Eighteen months ago I wrote a blog entitled: Cakism in energy policy begins to bite which gained a lot of attention, in which I pointed out that policy-makers tend to want to have their cake and eat it when it comes to energy policy. I cited the example of US President Joe Biden, who once told a young woman: “I want you to look at my eyes. I guarantee you. I guarantee you. We’re going to end fossil fuel.” but later, when gasoline prices rose on the back of refinery capacity reductions, threatened to use emergency powers if oil companies didn’t increase supply in response to high prices, telling them:

“You need to work with my Administration to bring forward concrete, near-term solutions that address the crisis and respect the critical equities of energy workers and fence-line communities….in advance of that, I request that you provide the Secretary with an explanation of any reduction in your refining capacity since 2020…”

– Joe Biden, President of the United States of America

I still don’t know what “critical equities of energy workers and fence-line communities” are, but the meaning was clear – and not at all consistent with “ending” fossil fuels.

Now we have another refinery crisis, this time in Scotland with the potential closure of refinery activities at Grangemouth, which is set to be converted to a fuel import terminal in 2025, and a governing party, this time the Scottish National Party (“SNP”) which similarly wants to move away from fossil fuels, saying it is proud to have “the most ambitious legal framework for emissions reduction in the world”. It intends to reach net zero by 2045.

So, one would expect the SNP to be delighted to see the closure of Grangemouth, after all just a few months ago, the SNP opposed the provision of a drilling licence for the Rosebank oilfield in the North Sea, with First Minister Humza Yousaf describing the award as the “wrong decision”. In a recent speech he said Scotland was “collectively guilty of catastrophic negligence” by remaining a major oil producer. But the closure will cost many jobs and threatens both the country’s energy security and the viability of the Acorn carbon capture project, since in ending its refinery operations, Grangemouth will emit much less carbon dioxide on site.

Grangemouth just transition plan delayed to the point of being pointless

The SNP is widely seen as being paralysed by its coalition with the Green Party, which opposes both fossil fuel use and carbon capture. It has dithered in bringing forward its draft energy strategy and just transition plan, which is now delayed until next summer. Grangemouth is to have its own dedicated plan, being “ideally placed to produce future products in a net zero economy”.

The Scottish Government’s energy strategy states that there is significant potential for carbon-intensive industrial clusters, such as Grangemouth and Mossmorran, to unlock deeper de-carbonisation across Scotland.

“In particular, Grangemouth’s wealth of investment, infrastructure, skills, knowledge and productivity has strong potential for supporting a net zero economy… Given the critical role of Grangemouth, both for our economy and our climate change targets, it is our ambition to see the site remain not only a key manufacturing base for the future, but also one that is significantly decarbonised, supporting further carbon reduction across Scotland,”

– Scottish Government Draft Energy Strategy and Just Transition Plan

The just transition plan for Grangemouth is expected to be finalised by the end of the year, and will include “baseline mapping” of the state of the cluster as it stands today, as well as a “future vision” for 2045. A draft plan is then set to be published for a consultation in the spring of 2024. However, the Scottish Government has been criticised for not delivering the just transition plan for Grangemouth sooner. In fact, far from being “just” the energy transition in Scotland appears reactive and chaotic, and even the SNPs own expert advisors have apparently compared the potential job losses at Grangemouth to the loss of industry jobs under Margaret Thatcher, which given the extent to which Mrs Thatcher was abhorred by the SNP, is some criticism.

The delays in developing the just transition plan for Grangemouth risks making it moot. If the company moves away from refining to pure fuel import, its emissions will fall dramatically.

Grangemouth set to end refinery operations and become an import terminal

Built in 1924, Grangemouth is one of just six refineries in the UK and the only one in Scotland that processes crude oil, often produced in the North Sea, turning it into fuels such as gasoline and diesel. It has a refining capacity of 150,000 barrels per day and employs around 2,000 people and up to 7,000 contractors. Grangemouth is owned and operated by Petroineos, a joint venture between Ineos and PetroChina, and accounts for about 4% of Scottish GDP.

The plant produces a range of refined products:

- Ethylene – intermediate (building block) used in the manufacture of the plastic: polyethylene (on site) and other chemicals in the petrochemical industry (eg emulsion paint, car fuel tanks, resins, adhesives)

- Propylene – intermediate (building block) used to manufacture, for example, the plastic: polypropylene (on site)

- Polyethylene – typical applications include plastic bottles (milk, shampoo), wrappers, food film etc

- Polypropylene – carpets, carpet backing, DVD cases, cabling, water pipes etc

- Ethanol – used in the pharmaceutical industry in the manufacturing process as a solvent

- LPG – for example camping gas

- Gasoline (petrol) – fuelling vehicles

- Jet fuel – aviation

- Home heating oil

- Diesel – fuelling vehicles

After the mid-1970s, the development of North Sea oil enabled Grangemouth to take crude through the Forties Pipeline giving access to the very oils used in setting Brent crude prices, giving the plant an advantage over other refineries. In addition to receiving piped crude through the Forties Pipeline, Grangemouth imports other crudes, notably from West Africa, via its deepwater terminal.

