Today I took part in a webinar The Energy Crisis: Causes and Solutions hosted by Net Zero Watch (it can be viewed on YouTube here: https://www.youtube.com/watch?v=J9sBOWYkv1M)

Below is a copy of my opening remarks to which I have added some charts for illustrative purposes that were not included in the webinar, and links to relevant previous posts…

Hello everyone, I’m delighted to participate in this event today.

We’re experiencing what the press is calling a “cost of living crisis”, largely driven by rapid increases in energy costs. There are three factors at play: two which have received a lot of attention and one which has not.

Last autumn we saw global gas prices shoot up as a result of an asymmetric response to the pandemic: supply was cut by more than demand and took longer to recover. Combined with a cold winter in Europe and then heat waves across much of the norther hemisphere last summer, Europe went into last winter with very low gas inventories and prices ramped up as we had to compete with Asian buyers in the LNG markets.

The expectation was that this situation would stabilise sometime in 2022, but the Russian invasion of Ukraine de-railed those expectations. With Western buyers now wanting to stop trading with Russia, new gas projects will need to come online to replace those volumes, and that is going to support prices for much longer.

So while covid and the war have both been very well publicised, the other pricing dynamic has received much less attention and that is the effect of de-carbonisation. Many people mistakenly believe that renewable energy is cheap and reduces energy prices.

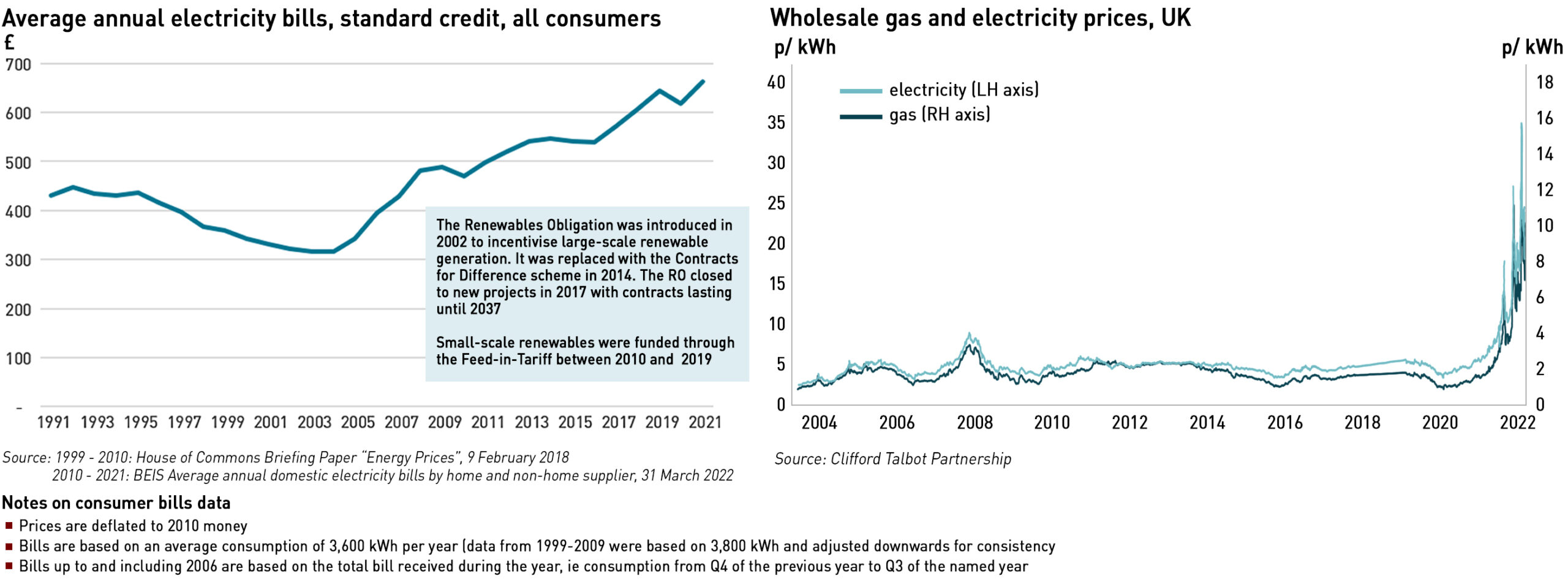

Well, we have been subsidising renewable generation in Britain now for over 20 years, and during that time we have seen a steady increase in end user prices, a trend which is completely different to the behaviour of wholesale prices during the same period.

