There has been a consistent narrative that the cost of building new wind farms is falling, with falling subsidy prices being offered as evidence. I have challenged this narrative in the past, pointing out that evidence from the accounts of windfarms themselves does not support this argument, citing the work of Professor Gordon Hughes at the University of Edinburgh, and indeed his work as subsequently been replicated by Andrew Montford of the Global Warming Policy Foundation (“GWPF”). However, there is another big reason to question this narrative: turbine manufacturers are losing money hand over fist.

Falling subsidy prices at the same time as massive manufacturing losses makes no sense and is clearly not sustainable. Of all of the projects that secured Contracts for Difference (“CfD”) agreements in the most recent subsidy round, known as AR4, only two have actually taken their Final Investment Decision (“FID”) – ScottishPower’s East Anglia 3 project, and Moray West which is a joint venture between EDP Renewables and ENGIE. Ørsted has warned that Hornsea 3 could be at risk without Government action “to maintain the attractiveness of the investment environment”. It has said it will make its final investment decision later this year.

The Government has said that the CfD is structured to take inflation into account, but other than introducing 100% capital allowances for a limited period in a bid to stimulate business investments in the Spring Budget, it has offered little additional help to renewable developers. “Long-life assets” only benefit from 50% relief, with many commentators believing that wind turbines will be considered to be “long-life assets” – these are typically assets with a life of at least 25 years, which tends to be the upper limit of the life of a wind turbine.

With the pot of money available for AR5 being lower than for AR4 there are now real questions about the sustainability of the trend of ever lower strike prices, and whether the AR4 projects will ever see the light of day.

So what’s going on? Something in this market is clearly broken, the questions are what, and what can be done about it?

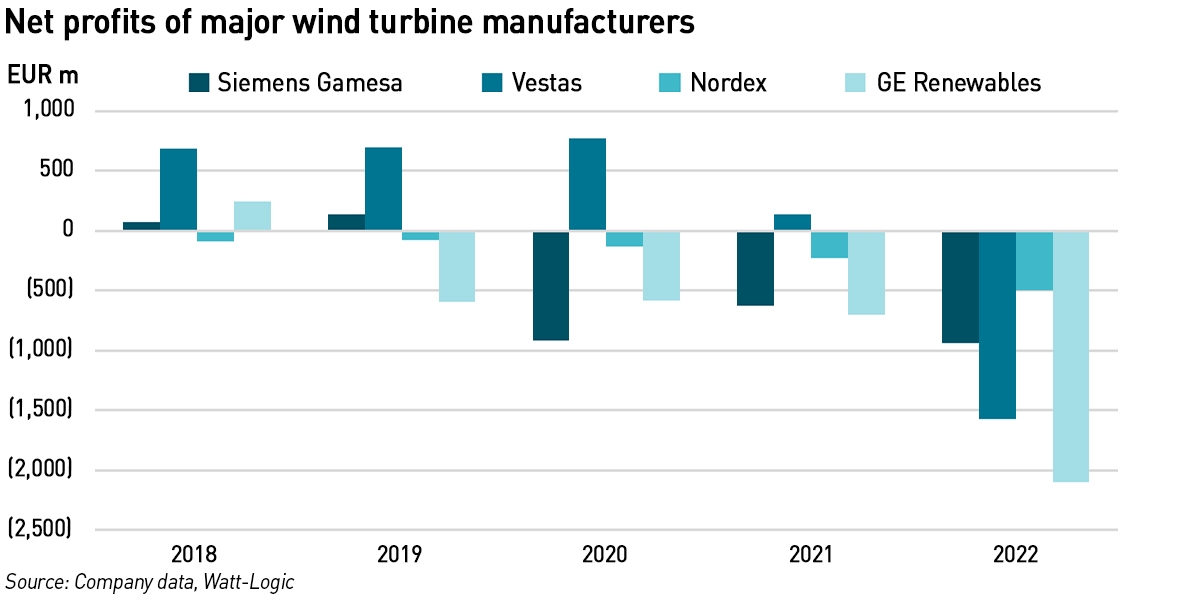

Turbine maker losses have been growing over the past three years

Turbine manufacturer losses began to be commented upon last year, and largely explained away as being a result of supply chain costs increasing due to covid and the Ukraine war. But looking at the figures more closely it is clear that the losses pre-date these events:

Senior participants at last year’s WindEurope 2022 conference said that the trend of turbine manufacturers selling at a loss will (self-evidently) threaten renewable generation targets.

“The state of the supply chain is ultimately unhealthy right now. It is unhealthy because we have an inflationary market that is beyond what anybody anticipated even last year. Steel is going up three times…It is really ridiculous to think how we can sustain a supply chain in a growing industry with these kind of pressures…Right now, different suppliers within the industry are reducing their footprint, they are reducing jobs in Europe. If the government thinks that on a dime, this supply chain is going to be able to turn around and meet two to three times the demand, it is not reasonable,”

– Sheri Hickok, Chief Executive for onshore wind, GE Renewable Energy

According to Nordex chief executive, José Luis Blanco, the economics in the wind industry had been destroyed due to price pressures from competitive tenders coupled with a low visibility of wind capacity pipelines due to failed government policies even before the Ukraine war. This is reflected in the financial results of turbine manufacturers.

“We are still selling at loss, because of the dynamic of auctions, the low predictability of volumes. We are investing in volumes in trust in market dynamics, then the volume doesn’t come, then a factory is empty, [and then] it is better [to have] some cash flow than no cash flow — and [consequently] the sector enters into a self-destructive loop…The energy independence is supported by a supply-chain dependency policy. This a huge risk.,”

– José Luis Blanco, Chief Executive, Nordex

Blanco said he was not only referring to rare earths, but also “normal things” such as metallic turbine shafts, 95% of which originate in China.

Enercon’s chief executive Jürgen Zeschky went even further, saying that over the past eight years, cost was the only driver for developments, with low levelised costs of energy and low turbine prices driving the industry. As a result, companies have been shedding manufacturing jobs in Europe, moving production to lower cost countries. The job cuts continued with GE Renewables and Siemens Gamesa both cutting staff last autumn.

Turbine manufacturer losses have continued into 2023. Siemens Gamesa reported its first-quarter net loss more than doubled due to higher warranty provisions as a result of faulty components – the company has been struggling with operational issues including problems with the 5.X on-shore turbine. The net loss in October-December the company’s fiscal first quarter, increased from €403 million in the same period last year to €884 million this year. Competitor Vestas has also had warranty issues in the past year.

“The negative development in our service business underscores that we have much work ahead of us to stabilise our business and return to profitability,”

– Jochen Eickholt, Chief Executive, Siemens Gamesa

Nordex also reported increased losses in Q1 2023, which went up by 9% compared with Q1 2022, attributed to “old contracts with a poor cost structure”. Its EBITDA margin remained broadly stable at -9.4% compared with -9.5% last year. The company’s rate of installation has grown this year and it expects profitability to improve due to “revised pricing and contract arrangements”.

GE Renewables saw Q1 2023 losses in line with 2022, with a net loss of US$ 414 million compared with US$ 434 million in the same period last year. There was a slight improvement in the profit margin from -15.1% to -14.6% due to the effects of cost cutting.

