Britian’s latest subsea interconnector, the 1.4 GW Viking Link with Denmark began commercial operations at the end of December. Initially its capacity will be limited to 800 MW until internal grid reinforcement in Denmark is completed, since if it ran at full capacity the link would risk overloading the Danish network in the West Jutland region. Expansion of the 400 kV grid along Denmark’s west coast will enable Viking to operate at full capacity, with the first part of the West Coast Link from the German border to Endrup expected to open in Q1 2025. Analysts at S&P Global Commodity Insights forecast net flows to average around 500 MW from Denmark to Britain until February 2025. The Viking Link is the longest subsea power cable in the world at 765 km.

“Great news today as the new Viking Link interconnector starts to transport energy between Denmark and the UK, under the North Sea. The 475-mile cable is the longest land and subsea electricity cable in the world and will provide cleaner, cheaper more secure energy to power up to 2.5 million homes in the UK. It will help British families save £500 million on their bills over the next decade, while cutting emissions,”

– Claire Coutinho, Secretary of State for Energy Security and Net Zero

The news of yet another interconnector between GB and other nations has been widely celebrated, but is it really such good news? Regular readers will know I am sceptical that interconnectors can be relied upon to deliver imports when needed. Under Capacity Market rules, interconnectors only need to be operational during times of system stress – they do not need to be importing, and there are no mechanisms to force imports if the capacity has been sold to market participants for the purposes of exporting (although exports can be stopped). If both markets at each end of the cable have simultaneous system stress then, technically, there would be price competition between them to secure imports, but in reality it is expected that system operators would intervene to float the cable, meaning power would not flow in either direction.

