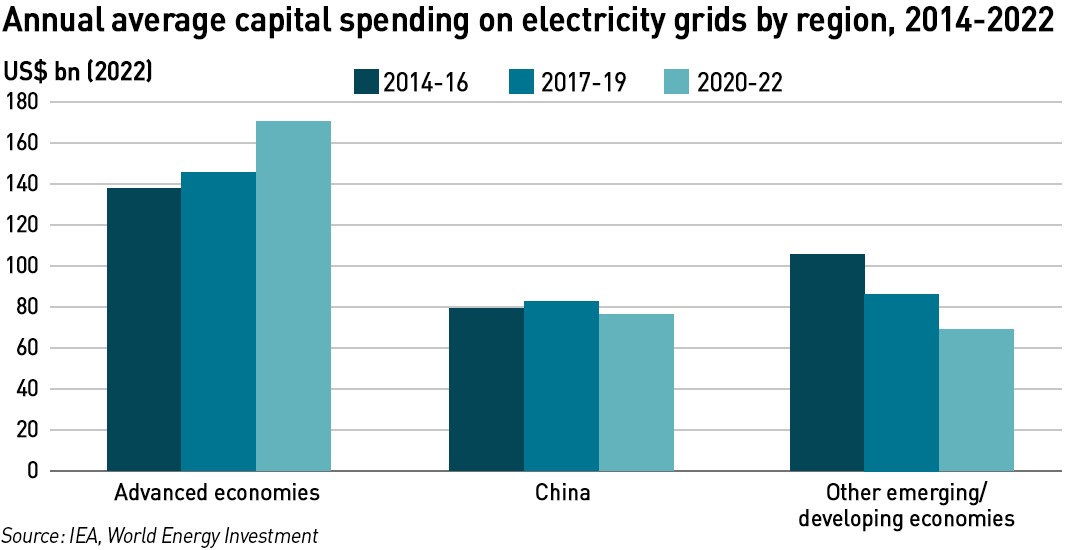

Increased grid investment: grid investment needs to almost double by 2030 to over US$ 600 billion per year after over a decade of stagnation: emerging and developing economies, excluding China, have seen a decline in grid investment in recent years, despite robust electricity demand growth, while advanced economies have seen steady growth in grid investment, but at too slow a pace.

Developing supply chains and workforce skills: the expansion of supply chains can be supported by creating firm and transparent project pipelines and standardising procurement and technical installations. There is also a significant need for skilled professionals across the entire supply chain, as well as at operators and regulatory institutions.

According to the IEA, the most important barriers to grid development differ by region. The financial health of utilities is a central challenge in some countries, including India, Indonesia and Korea, while access to finance and high cost of capital are key barriers in many emerging market and developing economies, particularly in Sub-Saharan Africa. For other jurisdictions, such as Europe, the United States, Chile and Japan, the strongest barriers relate to public acceptance of new projects and the need for regulatory reform. Here, policy makers can speed up progress on grids by enhancing planning, ensuring regulatory risk assessments allow for anticipatory investments and streamlining administrative processes.

Developed world power grids are aging at a time when expansion is necessary

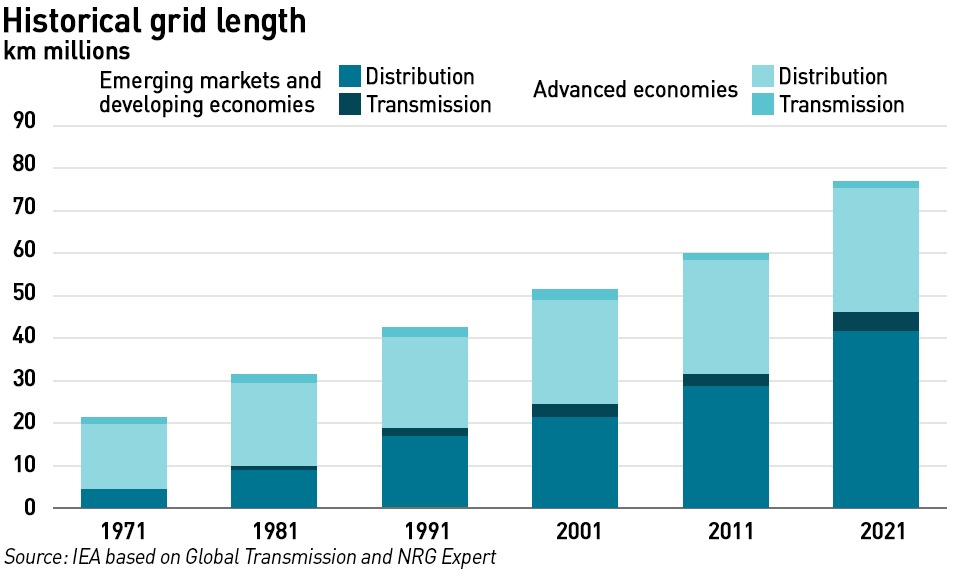

Grid length has almost doubled over the past 30 years, growing at a rate of about 1 million km per year, primarily driven by expansion of distribution networks which account for about 93% of the total length. In 2021, there were almost 80 million km of overhead power lines and underground cables worldwide, which equates to about one hundred trips to the moon and back.

