In this final post in my series on minerals critical to the energy transition I look at rare earth metals.

The name “rare earths” is often used to describe all 15 elements comprising the lanthanide series on the periodic table along with scandium and yttrium. The term “rare earths” arises from the minerals from which they were isolated, which were uncommon oxide-type minerals, however they are neither rare nor “earths” (an obsolete term for water-insoluble strongly basic oxides of electropositive metals incapable of being smelted into metal using late 18th century technology). The term “lanthanide” also reflects a sense of elusiveness since it derives from the Greek λανθανειν (lanthanein) meaning “to lie hidden.”

These elements are in fact fairly abundant in nature, although rare as compared to the “common” earths such as lime or magnesia. Cerium is the 26th most abundant element in the earth’s crust, while neodymium is more abundant than gold and even thulium (the least common naturally-occurring lanthanide) is more abundant than iodine.

Rare earths – typically neodymium, praseodymium, dysprosium and terbium (which account for 90% of the market value of rare earths) – play an important role in electric motors, with 90% of EV models using rare earths as part of their drivetrain – the electric motors use the force produced when two magnets repel one another, causing the axle to spin rapidly and creating sufficient torque to turn the wheels. Without certain rare earths, this process would be difficult to replicate. Rare earths are also critical to the construction of wind turbines, which rely on rare earths to create the same torque-generating magnet functionality. They are also used in a wide range of other applications such as high-tech consumer products and in the production of catalysts for car exhausts. Europium, terbium and yttrium are used in energy-efficient fluorescent lighting and yttrium and scandium are used in hydrogen electrolysers.

