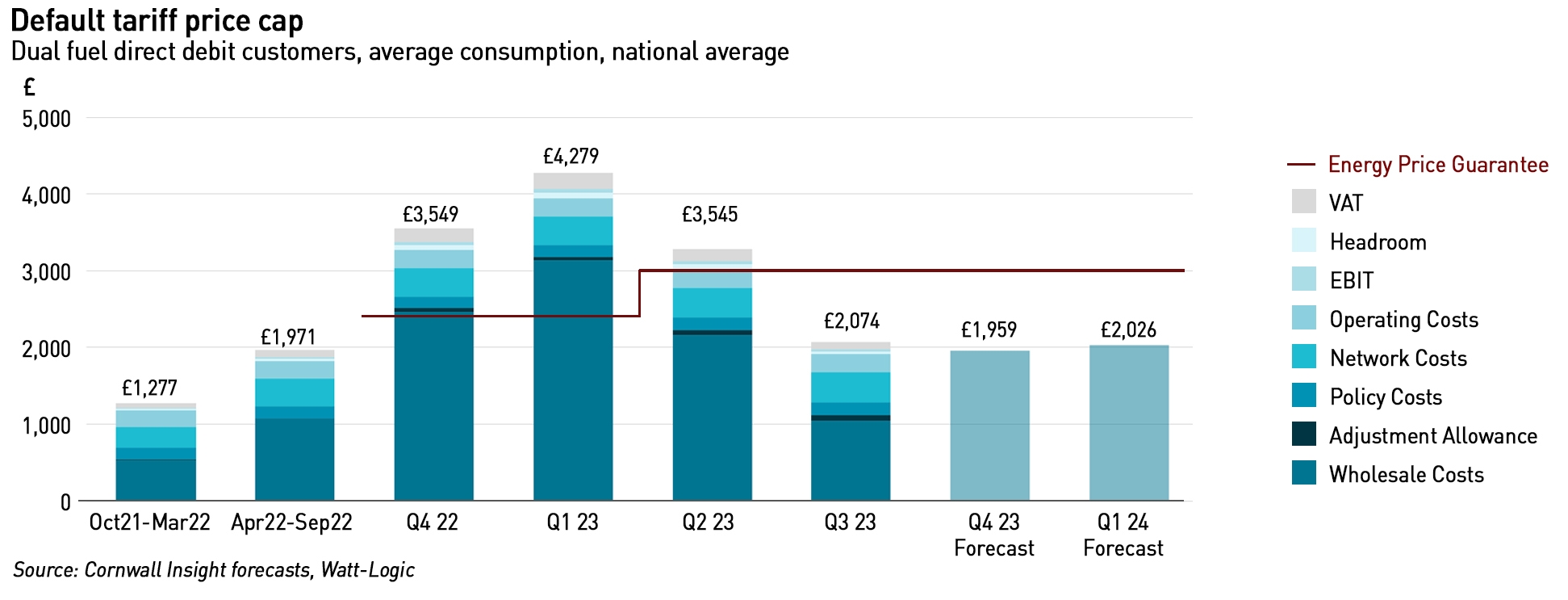

On 25 May, Ofgem announced the new price cap level that will apply from 1 July. The cap level is to fall from £3,280 now to £2,074 for a typical dual fuel household. Of course, consumers currently benefit from the Energy Price Guarantee (“EPG”), which has limited bills to £2,500 per year assuming an average consumption level. This reduction in the price cap will see it falling below the EPG, and raises the prospect that the market might re-open with suppliers offering fixed price deals, leading to a return to competition and switching.

Despite this welcome reduction, households will still be paying more than double the £1,042 they were paying in the Winter of 2020/21. There is a widespread expectation that prices will remain at roughly this current level for the next couple of years, which is causing concern to energy poverty charities and intensifying calls for a social tariff.

Price cap falls significantly but further reductions are unlikely and prices may yet rise again

The reduction in the price cap is overwhelmingly due to the reduction in wholesale costs which have fallen significantly since mid-December. The price observation period for the new cap period beginning on 1 July was mid-February to mid-May during which time prices fell by around 45%. Cornwall Insight is forecasting that the cap will remain broadly at the current level for the next two quarters.