Some 15 million km of distribution lines have been constructed in the past decade, with emerging markets and developing nations accounting for almost 12.5 million km. India alone contributed more than 3.5 million km, while China added nearly 2.2 million km and Brazil added 1.7 million km. Advanced economies experienced a modest rise of around 9% over the past ten years. The US added around 925 000 km of new distribution lines, and EU countries added around 715 000 km. Japan’s grid only experienced a 3% increase, equivalent to fewer than 40 000 km.

In terms of transmission infrastructure, China accounts for over one-third of global expansion in the past decade, having constructed over half a million km of transmission lines. India and Brazil have also undertaken significant expansion – India has added nearly 180 000 km of transmission lines over the past decade, an increase of around 60%, while Brazil added over 92 000 km during the same period, growing by more than 50%. Advanced economies saw a more modest 9% transmission system growth.

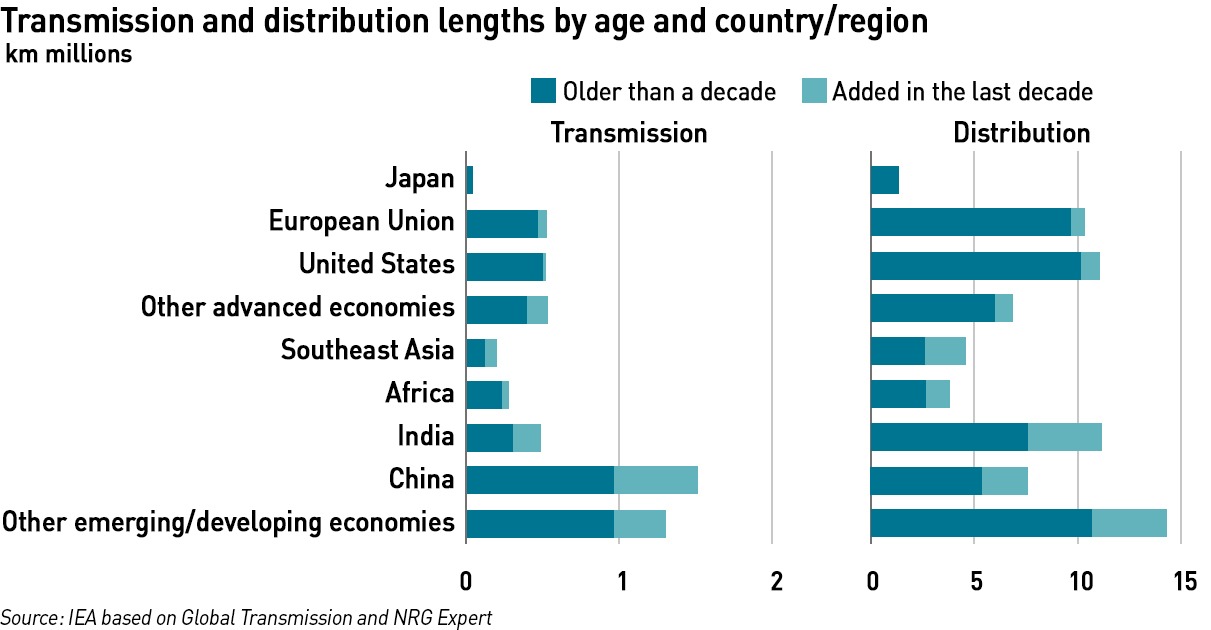

Grids, particularly in the developed world, are aging, posing safety and reliability risks as well as a requirement for additional investment. Only around 23% of grid infrastructure in advanced economies is under 10 years old, and more than half is over 20 years old. Countries such as Japan, the US and those in Europe, have a high proportion of their grids dating back over 20 years.