Originally Brent crude prices were set by the Brent field, but in 1984 as production from the field peaked, the output of other fields was added, initially from the nearby Ninian field in 1990. Forties and Oseberg were added in 2002, followed by Ekofisk in 2007 and more recently Troll in January 2018, together known as “BFOET”. The Forties stream alone is a blend of crudes flowing from 70 different fields, including the sour Buzzard stream. Being lower in quality, Forties is in theory the cheapest grade to deliver. Since the cheapest BFOET cargo traded in the 4 pm – 4:30 pm London trading window sets the price of dated Brent, Forties typically sets Brent spot prices. (Dated Brent is the basis for pricing spot brent cargoes – the term “Dated Brent” refers to physical cargoes of crude oil in the North Sea that have been assigned specific delivery dates.)

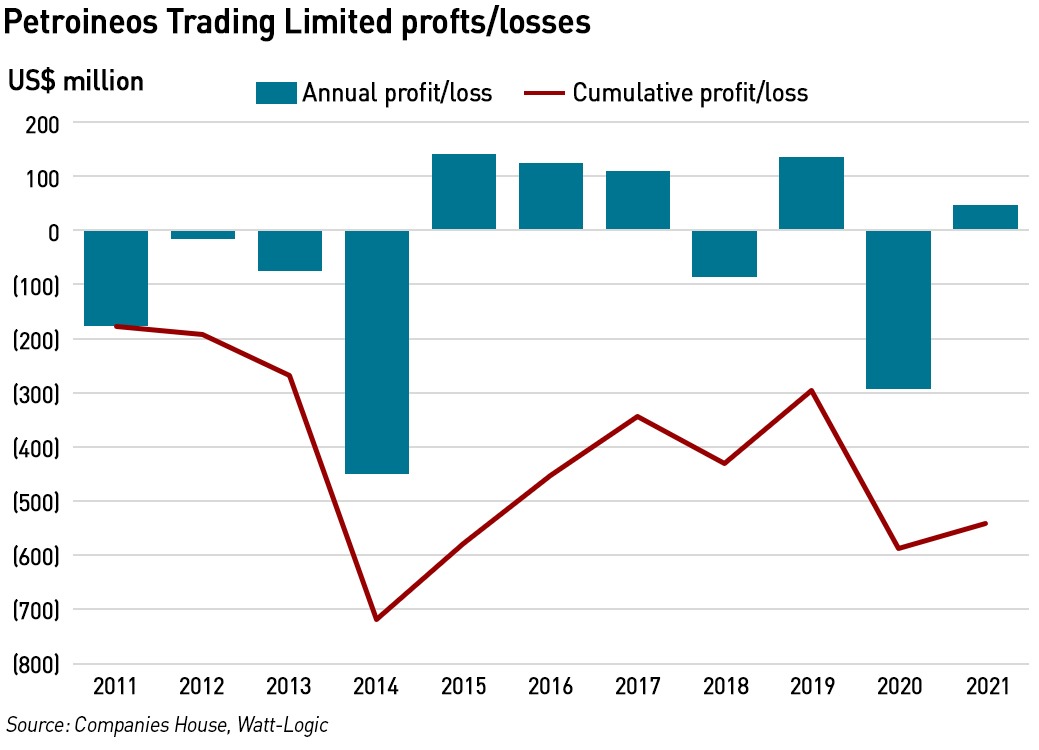

Despite its locational benefits, the refining business has not performed particularly well. Petroineos Trading Limited which owns both Grangemouth and the Lavera refinery in France lost over US$ 0.5 billion between 2011 and 2021 (the most recent available financial statements), driven by particularly bad years in 2014 and 2020. The accounts do not separate out the two businesses, but it appears that the Lavera accounts for about 60% of the financial performance and Grangemouth about 40%.

During the pandemic, Grangemouth, like many other European refineries, mothballed some fuel-processing units, due to lack of profitability. In November 2020, Petroineos announced the mothballing of the oldest of the three crude oil distillation units, and its fluid catalytic cracking unit, both of which had been shut down since the start of the pandemic. This was accompanied by the loss of up to 200 jobs and reduced the plant’s capacity to its current level of 150,000 bbl /day, from 210,000 bbl /day. At the time, Petroineos blamed this restructuring on the reduction in demand for road and jet fuels – a direct result of the pandemic – along with a gradual long-term increase in the electrification of road vehicles, and a decreased reliance on fossil fuels.

