There has been mixed news on the subject of ESG (Environmental, Social and Governance) investing recently, and I have a sense there is something of, if not a backlash, then a re-adjustment in how such investing is being viewed. Up until a year ago, ESG was all the rage, and while there are still stories of organisations such as universities being pressured to divest things like fossil fuel investments, there has also been a change of tone, not least from the oil majors such as Shell and BP which appear to have decided there is a lot of money still to be made in oil and gas production and they may as well stick to their knitting and make it while they can.

This is in fact not only rational but desirable. Markets do not typically reward diversification at the corporate level – investors prefer to do this themselves and assume that companies are better off sticking to what they do well. Oil majors do oil and gas well, they do not necessarily do other things well, and nor should they, unless there are clear synergies.

While some believe the market is growing, others disagree

Back in October, PwC said that global asset managers were expected to increase their ESG-related assets under management to US$ 33.9 trillion by 2026, up from US$ 18.4 trillion in 2021, saying that the projected compound annual growth rate (“CAGR”) of ESG assets of 12.9% meant they are likely to constitute 21.5% of total global assets under management in less than 5 years. Under PwC’s base-case growth scenario, ESG-oriented assets in the US (the largest market) would more than double from US$ 4.5 trillion in 2021 to US$ 10.5 trillion in 2026; in Europe (up 172% in 2021) they would increase 53% to US$ 19.6 trillion, while in Asia-Pacific ESG assets were expected to more than triple, reaching US$ 3.3 trillion in 2026. However, on a global basis, ESG funds still only account for a small portion of total assets under management, which reached US$ 126 trillion in 2022.

PwC also found that nine out of ten asset managers surveyed believed that integrating ESG into their investment strategies would improve overall returns, and 60% of institutional investors reported that ESG investing already had resulted in higher performance yields, compared to non-ESG equivalents. As a result, 78% of investors surveyed were willing to pay higher fees for ESG funds, although higher fees were seen as necessary to cover increasing ESG compliance costs. Three-quarters of investors considered ESG to be part of their fiduciary duties, although the extent to which this overrode financial return varied across firms.

“ESG has become perhaps the most powerful driver of growth in asset and wealth management. The surge in demand for ESG investments highlighted in our survey exceeds almost all previous expectations. With the current economic headwinds, we have seen some correction in asset prices and there is a risk of significant contraction in capital markets that would result in a further decline. This underlines the importance for asset managers and institutional investors alike to understand how to capture the shift to ESG as a counter-balance to potential portfolio underperformance as well as legacy product obsolescence,”

– Olwyn Alexander, PwC Global Asset & Wealth Management Leader, PwC Ireland

However, less than half of the managers surveyed said they were planning to launch new ESG funds – instead their immediate priority was converting existing products so they can be labelled as ESG-oriented. Almost three quarters of institutional investors and over eight in ten asset managers said mis-labelling is prevalent in the industry, with many calling for better regulation and improved disclosure rules for listed companies.

Although the Investment Association says there has been a net outflow in sales of retail investment funds in the UK, a Deloitte survey found that 84% of ESG investors it surveyed have either maintained or increased their proportion of ESG assets since the start of pandemic. Make My Money Matter reported that, as of November 2022, around £1.3 trillion of UK pension money (out of around £3 trillion) was managed in a way that is committed to a net zero future.