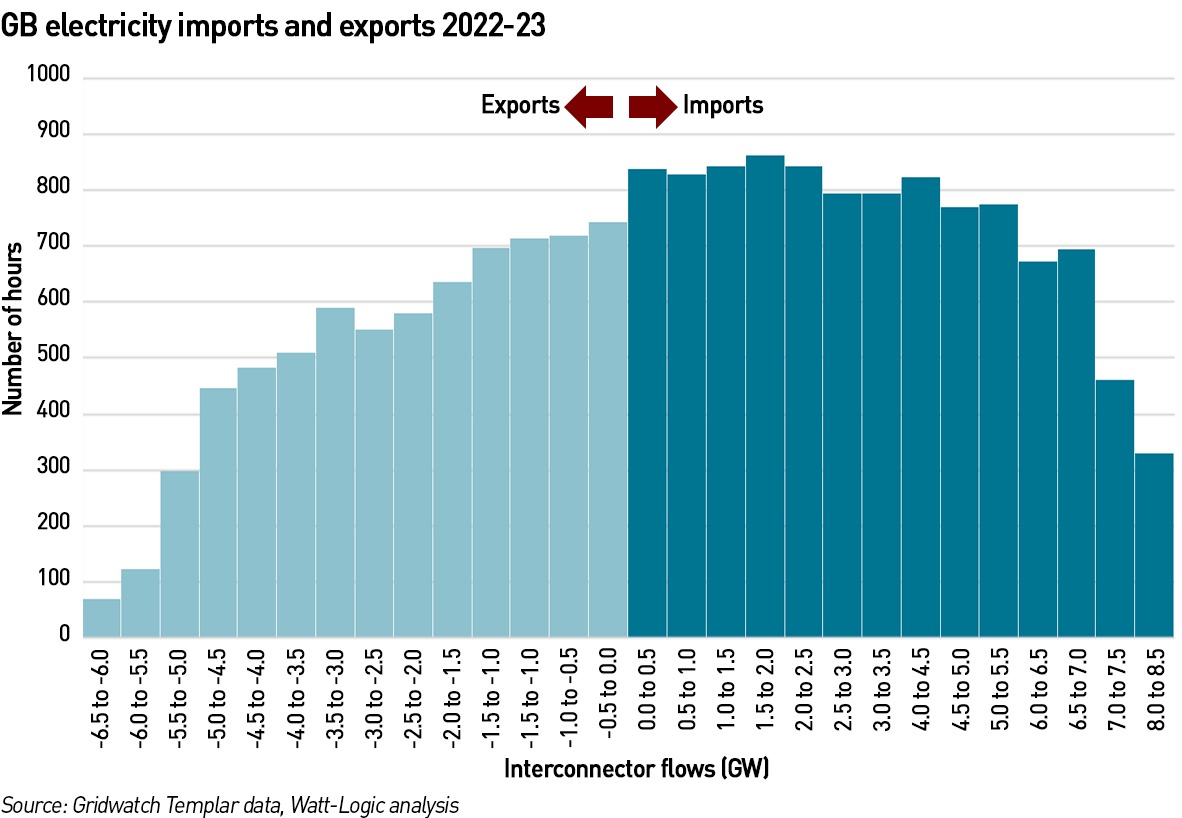

Back in 2020 I looked at the behaviour of our interconnectors with the Continent and found that during periods of high GB winter demand, the country often exports electricity: Britain exported electricity to Continental Europe during 13% of the hours with the top 5% of demand since the beginning of Winter 2020, while exports accounted for 16% of all hours over that period. (Considering Winter 2019, which was less affected by covid effects, Britain exported electricity to the Continent in 18% of all hours and 12% of the hours with the highest 5% of demand.)

I have updated this analysis for 2022 and 2023 and found that across the two years, Britain exported in 23% of the top 5% of hours with the highest demand (I sorted all the hours in the period by demand, highest to lowest and then looked at the top 5% of hours to determine the levels of imports and exports – in 23% of these hours, GB was exporting).