In November 2021, Petroineos shut the hydrocracking unit at Grangemouth. A hydrocracker converts vacuum gasoil (“VGO”) primarily into regular gasoil, which is typically de-sulphurised to produce diesel, although the unit also produces kerosine, naphtha and fuel oil. European hydrocracker units had become increasingly expensive to run as natural gas prices increased from September 2021 onwards having a knock-on effect on hydrogen costs – hydrogen is injected during the hydrocracking process. This closure came just a month after TotalEnergies closed the hydrocracker at its 310,000 bbl /day Antwerp refinery, and a host of other European refinery capacity reductions.

“At the start of the year we did our [regular] analysis on closure risk, and didn’t see a high risk of closure in the near term,” he says. “But in April, the hydrocracker unit which produces a lot of diesel went offline and hasn’t come back. That hits the profitability of the refinery very hard. Global refining profit margins are expected to weaken next year so they might well have doubts about how much money they need to spend and how effective that would be. So all those things have come together for them to say, actually, let’s just stop processing crude and convert it into an import terminal,”

– Alan Gelder, vice-president and lead analyst for refined products at Wood Mackenzie

The Grangemouth hydrocracker was subsequently re-opened, only to go offline again in April 2023, and has not operated since. The Telegraph reported that the cost of repairing the unit has contributed to the plant’s anticipated closure in 2025, when it is set to convert into a fuel import terminal. Analysts say that the costs make keeping the refinery in business are unrealistic – particularly with the profitable hydrocracker out of action.

Refinery economics are likely to be increasingly volatile

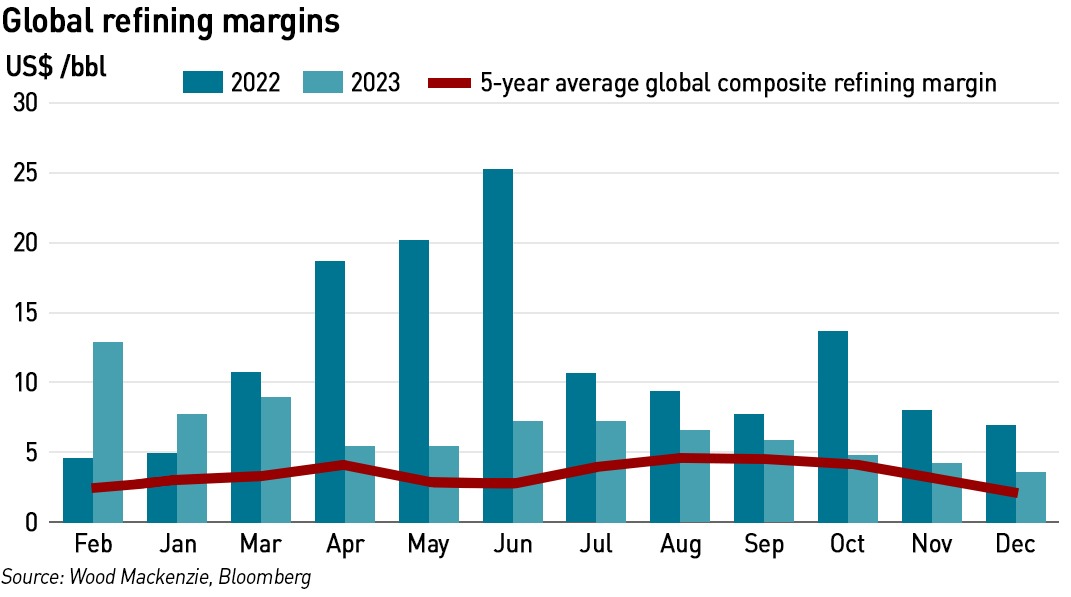

European refineries are older than more modern plant elsewhere, and are struggling to compete, despite recovering refinery margins. According to Rystad Energy, the sector has experienced a “significant strategic shift” over the past few years. Demand collapsed during the pandemic, but the Ukraine-Russia war “catapulted refining from famine to feast in term of margins”. More recently, concerns over global economic conditions and oil demand have seen margins contract again.

Between December 2018 to December 2025, the refining industry is forecast to add 12 million bbl /day of production capacity due to new projects which were sanctioned some years ago were subject to delays, including the Al Zour refinery in Kuwait and the Dangote refinery in Nigeria. Over the same period, refinery closures are expected to remove 10 million bbl /day of capacity. Depending on the region it takes between five and ten years to open a new refinery, and there are questions about the long-term future of the sector against de-carbonisation ambitions. In addition, due to the cyclical nature of the industry, refineries typically require 10-20 years of cash flows to justify the large upfront investment.