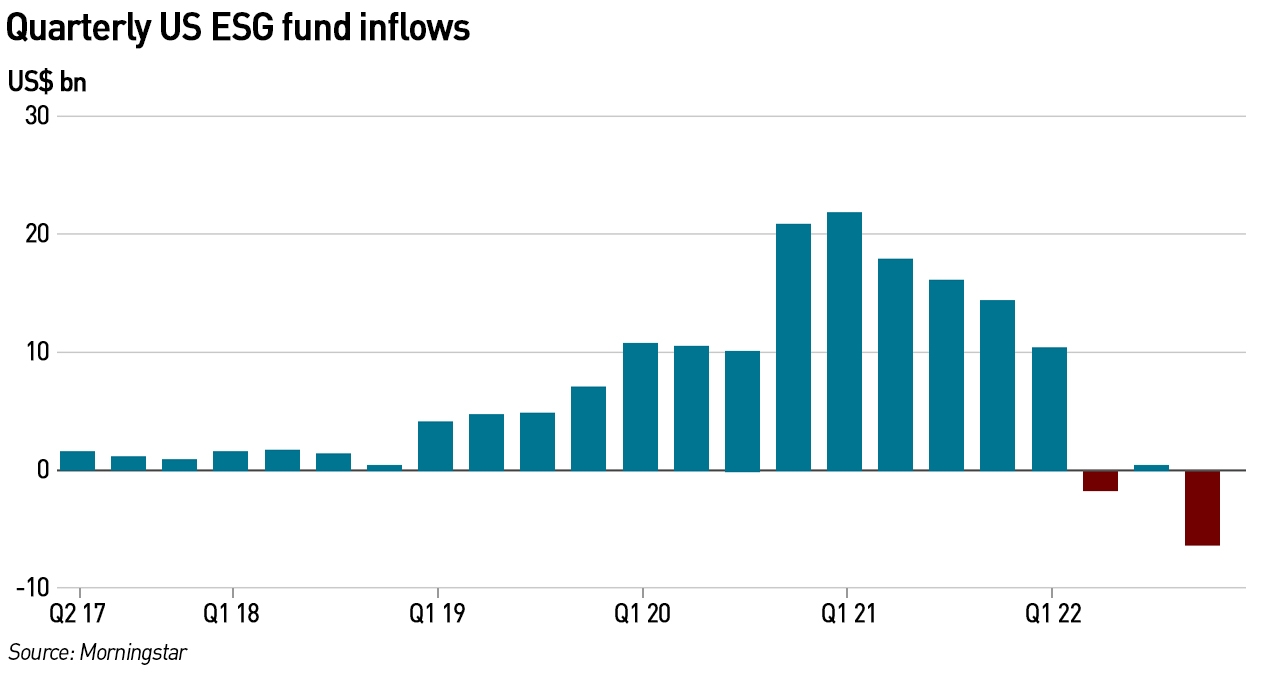

But these positive attitudes bely a recent shift in behaviour. According to tax advisory firm Buzzacott, sustainable investing, while “still growing in popularity” has experienced a two-year decline in net inflows from its peak, with energy security, political concerns, recent performance and green-washing deterring investors. It cites data from Morningstar showing that global sustainable funds attracted around US$ 29 billion of net new money in Q1 2023, down from US$ 38 billion the previous quarter and a peak of over US$ 180 billion in Q1 2021.

“It’s been a rough year for funds that focus on environmental, social and governance factors, or ESG. Adverse politics, performance and product design have all weighed on the sector. Once again, investors have learnt the hard way that investing by acronym is never an enduring way to allocate capital. Many ESG funds suffered a roughly 3 to 4 percentage point underperformance compared with broad equity markets in 2022, according to Oliver Wyman analysis,”

– Huw van Steenis, vice-chair at Oliver Wyman

The recent underperformance of sustainable funds against the wider market has not helped, something that may well continue to be a challenge due to current macro-economic conditions and the ongoing energy crisis. ESG fund performance has suffered from high fossil fuel prices as sustainable funds tend to be underweighted in conventional energy stocks. Total assets under management in ESG funds fell by about US$ 163.2 billion globally during Q1 2023 from the year before, according to fund benchmarking firm Lipper. In March alone, total assets under management in the responsible investments fund market fell by US$ 6.8 billion.

