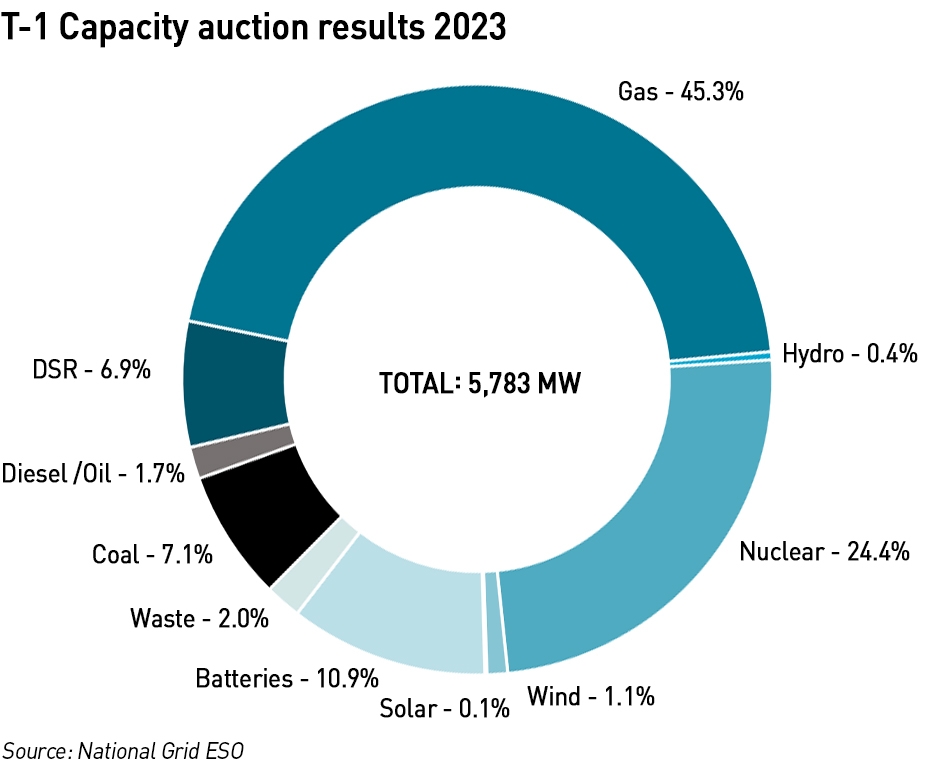

Last week saw the T-1 capacity market auction clear at its second highest level ever of £60 /kW/year, down from £75 /kW/year last year when the auction cleared at its maximum price since the procurement target was higher than the amount of capacity participating (some 365 MW having withdrawn prior to the auction). 5,783 MW of capacity was procured this year compared with 4,996 MW last year. 341 MW of capacity was unsuccessful this year (last year all assets that remained in the auction secured contracts).

“ESO have [sic] procured more capacity than ever before in a T-1 auction and the result is a high clearing price, though the price is likely cheaper than that of the Winter Contingency contracts seen this winter. The key beneficiaries of this auction are the larger units Medway and Corby that did not secure contracts in the prior T-4 auctions but are being kept online by the prices in this T-1.

It demonstrates that, going forward, ESO is keen to reduce their [sic] reliance on interconnectors and become more confident in their [sic] ability to resolve supply issues domestically…New build-battery units have also benefitted from the higher prices, with more than half of the new build capacity that was awarded contracts being from batteries. Many of these units will see their start dates brought forward in order to make the most of the high clearing price.”

– Phil Hewitt director at EnAppSys

Despite changes to the capacity market rules that removed barriers to participation for mothballed plant, the former Calon CCGTs, Severn Power and Sutton Bridge, did not enter the auction. However, two units at Hartlepool and one unit at Heysham 1 did secure contracts which was unexpected since both are scheduled to close in March 2024. EDF has been considering extending the lives of these plants, and securing well priced capacity contracts might provide an incentive, off-setting the negative impact of the windfall tax which also applies to nuclear generators. But EDF could fulfil these contracts without any meaningful investment, either by simply selling on its obligations in the secondary market, or taking them out of regular use and simply managing the fuel to ensure there is enough to cover any potential system stress event during those additional six months.