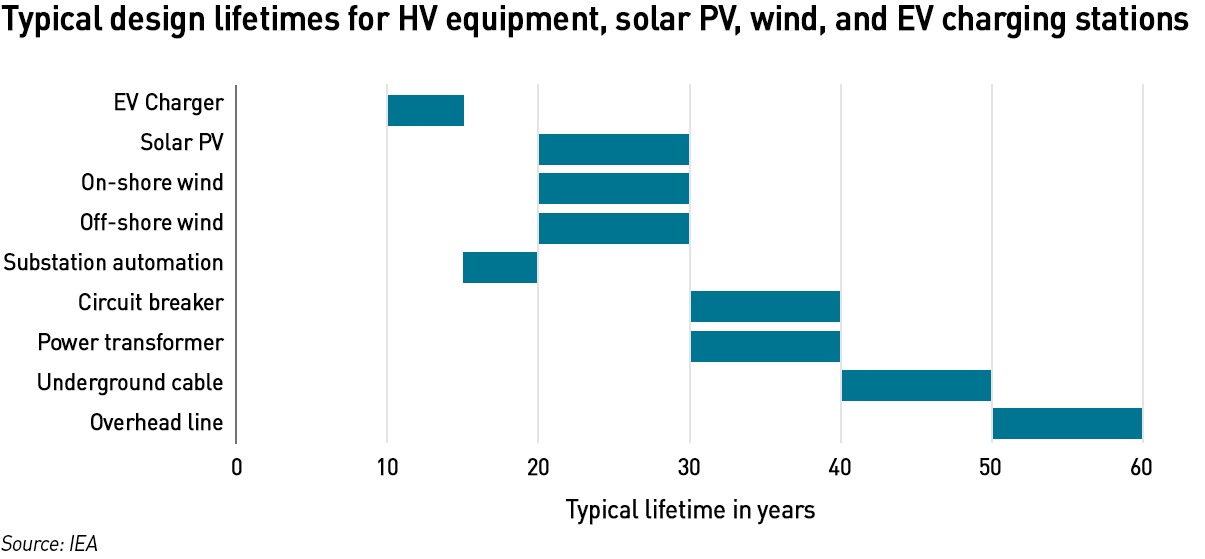

Transformers, circuit breakers and other switchgear in substations typically have a design life of 30 to 40 years. Underground and subsea cables are generally designed for 40 years, although newer versions may be expected to last for 50 years, while overhead transmission lines can go for up to 60 years before requiring a major overhaul. However, expensive items such as transformers are often kept in use past their expected lifetime, due to their high cost of replacement.

The digital elements of power grids have a much shorter lifetime, but also have faster innovation cycles. Control and protection systems often have a design life of 15 to 20 years, which offers significant opportunities to introduce new functionality that increases the flexibility and reliability of grid operation, however, issues such as software life cycles and cybersecurity must also be taken into account with updated equipment.

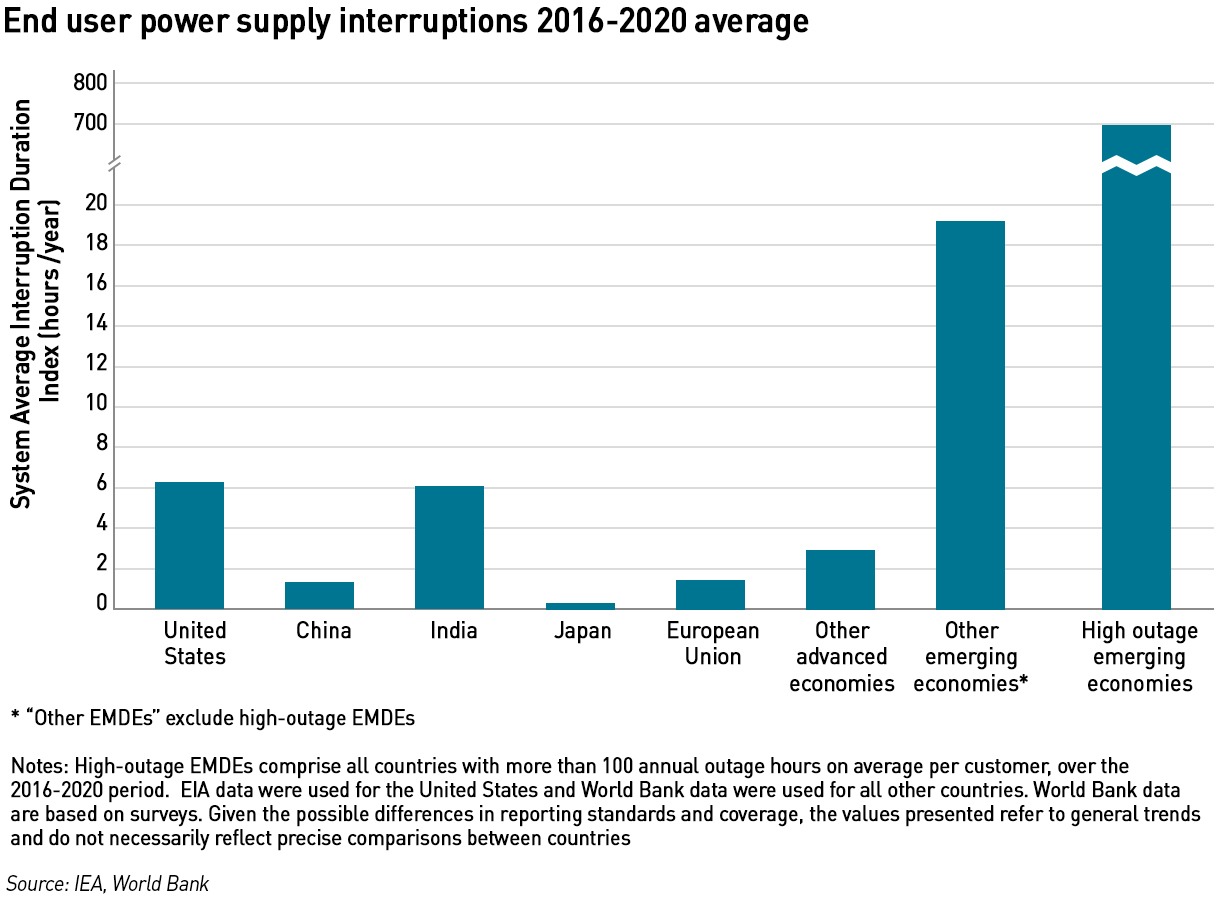

Grid reliability varies widely by region. Issues of reliability are growing in importance with increased electrification. Reliability data are hard to come by, and few countries differentiate between interruptions originating from generators, from transmission or from distribution networks. In four countries that do provide this information – the US, Japan, Australia and Chile – over 90% of power supply interruptions originate in distribution grids. In the EU, although comprehensive data for individual outage events is not available, reliability indicators show that most outages originate in low-voltage grids.