Siemens Gamesa said the outlook for the wind industry remained good, pointing to the US Inflation Reduction Act (“IRA”) and the EU’s RePowerEU programme, but said that “governmental action is needed to close the gap between ambitious targets and actual installations”. There are signs that the IRA is having a positive impact on US manufacturing with companies growing production capacity in the country in response to its incentives. Vestas, Siemens and GE have all announced plans to build new turbine component factories in New York and New Jersey, albeit contingent upon securing orders and receiving state and federal funding.

Ratings agency Fitch, said that “while turbine manufacturers’ profitability is under pressure due to increased raw material prices, supply chain difficulties and temporarily reduced orders”, the long-term sector fundamentals remain supportive. It pointed to significant cost increases in a market where most customer contracts are fixed-priced putting pressure on OEMs’ (Original Equipment Manufacturers) margins, and while OEMs have increased their selling prices over the past year, the pace of cost growth has been higher, leading to negative margins. Fitch expects margins to recover later in the year as manufacturers adjust selling prices, and raw materials costs fall, however, it says that the rate of new orders has slowed over the past year, due to adverse economic conditions and slow permitting processes in Europe.

Vestas, the leading OEM, with about 20% of installed onshore wind capacity worldwide, saw a decline in orders of about 18% in 2022 compared with the previous year. Nordex’s orders fell by 20% in 2022 versus 2021, while Siemens Gamesa’s onshore orders fell by 44%. However, in the first quarter of this year, most of these companies reported increases in orders.

Actual capital and operating costs of wind farms

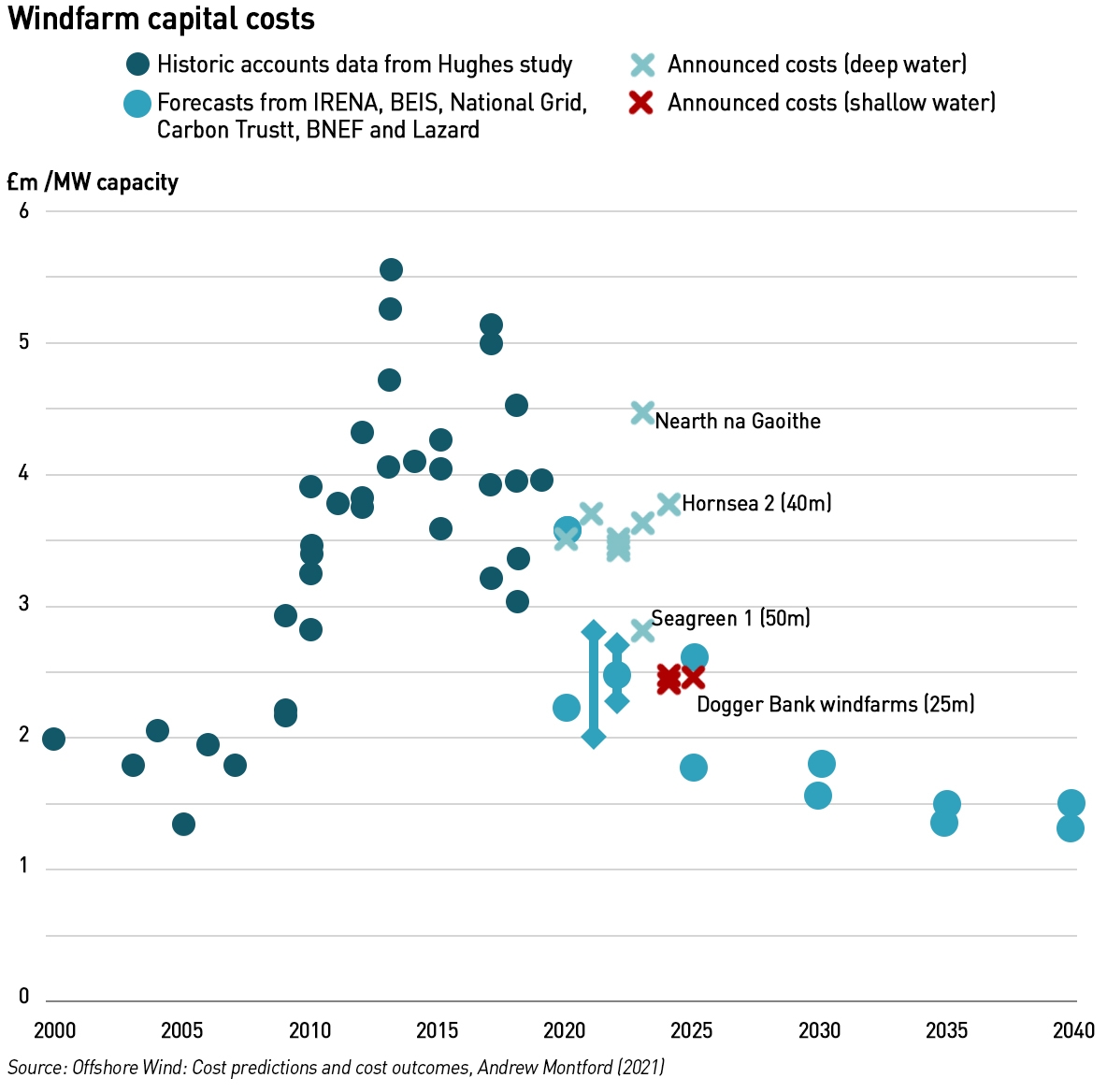

Back in 2020, Gordon Hughes published a paper in which he analysed the capex and opex of windfarms larger than 10 MW built in the UK since 2002. Most wind projects are individually incorporated as special purpose vehicles (“SPVs”) whose accounts are lodged with Companies House and available for public inspection. SPVs rarely employ staff, so it is straightforward to determine actual operating costs. I replicated part of his work and can confirm his conclusions, which were that:

- The actual costs of on-shore and off-shore wind generation had not fallen significantly over the previous two decades and he saw little prospect that they would fall significantly in the next five or even ten years;

- While some of the component costs had declined, overall costs had not. The weighted return for investors and lenders had fallen sharply, especially for off-shore wind, due to a reduction in perceived risk. In addition, the average output per MW of new capacity may have increased, particularly for off-shore turbines, however, those gains were offset by higher operating and maintenance costs;

- The capital costs per MW of capacity to build new wind farms increased substantially from 2002 to about 2015 and then, at best, remained constant until 2020; and

- The classic period for early cost reductions was over by 2010. While off-shore wind was in itself an immature technology, it was based on two significantly more mature technologies: on-shore wind and oil and gas infrastructure, limiting the potential for learning curve benefits.

Hughes compared actual capital costs with costs reported in public announcements before or during construction – both adjusted for inflation (to 2018 prices). He found that on average, actual costs were 18% higher than reported costs and in a third of cases the cost overrun was at least 30%. Reported capital costs were clearly affected by an “optimism bias”, but even so, there was a large increase in the reported capital cost per MW of capacity for off-shore wind farms over the 20-year period, with the main change being between projects completed up to 2009 and those completed in 2015-2018.