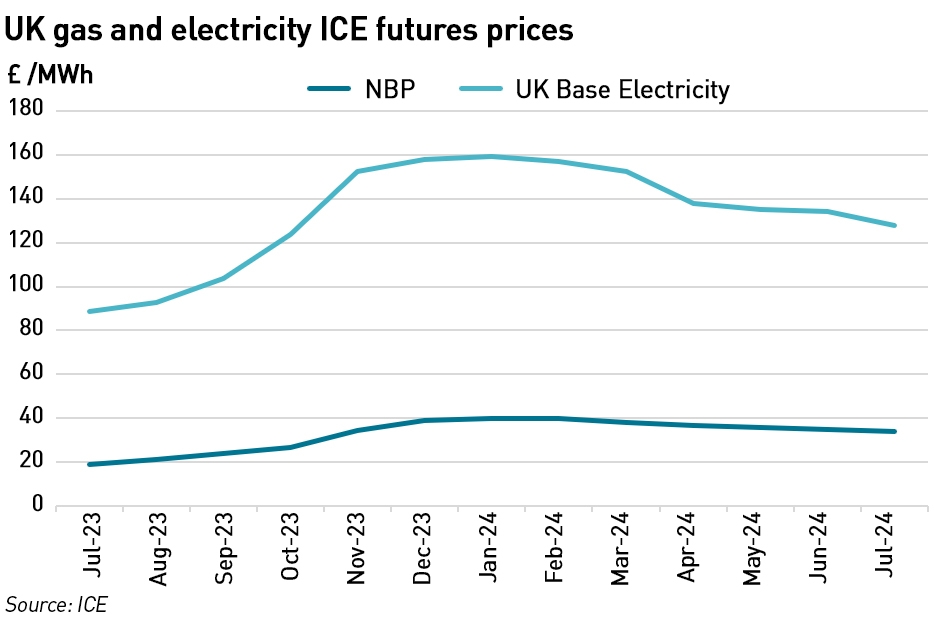

However, current gas and electricity forward curves, indicate risks. Both gas and electricity forwards are trading higher, by successive months, until early next year, when they decline again. This reflects two aspects of the fundamentals: the first is seasonal – prices are almost always lower in the summer than in the winter because demand is lower. The GB gas market is typically well supplied in summer, and is normally exporting to the EU in order to remain in balance, due to a lack of domestic storage capacity. In winter, this reverses as demand rises. Electricity prices tend to follow gas prices.