Demand for rare earth metals is set to grow significantly

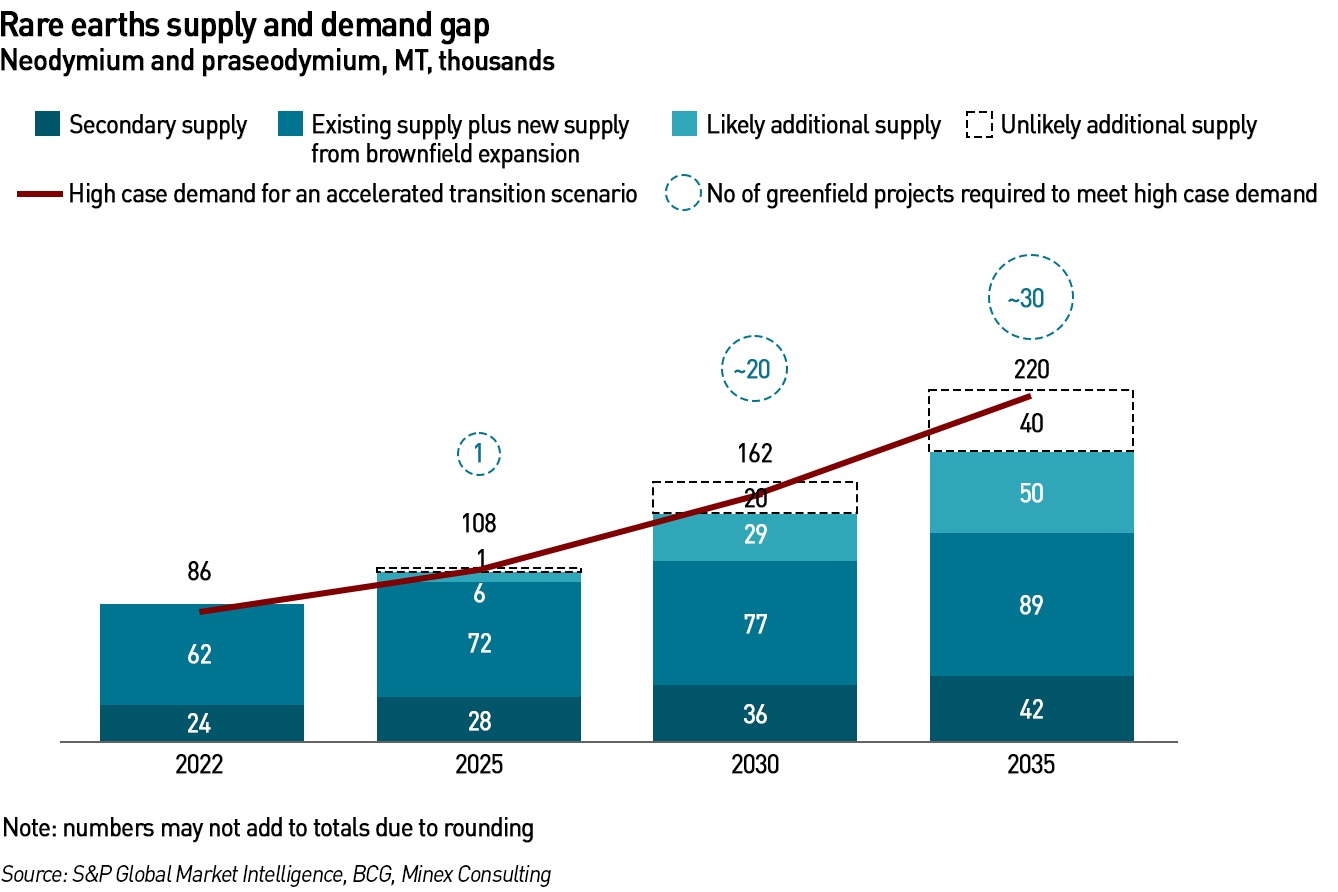

Although natural rare earth resources significantly exceed current consumption, they can be difficult to extract and separate (see below). Production was estimated at 240,000 MT in 2020. There are more than 3,000 million MT of inferred resources in the 40 largest ore exploration projects around the world, principally in hard rock deposits and clays, according to the International Renewable Energy Agency (IRENA). Demand for certain rare earths is expected to far exceed supply by 2030.