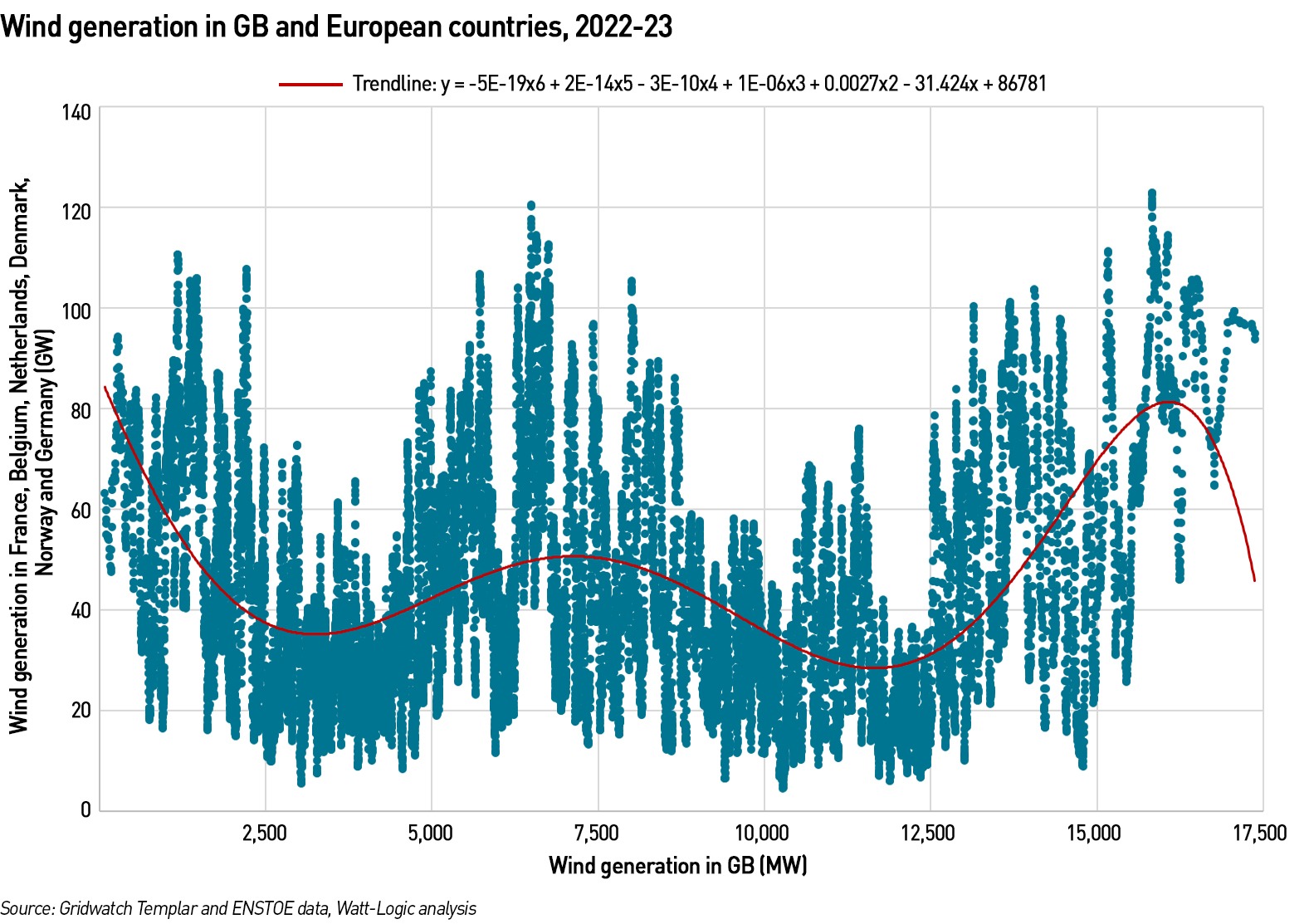

For 2023-23 I also looked at wind output in GB and also its connected markets (France, Belgium, Netherlands, Norway and Denmark) as well as Germany. Although there were no flows between GB and either Denmark or Germany during the period, the supply and demand balance in these countries impacts both the connected countries and GB, and therefore I included them in the analysis.

In the past couple of months I have been providing a client with daily market updates for GB, looking at demand, imports and wind generation. What I noticed was that during periods of high wind generation in December and January, GB also attracted significant electricity imports, however during the cold spell when wind generation was lower, imports were also lower and exports higher. So, I decided to see whether this was part of a wider trend. Taking my two year dataset, I considered the times when wind generation was high (above one standard deviation from the mean) or low (below one standard deviation from the mean).

In 11% of hours there was high wind in both GB and the other countries, and in 13% of hours wind was low in all countries – that is significant, as 13% is close to one day per week. During 8% of hours it was windy in all countries and GB imported, and in 5% of hours it was not windy in all countries and GB exported. GB exported in 7% of hours when it had low wind generation and received imports in 13% hours when it had high wind generation (regardless of the wind levels in the other countries).

The data don’t entirely support the anecdotal evidence of the past couple of months, but nor do they suggest that interconnectors provide reliability in times of high GB demand. It’s likely that the high volume of overall exports in 2022-23 was due to the specific challenges in France and Norway during 2022 when large parts of the French nuclear fleet were offline due to the stress corrosion problem and Norway faced 20-year reservoir lows in its hydro-dominated electricity system.

But the French fleet is aging and this was the second time in six years that a systemic problem had taken large parts of the fleet out of action. The French nuclear regulator has indicated it may not be the last time. Meanwhile, while Norway’s reservoirs may not see such lows again for some time, the country has gone notably lukewarm on exporting electricity since it opened its interconnectors with Britain and Germany in 2021. Not only has the country amended its Energy Act to allow it to restrict exports if it is experiencing domestic system stress, it has proposed a further amendment to allow restrictions in case of potential domestic shortages.

“We must have control that we have enough power in Norway. The bottom line for this is our own security of supply. We must be sure that we always have enough water in our reservoirs. There must always be electricity in the socket and we must have enough power for our industry,”

– Jonas Gahr Støre, Prime Minister of Norway

In addition, the Norwegian Finance Minister, Trygve Slagsvold Vedum, has said two of the interconnectors between Norway and Denmark (Skagerrak 1 and 2) should not be replaced when they reach the end of their lives in the next year or so. While Energy Minister Terje Aasland, takes a different view, each minister appears to reflect the position of their party (the current Norwegian Government is a coalition between Vedum’s Centre Party and Aasland’s Labour Party). This comes after Norway refused to licence the proposed 1.4 GW NorthConnect interconnector between Norway and Scotland last year. Norway is also considering taxing electricity exports in a bid to keep domestic electricity prices down. 70% of Norwegians believe that high power prices in the country are caused by cross border power cables, creating political opposition to greater interconnection with neighbouring countries.