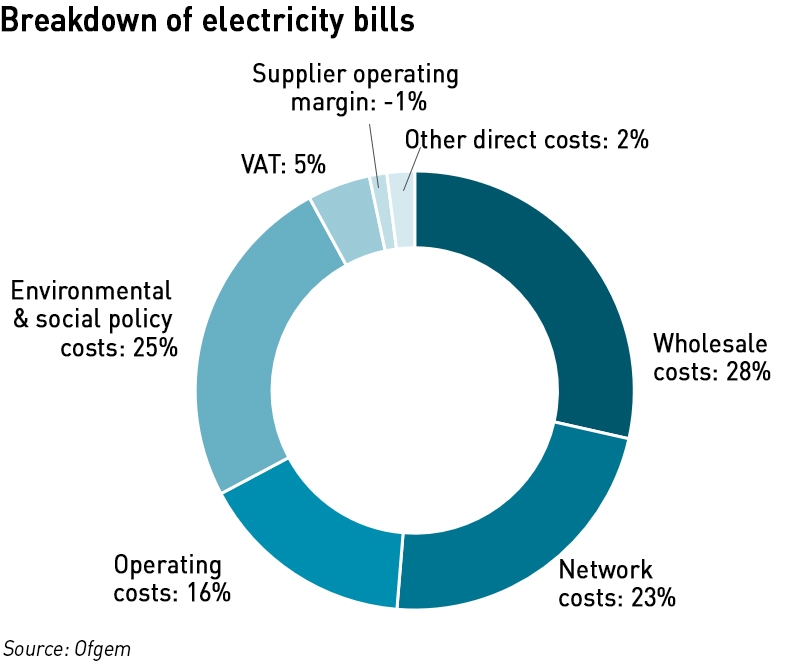

All of the evidence to date indicates that renewable generation increases end user prices, and when you break it down, you can see why:

- First of all we have to pay subsidies to build this generation

- Then, because it is intermittent, we have to subsidise conventional generation to be available to provide a backup when it isn’t windy or sunny

- The new generation is built in places that do not have existing network infrastructure, particularly in the case of offshore wind, and in Britain, the windiest places are also furthest away from the demand centres. This means we have to pay for new network infrastructure and increasingly also have to pay curtailment fees to generators when network constraints force them to turn down.

- Finally, we have to pay much higher balancing costs to maintain a balance between supply and demand in real time, which is harder when higher proportions of generation are intermittent.

Even before the increases in gas prices last autumn, these factors were driving significant increases in prices. By last summer, environmental and policy costs were 25% of end user bills and network costs had grown to 23%.

The Government has liked to portray suppliers as profiteers who have earned excess returns on the backs of consumers – that was the premise of the price cap. But it is not true, and wasn’t true back in 2016 when the Competition and Markets Authority claimed suppliers were earning £1.4 billion per year in excess profits.

As former regulator Stephen Littlechild has demonstrated, the CMA failed to follow its own guidelines in calculating this figure and as a result got it wrong by a factor of 10. According to Littlechild the actual customer detriment was only £170 million and was probably because of Ofgem’s previous restrictions on tariffs.

In fact, the supply of electricity to the domestic market has been loss-making for years now, and in the past year, the domestic gas market also became loss-making, forcing half of the suppliers out of the market. This lack of profitability explains the lack of innovation in the sector – many people had assumed that with the development of networked home technology, tech companies would enter the supply market, and supermarkets did briefly flirt with the idea as well.

But the combination of low profitability and high regulatory burdens has scared many of these companies away, and inhibited innovations that might see the development of new business models such as energy as a service that are widely seen as important in supporting consumers through the energy transition.

The result is that the domestic energy segment has stagnated, while prices will remain high, driven by a combination of external shocks and poor policy decisions.