The IEA estimates that grid-originated technical/equipment failures caused outages that amounted to a global economic loss of at least US$ 100 billion in 2021. Most direct economic losses from outages arise from lost productivity at businesses experiencing interruptions, supply chain interruptions and potential damage to equipment. More indirect economic losses, such as those from fuel consumption in back-up diesel generators, can also be significant – for example, in Nigeria 40% of electricity is produced from back-up generation.

Common sources of technical failure are power transformers, instrument transformers and cables. In regions subject to high levels of precipitation, storms, monsoons and tornadoes, weather events typically account for a higher share of the outages. Human-related factors such as accidental damage, faulty installations and vandalism remain significant in many regions, with a notable trend in some countries toward increasing theft, vandalism and cyber attacks on grids.

Power system interconnection is being used to strengthen grids to accelerate renewables integration

Until relatively recently, power systems generally operated independently, but with the increase in electricity demand, and the deployment of renewables, regional co-operation has grown, and with it, there has been growth in cross-border connectivity. This is generally seen as beneficial – countries with surplus electricity can support those with a deficit, however since the Russian invasion of Ukraine and water shortages last year in Norway, there has been an increase in energy nationalism in Europe that is likely to be indicative of sentiment more broadly in times of regional system stress.

For the most part, cross border flows work well, but have the potential to create problems in neighbouring grids. For example, Germany built a large amount of renewable generation in the north of the country but did not build the necessary transmission capacity to move that electricity to demand centres in the south, choosing instead to send this electricity south via the Polish and Czech grids. This caused problems with local overloading in those countries leading them to complain to Acer (the Agency for Co-operation of Energy Regulators in Europe) and install circuit-breakers on their borders. Germany and Austria were forced to split their single bidding zone as a result.

Electricity shortages last year in typically exporting countries (France and Norway), together with concerns over gas supplies due to the Ukraine war, prompted concerns over energy nationalism in Europe with some grid operators suggesting privately they would protect their domestic interests irrespective of market rules. Even without explicit energy nationalism, with many countries sharing both similar weather and a growing dependence on weather-based energy resources, interconnection could create risks in times of system stress since many countries could face shortages at the same time. A prolonged heatwave across much of Europe last year highlighted this risk as many countries experienced several weeks with low wind output.

It may be the case that in normal times, increased interconnection allows more efficient use of energy resources, but in times of system stress, countries display a reluctance to export unless their own market is adequately supplied, regardless of price signals.

Importance of digitisation currently focused on EV infrastructure and smart meters

The IEA asserts that digitisation is a major trend in modern power grids, but its data suggest that aside from the introduction of EV charging infrastructure and the deployment of smart meters, this trend is actually quite weak. While smart meters can provide grid operators with instantaneous information about demand, there is limited evidence that this is happening in practice, generally because the structures necessary to capture these information flows have yet to be developed.

There is a couple of challenges here. One is driven by ownership of the meter itself and the underlying customer relationships. In most countries, electricity meters are owned and operated by network operators, so they have direct access to the data, however in the UK, suppliers sit between the customer and network operator, meaning that data protection requirements must be met which may reduce the transparency with which data can be shared. Secondly, different markets have different settlement rules – in GB, many classes of consumers are still part of the old demand profiling system where demand profiles rather than actual consumption inform settlements at the supplier level and there is no half-hourly settlement for consumers who are billed on consumption during longer periods of time (weeks and months).

Increasing digitisation of both distribution and transmission networks can also be used to help network operators understand what is happening on their grids, and the health of equipment. Remote control of the grid minimises intervention times and the number of operations that need to be performed locally, making operation possible from a single control centre using dedicated supervisory control and data acquisition (“SCADA”). Advanced automation tools allow the grid to act autonomously, quickly identifying and isolating the faulty element. For example, self-healing automation of the medium- and low-voltage grid, already implemented in some countries, ensures automatic containment preventing cascading power outages. Machine learning is increasingly being used to process the growing amounts of grid data being collected, to predict demand patterns and potential grid issues.

In transmission grids, flexible alternating current transmission system components such as static VAR compensators (“SVCs”) or Static Synchronous Compensators (“STATCOMs”) enable real-time control of power flows, voltage levels and other stability characteristics. They could also modulate the generation of reactive power depending on need, further enhancing grid stability, however these devices are currently relatively rare, with higher deployment observed in Europe and Australia. The use of grid forming power electronics is expected to grow as the share of inverter based generation increases.