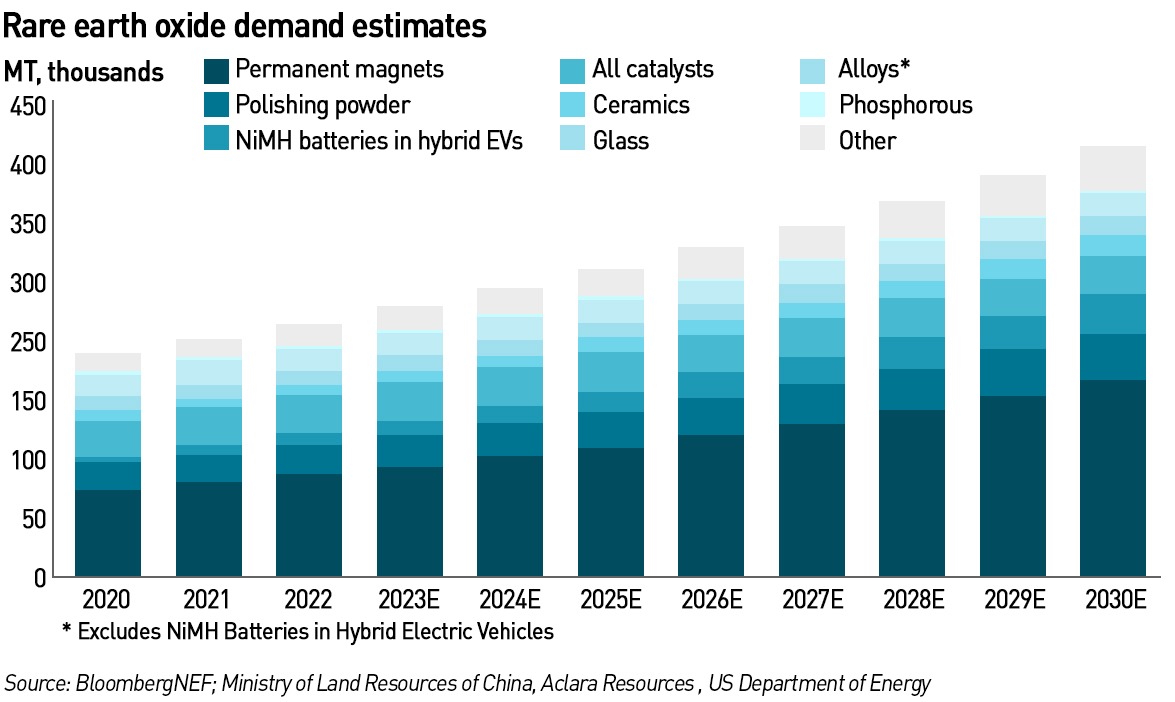

The global demand for rare earths is expected to grow from 170,000 MT in 2022 to 466,000 MT by 2035, an 8% compound annual growth rate. According to IRENA, the market for permanent magnets accounted for 34% of rare earth demand in 2019, but this is expected to reach 40% by 2030. 1 MW of direct drive wind turbine capacity requires around 500 kg of permanent magnets., with about one-third of a magnet’s weight being attributed to rare earths. In 2020, 25% of permanent magnets produced were used in transport. Approximately 2-5 kg of magnets are be used in a typical EV.

Since wind turbine capacity is expected to double between 2020 and 2050 and electromobility become the dominant road transportation option, rare earth production will need to rise by 11 to 26 times over current levels to maintain pace with 2050 global wind targets and by a factor of six to meet EV targets.

The global market for rare earths was expected to be worth US$ 9 billion in 2023, but is forecast to more than double in 10 years to US$ 21 billion, according to Project Blue, a critical metals consultancy.

Rare earth ore deposits are found all over the world, with the main ones being in China, the United States, Australia, and Russia, while other viable ore bodies are found in Canada, India, South Africa, and southeast Asia. The major minerals contained in these ore bodies are bastnasite (fluorocarbonate), monazite (phosphate), loparite, and laterite clays. About 94% of the rare earths mined in China are from bastnasite deposits, primarily at Bayan Obo, Inner Mongolia (83%), while smaller deposits are mined in the Shandong (8%) and Sichuan (3%) provinces. About 3% comes from laterite (ion absorption) clays in the Jiangxi and Guangdong provinces in southern China.

However, despite their abundance, the supply of rare earths is vulnerable since most are produced in China. As of mid-2023 the rare-earth project landscape was constrained by a lack of regional diversity, which an examination of planned projects indicates is unlikely to change. From the upstream mining of rare earths, through the midstream processing into separate oxides, to the downstream manufacture of permanent magnets and other components, most projects are located in China. There are only two non-Chinese companies active in rare earth mining, but their current capacity and recoverable reserves are limited. China accounts for 87% of rare earth processing and 91% of the manufacture of metals, alloys and neodymium-iron-boron magnets.

Extracting and purifying rare earth metals is complex and polluting

All rare earth ores contain less than 10% percent rare earth oxides and must be upgraded to around 60% before further processing. There are two primary methods for rare earth mining, both of which release toxic chemicals into the environment. The most common method involves removing topsoil and creating an open pit mine from which the ore is removed by blasting. The ore is then transported to a processing plant where a variety of separation processes can be used. The second method involves drilling holes into the ground and using polyvinyl chloride (PVC) pipes and rubber hoses to pump chemicals into the earth, with the resulting slurry pumped into leaching ponds to separate out the rare-earth metal. Sometimes these PVC pipes are left in situ once the mine closes.

Typically, rare earth ores are ground to a powder and then separated from the other materials in the ore body by various standard processes that include magnetic and/or electrostatic separation and flotation. These can be complex since the members of the rare earth family have similar chemical properties. The two main approaches are ion exchange or solvent extraction.

In the case of Mountain Pass bastnasite in California, a hot froth flotation process is used to remove the heavier products, barite and celestite, by letting them settle out while the bastnasite and other light minerals are floated off. The 60% rare earth oxide concentrate is treated with 10% hydrochloric acid to dissolve the calcite. The insoluble residue, now 70% rare earth oxide, is roasted to oxidise the cerium. After cooling, the material is leached with more hydrochloric acid to dissolve the trivalent rare earths (lanthanum, praseodymium, neodymium, samarium, europium, and gadolinium), leaving behind cerium concentrate, which is refined to various grades and marketed.