Each winter thousands of people die in Britain as a result of being unable to afford to adequately heat their homes. With some 40% of consumers expected to be in fuel poverty this coming winter, that figure is set to rise, particularly if the weather is colder than normal. The Government has announced support measures that will cover about half of the expected price increases but things are expected to become very difficult and there are already signs of self-disconnection among the most vulnerable consumers.

The other big area of concern in Britain is around security of supply. Although the press is focusing on gas, the real worry is in the electricity market where we could see rationing for industrial users this winter.

The reason is that the winter capacity margin has been falling steadily, and closing conventional capacity which makes the highest contribution to margins is not being replaced on a like for like basis. This year we are expecting 2 GW of nuclear capacity to close as well as 4 GW of coal capacity.

The Government had apparently hoped that EDF would keep one of its nuclear reactors open – it won’t – and is negotiating with the coal operators to keep their plants open this winter. There is news of some special arrangements being negotiated between the Government and these operators and last week agreement was reached with EDF to keep 400 MW of capacity at West Burton A open as the station of last resort. The remaining 1600 MW will no longer be available.

The other huge challenge this winter relates to the situation across the Channel in France – half of the French nuclear fleet is offline after systemic problems have been identified in the cooling systems of their reactors. The French nuclear regulator believes these problems will take years to fully resolve.

This means that instead of exporting, France is now relying on imports, including from Britain – in the past month we have been exporting to France pretty consistently. So come the winter, instead of benefitting from 3 GW of imports from France, we could be exporting 3 GW, a net impact of 6 GW. That means that the available capacity for the winter would be 10-12 GW lower than last year, or around 8 GW on a de-rated basis.