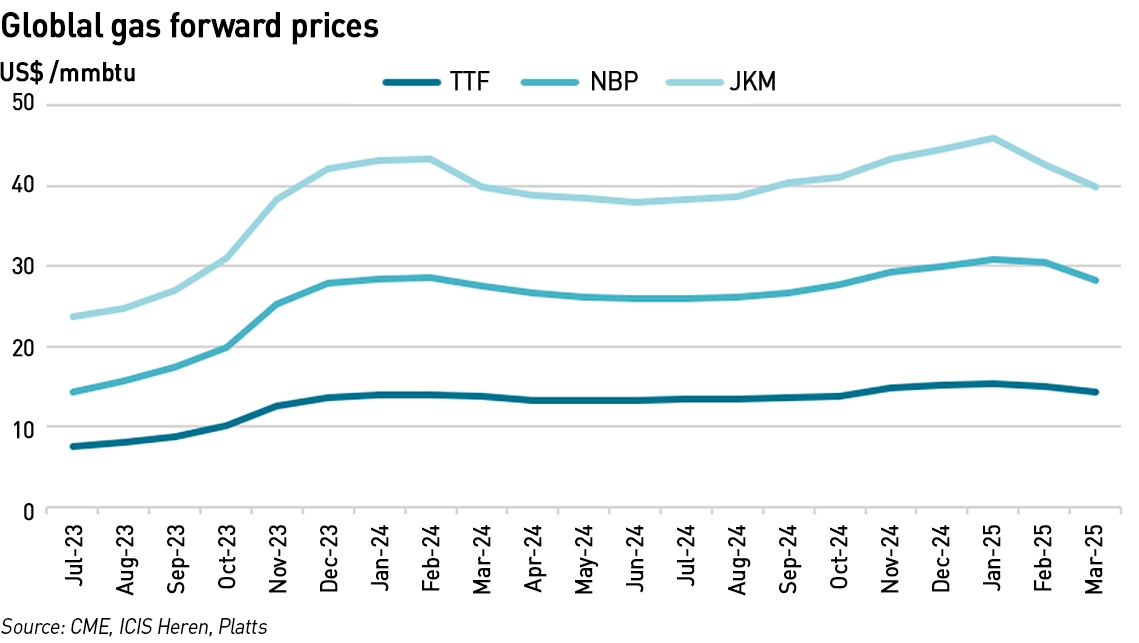

The other aspect of the fundamentals relates to the wider gas balance across Europe. A mild winter allowed the EU to enter the summer gas injection season with above average inventories, but lower prices make it harder to compete with Asian markets for LNG – JKM spot prices are above the European benchmark now for the rest of the year making it more profitable for US sellers to sell into Asia than Europe.

“Europe can’t be complacent as only 40-45% of its winter LNG demand is contracted, narrowing the buffer versus demand upswings or potential disruptions,”

– Patricio Alvarez and Joao Martins, analysts at Bloomberg Intelligence

Imports from Russia continue to be minimal, limited to flows through Ukraine and Turk Stream. Nord Stream continues to be inoperable, and the Yamal pipeline has not returned to east-west flows despite suggestions it might late last year.

Although Japanese LNG demand is falling as the country continues to bring its nuclear power stations back into service (there are now ten up and running), elsewhere in Asia gas demand is rising. India is pressing ahead with the large-scale implementation of LNG import infrastructure, while the Philippines and Vietnam are ready to begin commissioning several LNG terminals this year. Thailand and Bangladesh are trying to secure additional volumes from the market. Chinese demand is also recovering after covid, increasing by 16% in the year to March, although there are some doubts as to the strength of this recovery. While not all of these countries will have the financial fire power to outbid European buyers, the additional competition will put upward pressure on prices.

This means that there are risks to Europe’s gas supplies heading into next winter which could see prices rise significantly. Analysts at Goldman Sachs suggested they might treble by the winter:

“While this lower-than-expected rebound in European gas demand buys Europe more time, it doesn’t solve the market deficit we see lending support to prices next winter and in summer 2024. Even if industrial demand remains sluggish this summer. This is not a guarantee that storage will be comfortable throughout winter, as there is only so much capacity to store gas ahead of heating season,”

– Goldman Sachs research

So far in the price observation window for the next price cap starting in October, prices have continued to fall, but the period has barely begun. Should prices rise, including through the summer – the August and September contracts are both trading above July which is not encouraging, and as expected the October, November and December contracts which suppliers are using (or their equivalent forwards) to hedge the next price cap are all also higher.

In addition, there will be changes to the price cap methodology from October, including a likely increase in the EBIT allowed from 1.9% to 2.4% of the full price cap level, which will add about £10 per year to the average bill. Of course the press has jumped on this as a negative, complaining that “Ofgem wants your energy supplier to make more money”, but the increase is modest and necessary. Ofgem believes that increasing the EBIT margin will be positive for consumers as it will reduce the chance a supplier will fail and therefore the chance consumers will pay the socialised costs of those failures. Although other regulatory changes are also designed to reduce the risks of failure, it is certainly true that when profit margins are low, suppliers struggle to accumulate the reserves needed to see them though difficult periods.

As prices are expected to remain relatively high is a social tariff the answer?