Part of the increase can be attributed to a move to deeper waters, but reported costs have increased even when adjustments are made for sea depth and other factors. The analysis of actual costs for UK off-shore wind farms completed up to 2019 shows an even worse picture than that visible in reported costs: in real terms the average capital cost per MW of capacity more than doubled from 2008 to 2019.

Actual capital costs for on-shore wind also increased significantly in real terms from 2002-2004 to 2012-2014. From 2014-2019 on-shore capital costs were roughly constant with no sign of any systematic decline. For a handful of individual projects, the switch to larger turbines (>3 MW) reduced the capital cost, but average capex of all on-shore projects with larger turbines actually increased since 2012. The median capital cost at 2018 prices of all projects completed in 2018 was over £1.6 million per MW compared to a median of £1.0 million per MW in 2006.

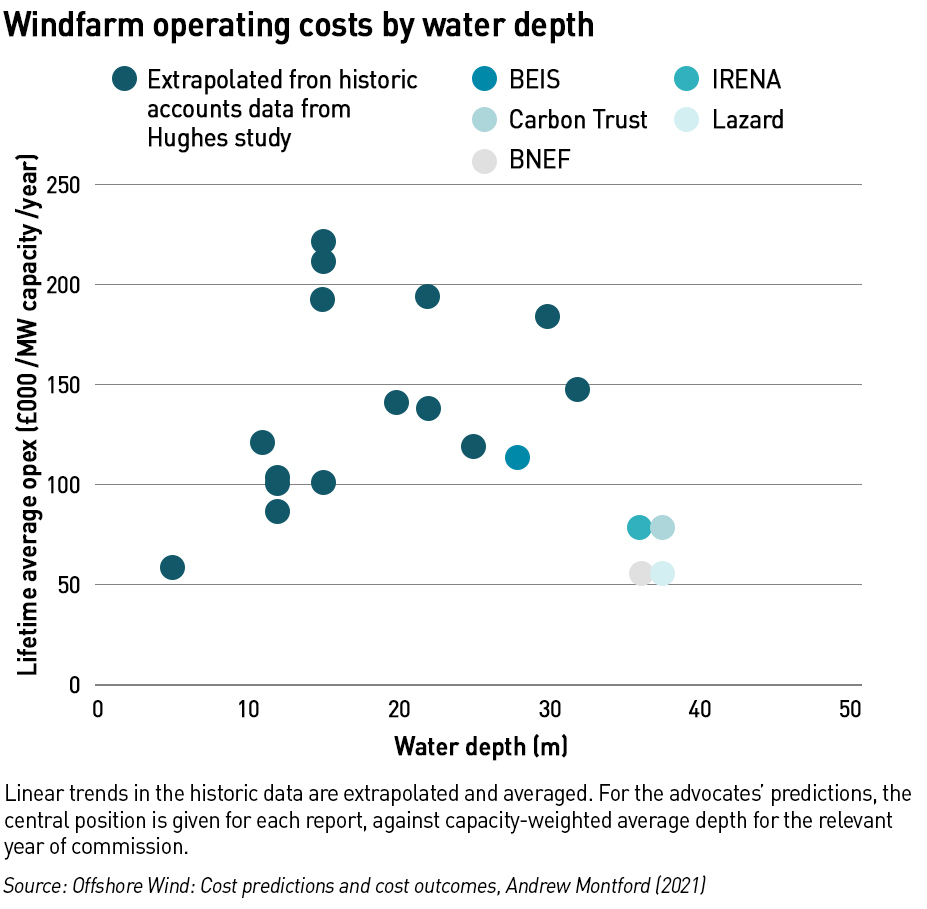

In terms of operating costs, there was strong empirical evidence of a powerful rising trend in opex per MW, with two factors driving the trend:

- As wind farms age, the average cost of operating and maintaining turbines tends to increase because equipment failures and breakdowns become more frequent. The average increase in operating costs with age is 2.8% per year in real terms for on-shore wind and at least 5.0% per year for off-shore wind (or 5.9% where operating costs included separate transmission charges); and

- The average cost of operating and maintaining new wind farms in their first or second full year of operation also increased rapidly over time: on average 4.4% per year for on-shore wind, and 5.5% per year for off-shore wind, together with substantial additional costs for working at depths of either 10–30 metres or greater than 30 metres. After allowing for the combination of the underlying increase in costs plus greater depth and changes in the regime for off-shore transmission, the initial operating cost per MW of capacity for a typical off-shore project quadrupled between 2008 and 2018.

While most wind turbines have a physical life of 25-30 years almost all are de-commissioned before they reach 25 years and many before 20 years, meaning their initial capital costs must be recovered over a shorter period and therefore the capital charge is correspondingly higher.

Despite the evidence from the audited accounts of actual wind farms, policy-makers persist in their belief that the costs of wind generation are (and have been) falling. They are supported in this view by all sorts of consulting firms and other interested parties, whose analysis suggests ever lower future costs. In his 2021 report for the GWPF, Andrew Montford compared the historic capex data from Hughes’ analysis with forecasts by a number of such analysts. He then compared them with announced costs for new projects as shown below:

The data indicate that depth appears to be the main driver of capital costs. It became more expensive to build off-shore windfarms between 2000 and 2010, although not all of this increase can be attributed to the move to deeper waters. Since then, costs remained in the range £3–5 million/MW, with little evidence of a sustained fall. In terms of predictions, BNEF, Lazard and Carbon Trust all predicted that capital costs for a windfarm completing financing in 2019 (and therefore starting operations in 2021 or 2022) would be around £2.3–2.7 million/MW. BEIS predicted that costs would fall to little more than £1 million/MW within ten years, with National Grid being similarly optimistic. [I was unable to find the two BNEF papers cited by Montford: Brandily T. 2H 2019 LCOE Update: Solar, wind and power prices at the crossroads, and 2H 2019 Offshore Wind Market Outlook: A blip before the bounce.]

Despite this, the costs announced by developers (bearing in mind Hughes’ findings that announcements tend to understate actual costs) showed an expectation among developers that capital costs in deep waters would remain largely unchanged, at least until 2024–25.

Similarly, the opex costs predicted by various analysts have been optimistic, particularly considering the ongoing trend to move into deeper waters. BNEF and Lazard have issued the most aggressive predictions, suggesting that opex costs of little more than £50,000/MW per year is likely for projects commissioning over the coming years.

There is little explanation of the cost reductions although BNEF suggests larger turbines will be “unlocking capex and opex savings”. The BEIS figure of £113,000 /MW for 2025 was based on the Dogger Bank project that was due to be commissioned in 2025, but while this is in relatively shallow water, it is almost 200 km from shore making it likely that this too will prove be an underestimate.

IRENA includes some discussion of operating costs, saying: “for 2018, representative ranges for current projects fell between [£54,000 and £100,000 per MW] per year (IEA et al., 2018; Ørsted, 2019; Stehly, T. et al., 2018).” However, Stehly et al. actually give a representative opex figure for off-shore wind equivalent to around £111 /kW /year (converted from US$ at 1.29).