The main purpose of refineries has been the production of road and aviation fuels but climate poicies mean demand for these products is set to fall. For example, by 2040 road transport fuel demand in the US is forecast to decline by 50% versus 2022 levels, and to 25% by 2050. This undermines the rationale investments in new capacity or plant upgrades, and is driving the closure of older, and less efficient sites.

Rystad Energy sees three possible scenarios for the future of the sector:

- Steep decline: refinery closures in anticipation of de-carbonisation, particularly in the US and Europe;

- Resilience: the US benefits from strategic advantages in terms of technological complexity, location, crude supply, and fuel costs, and could remain resilient with government-aided de-carbonisation initiatives and moves to bio-refining and petrochemical integration. Europe is unlikely to provide that support will struggle to compete with refineries in the Middle East and Asia. An integration with petrochemicals, bio feeds, carbon capture and storage and green hydrogen technologies being the only feasible path;

- Volatility: the most likely scenario with policy shifts and volatility in a carbon credit-driven financial operating environment. The recent recommendation by the US Environmental Protection Agency to delay a scheme to give electric vehicle manufacturers tradable credits under a federal biofuels program is “symbolic” of the expected policy landscape.

Rystad Energy expects refineries east of Suez to gradually gain control of the global market for refined products making the west increasingly dependent on flows from the east. In this case, it says western countries may need to consider building significant strategic stocks of products. With declining global crude oil demand the Middle Eastern refineries are expected to accelerate crude to chemicals, with OPEC potentially moving to controlling the flow of refined products as well as crude.

In terms of prices and margins, Rystad Energy believes there will be more price spikes and higher volatility in the aviation and petrochemical sectors as declining refiner capacity creates shortages in sectors with resilient demand such as jet fuel, liquefied petroleum gas, bitumen, and petrochemical feedstocks. With refinery closures happening faster than the transition to EVs, there could also be shortages in road transport fuels.

It also thinks refineries will face an “upside-down operational shift” – demand for heavier sour crudes will be drastically cut while light sweet paraffinic crudes of shale quality would become particularly sought after.

This analysis throws up some interesting food for thought. Refineries in Europe face some major headwinds – their age and relatively unfavourable cost base, and the desire of governments in the region to drive de-carbonisation. However, there are recent signs that the push to replace conventional cars with EVs is slowing, and with concerns over access to minerals required not just for making electric cars but also delivering renewable generation, charging infrastructure and wider grid infrastructure, there is a growing realisation that it will be difficult for these targets to be met as they are pursued by many countries simultaneously. Concerns over the costs of the energy transition is also growing. Against this backdrop, it is not unreasonable to conclude that the pace of the transition may slow, supporting fuel demand beyond the next decade.

“Grangemouth is quite small and quite old by global standards. This is a problem for all the refineries across the UK and Europe and we are likely to see more closures in coming years. The UK now just has five refineries left, so this is going to make the UK very vulnerable to future global shortages,”

– Greg Newman, chief executive of Onyx Capital Group

Another factor is the risk associated with reliance on refineries in the Middle East and Asia, and in particular, China. China is already cornering the market in many minerals essential to the energy transition – allowing it to also dominate conventional fuel markets would be to create a major geo-political risk. Rather than European countries trying to build strategic product inventories as suggested by Rystad Energy, it might make more economic sense to retain European refinery capacity. This also has environmental benefits in that emissions from shipping refined products would be reduced.

It appears that Europe is going to need to invest one way or another, so it would be sensible to make investments that provide the most energy security, even if that comes at an apparent near-term premium. And in this there is some serious thinking for the UK and Scottish Governments to do in relation to Grangemouth.

Parallels with Rough – let’s not make the same mistake twice

Back in 2016, Centrica determined that it was no longer feasible to continue operating the Rough gas storage facility in the North Sea. After 10 years as a working gas field and then 31 years as a storage facility, its wells were old and beginning to fail. Centrica deemed that the only truly safe option would be to re-drill the wells, at an estimated cost of around £1 billion. The trouble was that with a global supply glut, the value of its storage operation was too small to justify such an investment, particularly with net zero ambitions likely to limit the life of the facility.

So, Centrica decided that unless the Government stumped up the cash, it would close the UK’s largest gas storage facility. The Government demurred, and Rough duly closed, with Centrica producing all of the cushion gas and a good portion of the tail reserves in the original gas field.

Then came the post covid gas bull run and the Russian invasion of Ukraine. Suddenly there was no global gas glut and gas prices became much more expensive and volatile – the ideal conditions for a storge operator. There were many complaints about the short-sightedness of the decision not to keep Rough open (although none that I saw supported by a cost-benefit analysis demonstrating that the £1 billion would have been well spent), and Centrica decided to re-open the facility, initially with 25% of the working volume available, rising to 50% this winter. However, with no cushion gas and less tail gas, the reservoir pressure is greatly reduced, and with no compressors on the production wells, deliverability rates are a fraction of what they used to be (although this lower pressure makes the well integrity concerns smaller).