There have been widespread calls, including from Ofgem, for the introduction of a social tariff for energy to protect vulnerable consumers, with many people also noting that the price cap was originally intended to be a temporary measure until “the conditions for effective competition in this market are in place”

“The introduction of a social tariff for energy would be a significant step in the right direction. The funding of it will be a policy decision for the government but if we can get this right and deal with the root cause of the affordability crisis, some of the difficult issues around fitting prepayment meters should no longer be necessary,”

– Chris O’Shea, Chief Executive, Centrica

Age UK recently wrote a Parliamentary Briefing calling for the government to directly fund a 50% energy bill discount for those in “greatest need”, saying this must:

- include automatic enrolment for eligible households

- be universal across suppliers

- sit alongside existing consumer protections

- be accessible for all customers struggling with their energy bills

It said this should apply regardless of how energy is paid for, what type of fuel is used for heating, and whether the household has access to the welfare benefits system. Age UK believes this discount should be paid for through taxation rather than bills to avoid the current situation with other benefits such as the Warm Homes Discount, where people who only just fail to qualify for the support pay for it to be extended to others, thereby making energy less affordable for themselves. The charity also wants households on this tariff to be exempt from standing charges.

According to Age UK, 7 million households are currently in fuel poverty ie more than a third of the country’s 19.4 million households. That represents a significant challenge for any social tariff scheme, and underlines the importance of not trying to fund such a scheme through bills, since it would likely push more households into poverty. Age UK pointed out that Belgium has a social tariff which benefits 20% of its population, where household have a one third discount on their bills – yet the scheme it is proposing for the UK is both more generous and more wide-reaching, and would be difficult to afford.

A paper by the University of York for the Child Poverty Action Group suggests that if the objective is to mitigate 50% of fuel stress it would be necessary to extend mitigation to 70% of households. Previous studies by the University had explored two options for delivering a social tariff: a fixed £x discount in £ terms on bills (eg equivalent to abolishing the standing charges/prepayment premiums), or a fixed discount in £ terms on the bills of low-income consumers (but the question is where to draw the line). In this study, it considered a third option, reducing bills for lower-income households by a percentage which declines as income rises. This is similar to a previous suggestion I have made of tiered support, where households receive different levels of support depending on their income levels. My suggestion was to link it with income tax bands as this would be relatively quick to implement, but I recognise that it has limits relating to households with more than one wage-earner.

The study found that in principle, this approach would help to bring the fuel poverty rate down from 20% to 9% at an additional cost of £24 million per week (which translates to £1.25 billion per year) to taxpayers. However, it goes on to say that “operationalising such a system requires a reliable way for the government to identify low-income households, which is not straightforward”, which also reflects the downsides of my proposed solution – I came up with a model that had obvious drawbacks but was at least well defined. The York study does not attempt to offer a means of making the necessary household selections.

Of course, even a selection based on income tax brackets would miss people with specific needs such as those who have average incomes but very large energy bills due to the need to run medical equipment in the home. But these are a minority of people who are likely to be in regular contact with health authorities, so a medical certification system could be added so that people having such medical needs could receive a certificate from their doctors that would allow them to benefit from the social tariff.

However the idea of a social tariff does not have universal support, with some critics pointing out that it narrows the idea of vulnerability to purely financial considerations. This is indeed true – vulnerability, as I have often said before, encompasses much more than just poverty. Disability, poor literacy and numeracy, and digital exclusion are all other major causes of vulnerability, and there are temporary causes as well such as ill health or bereavement. I understand this very well, since I live with a disability and have recently suffered a bereavement (one of the reasons the blog has been quiet recently) but although I do not consider myself to be vulnerable it is certainly true that these things take a lot of time and energy, leaving less time and energy for other things. Personally, I’m not interested in changing my supplier, but I am now thinking about whether it might be time to look at fixed rate deals, but that means finding the time to look at the options and do something about it.

As the energy market re-opens, if Ofgem up to the challenges ahead?

After 1 July, the Energy Price Guarantee will no longer be lower than the price cap, so most people will go back to paying a market price for their energy. There is also an expectation that fixed priced deals will also be offered again by suppliers, providing a basis for competition. So there is an expectation that the market may begin to revive, but the question is by how much? At the start of the energy price crisis in late 2021, I questioned whether Ofgem was meeting its statutory duties under the price cap legislation, specifically in relation to ensuring the cap is set at a level which:

- creates incentives for holders of supply licences to improve their efficiency;

- sets the cap at a level that enables holders of supply licences to compete effectively for domestic supply contracts;

- maintains incentives for domestic customers to switch to different domestic supply contracts; and

- ensures that holders of supply licences who operate efficiently are able to finance activities authorised by the licence.