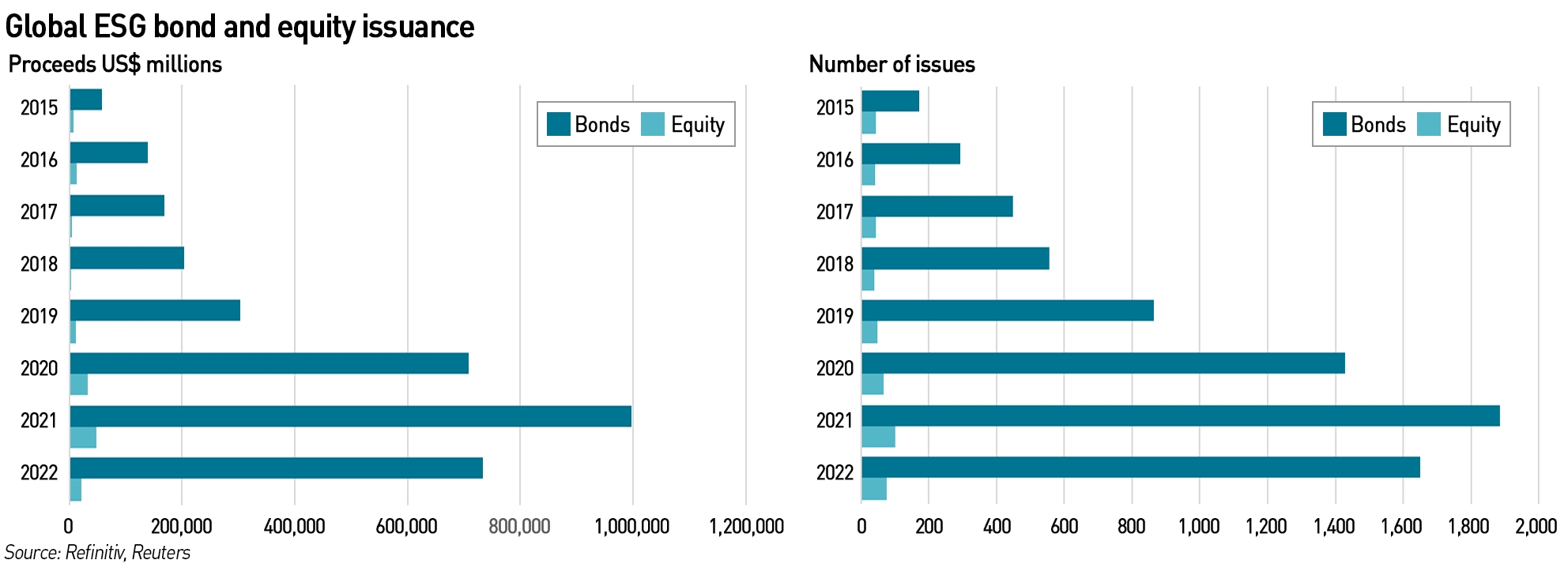

New issuance is also slowing with both green bonds and equity issuance from sustainable sectors such as renewable energy, electric vehicles and organic farming falling sharply in 2022 compared with the previous year.

ESG investing is declining particularly steeply in the US, where concerns over green-washing and “woke capitalism” have seen an increasing politicisation of the subject. Research by Morningstar also found flows into so called anti-ESG funds to be growing, peaking at US$ 376 million during Q3 2022, more than five times the previous quarterly record. One of the best-known funds, the Strive US Energy ETF accounted for the bulk of the flows at over US$ 300 million in the month after it launched last August.

A lack of standardisation has exacerbated concerns over green-washing, with regulatory actions drawing further negative attention. In May 2022, German police raided the offices of fund manager DWS, a subsidiary of Deutsche Bank, over allegations of green-washing. The company subsequently set aside €21 million in anticipation of fines. In November last year, Goldman Sachs agreed to pay a US$ 4 million penalty to settle charges brought by the US Securities and Exchange Commission for policy and procedural failures in its ESG research.

In addition, recent research by Scientific Beta, an index provider and consultancy, shows that companies rated highly on widely accepted ESG metrics pollute just as much as poorly rated counterparts. This lack of correlation holds even if companies’ carbon intensity (carbon emissions per unit of revenue or market capitalisation) is compared purely to their environmental rating.

“ESG ratings have little to no relation to carbon intensity, even when considering only the environmental pillar of these ratings. It doesn’t seem that people have actually looked at [the correlations]. They are surprisingly low. The carbon intensity reduction of green [ie low carbon intensity] portfolios can be effectively cancelled out by adding ESG objectives,”

– Felix Goltz, research director at Scientific Beta

The study examined 25 different ESG scores from three major providers: Moody’s, MSCI and Refinitiv, and found that 92% of the reduction in carbon intensity investors gained by solely weighting stocks for their carbon intensity was lost when ESG scores are added as a partial weight determinant. Even just using environmental scores, rather than the whole range of ESG metrices, “leads to a substantial deterioration in green performance”. Mixing social or governance ratings with carbon intensity typically resulted in portfolios that were less green than the comparable market capitalisation-weighted index.

“[There is a] perception that ESG assessments do something that they do not. ESG assessments are an aggregate product, their nature is that they are looking at a range of material factors, so drawing a correlation to one factor is always going to be difficult…In 2015-16, post the SDGs [UN sustainable development goals] and COP21 [Paris Agreement], when people began to really focus on the issue of climate, they quickly realised that an ESG assessment is not going to be much use there and that they need the right tool for the right task. There are now more targeted tools available that look at just carbon intensity, for example,”

– Keeran Beeharee, vice-president for ESG outreach and research at Moody’s

The research showed that the correlation between ESG scores and carbon intensity was close to zero (4%). This could be because a company with high emissions might be good at governance or ave high have high employee satisfaction. Even the environmental pillar had low correlation to carbon emissions since it could be determined by factors such as a company’s use of water resources and waste management practices.