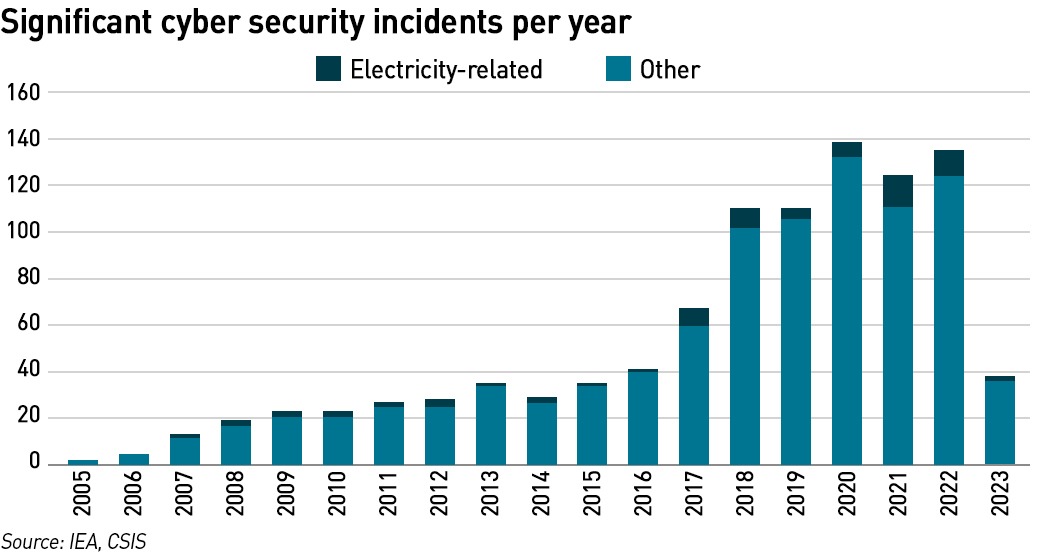

However, with increased digitisation comes a greater need for up-to-date cyber security measures as grids become more vulnerable to cyber attacks. Electricity transmission systems are considered to be critical national infrastructure, for example, the 2023 UK National Risk Register puts the likelihood of a cyber attack on critical infrastructure at between 5% and 25%, ranking as moderate, with a potential impact of hundreds of millions of pounds in losses.

In recent years, the number of cyber incidents has increased and there have been many cases in which cyber attacks on key infrastructure have caused major social disruption, such as the power outages that occurred in Ukraine in 2015 and 2016. The first outage in western Ukraine, including Kyiv, took up to six hours to restore and affected 225 000 people; in the second outage in Kyiv in December 2016, attackers disrupted power grid control equipment through unauthorised access, resulting in a 200 MW outage for about an hour. While the 2015 attack consisted of a multi-stage attack in which malware stole information and used it to remotely operate the control system, the 2016 attack is believed to have involved malware directly manipulating power grid equipment. This indicates a marked increase in the sophistication of attack methods even within a short period.

Another example is the military cyber attack on a satellite in February 2022, as a result of which around 5,800 wind turbines in Germany lost their internet connections, making remote monitoring and control difficult.

Congestion and connection queues holding back the energy transition

The dual trends of increased electrification and deployment of renewable generation, particularly in distribution grids, is increasing the demand on grid infrastructure leading to problems with congestion and difficulties in obtaining grid connections.

Grid congestion is a growing concern for both network operators and policy makers. Congestion arises when there is not enough network capacity to transmit all the available power from one point on the grid to another. This means that generation is not dispatched optimally as generation on one side of the constraint may need to be curtailed while potentially more expensive generation downstream of the constraint is used instead. This frequently occurs in GB where Scottish wind is curtailed in favour of gas generation in England due to a lack of north-south transmission capacity.

Congestion management data are not always reported, particularly in regions where the system operator owns and operates generators as well as the grid. In markets where system operators are required to report congestion costs, the indicators may also differ based on congestion management techniques. From those countries which do report such data, congestion costs are increasing. In Germany, congestion management costs reached more than €4 billion per year in 2022 while a recent study estimated that transmission grid congestion costs in the US more than tripled from over US$ 6 billion in 2019 to almost US$ 21 billion in 2022. In winter 2021/22 alone (November-March), Great Britain spent almost £1 billion due to balancing in response to transmission constraints.

“There is a direct link between renewable curtailment caused by grid congestion and (the lack of) progress on transmission and distribution capacity deployment. Even though some complementary solutions such as electricity storage via flexible EV charging can be beneficial, investing in grids will in many cases be essential to unlock the full potential of renewable resources,”

– IEA

Issues with grid congestion also effect the ability of network operators to connect new assets or loads to the grid. The US, Spain, Brazil, Italy, Japan, the UK, Germany, Australia, Mexico, Chile, India and Colombia collectively have grid connection requests totalling almost 3,000 GW of solar PV, wind, hydropower and bioenergy capacity. According to the data presented (which conflict with the text due to what looks like a typo) of this, 500 GW relates to advanced projects with a grid connection, or one close to being agreed, 1,000 GW are projects that are currently under review, and the rest – about half of the total – are still in the early stages of the development process. A significant investment in grid infrastructure will be needed to accommodate many of these new projects.

The addition of both grid-scale transmission-connected renewable generation and distribution-connected renewables are giving rise to a requirement for more grid infrastructure. This is easier said than done – deploying additional network capacity is complex, involves multiple stakeholders and can take many years. Large transmission projects can take a decade or more to complete, often much longer than building the new wind and solar projects that connect to them.