Of course, Ofgem is of the opinion that these objectives are merely guidelines and that ignoring any or all of them is at its sole discretion. However, the regulator has been strongly criticised for its regulation of the retail market, and although it was rarely stated explicitly, if it had followed these objectives, some of the problems might have been avoided.

Later this year, Ofgem expects to increase the EBIT margin suppliers can earn. This is helpful, but probably does not go far enough – suppliers need to earn decent profits to enable them to build reserves ahead of future market volatility, and to provide a cushion to support innovation (without which suppliers are likely to continue to be risk averse with their business models). However, the idea that suppliers should earn any profits let alone more profits is deeply unpopular, partly because energy has become so expensive – something for which suppliers cannot be blamed – and partly because other energy companies, in particular oil and gas producers, have earned record profits in the last couple of years.

But the solution to expensive energy is not to cut supplier profitability. If there is a genuine consensus that suppliers should not earn profits then the industry should be nationalised – this is unlikely to be in the best interests of consumers, but it is the only logical approach if people want energy to be treated as a social good. The alternative is to reform the market. Sensible reforms would be to strengthen prudential regulation to reduce the risk of supplier failure, but to reduce other aspects of the regulatory burden, in particular the non-supply activities imposed on suppliers. I continue to be of the view that green levies should be recovered through general taxation, that the Warm Homes Discount should be rolled up into the benefits system, and that the Energy Company Obligation should be the responsibility of local government. The smart meter rollout should be completed by distribution network operators. And the price cap should be abolished, freeing suppliers to set their own prices on whatever basis they see fit.

By reducing the regulatory burden and allowing suppliers to become profitable, the market will become attractive for new entrants with genuinely new business models. Consumers will have wider choice, with options to chose based on price, or based on different types of value-added services. Protection of the fuel poor should be the responsibility of the government, through a tax-funded social tariff, which provides a basic amount of energy at cheap rates (with sensible exceptions for people with health-related high energy needs). This basic tariff would be a simple, unique, price-based offer – there would not be multiple variations as expected in the rest of the market.

I also continue to believe that the retail energy market should be regulated by the Financial Conduct Authority under the supervision of the Treasury. I have little confidence that Ofgem could design the necessary regulatory reforms. Ofgem has a very wide remit, and despite being one of the largest energy regulators in the world by headcount, it struggles to deliver its various mandates because it has too much to do. High staff turnover does not help. Neither does its persistently hostile tone towards suppliers.

As market fundamentals improve there is scope for a proper retail energy market to develop. Can Ofgem rise to the challenge?

You make valid point as usual. Judging by past results it would seem that Ofgem are incompetent at the core. They have botched the management of retail suppliers and we all paid for this mess, the mismanagement of the Smart Meter project with different specs and having units fixed to suppliers reeks again of incompetence and again we are forced to pay for mess. Ofgem should have separated the price of electricity from the cost of gas and their inability to manage the pricing of wind farms generation fees is close to criminal.

With the highest priced Electricity in Europe we are a county have been stitched up and Ofgem need to take responsibility.

I say they are not fit for purpose and should be closed down.

Separating the cost of gas from the cost of electricity actually isn’t within Ofgem’s powers. That would require a fundamental change in market arrangements which is a matter for Government and is being considered as part of the REMA process. However there are no easy or quick fixes and any market change would likely take 5-7 years to implement. That’s why the Government has addressed this issue by imposing a windfall tax on generators other than gas generators to claw back some of the excess profits they have earned. This is a good idea for windfarms in particular who also benefit from generous subsidies, but a bad idea for nuclear since there is a need for new investment if necessary life extensions are to be secured.

I’m no fan of Ofgem, but it’s important we criticise it for the things it can control, not the things that are outside its remit.

We don’t have a social tariff for food, so why is one appropriate for energy?

In fact the Government has been toying with the idea of price controls in food, but they are unlikely to work because food producers can choose to sell food in other markets ie not import into the UK and export home-grown food. Infrastructure constraints limit or outright prevent electricity and gas produced in Britain from being exported.

Energy is also a basic necessity. While you can say the same for “food” as a broad category, how do you go about deciding which foods exactly are essential and should be subsidised? 80% of households use gas for heating and close to 100% of households use electricity, so the market is quite different and support measures can be defined much more easily .