Attitudes to ESG investing are evolving but further change is needed

The recent under-performance of ESG funds has led investors to undertake a review of the investment attributes of ESG portfolios, and are finding that many have been poorly constructed and are overly simplistic. The breadth of ESG metrics can produce counter-intuitive results, as outlined above, and there are questions about moral equivalence – tobacco companies are generally excluded from any form of ESG investing, for obvious reasons – it is hard to identify any benefit from the production of cigarettes – but investors remain content to fund businesses producing highly processed foods linked to a wide range of diseases. There are also questions about reach – if a fossil fuel production business is to be shunned, then what about the companies providing services to such businesses, not just operationally but corporate services such as accounting and software? Should they also be shunned?

The ongoing war in Ukraine has led investors to reconsider investments in both the energy and weapons sectors. Where previously investors had shied away from weapons firms, there has been a shift in sentiment in recognition of the need to support Ukraine in the face of Russian aggression, while the social hardship resulting from the high prices caused by the reduction in Russian gas imports to Europe has prompted a re-think about attitudes towards conventional energy companies.

In recent years, activists targeted organisations and events which receive sponsorship from producers of fossil fuels – one example was author and climate activist Michaela Loach who walked out of the Edinburgh international book festival in protest at its receipt of sponsorship from Baillie Gifford, and investment management firm that continues to invest in fossil fuel production. However, Loach travels all over the world as part of her activism, relying on those self same fossil fuels to do so, despite the fact that air travel is the single most polluting activity an individual can engage in.

“…moral high grounds invariably crumble — mostly due to changes in scientific knowledge, attitudes, money or politics. Even Joe Biden demanded that big oil companies in America get pumping when rising fuel prices risked three congressional elections last year…”

– Stuart Kirk, writing in the Financial Times

Policy-makers have re-discovered the need to focus on energy security, creating a headache for investors: having previously pulled back from financing new oil and gas production they now face either missing out on lucrative new projects or having to reverse previous strategies. The reality is that the need for fossil fuels is not going away, and since energy security is essential for not just economic performance but also social welfare, investors are having to adjust to new these realities. The recent out-performance of conventional energy businesses at a time when the renewable energy sector is facing challenges further adds to these difficulties.

The first phase of climate-aware investing was largely to avoid polluters, something which led to perverse outcomes for example failure to invest in emissions reductions which could be achieved by switching from dirty solid fuels to cleaner natural gas. It also meant ignoring large swathes of the economy in developing investment strategies since greenhouse gas emissions are highly concentrated in a few key equity sectors that make up about a third of the public equity market and account for about 90% of public company emissions and about 60% of all global emissions, according to Bridgewater Associates.

In response to recent changes, investors are increasingly interested in so-called “carbon improvers” — firms that are progressively reducing their emissions footprint while still generating financial returns. The next generation of climate-aware indices focus on forward-looking measures of de-carbonisation, such as the new MSCI Climate Action Index, launched in late 2022, which includes estimates of future reduction in emissions. There is growing interest in capturing value from investing in companies enabling a faster transition.

“We know that the transition will not be a straight line. Different countries and industries will move at different speeds, and oil and gas will play a vital role in meeting global energy demands through that journey,”

– Larry Fink, CEO Blackrock

There is a growing recognition that the approach to ESG investing needs to evolve. In his 2022 letter to investors, Blackrock chief executive Larry Fink wrote extensively about the transition to net zero, emphasising the risks businesses will face from climate change and the impact of transition policies. This year the tone was more nuanced, recognising that oil and gas would contibue to play a major role and making a distinction between near-term and longer-term factors, the implication being that the the energy transition and impact of climate change fall into the latter category.

While he correctly identifies the insurance implications of changing weather patterns, he also mentions wildfires which are more likely a result of less effective land management practices than climate change – activists persuaded policy-makers that controlled burning in the cold season was harmful to the environment leading to major build-ups of undergrowth fuelling uncontrolled fires in the hot season. Arson was also a major factor. Interestingly Fink also mentions the implications of polutation migration for example people moving away from coastal zones to avoid flooding, but does not mention other large-scale migration such as the movement of people away from California in response to high housing costs and rising crime. While investor attitudes to ESG may be starting to change, there is still some way to go before they can claim to be genuinely coherent and effective.