The salient point, however, is that an important piece of energy infrastructure was allowed to close because remedial investment was considered uneconomic, a decision which many have subsequently regretted. While I continue to criticise those who insist Rough should have stayed open without demonstrating that the £1 billion cost was justified, the saga should be considered now when evaluating the situation at Grangemouth. Like Rough, analysts are suggesting the fundamental economics are tricky, even without the technical challenges, but as with Rough, it is easy to imagine a scenario where a few years down the line, this situation changes.

I’m not suggesting that Petroineos needs to cough up the money for a new hydrocracker, but that the UK and Scottish Governments should think long and hard about whether this is a strategic asset which is important to the country’s energy security. Realistically, the energy transition will take a significant amount of time, during which, hydrocarbons will continue to be required – and it is important to remember that refineries do not only produce fossil fuels, they produce petrochemicals which are used in a wide range of other industries.

When Russia invaded Ukraine, the global gas market underwent a seismic shift, with Europe scrambling to replace Russian gas and other energy products (with mixed success). This resulted in sustained higher prices, requiring the UK and other European countries to subsidise end users, both domestic and industrial, to minimise hardship and maintain competitiveness. The previous logic about the ability to meet UK gas demand on a just-in-time basis was called into question, with many believing that the country would be more resilient if Rough had remained open.

There are clear parallels with the Grangemouth situation – in order to remain competitive, the plant likely needs significant investment, but without it, the UK will have a higher reliance on imports, and in particular, imports from countries whose friendliness is not certain. If China were to invade Taiwan the resulting sanctions could impact the markets for refined fuels in much the same way that the Russian invasion of Ukraine impacted gas markets. It is no longer sensible to discount such concerns – the Russia-Ukraine situation has shown the importance of properly managing geopolitical risks and not placing undue reliance on imports.

.

As Joe Biden discovered, when refinery capacity closes, petrol price rise. This may be less politically sensitive in the UK than in the US, but it is still undesirable. Moves to embrace electric cars are stalling, with EV mandates being delayed, and other problems such as access charging infrastructure and insurance hurting demand for electric vehicles. Demand for petrol and diesel is likely to continue for at least another decade even for light vehicles, and longer for heavy trucks. Transition timescales are likely to slip, so it would be wise to ensure the infrastructure necessary to maintain energy security is not compromised in the meantime.

The closure of Rough storage is something many came to regret. The UK and Scottish Governments should take a long, hard look at Grangemouth and avoid making the same mistake again.

The closure of the Rough storage : It is interesting to watch the HoC Public Accounts Committee meeting 25/10/2021 taking oral evidence on “Achieving Net Zero : Follow Up” :

https://parliamentlive.tv/event/index/e7153087-35c9-44c4-8d7f-6522b4acf8e1

Start at 16:54:50

Could the Rough wells not simply be re-completed rather than re-drilled? It seems all their issues are to do with integrity of the tubing and casings and I don’t understand why that would require drilling a new well.

You can read the report here

https://assets.publishing.service.gov.uk/media/5a0c1010ed915d0ade60db73/rough-gas-storage-undertakings-review-provisional-decision-15.11.17.pdf

This country need to realise before its too late that we need to have core industries onshore maybe not for self sufficiency but certainly at a level that will suppress social unrest.

As an aside whilst EV’s demand is dropping there is a mandate on ICE manufactures with sales of more than 1000 vehicles pa to sell an increasing percentage of EV vehicles – 22% next year 80% by 2030 – if they dont they will be fined 15k per vehicle missed. This risks manufactures withdrawing from the market.

It looks like another loss for British industry, where because of the inefficiency of the industrial base (costs), the economics don’t add up.

I don’t know how much energy a refinery uses, but today, with us creating 23.7GW of instantaneous electrical power from burning gas, if 50% efficient 23.7GW of energy waste or 15.8GW of energy waste if 60% efficient, one has to ask if it would be better for a government to have an industrial strategy that insists that CCGT are co-located with energy intensive (heat intensive) industries, such that we don’t have 10s of GW of wasted heat every damned second of the day when the wind isn’t blowing.

The separation of different industries may make commercial sense for individual companies when power/energy is cheap, but when it gets more expensive, diversification of commercial activities to include self-sufficiency in some areas can make better sense and more profit. After all, a company’s objective is to make profit.

A bit of central co-ordination by government (or the future system operator) and co-operation with industry to reduce energy wastage on a massive national scale would go a long way to help the transition, and help the UK economy.

23GW of wasted heat per hour = say 10p/kwh for gas = £ 2.3 Million per hour………about £20 Billion per annum, if it were 24hours a day every day.