Of the remaining coal plant, only Ratcliffe unit 3 entered the auction and secured a contract – the other three Ratcliffe units already hold contracts for the 2023-24 delivery year from the T-4 auction in 2019. Despite having a capacity contract, Unit 1 had been due to close last September, but participated in the coal contingency scheme this winter, which expires at the end of March – Uniper has been kind enough to confirm that it intended to re-allocate that contract to Unit 3 had the closure gone ahead. Since Unit-3 has now secured a contract for next winter in the T-1 auction, all four units will remain open until the statutory closure date for coal of September 2024.

The last two coal units at Drax which also participated in the winter coal contingency are still expected to close at the end of March although they could in theory remain open for longer. The two units at West Burton A will certainly close at the end of March as they have reached the end of their lives.

None of the interconnectors participated since they had all secured contracts in the T-4 auction for the 2023-24 delivery year.

The other interesting aspect of this T-1 auction is that an offshore wind plant secured a contract for the first time. It’s only 32 MW at SSE’s Seagreen project. Four other units were unsuccessful. Eight onshore wind plants secured contracts with a combined capacity of 33 MW.

As with the interconnectors, the inclusion of intermittent renewables, and in particular wind, is questionable. System stress events are most likely to occur in periods of low wind output, so regardless of intent, these wind assets may not be able to contribute. They could co-locate with batteries to protect themselves against this risk, but as batteries can participate in the auctions directly, this seems inefficient. As I understand it, they are just assuming there will either not be a system stress event – there have been none so far – or that they will pay the penalty if they cannot generate at the time. This strategy will become increasingly risky as wind penetration grows and the system become more vulnerable to periods of low wind output, however, at the moment, penalties in any year are capped at the annual capacity income, so a failure to deliver simply means that no capacity market income is received for that year.

The risk with interconnectors is that they are exporting at the time a system stress event occurs. This is not a risk for the owners since the assets would meet the availability criteria (in that they are capable of importing) but there is no mechanism to ensure that they are importing rather than exporting. So, this is a significant system risk, and one which is compounded by the high weather correlation with most of our connected markets which means they often experience low wind output at the same time we do. Norway is the exception but NSL only trades on the day ahead, so within-day changes to output cannot be managed through intraday trading on NSL. There are no plans for this to change in at least the next year.

Capacity market rules being evaluated in new consultation

The Government has been consulting on the future of the capacity market with a Call for Evidence last summer and a new Consultation launched last month. In the Call for Evidence, it was noted that, as a consequence of Brexit, the requirement to implement direct cross-border participation in the GB capacity market was no longer part of domestic law (having been revoked from retained EU law). It also noted that the arrangements necessary for implementing direct cross-border participation have not yet been fully established in the EU either. This means that the Government can consider a range of options for cross-border flows in the capacity market, including the current indirect model for interconnector participation, or a direct model involving non-domestic capacity participating directly in the GB capacity market alongside domestic capacity.

There were 39 responses to this part of the consultation: 14 preferred to retain the current indirect model, 11 preferred a direct cross-border participation model, 2 argued for maintaining the current indirect approach in the short term before moving to a direct model, 5 argued for an approach involving only domestic capacity competing in the GB capacity market, and 5 argued for the immediate exclusion of interconnectors. 2 responses were neutral. My vote would be for the exclusion of interconnectors from the capacity market since it is not possible to ensure they are importing during a system stress event, and could even make matters worse by exporting (although in practice, National Grid ESO would likely enact emergency measures which would prevent this).

Most respondents opposed early action on interconnectors. Concerns were raised that interconnector participation may be deterring investment in firm domestic capacity. Some responses suggested that interconnectors are being overcompensated by benefiting from a cap and floor regime alongside access to the capacity market, as well as being exempt from transmission charges. One respondent argued that interconnectors may be displacing firm domestic capacity in auctions to the detriment of GB’s future electricity security. Views I tend to share. Unfortunately, the new consultation is largely silent on the topic, instead focusing on other areas raised in the Call for Evidence, including the penalty regime and if/how the capacity market should be aligned with wider net zero ambitions.

“The impact of increased geopolitical uncertainty on energy security and the government’s clear ambitions for power sector decarbonisation have strengthened the rationale for taking action to reform key aspects of the CM’s design,”

– Department for Business, Energy & Industrial Strategy

In terms of penalties, the Government is minded to make one change to strengthen the penalties for non-delivery and that is to adjust the calculation multiplier from 1/24 to 1/4 thereby increasing the value of the charge. However the annual caps will remain the same, reducing the impact of the change. The penalty charge would now be:

Penalty rate (£ /MWh) = Clearing price (£ /MW) x 1/4

On the de-carbonisation objective, the Government is minded to make changes recognising the fact that new-build unabated gas can earn contracts which extend beyond 2035, the date by which the electricity system should have been de-carbonised. It views hydrogen and CCS conversion as the main de-carbonisation pathways for unabated gas generation in the medium term.