Whatever the outcome I remain very concerned for the wellbeing of consumers who use electricity for heating. We assume that there is some path forward, supported by this government, to move domestic heating away from fossil fuels and also assume that this will be met by heat pump systems, modern night storage devices and some direct, resistive, heating. There is now a choice of new, very efficient, thermal storage “boilers”* that heat “bricks!” or use phase change materials, using off peak electricity. These generally need 7 hours of charging and then supply heat as required using conventional water filled radiators. However, a bizarre situation exists where potential customers can have no certainty what the cost of charging at night will be and are disincentivised to commit capital to moving from gas. I have seen the day to night tariff ratio varying from over 5:1 to 2:1 and the suppliers seem to take full advantage of altering the off peak tariff by much more than that of gas. There seems to be no control or oversight of this aspect of domestic energy supply, and as a result, the most vulnerable users are punished. I realise that this is not the main subject of this post but there is a connection with how the price caps and energy market operates.

We assume that the government is supporting a path away from fossil fuels and that OFGEM haa an oversight of the market and has a similar interest. It looks to me though that the 10% or so using electricity for heating are completely forgotten. As an example of the mixed messages we are getting, a neighbour of mine moved from oil to air source heat pumps. Inevitably though backed up with a log burner.

* Thermal storage systems will be needed alongside heat pumps in a zero carbon future and local storage using the existing electrical distribution network is the most cost efficient way of coping with diurnal variations in domestic energy demand.

The main day-night tarff is still the Economy system and that is designed around the assumption that the heating is electric and specifically using storage heaters. When it was first introduced, it reflected the pattern of usage, with people using electricity at night to “charge” the heaters, but now storage heaters are much less common but the tariff approach has not been adjusted to reflect the fact that people are just using electricty during the day for heating. It’s a very expensive way of doing things, and I don’t think many people understand how the Economy tariffs work and why.

Indeed, not may people do. Perhaps the junior school curriculum should cover energy use in detail. There will be a time when most domestic heating is powered by electricity. Wind has the unfortunate habit of blowing at night so diurnal storage is essential. There is work to use high temperature thermal storage which powers steam turbines, linked to windfarms. But it is more efficient to do this storage in people’s homes. The losses over the whole cycle are less, and the consumer pays for the hardware. I have 35 Yr old storage system that stores 100kWh which works just as efficiently as it did when new (GEC Nightstor 100) and a UK company (Tepeo) is now selling a smaller similar system more suited to modern housing.

The problem that I tried to describe is that the Eonomy 7 tariffs vary much more than those of gas, both from supplier to supplier and year by year. Suppliers know this and take advantage of those who are unable or unwilling to change supplier every year.

The number of households in the UK is more like 30 million.

You persistently talk about profits in supply as if they exist. Ofgem’s segmental statements show that they do not. The average margin in the most recent statements for 3 large suppliers (BG, EdF and SP) in their residential supply businesses was nearly -5%. That’s way below Ofgem’s theoretical 1.9% EBIT margin. Increasing the theoretical EBIT allowance in the price cap model to 2.4% will not increase profits it will only reduce losses.

Thanks, I used the families stat by mistake – there are around 19 million families….https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/families/bulletins/familiesandhouseholds/2022

Various forms of a ‘social tariff’ have been proposed in general terms, typically involving a subsidised retail price for qualifying customers. While such a design would alleviate the financial burden of high energy prices, it will dull the incentive to reduce energy usage, which is the very response that ought to occur in response to higher energy costs. Rather than a subsidised price, a direct payment to qualifying energy customers, without adjusting retail tariff rates, would both lessen the financial stress and maintain the marginal incentive to reduce energy use. Such an approach also has the advantage of ease of implementation, with the Warm Home Discount or Energy Bill Support Scheme (EBSS) being easily amendable to a targeted direct payment. Price inflation of the basic goods of energy and food has exceeded the general level of inflation, and as these essential goods form a larger proportion of the expenditure of those on low incomes, the ONS estimates the gap between the rate of inflation between the richest and poorest households to be the highest since 2009 . Although energy prices have decreased considerably in recent months, most of the decrease will be realised in lower government expenditure on energy subsidies, specifically the Energy Payment Guarantee (EPG), and retail prices over the coming year are likely to remain similar to the current subsidised prices. In fact, with the intended withdrawal of the EBSS, energy costs for the coming winter will likely exceed those of winter 2022/23.