CHP is an important step to achieve to make hydrogen economic as a fuel for power generation, where we have to stop wasting half of the energy that it embodies.

There appear to be too many industrial silos where many companies are not thinking broadly enough as to how to restructure their own industry with significantly higher efficiency. It may take the environmental lobby groups to keep up the pressure, but you have to ask, how many companies would benefit from becoming self-sufficient for power and heat with CCGT facilities or some other more basic turbine powered electricity generation as part of their industrial complex?

Perhaps the hydrogen economy is viable, only if the wasted heat from CCGT is actually put to commercial use and the electricity generated (at an excess for national demands) is seen as the cheaper by-product, as it is available at an excess.

It might make production facilities more expensive to build, but doesn’t that reduce the cost of upgrading the national grid, and the cost of electricity?

Is there anyone in government with a comprehensive industrial strategy that has identified where CCGT or basic GTs could be strategically located within industrial complexes to power the industrial processes and provide process heat as well?

Perhaps we can achieve net zero without destroying the economy, but only if the whole range of possible changes necessary are embraced.

Theoretically if discreet CCGT (electric power generation only companies) become extinct or at least a smaller part of the electricity generation industry, it should reduce the cost of electricity. When will it happen?

Centralised power generation should be seen as back-up to the self-sufficient distributed electricity and CHP power generation.

With Grangemouth, would just a GT set-up (without the combined cycle part) actually provide a better balance of heat and power? where is 40% efficiency needed if more heat “waste” is more useful?

Is Grangemouth closing a failure of both industry and government, unable to embrace the necessary changes to achieve economic efficiency……..a failure of imagination?

Needs must when the devil drives…….perhaps it will only happen when things get really difficult.

How much would advice be worth to obtain some of those £ Billions that are currently going into the atmosphere as waste heat?……..up in smoke…….money being burnt.

My specialist subject…

When BNOC was formed in 1975 the Forties system pipeline was being built and Tony Benn was minister, factors that led to Forties being the initial BNOC price benchmark. BNOC was a price follower, adjusting prices after each OPEC price change. Before Sullom Voe opened Brent crude was produced only from Brent Spar via shuttle tankers which limited its tradability. The role for BNOC in selling not only its own oil production (before Britoil got hired off) but also participation oil from producers without UK refineries and Royalty Oil, mostly on term contracts, gave the BNOC price a significance. But as production started ramping rapidly across the North Sea, it was forced to sell oil in spot markets as its availabilities were not sufficiently predictable.

The Forties system gave BP a cost advantage at Grangemouth because the cost of the pipelines and export terminal at Hound Point next door were all inside the North Sea ring fence, and thus offsettable against PRT. Pumpover FIP Kinneil was almost zero cost delivery. Only the PIP refinery on the Tees also had a direct feed from the North Sea (Ekofisk via the Seal Sands terminal), but because Ekofisk is Norwegian there wasn’t quite the same synergy. Shell Teesside had to shuttle Ekofisk across the river by tanker, and Wytch Farm production still loads from the Hamble terminal across the estuary from Esso Fawley. Because the Forties System was dominated by BP as a producer and as a consumer, thanks to Grangemouth, it was a less fungible grade for trading, and it was soon eclipsed by the Brent System as other fields were hooked in for production. Although BNOC continued to publish its official prices for both Forties and Brent, the much more liquid market for Brent soon established it as the sole effective marker grade.

That was greatly reinforced by the miners’ strike in 1984. Most UK refineries were called on to supply large quantities of heavy fuel oil to power stations to fill their tanks ahead of the strike and to provide an alternative to coal during the strike. That meant swapping the diet of light North Sea crude for heavy gunge primarily from the Middle East – all while the Iran-Iraq war was raging. It was in fact Arthur Scargill who gave the real impetus to the 15 Day Brent market, which became the global oil price marker with a much higher traded volume than anything else, including NYMEX WTI and Arab Light which previously held the global marker role. Cargoes could be assembled into VLCC loads for shipment to the US and even as far afield as Japan. It marked the undermining of OPEC’s ability to set prices, and of official posted prices more generally. BNOC found itself with big losses buying participation oil at posted prices and finding that its term customers were not renewing deals, so being forced to sell into an increasingly weak spot market as the miners’ strike drew to a close. Nigel Lawson had no difficulty winding up the role of BNOC, and on the back of my advice, taxable values for North Sea crude on a non arms length basis were based on differentials to average traded 15 day Brent prices during the delivery month and the month prior with a small admixture of dated deals that occurred mainly to swap dates to make a convenient multi parcel export loading, or for the convenience of a particular refiner, with differential adjustments for other grades.