The capacity market currently contains an emissions intensity limit and a yearly emissions limit. New build CMUs must meet the emissions intensity limit to secure multi-year agreements, whilst from 2024 existing capacity must comply either with the intensity limit, or the yearly emissions limit. The current intensity limit is 550gCO2 /kWh which is below the level emitted by coal, diesel and some older gas plants, but above the level of most gas plants. CMUs that do not meet the intensity limit, can still participate if they meet the yearly limit of 350kgCO2 /kWh, which equates to around 400 operating hours per year for an oil or diesel plant, less for coal plant and more for an older gas plant, depending on the plant efficiency. CMUs which do not meet either limit, cannot participate in the capacity market.

The government proposes that from 1 October 2034, for new and refurbishing units which secure capacity agreements after this rule change comes into force, intensity emission limits would decrease to 100gCO2 /kWh. The intention is for low-carbon technologies that have some residual emissions, such as CCS-enabled generation, to meet the limit while unabated gas probably would not.

From 1 October 2034, the yearly emission limits for new and refurbishing capacity, would be set at the same level as that which existing capacity can access if it does not meet the intensity limit for existing plant. The yearly emissions limit is already set at a level which allows unabated gas to operate with peaking profiles without constraint but prevents non-peaking (ie mid-merit or baseload) operations. The limit would be set to allow for additional running hours in unusual years where necessary to safeguard security of supply.

The purpose of the two limits together would be incentivise unabated gas plants to either abate by 2035 or operate a limited peaking profile beyond 2035.

Of course, all of this assumes that abatement is possible and economic over that time frame. The track record for power-CCS to date has been extremely limited, with reliability problems and capture rates falling well below expectations. The use of hydrogen would rely on hydrogen being available through the gas grid. It may be that neither abatement mode is practical by 2035, but in that case the Government would need to adjust the limits to ensure that unabated gas plant can continue to run if necessary for security of supply reasons.

The capacity market is more important than it has looked to date

I believe we are entering a danger zone in the electricity market, with the closure of conventional plant and the growth in intermittent renewables. We have seen time and again in the past couple of years that wind output can be very low (below 1% of nameplate capacity) and that periods of low wind can be both prolonged and widespread, limiting the scope for imports to fill the gap. Currently there are no storage solutions available in GB to manage this intermittency.

This week EDF has announced massive further cost over-runs at Hinkley Point C and signalled that further delays are likely, possibly to late 2028. The cost has now ballooned to £33 billion compared with the £18 billion estimate when the final contracts were signed in 2016. EDF has yet to open an EPR in Europe – Olkiluoto has still not opened despite expectations it would be completed in 2022. Now it won’t be open until the end of March. EDF has also warned that it may end up paying a larger share of the Hinkley Point costs under the agreement it has with CGN surrounding cost over-runs. This does raise some questions about the prospects for Sizewell C and how much appetite EDF has for another first generation EPR against the backdrop not just of its problems delivering this reactor but also with the existing French fleet.

Based on current plans, all remaining coal plant will close by the end of September 2024, as well as 2.3 GW nuclear (see above). That means that September 2024 could see 4.3 GW of capacity closing, an amount larger than the current winter capacity margin.

Although there has never been a capacity market system stress event, this is in part because once a plant has a capacity contract it is in the market, so the contracts reduce the risk of system stress events happening in the first place. But there are risks because of the treatment of interconnectors and the inclusion of intermittent renewables (although this is currently at low levels, it may grow in the future). Last summer showed that system tightness can occur in the summer as well as in winter, which is a big problem since thermal and nuclear plant tends to take maintenance outages in the summer. If system stress can occur year-round it will be difficult for operators to schedule maintenance and this itself could push up prices as the risk of penalties grows.

It is important that de-rating factors reflect a proper view of likely plant availability, and that the amount of capacity being procured is large enough to cover the deficits that arise when wind output is low. As we move through this decade, the assumptions underpinning the energy transition will be challenged – the costs of getting this wrong could be significant.

It seems like Private Fraser was right – just 80 years ahead of his time.

How much of a risk is any generator really taking if it fails to supply when the ESO calls upon it?