Targeted support for energy bills is the affordable and effective solution until such time as energy prices return to historical levels. The need to support the poorest energy customers through this period of high prices is widely understood, with the solution proposed often being a ‘social tariff’ entailing a discount to the energy tariff unit rates of qualifying customers for some or all a customer’s usage. While addressing the problem of affordability, this approach has several drawbacks:

1. The price signal of high energy prices is dulled. Retail prices are high because the marginal cost of gas is high. If this price signal is lessened, a more than economically optimal level of energy will be used, i.e., the country will be poorer as a result. At present, the price signal serves a useful purpose in reducing demand in response to a high marginal price, with domestic customers having cut energy usage last winter, and this demand response has helped to bring wholesale prices down. The economic reality of the price signal, therefore, has a useful purpose in ensuring the best allocation of resources for maximising utility, and ought to be maintained.

2. Preclusion from innovative tariff and product offerings. Decarbonising the energy system will require innovation in retail services to smooth demand over the day. Half-hourly pricing, solar and battery systems, and demand reduction incentives all rely on accurate price signals, and a social tariff of reduced retail prices would preclude the poorest in society from taking up products that could benefit them financially.

3. Poorly targeted support. Higher users of energy are not always well off and should a social tariff take the form of subsidised initial units of energy, i.e., a lower price for the first x units in any given period, many of the poorest in society, such as some pensioners and disabled people, who are often high user of energy, will still face very high energy bills.

Rather than subsidising rates, a direct payment to qualifying customers offers a superior solution in my opinion to the problem of high energy prices for poorer households. A direct payment to customers, while leaving unit rates unchanged, maintains the price signal necessary for an economically optimal energy usage, and allows customers to participate in innovative energy products and services. There is a further advantage if the subsidy is applied directly to a customer’s bill or prepayment meter: Utilita’s analysis of prepayment customer self-disconnection shows that propensity to self-disconnect approximately halved between the summer and winter of 2022, even as prices and usage increased, due to the application of EBSS payments directly to customers’ prepayment meters.

A direct application of a subsidy, therefore, rather than lower prices, is likely to be more effective in keeping prepayment customers’ energy supply uninterrupted. The development of the EBSS scheme has brought about a mechanism that lends itself very well to applying a direct payment to qualifying customers on a monthly basis over the winter months, which could be effectuated with little modification to the existing scheme. A further advantage of a direct payment is that it can be quickly varied over time to offset the change in energy prices, increasing should prices rise and reducing to nothing should energy prices return to historically normal levels. Unaffordable energy prices for poorer households is a problem that will persist even with the recent reduction in wholesale prices. A social tariff that subsidies some or all a customer’s energy usage has several disadvantages that can be avoided with a direct payment, something that can be implemented quickly and easily, and certainly in time to avoid a crisis of affordability for poorer households next winter.

Russian LNG continues to flow into Europe. There is a nice question what they will do with the expansion of capacity. Good update here

https://www.highnorthnews.com/en/eu-begins-consultations-curb-inflow-russian-lng

Spain seems to have been a big importer of late. I caught simultaneous discharges at Bilbaο, Ferrol, and Sagunto recently. I think there will be reluctance to cut Russian flow.

On topic: there is no way OFGEM will act in consumer interests. They have secured Parliamentary endorsement to be a Net Zero delivery mechanism as their primary duty, which means that any vestigial support for consumer interests left from the Ed Miliband 2010 Energy Act is erased. Brearley will be free to impoverish consumers any way he sees fit. OFGEM needs to be completely disenfranchised.

I think it’s time we had a consumer oriented body, and one with some teeth to overrule OFGEM and DESNZ. Might even be worth trying to launch a No 10 petition to that effect. Wrap in Howard Cox’ Fair Fuel campaign angled at supermarket profiteering as well.