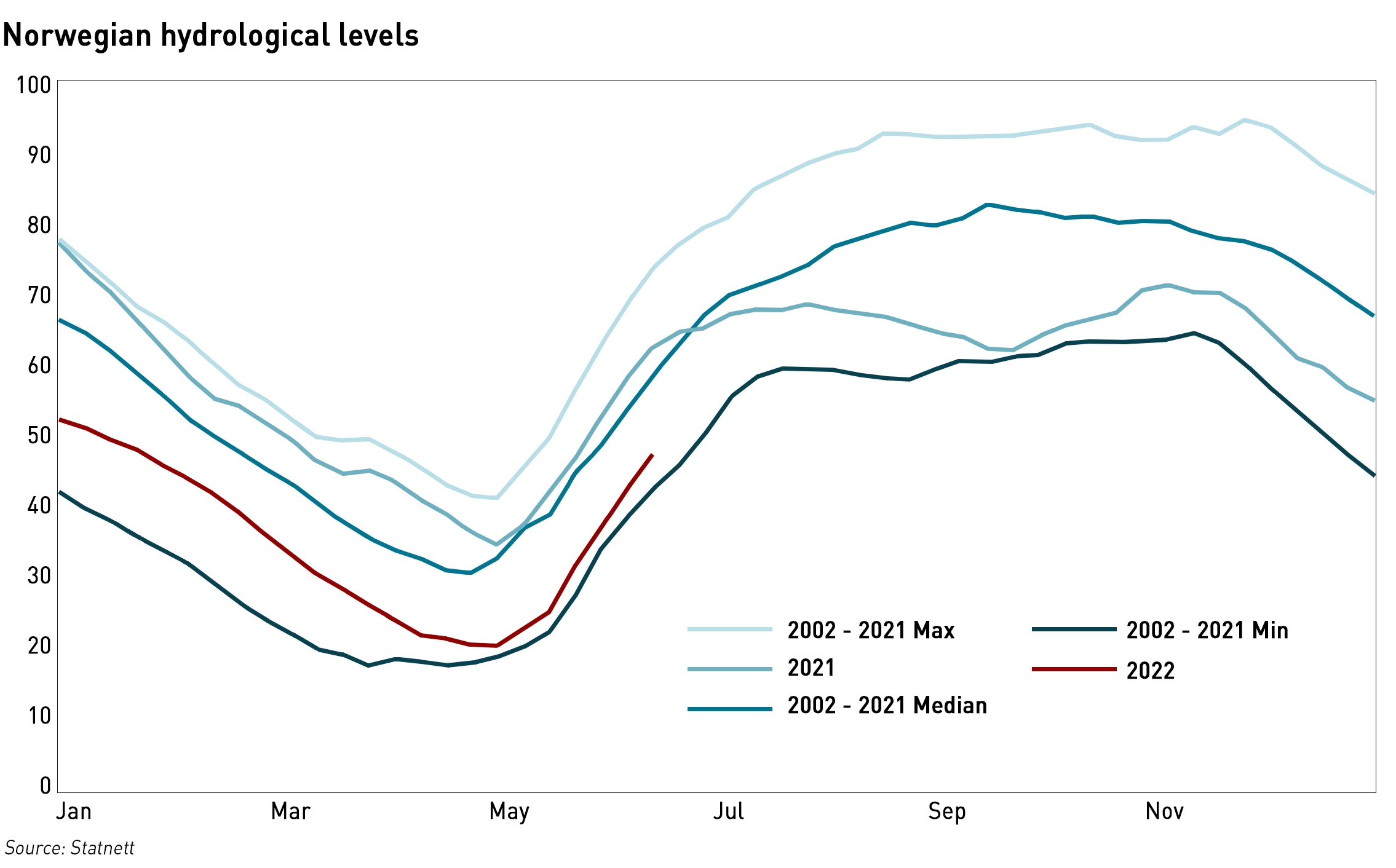

We may also be unable to rely on imports from elsewhere. The situation in Norway is also a cause for concern. Last year, Norway opened two large interconnectors, one with us and one with Germany. Since then, power prices in Norway have risen by a factor of ten with the government subsidising end users to up to 80% of their electricity costs. These exports have been draining Norwegian reservoirs – and contrary common belief, Norway can’t simply replace these volumes through pumping since only a small amount of its hydro has pumping capacity.

To make matters worse, Norway is having a dry year, and its hydro levels are approaching 20-year lows. The government has instituted an Energy Commission to investigate the issue, and it may well be that when it reports back in December it recommends reducing electricity exports.

The final problem for capacity margins is that the top-up capacity auction for this winter saw a shortfall for the first time ever, with the amount procured being 365 MW less than the target.

Last winter, the de-rated capacity margin was 3.9 GW – this is likely to be completely wiped out by the changes I have mentioned. While new renewable generation has been built this year, we can experience periods of up to 2 weeks with no wind, so this is very concerning.

National Grid has said it will issue another early indication of the winter margins next month, but the signs are not good…even if the other 2 GW of coal capacity stays open, winter capacity margins will be very low or even negative depending on the assumptions made for interconnector flows, making the grid extremely vulnerable to unplanned outages. Large industrial users are very concerned about the prospect of involuntary curtailment this winter, and the best advice is for them to buy or hire diesel gensets in order to reduce the impact on their operations.

The headlines are all about energy costs at the moment, but once we get into the winter, security of supply issues may well emerge to be an even bigger issue. It’s also pretty clear that net zero ambitions are only important until they’re not: affordability and security of supply can very quickly take over which is why we’re now seeing the Government scramble to keep the dirtiest old coal power stations open this winter. And while expensive energy is unpopular, unreliable expensive energy is likely to be even more unpopular. The Government should take note…

While we spent a fair amount of time discussing the causes of the energy crisis, solutions are thin on the ground. Regular readers will know that I favour a renewed push on nuclear power, based around Advanced Boiling Water Reactors. I would also like to see progress on Small Modular Reactors, and don’t really understand why they are still so far from commercialisation.

We didn’t really touch on energy efficiency. I am a strong proponent of a Government-backed programme to reduce heat losses in homes but do not support the current approach: the Energy Company Obligation is not efficient (suppliers should not have to participate in the building products market) – central Government should set targets while local government should be responsible for delivery. I would prefer limited resources to be spent on this rather than further subsidies to renewable generation.

Reducing energy waste is both environmentally sustainable and will save money for consumers, something which is important in times of high prices. Other measures to limit the impact of high prices include VAT relief on domestic energy bills and removal of green levies to general taxation. There is also an argument for the Government to buy up the Supplier of Last Resort credit balances whose recovery is currently adding so much to standing charges.