The Dated Brent market emerged as the “Wall Street Refiners” (J Aron/Goldman Sachs, Morgan Stanley, JP Morgan etc.) started to get much more involved in oil markets. They introduced CFDs into the market, priced at a differential between 15 Day Brent and Dated Brent quotes. It was for them a money spinner, as they would assemble large long or short positions in the CFDs and then trade in the Dated market at outrageous differentials that would apparently seem loss making until you accounted for their CFD positions which would then be in huge profit. By persuading refiners and producers to consider Dated as the “true” market, they pulled the wool over a lot of eyes and pocketed the difference. In fact the real Dated market was always limited by the physical availabilities and then only those that were open to further trade. It was easy to corner.

As Brent System production started to decline the daily routine of cargoes being nominated 15 days ahead into chains of contracts, with pass-the-parcel ending when either someone declared they were “keeping” for physical delivery, or someone got caught holding the baby at the 5pm deadline became not quite every day. Moreover, at Sullom Voe itself there were problems with pinhole leaks emerging in the pipes in the separate Brent and Ninian frac trains that separated out LPG . The Brent System borrowed some frac capacity from the Ninian system while repairs were effected. It became clear that there were potential cost savings from dropping to one frac train, and otherwise sharing the other facilities such as tankage that could only be achieved by commingling the streams. However, it was equally clear that Brent as a marker grade had a premium value that needed to be reflected in entitlements to lifting relative to volumes supplied. Difficult and at times fractious negotiations ensued before agreement on commingling was reached. That bolstered the volumes again and helped restore market liquidity.

Brent and Bonny Light had long been established as deliverable grades against NYMEX WTI at Cushing, Oklahoma, which equally long troubled Statoil, who wanted markets for their Gullfaks and Oseberg grades that were not entirely compatible, being somewhat naphthenic. They did succeed in securing NYMEX delivery, however it took until 2002 before BFOE became the norm in the North Sea, and Troll has been added subsequently. There’s a good summary of the post 2002 history here

https://www.oxfordenergy.org/wpcms/wp-content/uploads/2019/03/Changes-to-the-Dated-Brent-benchmark-more-to-come.pdf

Turning to the refinery itself.

It was BP’s last remaining UK refinery (having closed Llandarcy, Belfast , Grain before they sold out (and sold much of their North Sea interests too). It has long been closely intertwined with the adjoining petrochemicals complex, for which it continues to supply a large share of feedstocks. The hydrocracker had a troubled history with an explosion while coming back from maintenance in 1987. It was actually originally angled at naphtha production for petchem use and perhaps for reforming into high octane gasoline components. Being the only refinery in Scotland had other advantages: there is less competition in the marketing of fuels, as competitors not accessing product on an exchange basis with availabilities from other refineries were faced with costly coaster movements to supply terminals. The result was a higher average price for the output and better margins. Of course, when it closes all fuel will have to be imported from elsewhere, and prices will rise and supply security will fall.

The Grangemouth complex had long been a target of Lord Deben who had written publicly to the Scottish government to tell them it should shut to achieve Net Zero.

https://www.theccc.org.uk/publication/letter-lord-deben-climate-change-committee-to-roseanna-cunningham-msp/

Power station demolition expert Nicola Sturgeon agreed. Now it’s Humzat? A lot of the pressure on UK refineries really comes from net zero impositions limiting fuel choices and tightening regulatory standards at great cost and little benefit, destroying potential competitiveness. Green hydrogen and biofuels are not the answer, but instead threaten to guarantee uncompetitiveness and closure. Shell’s REFHYNE project showed the perils of green hydrogen as high cost and intermittent – not what you want for a continuous process. Steam methane reforming remains the cheapest source of hydrogen, increasingly needed for desulphurisation and upgrading.

Grangemouth is not the only refinery under threat. They all are, despite having had a bumper 2022 to make up for the dire 2020 when runs were cut severely and profitable aviation fuel sales reduced to almost nothing.

What happens to the 15 year ethane supply agreement from the US Ineos signed is an interesting question. The ethane supply did obviate the need for the hydrocracker to provide feedstock, as well as securing supply for Fife Ethylene Plant, Mossmoran on the other side of the Firth.

Already the UK refineries are heavily dependent on light sweet crude imports with the US now the largest supplier, with most North Sea crude being exported. A complete inversion of the miners’ strike position. And now US crude is added to the Brent benchmark pricing.

It will be interesting to hear what the Chinese think of seeing the Petrochina investment in Grangemouth turn so sour.

Thanks for sharing your expertise (and the pub at the end!)

I was at an event at Policy Exchange about energy security last night – it’s depressing how naive the thinking is.

Further to my point above about co-location of CCGT/GT in industrial complexes, it would be necessary to have two heating means for the processes, both electrical and CCGT/GT, because when there is enough wind, then direct electrical power should be sufficient, and the CCGT/GT shut down.