”The [Norwegian] Centre Party believes there is no reason to renew the licenses. This is our clear primary position. We believe the time is over for large, new offshore cables,”

– Trygve Slagsvold Vedum, Norwegian Finance Minister

In addition to concerns over the economic and political risks of interconnectors, there are also physical risks. Since the start of the Ukraine war, the focus has been on deliberate acts of sabotage after the Nord Stream and Balticconnector gas pipes, however there have also been instances of accidental damage to subsea power cables, notably four of the eight cables of IFA-1 which were damaged by a ship’s anchor in 2016.

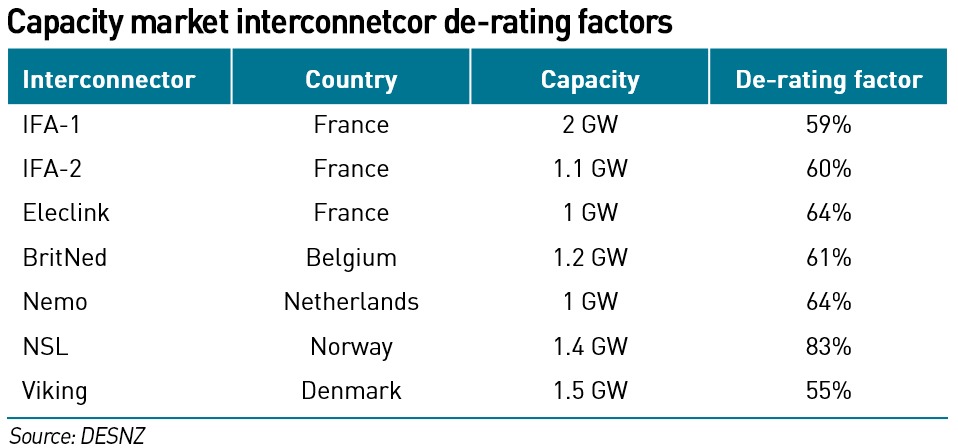

The overall expected availability of interconnectors is captured in the Capacity Market de-rating factors. The Government took a more conservative approach than had been recommended by National Grid ESO and the Panel of Technical Experts (“PTE”) which scrutinises the annual Electricity Capacity Reports (“ECR”) by National Grid ESO.

“Interconnector analysis has always been challenging. Firstly, because of their nature: they are transmission links but inject energy resources into the GB network like generators. Secondly, because an assessment of their contribution under stress events is quite hypothetical as there is an absence of sufficient historical evidence on flows under stress. As a consequence, the resource contribution and derating factor analysis is essentially model-based,”

– Panel of Technical Experts: Report on the National Grid ESO Electricity Capacity Report 2023

According to the PTE, the data analysis in the 2023 ECR shows that interconnector imports are modelled to be less than 40% of the total interconnector capacity for over 15% of tight hours. However, 80% of total capacity is available for around 70% of GB tight hours. France has a greater correlation of tight hours with GB than any of the other markets.

Each year the vulnerability of the GB power system grows as reliable thermal and nuclear generation is replaced with intermittent renewable generation, primarily wind. However, wind lulls can both coincide with periods of high system demand (anti-cyclonic weather systems characterised by cold, still weather in winter and hot, still weather in summer) and can be extensive, lasting for days or even weeks, certainly beyond the capacity of any currently existing batteries to back up. So far, there has not been a system stress event, triggering delivery under Capacity Market rules, but each year the risk of that increases, however, the performance of interconnectors in such an event is, as the PTE recognises, is entirely “hypothetical”.

A combination of high weather correlation, political sensitivities and physical risks could all threaten the ability of Britain to attract imports at times of need. Relying on interconnectors could prove to be a huge gamble and one we only know we have lost when it is too late.

Absolutely correct. The rush for nenewables combined with the assumption that the interconnectors will always fill the gaps is a serious risk to the security of our electricity supply.

Hi Kathryn,

When I was with the ESO, I developed the model we used for assessing season-ahead risk, for Summer and Winter outlooks. It’s more sophisticated than using 2 years’ worth of data, with flows already conditioned on market iutturn conditions.

We simulated 200,000 full seasons of weather (driving demand and renewable output) and availability of individual generators and interconnectors (effectively mechanical availability), taking into account planned outages. This gives a reasonably full stochastic view of possible outcomes.