Significantly shorter lead times for transmission lines are observed in China and India compared to advanced economies, largely as a result of more centralised decision-making. In more advanced economies there is a greater emphasis on public engagement and support – in the autumn budget, the UK’s Chancellor of the Exchequer announced utility bill discounts to people living close to new power lines in order to reduce the impact of public opposition to these projects.

Power grid project development typically goes through three phases: scoping, permitting and construction. Unlike local projects such as generation, power grid projects often involve multiple authorities and jurisdictions along the entire route, which all need to review and accept plans before granting approval. For example, the 340 km long Ultranet line in Germany requires around 13,500 permits. Significant delays can result from complex permitting procedures, flawed government agency review processes, subjective interpretation or insufficient review of regulations, complex land use change requirements, and estimation errors. In Europe, over a quarter of electricity projects of common interest are subject to delay, most frequently due to permitting. Similar problems are observed the US and Australia.

Lack of public support can also considerably increase lead times – according to ENTSO-E, the most discussed issues driving public opposition include the visual aspects, human and animal health, audible noise and biodiversity. As a result, it may become necessary to adjust the route, and consider burying some sections, essentially re-starting the entire design and planning process.

Tightness in supply chains holding back grid upgrades and expansion

Further delays in the delivery of new grid infrastructure relate to the availability of materials. Global supply chains of all kinds have faced bottlenecks in recent years, in part due to the effects of the covid pandemic and the Russian invasion of Ukraine. Prices for both energy and raw materials have soared and there have been shortages of certain critical minerals, semiconductors and other components. Grid technology supply chains were severely affected, for example 50 MVA power transformers had typical procurement times of 11 months before the pandemic, but are now over 18 months as manufacturers struggle to cope with labour and material shortages.

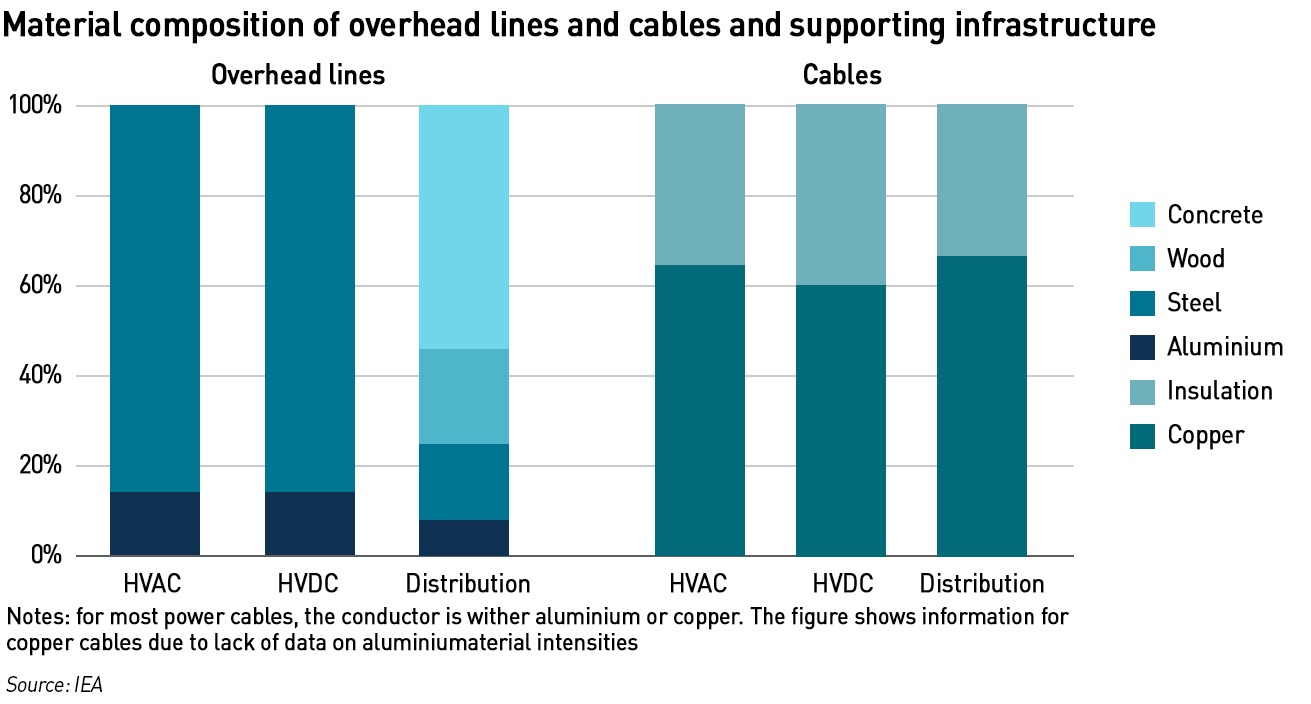

Building transmission lines is more complex than people think, requiring a number of different components and technologies – not just cables and lines, but transformers, substations and control systems, each requiring different materials and technologies. The material requirements depend on the voltage level – transmission capacity is the product of current and voltage: if the voltage is increased with the same current, transmission capacity increases.