On energy security, we are rapidly running out of options, and very soon the only choice will be to build new gas-fired generation. It’s the only technology that can be reliably delivered in short timescales: a CCGT can be built in a year and a half. While we’re unlikely to run out of gas, we will need to compete in the international markets for LNG, and that will remain expensive for some time. I believe we should increase domestic production as far as possible, primarily in the North Sea, but we should also explore the possibilities presented by shale gas. There should be parity with geothermal energy when it comes to seismic impacts and drilling should be allowed. Whether there are meaningful resources that can be commercially extracted is as yet unclear, but we should certainly investigate.

I set out my hopes for energy policy before the Government published its Energy Security Strategy, and my views haven’t changed since. I believe my 14 point plan is still the best route out of the energy crisis, and certainly more credible than anything currently on offer in Westminster.

Exactly. But what is currently on offer is a NetZero driven suicide note by incompetent corrupted politicians who would rather see us all live in mud huts than ditch their global paymasters.

(Wait for the nutjobs claiming we’re all gonna die by 2030……)

What we should do is invent a time machine and explain to the Major and Blair governments the seriousness of the energy crisis in 2022 and tell them that we can offset this by continuing the Sizewell B SNUPPS reactor programme to commission a further 8 power stations – this would instantly procure us in the present with an additional 9.6 GW of low carbon electricity at a fraction of the cost we’ve spent on renewables and Hinckley Point C.

I can think of more creative uses for a time machine 🙂

You said a number of times that you are unsure why the RR SMR is taking so long to come inboard, this is basically because it’s a brand new design, it’s not a development of its submarine designs.

I’ve aggregated a summary of RR SMR info which I’ll paste below, hopefully some useful tidbits there. Also saw this story in the Times today : https://www.thetimes.co.uk/article/rolls-royce-presses-for-early-go-ahead-on-mini-nuclear-reactors-b3fndszpf

The Rolls Royce SMR (is it really a small modular reactor?) is a 0.47 GW PWR, possibly developed from Rolls Royce’s Safe Integral Reactor design of the 1980’s.

Every aspect of its design is to reduce capital and finance costs, operating costs and decommissioning costs; to make nuclear power as easy for governments to fund as wind farms.

The solution is for a standardised power station design composed of factory built modules, all modules to be transportable by road on HGV’s. Final assembly is at an on site factory, complete with integrated crane gantry’s and its own weatherproof canopy – the on site factory itself is standardised and re-usable.

Rolls Royce SMR have said they expect to complete the first power station by 2030, that power stations can be built in four years – two years for site preparation, then two years for power station construction and commissioning – initially for a cost of £2.2 B for the first five, and then £1.8 B for the rest. By 2035 they expect to have completed 10 power stations, and their plan for the UK is to build 16 power stations in total. They also envisage the deployment of two power stations at each site, sharing offices and cooling towers – so each site would be twin power stations, in an area one fifth the size of a conventional nuclear power station, capable of generating 0.94 GW. Operating life is envisaged at 60 years at 95% availability. Refuelling cycle is 21 months. Modelled costs included fuel management, on site fuel storage for 60 years (waste volume 1 1/2 times Olympic swimming pool) and full decommissioning.

The design is now in its next phase of development: to get the design through the UK assessment (GDA), finalise engineering, identify factory sites and identify power station sites.

Rolls Royce SMR will build the power stations and intend to provide central nuclear management services for the initial fleet of 16. But the fleet itself will be run by energy companies, probably Exelon Corporation, on a contracts for difference (CfD) basis: £60 MWh indexed linked; CfD’s usually run for 15 years, so its a reasonable guess that the CfD contracts will cover the financing.

Rolls Royce SMR believe the £60 MWh energy costs are initially required because finance for nuclear is so expensive. Their hope is that if the design proves itself then the cost of finance will come down, a low cost of finance might support generating costs of £25 MWh, they seem to think £40 MWh is very achievable.

https://youtu.be/4kpZiQUhfI4

That’s really interesting, thanks for the info. Although it doesn’t explain why it had to be a whole new design – one of the attractions of RR getting into SMRs was leveraging the propulsion technology, but if this is something completely new then that isn’t happening. I wonder why not…

The impression I get from their presentations is that they saw a commercial opportunity for a commoditised nuclear power station (not just reactor) design. So they determined the parameters they thought were important and that’s what led to the actual design today.