Neither BEIS nor its successor department, DESNZ appear to have updated the official UK Government cost analysis since 2020 despite clear evidence that costs are unlikely to follow their previously predicted path.

Low CfD auction prices indicate strategic bidding rather than a genuine reduction in costs

Wind farm developers are warning that projects are at risk as a result of recent supply chain cost inflation and rising interest rates which have boosted financing costs. They are seeking tax breaks or enhanced subsidies from the UK government and claim that the sharp rise in costs is putting British projects at risk. According to the FT, several companies that won contracts in the AR4 CfD round last year have warned ministers that the projects will be difficult to deliver at the agreed prices.

Last year’s auction was the largest to date, and secured the lowest strike price so far, which surprised me at the time since the issue of cost inflation was already established at when the auction took place. Developers I spoke to afterwards told me they were confident of delivery, but that did not seem credible at the time. I think it is reasonable to question the auction strategies of these developers, when not only were rising costs evident at the time of the auction, turbine manufacturer losses had been growing for a number of years. This should have provided a strong signal that prices would have to rise since no company can be expected to trade at a loss indefinitely.

When the auction results were announced, they were widely celebrated as “proving” that renewables are cheap and that we should build more of them to reduce the country’s reliance on potentially very expensive gas, with claims that the projects securing contracts would “save consumers £58 a year compared to the cost of power from gas”.

“Low auction prices confirm that renewables are cheapest but we could have had a lot more. Now is the time to extend the use of Contracts for Difference to create a new deal between low carbon generators and the UK consumer,”

– Johnny Gowdy, Director, Regen

Of course, since then gas prices have fallen, and the successful AR4 projects are at risk of not being built, meaning consumers will save zero.

The pot and administrative strike prices for AR5 are lower than for AR4, leading to further concerns about the viability of Government targets. The administrative strike price in AR5 for offshore wind has been reduced to from £46 /MWh to £44 /MWh. The auction results are expected in early July, but many in the industry are calling on the Government to adjust the auction parameters or risk climate targets further:

“Unfortunately, in the light of global inflationary pressures, the budget and parameters set for this year’s CfD auction are currently too low and too tight to unlock all the potential investment in wind, solar and tidal stream projects which the industry could deliver…At a time when the US and EU are bending over backwards to offer incentives for renewable energy developers to come to them to build new projects, the UK is sending the wrong investment signals.

As a result, we risk losing vital opportunities to scale up our supply chains around the UK, denying communities the industrial-scale benefits which our sector offers…We’re calling for the government to revise the CfD budget so that we can stay on track to deliver on our renewable energy targets, as well as creating tens of thousands of high-quality green tech jobs and attracting billions in private investment in the years ahead,”

– Michael Chesser, economics and markets manager, RenewableUK

Unfortunately, Chesser made similar claims ahead of AR4. Although the Government set the budget for AR4 it did not force developers to bid, and the fact that a record number of contracts was awarded showed there was in fact strong developer appetite at the set budget. Or at least, so it appeared, until they started asking for more. The question is why did they bid they way they did knowing that costs were rising and that OEMs were losing £ billions? They must have known, or at the very least feared, that they would not actually be able to build these projects at the prices they bid at. This suggests their strategy was to secure contracts on the expectation they would be re-negotiated, because no-one would be able to deliver on them, providing the developers collectively with some kind of market power. Essentially, they got themselves a free option.

What happened to the Supply Chain Plans for the AR4 projects that are now apparently at risk?

Developers of projects that have a capacity of 300 MW or more must apply for a Supply Chain Plan (“SCP”) Statement from BEIS (now DESNZ) if they are planning to take part in a CfD auction, which they must provide to National Grid ESO (as the delivery body) as part of their CfD application. This is to ensure that “generators commit to a range of actions that can improve the competitiveness, productivity and capability of their supply chains. The rationale is that this, in turn, would increase competition and drive down the cost of generation over time, contributing to lower costs to consumers”.

It’s difficult to see how costs of wind power could have been driven down in AR4 compared with previous auctions when (a) supply chain costs were clearly rising due to higher raw materials prices which are fully outside the control of OEMs, and (b) those OEMs has for the most part already posted two years of significant losses suggesting that not only was there little scope for further price reductions, but that prices would likely rise.

In 2021, the Government modified the SCP process to accelerate supply chain development in light of its net zero targets. The SCP questions became more detailed, and BEIS introduced a more rigorous monitoring process to track SCP implementation. The delivery of a project’s SCP is assessed in a Supply Chain Implementation Statement issued by BEIS after a project has reached it milestone delivery date. Projects that do not score at least 60% of total marks in each section of their SCP at the implementation stage (or 50% overall for floating projects with projects under 300 MW) are unlikely to fulfil one of the Operational Conditional Precedents in the CfD contract, which may lead to CfD contract termination. Termination is recognised to be a significant consequence and is a last resort. The Government has subsequently consulted on making further changes to the SCP process.

Since the move to annual auctions the Non-Delivery Dis-Incentive (“NDD”), which prevents a developer from entering future auctions in relation to a particular site, has weakened since the exclusion period has shortened in line with the increased frequency of auctions. Last year the Government consulted on strengthening the NDD. Several respondents suggested it should be strengthened through the use of bid bonds particularly for Pot 1 technologies, with a quicker development process. (Pot 1 includes: energy from waste with CHP, hydro (>5 MW and <50 MW), landfill gas, off-shore wind, on-shore wind (>5 MW), remote island wind (>5 MW), sewage gas, and solar PV (>5 MW).)

Some also suggested that annual allocation rounds might increase the risk of speculative bids, as applying for a CfD could be seen as a risk-free alternative to merchant options. It was suggested that the NDD process should be strengthened to include fines for delays or non-delivery during the development phase (with a claw-back mechanism if the terms of the Supply Chain Plan were not met).

The Government decided that if a CfD offer is not signed or if a CfD is entered into and subsequently terminated in certain circumstances of non-delivery, then the eligible generator will not be allowed to make an application for a CfD in the next two allocation rounds in respect of certain sites, to apply from AR5 onwards. It also said it would closely monitor the results of AR4 to see whether the NDD remains an effective disincentive, while meeting the objective of increasing the generation capacity of renewables.

In other words, the penalty for non-delivery is a two-year restriction on applying for future CfDs at the site in question, which is arguably a very weak dis-incentive – it might discourage speculative bids in isolation, but where the entire market appears to have bid at unrealistic prices, the Government risks the collapse of the entire round with few if any developers actually building their projects. This means that the developers end up with the market power with the Government facing pressure to improve the economics of the auction notwithstanding the low headline price. And the worst outcome for developers is just a two year delay in progressing that particular project.

Should the Government improve the AR4 economics to ensure projects are built?

The Government has an unattractive choice: either it can insist on maintaining AR4 with its current economics, risking a failure of the round with few of the projects actually being built, which would undermine progress to net zero, or it could agree economic enhancements with developers. This would mean abandoning the narrative of ever-falling prices – arguably this should be abandoned anyway since it does not reflect economic reality – but the bigger problem is that it does nothing to discourage moral hazard. It leaves a bad taste to allow developers to get away with making artificially low bids to secure contracts they know they are unlikely to deliver, on the expectation of persuading the Government to sweeten the pot later on.