Europium can be easily separated from the other lanthanides by reducing it to divalent form, and the remaining dissolved lanthanides are separated by solvent extraction. The other bastnasite ores are treated in a similar manner, but the exact reagents and processes used vary with the other constituents found in the various ore bodies.

Monazite and xenotime ores are treated in broadly the same way. The monazite or xenotime is separated from other minerals by a combination of gravity, electromagnetic, and electrostatic techniques, and then is cracked (baked) by either the acid process or the basic process: in the acid process rare earth is treated with concentrated sulfuric acid at temperatures of 150 – 200 °C. The solution contains soluble rare-earth and thorium sulphates and phosphates. The thorium is then removed.

In the basic process, finely ground monazite or xenotime is mixed with a 70% sodium hydroxide solution and held in an autoclave at 140 – 150 °C for several hours. After the addition of water, the soluble sodium phosphate is recovered as a by-product from the insoluble boric acid, which still contains 5 – 10% thorium which is then removed either using hydrochloric acid or nitric acid.

There are several different processes of preparing the individual rare-earth metals, depending upon the metal’s melting and boiling points and the required purity for the desired application. For high-purity metals (99% and above), the calciothermic and electrolytic processes are used for the low-melting lanthanides (lanthanum, cerium, praseodymium, and neodymium), the calciothermic process for the high-melting metals (scandium, yttrium, gadolinium, terbium, dysprosium, holmium, erbium, and lutetium, and another process (the so-called lanthanothermic process) for high-vapour-pressure metals (samarium, europium, thulium, and ytterbium). All three methods are used to prepare commercial-grade metals (95–98% pure).

In the calciothermic process the rare earth oxide is converted to the fluoride by heating it with anhydrous hydrogen fluoride. The fluoride can also be made by dissolving the oxide in aqueous hydrochloric acid and then adding aqueous hydrofluoric acid to precipitate the rare earth trifluorides from the solution. The fluoride powder is mixed with calcium metal, placed in a tantalum crucible, and heated to 1,450 °C or higher, depending upon its melting point. The calcium reacts with the rare earth trifluoride to form calcium fluoride and the rare earth metal which are immiscible and allow for the separation of the metal, which is then heated in a high vacuum to above its melting point to evaporate the excess calcium. The metal may then be further purified by sublimation or distillation. This procedure is used to prepare all the rare earths except samarium, europium, thulium, and ytterbium.

There are two electrolytic methods. The first is to convert the rare earth oxide to the chloride (or fluoride) and then reduce the halide in an electrolytic cell. An electric current is passed through the cell to reduce the rare earth trifluorides to chlorine gas at the carbon anode and the liquid rare earth metal at the molybdenum or tungsten cathode. The second electrolytic process reduces the oxide directly in a molten salt of the rare earth trifluoride, lithium fluoride and calcium fluoride. Lanthanides prepared electrolytically are not as pure as those made by the calciothermic process.

In the lanthanothermic process, oxides of the rare earths being extracted (samarium, europium, thulium, and ytterbium) are mixed with fine chips of lanthanum metal and heated to 1,400 – 1,600 °C, depending on desired metal. The lanthanum metal reacts with oxide to form lanthanum oxide, and the desired metal evaporates and collects on a condenser. The four metals can be further purified by resubliming the metal.

The processing or rare earth metals is both energy intensive and requires the use of acids and other hazardous chemicals, producing significant volumes of toxic waste. Rare earth mine tailings contain processing chemicals, salts, and radioactive materials, with a high waste-to-yield ration: for every ton of rare earths that are produced, there are 2,000 tons of mine tailings, including 1 – 1.4 tons of radioactive waste. Tailings are generally stored in isolated ponds which require complex management, particularly if the tailings contain high levels of uranium or thorium. Air pollution from dusts and particulates released through blasting can cause respiratory issues and contaminate food sources as plants absorb the airborne pollutants.