This also means that if there is a problem with maintenance/repairs to CCGT/GT power, the process doesn’t have to go off-line. It requires a bit of planning and thought, and not all industrial processes would be suitable, but there must be some out there that could be adapted.

The use of dual heat sources may be a suitable application for AI to control the process, unless it is turned into a baseload type electricity generation, where it is a smaller part of the electric generation mix, but dual heating direct electric + GT exhaust should be able to make it fully flexible.

They removed the turbine halls on the last efficiency improvement, now there’s the integration into the industrial base that really needs to happen.

If there are periods when the industrial process has sufficient heat, but electricity generation is still needed, then it should be possible to exhaust direct to atmosphere away from the process, but at least using the GT exhaust for a significant period would mean substantial savings/profit.

Even if this were numbers of micro-turbines for building CHP instead of industrial processes, there would still be savings or another income stream.

Kathryn, you wrote, “Realistically, the energy transition will take a significant amount of time …” which certainly reflects the current (naive) political thinking. However, David Turver’s substack [https://davidturver.substack.com/p/why-eroei-matters?utm_source=profile&utm_medium=reader2] has popularised the EROEI (energy return on energy investment) parameter developed by Weissbach about a decade ago. Consideration of EROEI shows that the current generation of renewables is NOT in the least suitable for a competitive economy, nor for one which aims to maximise sustainability (although “minimise unsustainability” might be a better term).

None of the above negates the possibility of a NEW generation of renewables at some stage transforming the situation in favour of renewables. However, only a flourishing economy will be rich enough to reseach and develop those new renewables. Thus I foresee that the transition to renewables will take a very, very long time … unless political pressure for current renewables continues to depress (destroy?) the UK economy.

In light of the above argument, I believe that fossil fuels will be required for decades to come and so we should maintain our related strategic resources/infrastructure. But equally important, as you comment, is to counter the naive beliefs of the political and media classes for whom current renewables are unquestionnably to be adopted – but that way lies ruin as we fall, ever faster, over the EROEI cliff.

Keep up the good work. Speed the plough!

Regards, John.

Thanks John, I think recent events in the wind sector have been raising awareness of the cost issues. DESNZ is working on a new LCOE and intends to make it more cost-reflective. I asked Claire Courtinho whether this will be fully cost reflective at a recent Policy Exchange event. She blustered, but I made the point that renewables costs need to include increased balancing, reserve, and grid costs, and to be truly comparative, de-commissioning costs should also be applied to all generation technologies and not just nuclear. We’ll see…

The problem is there is no single inclusive LCOE, even if construction and fuel costs are constant. If you increase the penetration of renewables several types of cost scale much faster. We are only in the foothills of curtailment costs, with capacity at a level that produces occasional surpluses at lower levels of demand. Add capacity, and the surpluses become both larger and more frequent. If the Continent does likewise there isn’t even the option to have UK consumers subsidise exports at low or negative prices. Suddenly you are looking at the choice between curtailment and very expensive storage which adds massively to cost. Still you need backup, where costs increase due to lower average utilisation and damage from repeated and mostly faster ramping. Try to dispense with the backup and the storage requirements take a massive leap. Meanwhile the useful output from an extra wind farm becomes derisory as most of its output adds to existing surpluses while it offers very little to deal with Dunkelflaute.

Still, I suppose if someone starts to feed in more realistic costs to the Royal Society storage study perhaps the penny will start to drop. High cost input into a low round trip efficiency storage system produces very high cost output. An economy saddled with the prospect of such costs will simply collapse, and not be able to afford to handle any consequences of climate change, or even to pursue net zero goals.

I hope they are building the wind turbine towers better than schools, where they have used RAAC. If certain parts, such as the main tower structure are built for longevity, for several generations of refitting, decommissioning costs should be a tiny proportion for wind turbines, where the generator pod and blades should be the only components that need to be replaced with each repowering. Even if the blades need to be disposed of (pelletised/ground up/repurposed), the generator itself can be reconditioned. There’s an active generator reconditioning industry already working.

Although with repowering old wind farms, the strategy has been to reduce the number of turbines, but install newer higher powered turbines to significantly increase the output overall.

One has to hope that carbon fibre is the main component of the blades with a suitable resin, and not fibreglass, such that they can be burnt as solid fuel. A bit of thought as to end of life usage goes a long way to turn waste into a useful resource with economic value. How many tonnes of solid fuel would that provide per annum, instead of burning methane or hydrogen?…….or would it be better if aluminium is used as that is infinitely recyclable. Steel towers are no problem either.

If you could pelletize on site and ship direct to a solid fuel powered electricity generator…….the spawning of new industries and work and efficiency………you can’t do that with a nuclear power station.

My comment form was filled in with details for David Porter. It seems the system is still leaking email addresses.