“The offshore wind developers seeking additional subsidies are treating taxpayers as fools. CfD contracts are inflation-indexed, so electricity customers will be paying higher prices for their electricity until 2040 and beyond as a consequence of recent inflation. The notion that there has been an unexpected increase in capital costs since bids were submitted last summer is ridiculous, as suppliers have been warning of severe cost pressures for at least 18 months. The reality is that offshore operators have been submitting unsustainable CfD bids ever since 2017, hoping that something would turn up. Even a period of very high market prices is not enough, so now they want to be bailed out by tax breaks. The Chancellor should just say No,”

– Professor Gordon Hughes, University of Edinburgh

It is time for the Government and the market to recognise more explicitly that the role of subsidies has changed. Two decades ago, when they were first introduced, it was on the understanding that subsidies were required to support immature technologies and would be discontinued once the technologies matured and became cost competitive. However, there is a growing realisation that the market is unlikely to ever be sustainable without subsidies. This is because the more electricity is generated with technologies that have near-zero operating costs, the lower wholesale electricity prices will become. If we look forward a couple of decades to a time when in most settlement periods during the year, the market price is set by intermittent renewables, they are unlikely to ever repay their capital costs through selling electricity (in those hours when prices are higher, intermittent renewables are unlikely to be generating and therefore will not benefit).

The Government recognises this in the REMA consultation, but it does not seem to be connecting that logic with the performance of the CfD. Of course, we are not yet in that sort of market yet, but there is clearly a floor that is significantly above zero, below which the strike prices are unlikely to fall if they are to reflect the true capital costs of the projects and likely income from selling electricity. The nature of the CfD is that developers do not benefit when market prices are higher, regardless of whether they are generating. In fact, they are insulated from market prices altogether.

Perhaps in recognition of this, the Government is consulting on including other factors in the CfD process such as sustainability, capacity building, innovation addressing skills gaps and enabling system flexibility and operability. Of course, this will make the auctions complicated to run – how would the auction process differentiate between a cheaper project which has few non-price benefits and a more expensive project which does? Some approaches are outlined in the consultation and described here.

The key drivers of project costs are materials, labour and finance costs, all of which vary based on economic cycles. If course, technological developments continue, as evidenced by the increasing size of turbines, but there have been quality control issues with some of these larger turbines, leading to increased warranty claims by developers, which has contributed to the poor financial performance of the OEMs. Privately some speculate that it’s time to pause the quest for ever larger structures and focus on getting the basics right.

In any case, it should be obvious that the status quo is unsustainable.

Government policy needs to be coherent and recognise changing economic realities

It’s interesting that news about developer concerns peaked in mid-March ahead of the Spring Budget, with developers using public and no doubt also private channels to try to persuade the Government to extend support to renewable generation projects in the budget. Despite this not happening to any material extent, things have gone quiet since, but at the same time, there has not been any great progress on the AR4 projects with only two out of six off-shore wind projects representing under 30% of the total capacity reaching their FID (2.28 GW out of the total 7.89 GW off-shore wind awarded CfDs in AR4). None of the 1.5 GW on-shore wind projects has progressed to the construction phase either.

Of course, there is nothing to stop developers from going the merchant route, and building renewable projects outside the CfD regime. This will allow them to benefit from market prices for electricity that are likely to remain above the strike price for some time. However, this approach is hampered by the Electricity Generator Levy, which imposes a temporary 45% charge on sales of electricity at a price in excess of a benchmark level of £75 /MWh, for companies providing more than 50 GWh per year. The Levy applies only to exceptional receipts exceeding £10 million per year and is due to expire on 31 March 2028. While the Levy in its current form is due to expire relatively soon in the context of the lives of these projects, its introduction will make investors more cautious of merchant models in case the Levy is extended or new, similar levies are introduced in the future.

It is clear that the UK Government, like many of its counterparts around the world, wants to encourage a lot of wind capacity to be built. Unfortunately, while other jurisdictions are increasing tax breaks and other support mechanisms, the UK Government seems determined to reduce them. This means that in a competitive international market, developers are turning their attention to projects elsewhere, and manufacturers are focusing on expanding their own capacity in countries such as the US where the IRA has created a very favourable investment environment. With access to raw materials constrained and likely to become more so as the energy transition progresses, the UK cannot afford to fall behind.

Of course, I am not personally in favour of a race to build more wind. The rapid increases in balancing and curtailment costs indicate that the GB grid is struggling to accommodate the intermittent renewable generation it already has – it makes sense to properly digest what has already been built before hurrying to build more. It might be smarter to focus attention on investments in grid infrastructure and demand reductions rather than pushing for ever larger amounts of wind capacity, in a competitive international market. But either way, the Government needs to recognise economic reality and ensure its policies are coherent: if it wants a lot more wind capacity to be built it needs to understand that costs are rising and therefore the investment landscape needs to be made more attractive, whether this is through higher CfD strike prices, tax breaks or other incentives. Failing to think this through risks leaving UK taxpayers with the worst of all worlds.

There is an alternative. Reconsider the benefits of the pursuit of net zero. Many parts of the world use increasing quantities of coal to generate electricity. Other than making UK increasingly un-competitive are our efforts towards net zero achieving anything? A time to hit the pause button and thoroughly review and re think the options.

I don’t disagree, but it’s a seperate argument. My point is that the Government’s expectations for wind are inconsistent with economic reality, and that developers are treating CfD auctions as a free option rather than a commitment to build. So both the price expectations and the non-delivery regime need to change if the targets for wind capacity are to be achieved. The fact that it might be better not to achieve them is beside the point – it would be preferable to miss the targets because decided to adjust them rather than because you failed to adopt the necessary policies.

Excellent article. Thank you!

this excellent piece of work underlines the fact that we urgently need to build a fleet of new nuclear fission power plants, and for now we need to drill for our own oil and gas, at least until such time as we have discovered some other form of high density affordable energy – i.e. nuclear fusion. We need our land for food and housing as well as nature, and we also need our territorial seas for food and national security. Our land and sea are too important to be used for expensive unsustainable wind turbine technology with its huge footprint, destructive environment for wildlife and need of rare and expensive metals and minerals. Our race to Net Zero is not working and so far it has been nothing short of a foolish delusion.

Thanks. I agree we need more nuclear and to maximise domestic oil and gas production. I also agree with your comment on the footprint of wind and think this will be a growing issue in future. In the past few years, scientists have observed something they call “global stilling” – a reduction in wind speeds. There is evidence that the presence of windfarms is making this worse. More research is needed, but I don’t think this is on the radar of policymakers at all. If I were to take a purely risk-based view, I would slow the deployment of new wind, and direct investments towards nuclear in particular, as well as grid infrastructure and insulating buildings.