Reliance on China creates environmental as well as geopolitical concerns

China has been able to establish such dominance over the rare earth industry partly due to lax environmental and labour regulations which have enabled it to produce at low cost, where western countries shied away from the environmental consequences. This has allowed them to build significant expertise in the complex separation and purification processes.

The most infamous mine in China is Bayan-Obo – the largest rare earth mine in the world. There are over 70,000 tons of radioactive thorium stored in the area, which has become a major problem since the tailing pond lacks proper lining and its contents have been seeping into groundwater. The sludge, which is currently moving at 20-30 metres per year will eventually reach the Yellow River which is a key source of drinking water. Workers also suffer from health complications due to exposure to toxic chemicals. Worker safety is not prioritised, and protective equipment is lacking, meaning workers suffer skin irritation and disruptions to their respiratory, nervous, and cardiovascular systems. Human rights abuses have been reported throughout Chinese rare earth mines.

China estimates there has been US$ 5.5 billion in damage from illegal mining that needs to be cleaned. Smaller illegal mines have been closed, and there are plans for the rest to be consolidated under six state owned mining groups which the Chinese government claims will operate to higher standards, however farmers claim they are as bad or even worse than the illegal operations, leading to protests as crops and livelihoods were harmed.

China has built a significant rare earth industry and (along with Russia) has been acquiring interests in overseas mines in recent years, particularly in Africa. Weak environmental and labour practices in Africa are allowing it to maintain its low cost production. Geopolitical competition has centred on northern and western Africa, where China and Russia are mining and processing rare earths – China is leveraging its Belt and Road initiative while Russia provides mercenaries to support various conflicts in the region. As of October 2021, Chinese banks accounted for about one-fifth of all lending to Africa, focusing on strategic or resource-rich countries, including Angola, Djibouti, Ethiopia, Kenya, and Zambia. China is also investing heavily in Latin America.

China is fully aware of its market dominance and is happy to leverage it to gain further advantages. In December, it banned exports of technologies for processing rare earths, in response to US-led restrictions on the sale of advanced computer chips to Chinese companies. Under the current US Administration, US trade restrictions relating to China have grown and now limit the ability of Chinese battery and electric vehicle producers to access US government subsidies.