We then used scenarios to see the effect of political actions (such as a ban on Norwegian exports) or stress events (eg gas shortages, French nuclear unavailability etc), and allows us to see the risks if we are fully exporting or if particular interconnectors are set to float. Again we used 200,000 seasonal stochastic simulations for each scenario. We would typically have between 10 and 20 different scenarios.

This approach allowed us to assess the risk of shortages (there’s always a risk, even though it may be exceptionally unlikely), how long any shortages might last, and how reliant we are on being able to import on interconnectors, or our exposure if the market drives exports out of GB.

We were able, under these different scenarios, to report to Government any expected impacts at particular risk levels (typically we would report at 1 in 10 year and 1 in 20 year risk levels). We could identify periods of the season which were at higher risk than others.

Abbreviated summaries of these analyses were also reported to stake holders through the weekly Operational Transparency Forums.

I wouldn’t expect the Secretary of State to have a full grasp of the mathematical techniques we used to assess the risk. But I am not aware that any other Transmission Operator was using the same level of analysis that we were. We were certainly not complacent in doing the analysis.

Thanks for commenting Andrew. I wanted to model actual data but it’s difficult in Excel with so many data points – two years was the limit my pc could cope with particularly with hourlay data across 7 countries!

I have discussed ESO’s modelling approach with Fintan in the past and came away with the conclusion that the link between cold weather/high demand and still weather, as well as the correlation with other countries may be under-stated. However, as the Expert Panel says, this modelling is all purely hypothetical, Fintan also told me that other TSOs were privately clear that exports would be off the table if they had system stress. So essentially it’s a gamble on not having system stress at the same time…as several local countries are increasingly relying on weather, and are intending to electrify heating, this seems like a significant risk.

Coutinho’s degree is Maths and Philosophy. You hope she’d understand the philosophy, and perhaps even the maths of Monte Carlo type analyses. My experience of looking at Monte Carlo type approaches to simulating weather (and hence demand and renewables outputs) is that they don’t produce very realistic answers because the complexity of weather systems simply can’t be captured by a few correlations and feeding in random numbers plucked from some p.d.f.. Prof Andrew Blakers tried doing this for Australia, and although he got seasonality out of his model it really didn’t reflect the longer term realities at all: the El Nino/La Nina cycles have a big impact on the weather there and he failed to emulate that, or longer durations of particular weather patterns, even though his geographic short term correlations perfectly matched the correlations of data from BoM that he used as input (by virtue of the technique).

Seeing the sort of work that has been offered by AFRY and Regen in support of Net Zero calculations fills me with horror. The criticisms raised by the Royal Society are correct (and there is still a lot to criticise with the RS work too), even if I had raised them long before. For example, here is my submission to OFGEM when they were consulting about interconnectors:

https://www.ofgem.gov.uk/sites/default/files/2021-12/F2S%20Response%20%281%29.pdf

There is a common assumption amongst that section of eco-enthusiasts that even recognise that there is a problem, that we will only need enough storage to cover the expected duration of a long dunkelflaute, say a fortnight. But this doesn’t allow for the need to replenish the storage ready for the next dunkelflaute while simultaneously meeting demand.

How long would it take to refill a fortnight’s worth of storage using just surplus generating capacity? A month, two months? The amount of storage needed is mind-boggling and completely unaffordable.

We currently have no ability to cover a 2-day dunkelflaute in the UK never mind 2 weeks!

Pretty well since December we have had good average wind speeds and could have generated a lot more but almost daily ESO is forced to constrain off wind costing us over £12m on some days due to inadequate transmission capacity or is it SQSS rules that are too onerous. They are happy to contend with a loss of an 1.4GW interconnector as a system risk but seem to want to protect against a double circuit outage across boundary zone B6 as a result Scottish wind farms are constrained off. This of course drives up system price and makes us a one way bet for the i/c traders. Also in my youth govt used to worry about our balance of payments maybe it doesn’t matter anymore but a lot of consumers money is leaving the UK that could have stayed within the UK had we perhaps created and inter regional privateers HV DC interconnector market like we did with our European neighbours.

Oh Viking has exported 1.4GW

In the first couple of weeks in Jan wind speeds were lower, demand was higher and imports collapsed! It was quite interesting to watch. The data don’t suggest this is a wider trend, at least not in the past 2 years. Longer analysis is difficut in excel and in any case pre 2020-22 was impacted by covid so any demand-related analysis including cross-border flows isn’t really going to be very indicative of anything, and before then we had fewer interconnectorsin operation.