Excellent article. The Government is trying to maintain the sham that wind costs are low and falling. But Capex costs are rising, opex costs are rising and the cost of capital has gone up dramatically. Who would have though that a mineral and capital intensive source of energy would be sensitive to higher commodity prices and rising interest rates?

https://davidturver.substack.com/p/exploding-the-cheap-offshore-wind-power-fantasy

Appreciate the amount of effort that it takes to produce such high quality work. It’s a very good review of the situation.

The UK consumer is already in the worst of all worlds, as there is not a single one of the major political parties that understands the mess our energy policy is in our how to get out of it.

Whilst not wanting to contradict any of the facts presented in the article, it seems clear that costs for all engineering technology projects are increasing at a much higher rate than in recent times. For me, this is not surprising given the momentous problems affecting the world over the last 4 years. It also seems clear that there will be a need to move away from fossil fuels whatever the eventual timescale. Increasing taxes on fossil fuels has potential to be used to manage the move and this will inevitably increase costs to the consumer. As we move away from the rather easy task of digging up or drilling for high density carbon fuels, this was pretty much inevitable. All governments can do is manage the transition. Not easy.

Someone has to try to map out the future for energy in the UK and plan for this when we know materials and manufacturing costs are likely to increase above inflation. My gut feeling is that wind power will always have a part to play in the UK’s energy mix. It will, however need to be coupled with efficient storage. Some may have noticed that I have a preference for local thermal storage for domestic heating as much of the capital cost is paid for by the consumer and lifecycle costs are relatively low. For industrial use, very high temperature thermal storage and compressed air are under development, but these add to the costs again.

The planning, for the UK, is very likely to include nuclear and fossil fuels during the transition, but the obvious difficulty is to know where to invest and when. I have lived through a couple of recessions and based on those experiences would make the prediction that there will be hard times ahead and falling house prices. ETA – I don’t think planning can include nuclear fusion

I agree that costs are increasing across the board as a result of higher raw materials costs. My point is that (a) windfarm costs had not been falling even before the recent supply chain increases and (b) those recent issues were already apparent at the time of AR4 but there was a collective denial of these facts leading to a situation where most of the projects are not advancing towards construction.

I don’t have any issue with the fact costs are increasing, nor am I suggesting this is unique to wind, but I do take issue with claims that wind generation is getting ever cheaper when the evidence clearly suggests otherwise.

The infrastructure necessary to send wind or solar power from where it is produced to where it is needed has never featured in all the subsidy bribes that renewables need. Time to SLOW Net Zero down. It’s a disaster ( to paraphrase Hemingway? ) happening slowly then suddenly.

AR4 still has the option to fail to declare a Start Date, meaning that the CFD is in fact merely an option, not an obligation. AR5 contains provisions enforcing the CFD once the wind farm is commissioned, and also offers no compensation any time the market reference price is negative, which means these wind farms would be first in line to curtail. The economics must look appalling, notwithstanding the fact that they would be exempt from BUoS charges worth several £/MWh. I note the AR5 process is stalled because an application (not necessarily for wind) was turned down and appealed, or at least that is the spiel. Shapps now has until July 24th to decide whether to re-run the process. It is hard to bridge the gap between the ASP ceiling, now worth £58.85/MWh and the €86.05/MWh price in the Irish ORESS 1 auction in shallow water.

I don’t know whether you had time to look at my submission to the consultation on providing backdoor CFD subsidies as you will have been very busy, not least following your bereavement, for which I offer my condolences. Basically I suggested that DESNZ ought to be honest and redesign the CFD auction scheme to the extent that they intend to continue to rely on CFDs (questionable if REMA is going to be another kettle of cuttlefish). Moreover, they need to reappraise costs on a whole system basis instead of blindly proceeding with wind on the false assumption it is cheap. Carbonbrief are starting to notice that increasing wind capacity will come with costly curtailment and costly grid expansion: costs that should be loaded on the incremental wind capacity before assessing its true cost. Recent solar curtailment on the Continent has cost GB consumers up to £550/MWh to reduce BritNed imports.

This piece would have made an excellent contribution to the DESNZ consultation. I’m pleased to see it is already getting attention elsewhere. Maybe we can embarrass them into lowering their level of insanity – doing the same thing over and over and expecting the outcome to be different..

Many thanks for your condolences – the circumstances were very unexpected and dealing with everything has been difficult and time consuming, so unfortunately I haven’t had the time to read your submission..it’s sitting with a few other things on the to do list! I’ve been sitting on these thoughts for a a whole and agree I should have put them into the consultation.

I’ve been thinking recently about the whole issue of subsidies. 20+ years ago, the intention was to prime the pumps to get an immature technology running and that once it reached maturity, the matket would be self-sustaining. If policymakers thought about cyclical costs at all, I’m sure they thought that by the time it mattered, subsidies would have ended.

But if we look at the GB power market, we can see that virtually NOTHING is being built without a subsidy, whether a CfD or Capacity Market contract – certainly nothing of any size. So the subsidies are not in fact supporting immature technologies for the most part, they are fixing a structure issue with the power market being fundamentally uninvestable. The primary reason for this is lack of long term liquidity in wholesale markets leaving very few mechanisms for project finance payments to be secured. Both tolling agreements and fixed price PPAs have fallen out of favour, meaning that the merchant risk profile is simply unacceptable for investors.

Essentially the subsidies are not solving the problem policymakers think they are. And that is why we see this disconnect between and assumption that subsidy levels will keep falling against the reality of rising costs. They understand the nature of the actual problem they are trying to solve, they will continue to come up with sub-optimal designs. They ought to be looking at how to make the market work better – in seperate teams they worry about the retail market and the effect that lack of proper hedging by suppliers has.

There is a clear need to facilitate mechanisms where both generators and suppliers can lay off long term risk in the market – they should start with consultations that get to the bottom of why the market is not connecting properly to manage these risks. Why is there so little long term liquidity in the wholesale power market? Why are fixed price PPAs losing traction? Why have we not managed to introduce liquid standardised tolling agreements such as the ones in the US (although some of those have risk profiles I can’t believe people have signed up to….).

The other issues around the costs intermittent generation imposes on the system are also worth addressing, and forcing those generation projects to bare those costs will make the investment environment more challenging. But at some point these issues have to be dealt with – consumers cannot indefinitely cover these costs to enable developers to pocket the high levels of returns they’ve got used to.

Just an initial response to your point that you are not for wind power because of the intermittency problem. That is the view on current production practices. But I see a future where that is taken care of by industries that can work with that intermittency. Steel making is likely to need a lot of electricity to change from Carbon fuels to Electric Hearth furnaces using large amounts of hydrogen. The Swedes are already working at pre production trials, of course you might want to put the industry back in Scotland or Redcar where electricity is being landed from offshore. The hydrogen can be made and stored. Other industries that might be prepared to work in novel ways where workers are paid using annualised hours where production ramps up with the windy season and ramps down in the summer months, these may, for example be: fertiliser chemical production, brick and cement products and maybe glassware too. Certainly it might work for fertiliser which is generally applied in spring following windy winters and it isn’t something you want to store if you can avoid. I accept that people both industrial managers and work forces will need to consider carefully how this works for the benefit of all. But just as home working has surprised some managers as improving productivity, in the longer term additional tricks are required to maintain training and productivity.