Current determines the thickness of the conductor as well as its losses – the higher the current, the greater the conductor’s thickness and the higher the losses. Voltage determines the amount of insulation needed – either air for an overhead line or insulating material such as cross-linked polyethylene, PVC, cross-linked ethylene-propylene polymer and silicone rubber in the case of cables. The higher the voltage, the higher the need for insulation. The amount of conductor material and electricity losses can be reduced by increasing transmission voltage.

Copper and aluminium are the principal raw materials for cables and lines. Historically, copper has been preferred due to its good electrical conductivity and malleability, however it is three times heavier and much more expensive than aluminium. Aluminium has approximately 60% of the conductivity of copper, so wires need to be much thicker for the same capacity, but as it has a better conductivity-to-weight ratio than copper, it is usually preferred for overhead power lines and is increasingly also used for underground and subsea transmission lines, although copper is still more commonly used for these applications. An overhead ac transmission line requires around 11 kg aluminium per MW and per km (kg/MW/km), compared with 65 kg/MW/km for an overhead distribution line operating at a much lower voltage.

Wood, steel and concrete are used for the pylons in the distribution grid, while steel is used for transmission towers. Underground cables require 101 kg/MW/km of copper for transmission and 438 kg/MW/km for distribution.

An HVDC line requires around 5 kg/MW/km of aluminium for an overhead HVDC line and 29 kg/MW/km of copper for an underground cable. Reactive power makes a big difference in the material needs of HVAC lines compared with HVDC lines of the same capacity, as a significant portion of the power capacity of an ac line is used by reactive power (MVAr). This is not the case for HVDC lines, which is entirely used for active power transmission (MW). HVDC systems usually operate at higher voltages, which further reduces the material needs relative to ac for the same transmission capacity.

In addition to access to raw materials, there are other sources of bottlenecks in the supply chain. For example, subsea cables require cable-laying vessels, of which there are only 45 in operation worldwide, which can lay a total of 4,200-7,000 km of cable per year (depending on the type of project).

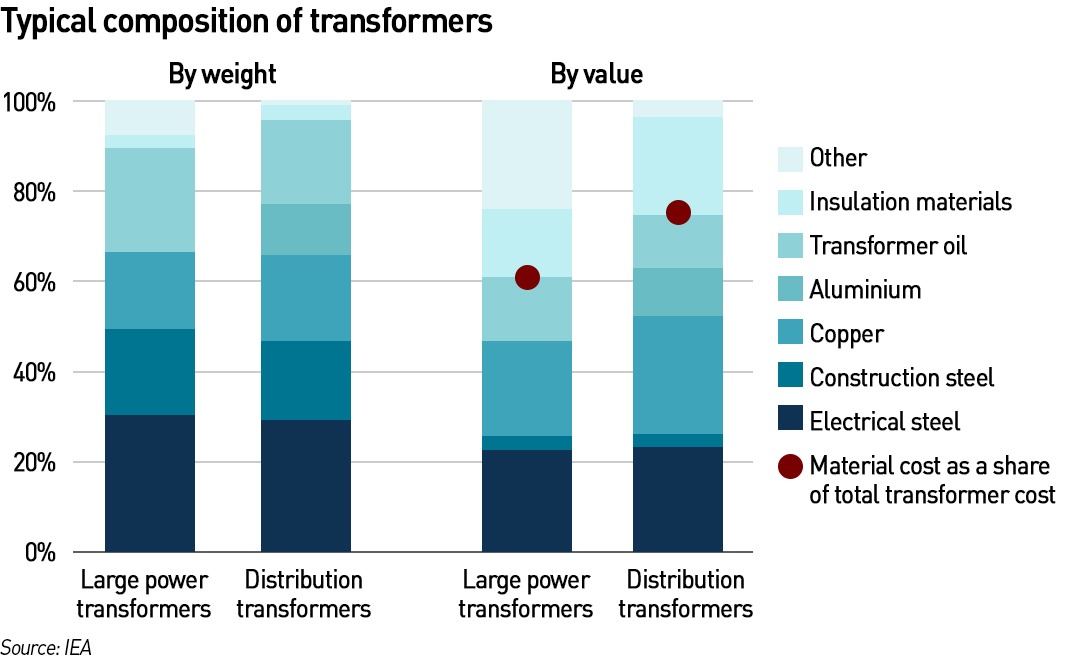

Electricity grids also rely on transformers to allow electricity to move across different voltage levels. Almost half of the material (by weight) required for their manufacture is steel, of which more than 60% is grain-oriented electrical steel (“GOES”) with specific magnetic properties and high permeability, while the remainder is construction steel. GOES is almost 2.5 times more expensive than construction steel, and is also a key raw material for power generators and EV charging stations. High permeability GOES enables transformers to be smaller, have lower losses and require less oil for insulation.

The cost of GOES in the transformer core represents more than 20% of a transformer’s total cost. Other raw materials include copper, aluminium, transformer oil for insulation, insulation material, pressboard, paper, plastics, porcelain and rubber. Aluminium is mainly used in low-voltage distribution transformers, while mineral oil is used in all types of transformers to insulate and cool the transformer windings (copper coils) and core.

Transformer manufacturing varies according to the size of the transformer. The production of medium-voltage and distribution transformers (building of the core, production of the windings and the oil tank, assembly of the core and windings and final assembly of the transformer and testing) is not particularly technologically demanding, and there are many factories around the world making them. However, production of large transformers is concentrated in a few companies since special facilities are required (drying ovens for windings, high power testing laboratories, etc.). More than the 40% of the global market is accounted for by just ten companies.