I fear that this article will prove prophetic before long and we will be left struggling with power shortages. Comments on other blogs have shown that periods of “dunkelflaute” can last for many days and afflict large areas of northern Europe. At such times charity will cetainly begin at home for our neighbours.

One small point…”But the French fleet is aging and this was the second time in six years that a systemic problem had taken large parts of the fleet out of action. The French nuclear regulator has indicated it may not be the last time.” This view does not reflect the “Grand Carenage” – a massive programme of upgrades and refurbishment that the French have been implementing for about 10 years and is nearing completion. It’s costing close to €50 bn – roughly €1 bn per reactor – and covers a huge scope of work including replacement of steam generators and other components, upgrades of controls and instrumentation, etc..

Claire Coutinho, Secretary of State for Energy Security and Net Zero :

“The 475-mile cable…..will provide cleaner, cheaper more secure energy……while cutting emissions,”

Isn’t the reason for interconnectors simply to reduce generation in the UK and thus reduce our CO2 emissions?

Yes, that’s a large part of it. All interconnectors are treated as providing zero carbon electricity irrespective of the actual generation mix of the connected country. Denmark is actually 2/3 renewables so there’s a stronger “green” argument for Viking, but not so much for BritNed and Nemo.

But the EU no longer thinks like that!

https://www.current-news.co.uk/energy-uk-eu-carbon-tax-detrimental-to-uk-renewables-unless-emission-trading-systems-linked/

It wants to impose carbon border taxes on our electricity exports.

Denmark is of course heavily cris-crossed with flows between Germany and Scandinavia, which makes determining the composition of its power exports more complicated. P-F Bach has been monitoring the situation for many years now, as Hugh Sharman pointed out below.

And yet the Government wants to go-ahead with the closure of our last remaining coal powered station.

Some energy is better than none.

I agree. At this point the Government should not allow any conventional power station to close unless it’s broken. 2 GW coal generation isn’t going to be the difference between climate change and not, but it could be the difference between a blackout and not.

I did some calculations as to what the Germans had used for sensible thermal storage. If using basalt rock and assuming £100/ton then and temperature of 1000 degC then it works out about £0.43/kWhr for the storage medium alone.

And so 46 GW for 100 hours would require 20 million tons of rock (costing £2 billion and occupying 7 million cu m) .

And there would be additional costs including the gas and steam turbines associated with the storage medium itself.

As to the issue of recharging any storage. I think that this most relevant point as I do remember seeing where there was a 20% dunkelflaute for 11 days which consisted of 2 5 day long 10% dunkelflaute with a small separation. (I think it was from the start of 2021).

However I think that there is no real appreciation of the risks that these prolonged periods of calm cause.

The government has put out a call for consultation on how to support LDES (Long Duration Electricity Storage – not energy) and is only looking at the duration of 6 hours or more. And has done a scenario analysis (but only for 2 years – 2023 and 2035) https://assets.publishing.service.gov.uk/media/659be546c23a1000128d0c51/long-duration-electricity-storage-scenario-deployment-analysis.pdf This seems much more focussed on the excess (but unloved and unwanted) wind generation.

It gives examples of LDES but most are less than a day ; there is an example of pumped hydro lasting 32 hours! In the UK 5 hrs would be more typical – such as Dinorwig and I know little about iron-air batteries though I did find a cost of about £25/kWhr!

It should be noted that the government has, also, LONGER duration energy storagehttps://www.gov.uk/government/publications/longer-duration-energy-storage-demonstration-programme-successful-projects/longer-duration-energy-storage-demonstration-programme-stream-1-phase-1-details-of-successful-projects

But that these projects do not seem to be addressing very long duration.

And there were no entries in their thermal storage section – perhaps this is more a reflection of the lack of UK interest in this – despite it being potentially cheaper (and fitting into replace combustion systems in coal or gas powered generation – as Siemens-Gamesa did in addressing potentially stranded assets.)

It should be noted that Siemens-Gamesa had a prototype (Carnot battery) 5 MW 130MWhr system but could not see a commercial market mechanism (- and has not been helped by the companies troubles).