Once again a useful informative post that raises several issues.

Capacity markets turn a simple issue of covering the intermittency of wind and solar into a complex and no doubt profitable one. It is incredible that wind and solar generation can participate. Inter connectors for similar reasons should also not participate.

There is much chatter in the current global situation on decreasing reliance on other countries and resolving matters domestically. Yet NGESO’s Future Energy Scenarios (FES) dramatically increase inter-connector capacity and make increasing use of them to try to cover intermittency issues, swinging them around wildly to cover our requirements. What do the parties at the other end think of this?

Conditions of low wind and solar during winter cold spells are now being highlighted but my analysis shows a far greater problem is periods of maximum wind and solar during the summer months. The supply far exceeds the demand. Yet the FES does not curtail any wind or solar output (indeed it is very optimistic on capacity factors) because it requires all of that output to meet the total annual energy consumption.

To allow unabated gas (or for that matter abated gas) to run for “Security of Supply issues” is a real cop out. We are apparently not concerned over CO2 emissions. Indeed setting a 2035 cap at 100g/kWh is only just below the current average annual emissions level.

Rather than a low carbon future from a balanced portfolio we are aiming for a totally renewable future- for renewable read only intermittent wind and solar. The target has become a dramatic increase renewables (wind and solar) not a reduction of CO2 emissions to zero. Indeed the Welsh Government publishes annual monitoring reports congratulating itself on the increasing percentage of renewables and yet is totally silent on CO2 emissions (which have remained unchanged since 2006)

Present policy leads us to an expensive and insecure future that is also nowhere near net zero.

The policy is no doubt popular amongst those who see profitable business opportunities or have a deep faith in renewables.

How can this be allowed to happen?

I stopeed reading the FES a couple of years ago. I ran some analysis which I never got round to publishing but I looked at four metrics which had been included in the FES for most of the 10 years I looked at and found the out-turn was frequently at the edges of or outside the boundaries set by the scenarios. I asked the FES team at ESO about this and it turns out that they don’t back-test their methodology.

I think the FES has declined into a political virtue-signalling exercise designed to show that ESO is being proactive in delivering net zero rather than being a tool for understanding the potential future parameters of the grid (other than that any forecast sits within the set of possible future outcomes).

As to how this can be allowed to happen…policymakers are not engineers. They have in mind a goal – in this case net zero – because some lobbyists with loud voices persuaded them its necessary and they enact policies they think will deliver it. They listen to consulants who earn a good living telling them what they want to hear rather than what they need to hear. The likely outcome will be blackouts as seen across the US this year. We ae degrading security of supply in the pursuit of net zero forgetting that blackouts can also cost lives.

Unfortunately the FES is not just of academic interest. It has real world significance. It is used as an evidence base by the Welsh Government to set future energy policy in conjunction with their advisors REGEN.

I have analysed the FES 2022 in great detail and am currently asking the team questions as to its assumptions and the validity of its conclusions. The scenarios look at an extremely limited range of possible options and are based on energy. The electricity network is a power system. I appreciate the position NGESO are in but they risk huge reputational damage (perhaps state ownership is their safest home).

To try and counteract group think and preconceptions I am starting to make available a simple simulation that can be played in the form of a game allowing players to experience and resolve the issues for themselves.

Interconnectors were excluded from the auction by being given a zero credit. I suspect there is capacity that was not previously fully committed at T-4 auctions, but I would have to check. Battery credits depended on duration, potentially earning 95% at 6 hours. However, earning £10/kWh per year is not going to go a long way towards paying off costs now that Tesla Megapack prices are in the region of $500/kWh. Battery economics are increasingly challenging for durations above 2 hours, and that only works in the very volatile markets we have had during the crisis. It is hard to see batteries having a real role to handle larger scale renewables intermittency, rather than being purely peaked sources with added ancillary services. I note that theESO has been willing to tolerate fairly frequent excursions beyond +/-0.2Hz because battery Dynamic Containment has been very effective in preventing further deviation at the levels of challenge posed by losing 1GW of interconnector or windfarm.

I see the T-4 auction has concluded in Round 3 at £60-65/kW/Yr. Double last time. It will be interesting to see what capacity types it has procured.

I also didn’t check if there was uncommitted interconnector capacity in the T-4 – I just noted that they were all there. Interesting to see the higher T-4 price…that’s what I would expect to see but I also thought AR4 would be higher and it wasn’t…auction behaviour isn’t always rational!