The transformer industry has been facing shortages of GOES, which led to price increases of 70% in 2022 compared with 2020. Sanctions on material exports from Russia, which accounted for almost 10% of global GOES production capacity in 2020, is an important factor. In addition, demand for non-oriented electrical steel has led some steel producers to switch part of their production away from GOES, reducing capacity.

There are also challenges obtaining HVDC convertor stations. A two-year supply shortage in the semiconductors market is expected to last into next year, and many of the materials required for components such as insulated-gate bipolar transistors, capacitors, switches/breakers, resistors, inductors, power transformers, DC filters, control systems and measuring instruments all face shortages of silicon, steel, aluminium, copper, nickel, polymer and zinc. The expected increase in demand for HVDC equipment over the next ten years will put supply chains under additional pressure. This could be amplified by a lack of experienced personnel in manufacturing and areas such as engineering, construction and project management, as well as drives to improve the sustainability of power grid components with several jurisdictions considering banning the use of materials such as lead and SF6, which have few alternatives.

The next phase of the energy transition will involve massive capital expenditure and may be unaffordable

Often in industry gatherings I hear people articulate a desire to “adopt best practice”, by learning from the experiences of others doing the same thing. This sounds great in theory, but in practice risks embedding bad ideas, which are unsuitable as circumstances change. This is largely what has happened with grid management – many advanced economies have similar approaches to things like grid connection queue management, having shared best practice for a world characterised by small numbers of large generation projects connecting to transmission systems, with largely passive distribution networks. All are now scrambling to adapt to an increasingly de-centralised grid environment.

But the developed world now faces a major challenge to ensure the grid infrastructure necessary for the energy transition is in place, and the necessary expansion of power girds is coinciding with a need to upgrade and refresh existing infrastructure, presenting a major funding and resourcing challenge. There are definitely things that can be done to improve matters – managing grid queues better and streamlining permitting processes. But availability of raw materials is likely to be a serious barrier that defeats these improvements, as I will describe in a forthcoming post.

Policy-makers are proud of the de-carbonisation that has been achieved so far in electricity systems (although in some places such as Britain, this progress was largely due to a need to move from coal to gas as coal reserves declined and cheaper North Sea gas came onstream), but this has very much been the low-hanging fruit. There is complacency about the next steps with several countries adopting 2035 as a target for a net zero power grid. But this means that many countries will be chasing the same resources at the same time. The transition so far has been expensive due to the need to subsidise renewable generation and the backup power needed to manage intermittency – the next phase is likely to cost even more as the cost of grid expansion in an environment of material scarcity begins to bite.

The questions of how this will be paid for have so far been ignored. But consumers in many countries are already struggling with both energy bills and the wider cost of living, so it is far from clear that these massive investments will be affordable. Policy-makers may well find that the next phase of the transition is harder, more expensive and has less public support than what has gone before, and that risks de-railing the entire enterprise. It’s all very well to argue about phasing out fossil fuels, as at the recent COP gathering, but developing the necessary replacements will be easier said than done, and it’s far from clear that this will be achievable over the desired timeframes. The net zero train may be about to hit the buffers.

Some quick sums: in the year to September wind and solar provided 77.5TWh according to Energy Trends. TNUoS costs have increased by about £2.7bn in the renewables era, while demand has fallen from 400TWh to 275TWh/year, and balancing costs have increased by about £3.5bn. The fall in demand is sufficient to offset inflation of up to 45% on pre-renewables grid costs, assuming a proportionate relationship. So it is not unreasonable to attribute the increase to renewables. £6.2bn/77.5TWh is £80/MWh of location and intermittency and instability costs. Wow!

And it’s about to get a whole lot worse as we add in storage, massive curtailment, pylons everywhere, floating windfarms etc.

Interesting view – unfortunately straw-man arguments:

– TNUoS costs have indeed increased; but it’s not all down to renewables. Interconnectors (who don’t pay TNUOS charges yet rely on the network and add to reinforcement costs), new transmission lines for HPC, new CCGTs and particularly business-as-usual asset replacement costs as SGTs and overhead lines reach the end of their life have also added to the bill (much of the transmission network is reaching the end of its design life and the true cost of the network that was ‘gifted’ to the industry at privatisation and had been paid for via central taxation previously, is only now becoming apparent)

– By concidence, your cherry-picked period of ‘year to September’ did indeed have one of the highest constraint costs recorded – but this was due to the record price of gas, not the cost of constraining wind volumes. But even accounting for the record gas price, the total bill for constraints was £1.5bn or £15 / year for a typical domestic bill, whilst carbon emissions from the GB power grid are at a less than half their value of 10 years ago.

– Renewables awarded CfDs have paid back £300 million over six months over the last winter period, and £1 billion forecast to be paid back between April 2022 and March 2023.

Why is it not obvious that domestically produced energy that is costs less than the marginal cost of that produced using gas, saves the consumer money and reduces the total volume of gas that needs to be extracted/imported, thereby increasing energy security too (irrespective of the environmental benefits)?