Three steps for cleaning up ESG investing

First of all, the primary aim of investors is to generate returns, and it is difficult to defend the under-performance of ESG funds compared with conventional investment strategies. As noted earlier, simply avoiding polluting firms means avoiding investing in some of the world’s largest companies. Not only is this likely to be un-sustainable as a financial strategy, it also to a certain extent misses the point, because some firms are incorrectly identified as polluters when in fact it is their customers who are responsible. This is particularly the case for oil and gas producers whose emissions are dwarfed by the emissions of their customers.

Secondly, issues of green-washing need to be resolved. This results in ESG investing experiencing the worst of all worlds – lower financial returns as well as lower social benefits since the benefits the investors believe they are supporting fail to materialise. While the introduction of stricter regulation should mitigate some of these effects, they add friction to the market since they are complex and compliance is expensive. A more prescriptive environment is emerging, but this encourages the gaming of loopholes. Unfortunately a principles-based approach would also be difficult to implement since it is very difficult to define generic objectives and criteria for such a broad subject.

It is also unfortunately the case that in order to support ESG investing, reporting requirements for companies are growing ever more onerous and expensive. The cost of producing annual reports, which typically run in to hundreds of pages, is a growing problem for listed companies. At 147,000 words or 237 pages, the average FTSE-100 annual report is longer than epic novels such as A Tale of Two Cities having increased by 46% in the past five years. The average report is adding 5,800 words and nearly eight pages every year. Even smaller listed companies face similar reporting obligations, which can be very expensive to meet. Reporting reform and standardisation should take account of the costs of compliance.

Thirdly, investors need to be more sophisticated in their understanding of what “good” looks like. While standards and standardisation designed to address green-washing will do some of the leg-work, this cannot replace the need for investors to do their own work in defining an investment strategy that achieves a clear and achievable set of desirable aims.

This historic polluter-avoidance strategy has other flaws, since it fails to provide funds which could reduce emissions for example companies such as Equinor have invested heavily in making their production facilities greener. It also ignores the fact that fossil fuels are used widely for things other than energy and that viable alternatives are yet to be developed. Starving these sectors of funding will simply increase prices, harming large segments of society as everyday goods become more expensive, without reducing their environmental impact. Indeed, by failing to support emissions reductions which require investment, they entrench existing means of doing business.

How should ESG investing evolve to better meet the needs of investors?

In a recent post, I described the statutory duties of company directors to maximise the benefits that accrue to shareholders. In a perfect world, “doing good” would be more profitable than “doing bad” but in the real world, not only is this not necessarily the case (the wealth that can be achieved from various illegal activities being a case in point) it is hard to define what is meant by “good” – as highlighted by the changing attitudes to defence stocks in light of the Ukraine war.

However, investors are not the same as company directors, and while fund managers have fiduciary duties to their clients, it is reasonable for people to apply a wide range of criteria to investing their own money (and by extension the money of their clients, in accordance with investment directives). The directors of a company that makes widgets should maximise profits from widget-making, and should not try to expand into unrelated sectors if widget-making is considered environmentally or socially harmful. Investors on the other hand might prefer an alternative to widgets and can provide funds to companies developing such alternatives – even if the widget company is highly profitable, investors are entitled to prefer a less profitable alternative as long as they are making an informed choice (or the asset manager/ investment fund has clearly explained its strategy).

There is nothing inherently wrong with considering a wider set of criteria than simple financial performance when investing, but establishing those criteria in a way that actually provides real-world benefits is much harder to do than to say. From an environmental and sustainability perspective, I have long complained about a narrow-minded focus on carbon dioxide both from policy-makers and the investing community. Such a focus risks the creation of other harms, notably major increases in other types of environmental pollution as a result of the massive increase in mining that will be needed to deliver the minerals required for the energy transition. I have particular concerns about the push for electric cars in this regard since their resource requirements are materially larger than for conventional cars, and tens of thousands of miles must be driven to make up for the higher energy intensity, and therefore emissions, from their production processes. Other concerns relate to the destruction of habitats and reduced biodiversity arising from biomass fuel production.