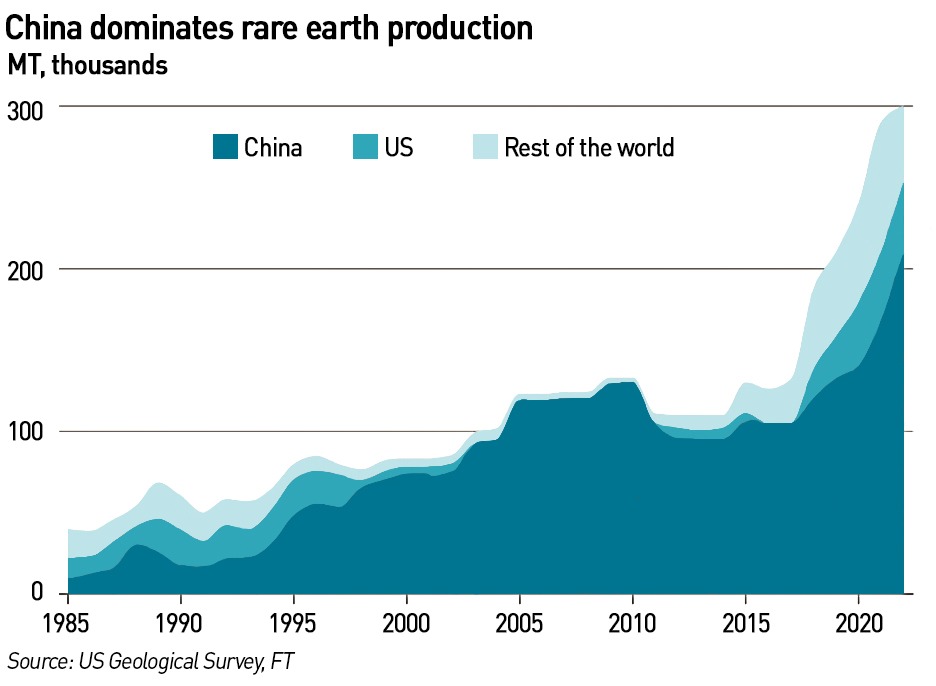

Policymakers both in the US and Europe have long been concerned about their over-dependence on China for rare earths and many of the other transition minerals and products, but while they are trying to develop their own rare earth production, this will take time. While non-Chinese production of rare earth oxides increased almost fourfold to 90,000 MT over the seven years to 2022 China has maintained its dominance, by doubling its own production to 200,000 tonnes. It generally takes more than 15 years to develop these mining projects outside China. This is leading western companies to pursue novel separation and purification processes which will have a lower environmental footprint, without adding significant cost, however there is some scepticism about whether these technologies can be successfully deployed in the timescales necessary to meet de-carbonisation targets.

Western policy-makers are under-estimating the critical mineral challenge

Over this series of posts I have set out the critical mineral challenges associated with the energy transition, and in particular ensuring a just transition. These challenges fall into five categories:

- Accessing capital and technical expertise: identifying mineral resources, accessing them through acquisitions, joint ventures and off-take agreements, and developing new mines. Mining and mineral processing is highly capital intensive;

- Reserves are geographically concentrated, often in less developed nations: many of these minerals are located in just a few countries. China has aggressively and effectively built positions of dominance in most critical mineral supply chains and is happy to leverage this position to gain wider benefits;

- Environmental and social concerns make securing a just energy transition more difficult: all extraction industries are polluting, and mining is particularly so, damaging soil, air and water, and causing loss of biodiversity, harm to food and water sources, and water stress;

- Resource nationalism and the risk of cartels: most critical minerals are located in indigenous territories and /or in under-developed countries where local populations are economically disadvantaged. In many of these places, mining is associated with human rights abuses in addition to an unequal share in the economic benefits of the mineral resources, leading to local opposition and resource nationalism;

- Trading risks: high cyclicality, low liquidity and price volatility present risks and lead to opportunities for abusive market practices such as cornering the market and short squeezes.

None of these is trivial to resolve. While progress is being made on cleaner extraction technologies, these also need to be cost competitive – even with current lax environmental and social controls, the prices of critical minerals are expected to rise due to supply and demand pressures. Against this backdrop, it will be challenging to introduce cleaner processes. The need to improve labour practices and ensure a more equitable share of the economics with indigenous communities will also challenge the finances of new projects, however failure to do so risks increasing resource nationalism and the sorts of protests seen recently in South America.

As I set out at the start of this series, there are trade-offs involved that have barely begun to be addressed. Is the climate emergency such that other environmental harms should be overlooked? And who gets to decide this? While inhabitants of low-lying islands complain about lack of progress addressing climate change, inhabitants of resource-rich countries are forcing mine closures in protest at poor environmental practices and inequitable shares of the economic benefits of their resources. It is not really in the gift of western governments to determine how these trade-off should be resolved, however they cannot be ignored.

The solution is to develop cleaner and fairer ways of extraction, but this is far easier said than done. Simply removing ores from the ground is environmentally harmful, even if better processing approaches can be found. Another solution is to increase recycling, but this can be technically challenging and expensive.

Realistically, policy-makers need to start considering a different set of trade-offs relating to the speed and nature of the energy transitions they want to undertake. Resources, both financial and mineral, need to be optimised. One solution would be to re-think the approach to intermittent renewables. The decision to build wind-farms is a decision to order huge amounts of copper, aluminium, rare earths and other minerals in the wind farm itself (plus energy intensive concrete and steel), but also large amounts of new grid infrastructure, and batteries or other forms of generation to provide energy when the wind isn’t blowing. This means building a lot more capacity than is actually needed, all of which sucks up resources.