The real nightmare for trying to use hydrogen is the appallingly low utilisation factors that you get as you wait for very intermittent and highly variable surpluses to fuel your electrolysers. Intermittent operation is not good for electrolysers. Please see Chris Bond’s post and my comments here:

https://chrisbond.substack.com/p/hydrogen-the-64b-question/comments

Remember that Sweden has a large amount of nuclear and hydro that means it doesn’t have an intermittency problem, at least so long as snowmelt is good enough. Hydrogen based steel is not commercially competitive.

See also Shell’s Refhyne project that sought to make 1% of its refinery hydrogen via electrolysis at Wesseling. This report was pre energy crisis:

https://refhyne.eu/wp-content/uploads/2021/11/D7.2-report-v7.0-clean.pdf

and this one in the middle of the crisis

https://www.refhyne.eu/wp-content/uploads/2022/09/REFHYNE-Lessons-Learnt_Aug22_PU_FV.pdf

Not encouraging that they found the costs becoming even less competitive.

Some industrial process can’t be easily flexed – glassmaking is particularly difficult because if the glass cools in the furnace it becomes unusable. I think in the long run, small nuclear reactors could fit better into this space, providing the high temperaure heat needed for a lot of these processes. Wind is unlikely to be the best option because it produces no direct heat that is useful for industrial processes, and the use of wind to generate heat via hydrogen may struggle to be economic.

Brian, once you factor in the energy losses on making hydrogen and turning it back to electricity, you lose your enthusiasm for the approach. Offshore wind goes in at £125/MWh and you get power out of the sausage machine again at £3-400/MWh. It’s a non-starter.

Do the costs of wind include all the associated infrastructure? In Scotland, SSEN’s Pathway to 2030 (https://www.ssen-transmission.co.uk/projects/2030-projects/) is a £7billion project to build new overhead lines and associated substations to accommodate the planned increases in wind capacity – the Scottish Government’s ambition is for a minimum installed capacity of 20 GW of onshore wind and 11GW of offshore wind by 2030 (currently 8.99GW and 2.17GW, respectively). Some at least of the substations are to stabilise voltage now that there is so much intermittent generation. Some of these developments are huge – the substations at Peterhead alone will occupy 100 hectares. And then there are the planned pumped storage schemes, which will give a few days storage at huge expense.

Thanks for all your additional comments Kathryn. It has been obvious to me that the electricity market has never really worked since the introduction of wind and solar subsidies, precisely because the burden of extra network and back-up power costs have never been properly considered by Government or by National Grid, let alone shouldered by the operators of these unreliable power generators. Any power plant requires an element of back-up supply and network support, but it does look like no-one considered the problems that would arise transitioning from power stations offering an average year round reliability factor of 90% of their total capacity to plants that offered between 10 and 30%. It really does beggar belief that a system that depends on the British weather could be given so much financial support when it was abundantly clear that there could be no short term or easy fix to the hugely expensive business of providing back-up from energy storage. I don’t think any of our politicians have had sensible plans for our future power supply. And I dread getting a Labour Government when, despite the concrete evidence within company accounts, Keir Starmer is still saying on TV that “wind power is 9 times cheaper than fossil fuels”. How on earth are we going to save our economy if we have to keep pouring money into weather dependent renewables; network expansion and balancing, and huge energy storage projects. I think the future looks very grim unless we get a realist in charge at No10.

UPDATE

On 22 June Siemens Energy withdrew its profit guidance for the year due to high failure rates in wind turbine components which are currently under review:

https://www.siemens-energy.com/global/en/company/investor-relations.html

More quality problems have been identified, going beyond what they previously thought. Higher costs for fixing the problems are now expected to be in excess of €1 billion but this does not include mitigation measures. Productivity improvements are not materialising to the extent expected.

The review indicates that 15-30% of installed turbines will have issues over their lifetime.

On the call, it was noted that the industry has driven itself to a business model that needs to be re-worked, a process which has started, and that to ensure the energy, risk and rewaard balance in business models need to be appropriate.

Reuters reports:

On Friday, Siemens Gamesa said that while rotor blades and bearings were partly to blame for the turbine problems, it could not be ruled out that design issues also played a role.

It said the problems could affect as many as 15-30% of its turbine fleet.

The company said quality problems “go beyond what we were previously aware of, and they are directly linked to selected components and a few, but important, suppliers”.

Siemens Gamesa said it has launched a technical review of the installed onshore fleet and product designs, and that Thursday’s announcement includes problems uncovered so far.

The review also includes the role of Siemens Gamesa’s suppliers and whether they can be made accountable for the quality issues.

The company is now evaluating measures to fix the problems and figure out the associated costs.

The company said that it would be able to provide a more accurate estimate of the costs from the problems when it publishes its third-quarter results on Aug. 7, after a full analysis of the situation.

The issues add to woes already felt among many manufacturers which have faced rising costs for raw materials and competition.

Governments across the world are setting even more ambitious climate targets which require the rapid development of renewables, including wind power, which might be difficult to attain within the prescribed timelines.

Many wind power developers have already seen delays in projects due to the availability of components and rising costs.

So they aren’t really saying, but so far the admissions relate to onshore turbines rather than offshore ones. Hopefully come August 7th a journalist with engineering knowledge can be primed to ask more searching questions. Presumably it is particular models that are affected. It would be interesting to know about characteristics such as power ratings and blade diameters. Signs of similar problems at other manufacturers might indicate that we are going beyond optimum size designs taking account of maintenance costs etc.

I listened to the analyst call and got the impression there were also concerns over off-shore installations. I’ve also heard off-the-record speculation from industry insiders that it might be time to stop trying to build ever larger turbines, implying a link between the warranty issues and turbine size which would make sense.

Hello Kathryn, I suspect there is a little-discussed but important problem when trying to make wind turbines bigger and bigger. This arises from the inherent incompatibility, at high rotational speed, between the propellers (turbines) and the electrical machines built into their hubs.

For a given propeller technology, will not the rotational speed of the turbines tend to fall as their diameter increases for reasons of turbine tip speed limitation or centrifugal stress limitation? However, electrical machines (of traditional topology) are sized by torque rather than power. Specifically, the electrical machine’s power is proportional to BLAN(D^2) where B is the magnetic flux density in the air-gap, A is the electric loading of the stator (which is an alias for cooling effectiveness – the better the cooling, the higher A can be), L is the axial or active length of the air-gap, D is the diameter of the airgap, and N is the rotational speed of the generator.

We see from this “power proportional to BLAND^2” formula that, as propeller size increases thereby reducing rotational speed N, some or all of the other parameters (B,A,L and D) have to increase in order to accommodate the increased power. Parameters A and B are largely fixed by the mature state of electrical machine technology, and so L and D^2 have to increase to counter the lower rotational speed N. However, the product LD^2 is proportional to electrical generator volume and thus proportional to generator mass.

Hence larger turbine power at lower rotational speed necessarily implies a higher generator mass at the top the tower. This in turn will increases the quantity of materials used in the tower construction and thus its cost.