It is good that investors are waking up to these issues (although recent ESG underperformance is likely a large motivator for this change), but the question is where should they go from here? In order to achieve the objectives of ESG investing, I think a split approach is needed where all businesses have a generic “good corporate citizen” score which would be around treating staff, suppliers and customers well, having appropriate waste management policies, and so on, and then for fund managers to develop strategies around particular topics.

For example, a “net zero enabling” portfolio would include companies with a high good corporate citizen score, that operate in businesses that promote net zero, such as wind turbine manufacture, clean storage development and so on. A similar approach could be taken to “carbon improvement” where the portfolio would include companies developing carbon removal or reduction technologies, which might be carbon capture and storage, but also companies making lower emission vehicles such as trains, trucks or diggers.

In other words, the ESG world would become more granular with funds homing in on specific objectives, while ensuring those objectives are met in a socially responsible way. The means of determining the “good corporate citizen” score needs to be reasonable and not impose excessive reporting burdens on companies, and there should be a degree of choice over compliance, whereby listed companies can decide for themselves whether they want to produce the information needed for them to be included in particular types of indices or portfolios in order to keep costs down. If producing this material has a share price benefit as investors seek out such companies, it will provide its own incentive for engaging.

The first phase of ESG investing is coming to an end. Now is an ideal time for investors and businesses to collaborate on the next stage, ensuring a balance between meaningful social objectives, regulations to avoid green-washing, and a balanced approach to reporting with costs that are reasonable.

This is an excellent summary of the current ESG mess and it’s a timely warning to all investors.

Younger people in general are becoming worried about the double whammy of insecure and under-performing pension plans combined with stagflation; the demographic shift to an older global population and the cost of living when there are insufficient taxes to fund state healthcare. They will blame these ESG market players for their green-washing and inability to see that choosing expensive unreliable and under-performing energy technologies can only ever destroy living standards while adding costs to business, industry, research and the development of new, possibly transformative, technologies. The youth of today will pay the price of unreal and failed Net Zero investment strategies advocated by politicians and activists who have lied about the astronomical costs to society of trying to get to Net Zero.

It’s very unlikely that Global Net Zero will be achieved this century, the only question in my mind is will Western democracy survive our attempt to achieve it.

ESG is a scam, designed to allow companies like BlackRock to charge higher fees without having to deliver higher returns.

If a company’s business model is unsustainable then, by definition, after a period of time those activities will cease. Why would anyone invest in a company without a sustainable business? ESG is a solution to a problem that doesn’t exist.

There are definitely some bad actors just looking for an excuse to charge higher fees (although I wouldn’t put Blackrock in that category). I think most ESG arose in response to the behaviour of activist investors, but it has been done in a muddled way that has created a lot of unintended consequences. I think it’s fair enough for people to want to use their money to “do good” /”avoid bad”….I do this myself by trying to avoid buying clothes made in China because of concerns over the use of forced labour and the difficulty in gaining confidence supply chains are ethical. ESG investing can be seen as the investment equivalent to addressing those types of concerns.

The purpose of ESG is to rewire the financial system for net zero. That is, to destroy it and replace it at best by politically controlled digital currency. Whether that is workable without causing a revolution is a gamble taken by its high priests who would surely be first on the gibbets.

In the shorter term it is an attempt to rig markets by debanking businesses it disapproves of and granting exclusive royal warrants to those it considers worthy. It is running into the reality that its programme produces an undesirable slowly collapsing economy, and that the market is fighting back, awarding superior returns to businesses ESG wants to strangle, while its favoured sons head towards oblivion.

If the totalitarians secure a victory the next generations face an unappetising future until they manage the overthrow. Best that it is achieved quietly and soon, and without fuss.

I think this strategy will be significantly stimied by the Farage scandal. The current Conservative Government is not on board with this trend and having woken up to the issue it is busy legislating and directing the FCA to force a change in direction. Just today there’s talk of legislating to protect people’s access to cash. I think we may well have cause to be grateful to those people at Coutts who decided it was OK to de-bank Farage – that one act of over-reach has exposed the system and caused people to question it.

ESG is run like a Mafia protection racket to ensure compliance and is designed to destroy the economies of western democracies by sabotaging their access to cheap and abundant energy and by replacing meritocracy with diversity.

That the reason given, that of CAGW (now CAGB), is completely false is evidenced by the fact that no activists have an issue with non-western countries emitting vast quantities of CO2 and that nuclear, the only low CO2 emitting energy source which is affordable, reliable and secure is ignored, and even in some western countries, being closed down.