Then there is also the impact of electrification, particularly in the transport sector. Not only do electric cars require significantly more minerals than conventional cars, they also require a lot of energy to produce. An EV must typically be driven over 10,000 miles before it breaks even in terms of emissions with a conventional car (depending on the source of elecricity used for charging). For some drivers this would take years. Policy-makers should question whether this is really the best approach, or whether people whose mileage is low should drive a petrol car instead. Scrapping functioning cars is wasteful, and given the resourcing challenges of electric cars, it may not be sensible.

These are hard choices for policy-makers to face, particularly after announcing such ambitious net zero targets. But those targets seem to be slipping out of reach. Their economic cost, and questions over public acceptance of those costs, is increasingly being questioned by voters. Courageous choices need to be made. And sensible choices would recognise for example that burning gas tends to be cleaner than burning coal or oil, and that all forms of waste should be minimised. This not only means not prematurely scrapping equipment, but also reducing heat losses through comprehensive insulation schemes. Hybrid solutions should be explored, for example heating systems that combine heat pumps with gas boilers.

Arguably the large-scale use of lithium-ion batteries should be paused until cleaner and cheaper battery technologies are developed. But better yet, other forms of energy storage should be found – thermal technologies show promise and should be developed further for static applications.

The current approach to the energy transition means building an awful lot of “stuff”, all of which has to be paid for, and most of which involves huge quantities of things that have to be dug out of the ground and transformed into usable forms typically using lots of dangerous chemicals and large amounts of heat. And if not managed properly, this approach will be very expensive and potentially ineffective leading to energy insecurity, inadequate comfort levels and a worse quality of life. None of which sounds very sustainable.

Critical minerals series

Following on from my post about the need to secure critical minerals for the energy transition, in this post I look at copper and aluminium…

Following on from my post about the need to secure critical minerals for the energy transition, in this post I look at copper and aluminium…

Continuing my series on critical minerals, in this post I will look at some of the main metals required for lithium-ion batteries: lithium, cobalt and nickel…

In this next post in my series on the critical minerals required for the energy transition, I look at graphite and manganese….

A great series of posts, Kathryn. Shame that few of the people who need to read it will. As to your final sentence, current policy simply isn’t sustainable, which means it won’t be sustained. The question is, how much economic, environmental and social damage will be caused before the wheels fall off the Green revolution?

Thanks Vernon! I spent most of Christmas working on it, but it was interesting to go through each element and see what the challenges are. I think it makes pretty sobering reading….

These are very well written articles about all the materials needed, and just goes to prove that insulation of properties, increasing energy efficiency and material efficiency are all going to be critical to maintain standards of living……..oil and gas running out (or getting risky to use/more expensive), and supply of critical materials limited (also getting more expensive).

If we can get a house down from 15,000 kwh heating requirement down to 2,000 kwh……Passivhaus standard, and introduce rationing to prevent rich people from taking all the mineral and energy wealth, perhaps we won’t need these quantities in these projections, but obviously once supply rate is limited there will be rationing (self-rationing based on price). To maintain current energy use structure and current inefficiencies, or the increasing inefficiency of the richest people on the planet, there are going to be some severe price shocks in a few years time when supplies get limited because of the demand.

More Oil and Gas isn’t the answer, efficiency is. Not just energy efficiency, but material efficiency as well……..you’ll see…….it’s a basic economic driver, where for higher profit, greater efficiency is needed in industries subject to competition, or for people on low wages the highest efficiency of living is needed, where you see people living in tents or their cars because of economic pressures already present.

The Green Revolution is possible, economically viable and necessary, but people still don’t understand all that it will entail. Limited supplies of certain raw materials…….inevitable.

Thanks, Kathryn, for an excellent series of articles. Unfortunately, dim-witted politicians and journalists persist in adding ‘clean’ and ‘cheap’ to any reference to renewables, despite the evidence to the contrary which you so clearly explain. Sound bites carry more weight than well-reasoned explanations, which is both sad and dangerous.

cheap. I guess that depends on what you think the alternatives are. Nuclear does not feel cheap to me if you take the whole system and cycle from extraction, transformation, delivery and then medium and long therm disposal of waste.

clean. I agree environmental damage beyond our shores is being ignored