The Royal society https://royalsociety.org/topics-policy/projects/low-carbon-energy-programme/large-scale-electricity-storage/ has addressed this issue – but has focussed on the storage and use of hydrogen. I think that there are still many issues to do with this that have not be resolved.

They did identify, in their briefing documents, Carnot batteries as one of the cheapest – especially as its operating temperatures increase.

The government LDES report works backwards. It starts with what it considers to be available technologies, and the works out how they might be used without evaluating whether they would actually solve the real problem. For them, interconnectors, or a just in time change in the wind allows Mary Poppins to continue to keep Mr Brown’s lights on even if the chimney sweep is out in the cold. They should be forced to redo their homework, starting with the RS paper, but reflecting real costs and performance of renewables rather than their fantasy world. A proper look at demand would not go amiss either: heating is grossly underestimated, and the idea that the economy could halve its energy intensity without triggering a revolution is distinctly fanciful.

I just checked up on some details about energy storage relating to the MOLTFLEX nuclear power. This is possibly a bit of a cross–posting. But they have their storage system “GridReserve” that they use to improve the economics of build (which is what interested me) as well as use.

They claim a levelized cost of electrical storage of roughly £50/MWh (and I think build costs is around £30/kWh). (see https://www.moltexflex.com/blog/gridreserve-the-future-of-energy-storage/) . And , of course, is charged by the nuclear reactor, has variable discharge rate but, typically, takes longer to charge than discharge (see https://www.moltexenergy.com/wp-content/uploads/Moltex-GridReserve-system-FINAL.pdf ).

The system is designed to be modular and to take cheap grid electricity, if available, as a heating source; indeed it could be used as an energy storage system in its own right.

I do not know how this might fit into the plans of The National Grid – and their criteria for energy storage being economic…

Thank you for analysing the daily figures of exported/imported energy via the interlinks. The daily balance varies so much when viewed on the GridWatch website it’s hard to make sense of them. In 1974 I was serving in N Ireland when the Ulster Workers’ Strike shut down the grid. After 4 days, the chilled and frozen food had been spoiled, bodies in morgues had thawed and civilisation was unwinding daily. I have used this example when writing to successive Secretaries of State for Energy to try to make them understand the consequences of their under-investing in UK base load. Another issue I have stressed is the vital importance of grid frequency stability; for a fixed load, current increases as frequency reduces, hence the importance of load-shedding when demand is excessive in order to avoid melting the grid’s cables. There must be a large scale demonstration that “artificial” rotational inertia can provide frequency stability in an all-renewable energy grid.There are not enough physicists in Parliament. Alok Sharma was the only physics graduate in the SoS for Energy post and he was “captured” by the eco-warriors. When the job of Ofgen’s CEO becomes vacant, please apply Kathryn.

Hello Kathryn,

As several commentators have indicated above, I fear that we may be greatly under estimating the amount of electrical storage required in the event of rare but not unknown long-duration dunkelflauten. As I have posted at Paul Homewood’s NALOPKT site, there can be periods of many weeks when the wind does not blow sufficiently. I estimate the storage requirement in tens of weeks rather than just a few days!:-

https://notalotofpeopleknowthat.wordpress.com/2024/01/26/ccc-wind-power-plans-ignore-the-nao/

Furthermore, the record shows that the annual wind resource can vary hugely over decadal timescales. And wind droughts can occur in adjacent years too.

So, if through foolishness/naivety we do not have sufficient dispatchable generation then we must ensure we have enough UK storage; relying on the kindness of strangers (i.e. interconnectors) is a recipe for disaster.

Regards, John.

Hello Kathryn,

I live in Denmark. The truly great Paul-Frederik Bach is logging the imports and exports to keep Denmark’s fragile power system in balance.

I am sure your subscribers will find is data inspirational!