The use of a gearbox between the propeller and the generator would increase the rotational speed N seen by the generator. However, that is a trade which, apart from increasing part-count at the usually remote wind turbine site, simply replaces generator weight with gearbox weight.

Regards,

John.

Great article on the financial aspects of wind power at the present time.

We will get to cost and reliability optimisation for the different forms of renewable power. Solar PV has very low maintenance due to no moving parts, which should show up to be considerably cheaper than wind in the long term. Solar PV with potential for more than quadruple the lifespan of wind turbines, yes, over 4x longer, where panels can have over 80% of their original output after 30 years, theoretically may still have 40% of the original output after 100 years.

Except for individual panel failures and the replacement of inverters, this starts to get to an entirely new level of efficiency of material use in power production ever seen before. Will we get to a steady state of only replacing panels as they fail or get damaged to truly get every bit of use out of them? How many other technologies could manage that?

If you ever look at the comparative efficiency of use of materials of the different renewable technologies, solar panels have significant advantages. If we install 50GW of solar panels at a cost of say £50 Billion, we really don’t want to be scrapping them after 30 years if they are still giving 80% of their output……that would be like scrapping £40 Billion, scrapping many power stations that can put out 40GW peak fairly reliable GW, with no fuel spend, and variable OPEX, but say 10% every 10-15 years i.e. lower spending on inverters and the occasional panel, but any wind turbine is hard pressed to even achieve 25 years.

If we need to maintain capacity output, 0.5-0.7% degradation per annum is all that occurs.

The wiring for solar panels needs to be of the highest quality to maintain safety, reliability and longevity, or must be easily changed if failure is possible.

Whereas £50 Billion spent on wind with 20-25 year lifespan, takes significant £ Billions spend every 20-25 years to replace all turbines as long as the electrical network is OK for longer periods, the economics, performance and capital expenditure rates are completely different. This is where the comparative LCOE calculations that I have seen done by others which set a 30 year lifespan for solar PV bears no relation to the possible operation for maximum efficiency, which could be much longer.

The 25-30 years corresponds to the warranty period, but like cars, doesn’t mean that you have to stop using them and buy another new one. Airliners can be kept flying for over 40 years with high quality maintenance. Airliners had to improve fuel economy as market forces on profit were the driver, and so too is the same happening to renewables.

All you have to ask is what is the total kWh/MWh output per £ spent over the whole life, even if it does take more years to generate the output. Solar PV has the potential to be the most efficient.

Whilst the initial economics of all renewable technologies look very high compared with other power generation technologies, solar PV offers potentially significant differences in terms of performance, lifespan and costs to wind.

Thinking of the costs over the next 100 years. Wind turbines with all their significant stresses/mechanical nature cannot last anywhere as long as a solar PV installation, or CCGT units which should be lasting longer than previously planned with being on standby for extended periods, but wind will always probably have a 20-25 year lifespan, unless the designs are enhanced significantly and possibly new materials used.

Yes we need CCGT to back up renewable, but should be steadily used as a smaller proportion as different intermittent loads using the output can start to be used instead of constraining the output, considerably lengthening the service life.

As far as I can see solar PV is the only technology that has the potential with the highly predictable daily output in terms of timing that corresponds to our demand profile, but does not give a predictable magnitude of output, but its reliability, low maintenance and potentially 100 years or more of output must give greater benefits than wind and many other renewable technologies in the longterm.

Renewable power generation technologies can make electricity cheaper, but only if we use the right ones, or ensure we optimize the proportions of each technology installed. Wind, like CCGT is potentially more expensive than solarPV over the long term, so hopefully we will get to cheaper daytime electric and more expensive nightime electric pricing, and cheaper in summer than winter, as the technology providing the bulk of the supply changes throughout the time of day and season of the year.

Shouldn’t we be covering all buildings, roofs and walls, in solar PV?

Shouldn’t we be going solid state?

Of course Elon Musk is a pretty smart guy, so can anybody think why he is investing in solar panel and battery production?……Giga factories…….solar tiles.

Part of the problem is that there is a disconnect, where we should be looking for synergies, like Mr Musk.

Their website says “With a 25-year warranty, Solar Roof will continue to produce clean energy and protect your home for decades to come.”

And “Our in-house team of energy professionals has installed nearly 4.0 GW of solar across approximately 480,000 roofs—cumulatively generating over 25.0 TWhs of clean energy.” That’s 8-10kw per roof, although in America they do use a lot more power than us…….less energy efficient, the highest fuel burn rate of any country.

If a roof could be supplying 40% of it’s original output after 100 years, i.e. a 10kw roof still putting out 4kw…….when would you replace the roof?

Don’t we repair our roofs? Don’t we replace damaged tiles now every few years……..synergies.

What was that phrase?……slow and steady wins the race.

Not all renewable power generation technologies are the same, they all have their own unique characteristics.

Wind may have its place, but don’t you think Mr Musk is onto something?

Shouldn’t we have a solar tile manufacturing capacity here in the UK as a core business?………GB Sol is a well-known UK manufacturer specialising in solar panel roof tiles.

From their website ” PV Slates can be installed by GB-Sol or your roofer at a similar speed and cost as the natural slates they replace.”

Synergies……

(other manufacturers are available that would require importing that wouldn’t help our balance of payments like importing loads of hydrocarbons……………….. again.)

Solar panels ?

Ok in empty parts of Africa Australia USA but not in U K where land is a very scarce resource

Got it ?

So with the Net Zero Strategy – Build Back Greener where on P19 we were informed that “our power system will consist of abundant, cheap British renewables…..and ensure reliable power is always there at the flick of a switch”, the increasing percentage of renewables means we will be subsidising renewable generation, subsidising gas generation to keep the grid stable, subsidising any grid-scale backup using gas or hydrogen or batteries and finally subsidising consumers because the resulting cost will be so high.

Truly a brilliant system, which has been enabled by tricking the MSM and public into believing there is no difference between energy and power with false claims that X GW of renewables can power Y homes. The total energy produced in a year may be sufficient for Y homes but the power produced is intermittent and hence unreliable and no-one in the UK (yet) believes their power should be intermittent.

Renewables are parasitic energy requiring either gas or very, very expensive storage as backup and hence, basically, not worth a light.

An example is the Labour proposal in June to decarbonise our electricity by 2030 by quadrupling offshore wind, doubling onshore wind and trebling solar. This may produce sufficient energy over a year but there are times when the power deficit is as much as 41 GW! If anyone is interested in viewing the calculations, based upon the demand, wind and solar data for 2022 downloaded from Gridwatch, then please email me at jbxcagwnz@gmail.com.

If increasing anthropogenic CO2 emissions were a serious threat to our climate then back in 2008 when the CCA was passed a nuclear program would have been started, the only low CO2 emitting power source which is affordable, reliable, abundant and secure.

Spot on John Brown – I guess the rent-seekers have been busy these last 20 years passing brown envelopes to anyone who has enabled their scam – either that or our political class is more useless than I give them credit for.

Would you be able to comment on why the following analysis produces significantly different results to your analysis.

https://peak-wind.com/update-2022-opex-benchmark-an-insight-into-the-operational-expenditures-of-european-offshore-wind-farms/