That Viking Inter-connector is certainly getting plenty of use these days.

http://pfbach.dk/firma_pfb/weekly_exchanges_2024.htm

P-F B’s insights are always very valuable. Here’s his historical summary of European interconnector flows:

http://pfbach.dk/firma_pfb/news_2023_1_e.htm

This commentary on 2023 is also an excellent pointer:

http://pfbach.dk/firma_pfb/references/pfb_france_is_back_as_europes_main_power_exporter_2024_01_26.pdf

Here is 2022 at daily resolution (click on chart for full size version to examine detail):

https://i0.wp.com/wattsupwiththat.com/wp-content/uploads/2023/02/GB-Gen-Price-HQ-1676233783.8236.png

Interconnector imports and exports are shown gross for each day: if an interconnector switches during the day between import and export, both will be shown, and likewise for pumped storage. It is easy to spot that from spring onwards exports were enabled by cranking up CCGT generation to keep the French supplied through their nuclear shortage, with additional volumes going particularly via Belgium. IFA1 was operating at reduced capacity because of the fire in September 2021 at Sellindge converter station. North Sea Link was also beset with technical problems. Western Link HVDC has had a shocklingly bad record of availablility with extensive cable repairs being needed, and BritNed has also suffered. Reliability is not a strong point, which is I suppose a reason for having alternative links, as is the need to keep the maximum loss within bounds.

Interconnectors are responsible for the largest chunk of grid frequency events. The worst one in 2023 saw frequency plunge to 49.275Hz on 22nd December. Full details have yet to emerge, but it was started by a 1GW trip on IFA1 that appears to have cascaded elsewhere with anecdotal reports suggesting significant wind generation knocked offline in Scotland temporarily. Pumped storage and “OTHER” provided the main response, but batteries do not seem to have responded quite as they have on previous occasions. The largest trip was the loss of 1.4GW of imports on NSL in June, but fortunately the grid was running over frequency at 50.1Hz at the time so the frequency decline was to less challenging levels of about 49.6Hz.

I have been working up similar monthly charts at hourly resolution for 2023, which allows better examination of the effects of overnight surpluses of wind, rush hour shortages etc. and some linkage to pricing, although circumstances after gate closure can lead to disadvantageous SO-SO trades, which David Turver looked at here:

https://davidturver.substack.com/p/the-great-interconnector-swindle

Market behaviour has changed as the crisis abated. In particular, exports to the Continent were driven by high renewables output rather than French shortages. Our trade last year with France included some 160GWh of counterflow on Eleclink and IFA1, with one exporting while the other imported, sending electricity round in circles, and adding 160GWh to exports and imports. These events were frequent – almost daily, and often lasted up to several hours. The worst case saw the entire 1GW capacity of Eleclink being used in counterflow, though usually such flows were 500MW or less.

Trade with France valued at hourly day ahead prices was

GWh Eleclink IFA1 IFA2 France

Import 4,648 7,159 3,803 15,610

Export -813 -1,265 -675 -2,753

Net Import 3,835 5,894 3,128 12,857

Import £95.07 £96.78 £98.37 £96.66

Export £93.53 £83.98 £87.46 £87.65

Utilisation 62.3% 48.1% 51.1% 52.4%

The other Continental links:

GWh BritNed NEMO NSL Viking

Import 4,262 3,983 8,942 64

Export -1,587 -1,003 -414 -12

Net Import 2,675 2,981 8,529 52

Import £104.09 £99.15 £99.27 £68.07

Export £79.19 £79.63 £37.33 £70.45

Utilisation 66.8% 56.9% 76.3% 0.6%

Ireland

GWh E-W Moyle Ireland

Import 239 422 661

Export -1,915 -2,454 -4,369

Net Import -1,676 -2,032 -3,708

Import £107.72 £103.45 £105.00

Export £86.80 £91.21 £89.28

Utilisation 49.2% 65.7% 57.4%

Overall

GWh Total GB

Import 33,522

Export -10,137

Net Import 23,385 =4,984MW on average

Import £98.70

Export £84.16

Utilisation 59.3%

Valuing the trade at Balancing Mechanism SSPs rather than day ahead prices would show a more disadvantageous pattern, I suspect, but BM reports doesn’t make it easy to extract them. It is clear that already we tend to be net exporters at low prices associated with general renewables surpluses, and importers at higher prices when renewables underperform. That picture is set to be accentuated as renewables capacity expands both at home and abroad. The implication is that consumers are subsidising cheap (even negative price) exports via ROCs and CFDs that don’t even benefit them. This chart which shows the cumulative export and import ranked by price at 1 percentile intervals illustrates:

https://i0.wp.com/wattsupwiththat.com/wp-content/uploads/2024/02/IC-Trade-by-price-Cum-1707786457.4989.png