So they decided everything needed to be road transportable, which gives you the reactor vessel size. That sloping roof design is to enable it to survive being hit by an airliner (disperses ignited fuel) and it sits on a mound to protect it from a tsunami.

Its also important to consider that being a sort of new reactor design (they actually had an existing design albeit never implemented) doesn’t mean they can’t still leverage their submarine nuclear engineering expertise – which I’m sure they have.

Submarine designs are based on rather different operational parameters. The cores have an operational life of about 30 years, and refuelling is not a consideration: the entire core is replaced as a unit. Power demands are highly variable, since a sub must leave a minimal energy signal in the water, with as little waste heat as possible, yet it must be capable of full steam ahead very rapidly. Average consumption is well below a battle stations peak. Operational performance is the dominant design consideration, with cost very much secondary. Peak output only 30-50 MW, average ? under 50%. Lots of features that are less well suited to commercial operation as baseload supply., hence the need for a complete redesign.

The financial calculus is easy to do provided you can trust the cost data. I did a simple table on the implicit financing costs with interest rates and utilisation as the key variables when RR first came out with their £1.8bn for nthOAK estimate, which substantiates the figures you quote, since O&M and fuel are small components of cost: the low end requires finance at 4%. Unfortunately, the present crisis means that interest rates are rising rapidly, and raw materials costs have shot up since those estimates were made, with construction labour fast following. Of course, Hinkley Point includes some costly Chinese finance at 10% on top of the horrendous capital cost. But I am sure that pension funds would have been more than happy to have offered funding rather more cheaply if they had been allowed to do so, especially when they were being forced to buy gilts with negative real yields. Fund via the Green Gilts programme, and the financing cost should fall substantially, but inflation is pushing up even government funding costs. A key part really will be ensuring that wind doesn’t get to cannibalise nuclear output.

Meanwhile, perhaps the best news is that EDF is considering withdrawing from Sizewell C. Of course, to benefit the government needs to progress rapidly towards alternative ABWR provision.

https://www.energylivenews.com/2022/06/23/edf-reportedly-ready-to-pull-out-of-sizewell-c-nuclear-project/

EDF barely got HPC over the line, and one board member resigned. Anyone that assumes Sizewell C is a done deal is dreaming…

Thank you for another thought-provoking post, Kathryn. RR has been building small reactors for nuclear submarines for half a century. Like you, I’m not clear why building some more small reactors is taking so long.

The whole webinar was a thoughtful, insightful discussion, though I’m not as optimistic as John Constable about the timeframe on which net zero policy will get put back in the bottle, even if we try to work hard to that end.

Kathryn,

I am a bit late reading this article. Very insightful as usual!

One thing I would like to pick up on though is your estimate of an 18 month build time for a new CCGT. IMO this is grossly optimistic. You might at a push, in normal times, make this if you have your consents/permits and all your contracts in place, etc. Realistically for a CCGT you are looking at around 3 years. You probably could hit an OCGT / recip in around 18 months.

However, we are not in normal times. Ongoing chip shortages will have an impact (1 year lead time for some instrumentation, control systems, etc). Energy prices / uncertainties are likely to impact on supply of the required specialist steels, components, etc. Covid induced backlog of work for some suppliers will also have an impact, as well the lack of much recent build (suppliers will need to gear back up).

All in all, I think you are looking at a 3 to 4 year build time for a CCGT. Which doesn’t fit will with the T-4 capacity market timescales.

Enron successfully built the 1,875 MW Teesside CCGT / CHP – at the time, the world’s largest – in two years flat, defying all the “3 years minimum” rhetoric of the time. It did this by, for example, not having a turbine hall, again defying convention. (Turbines don’t need a hall, any more than does oil refinery equipment – it’s soft electricity-industry plant operators who don’t like being in the rain.) It took several other simple but radical time-saving measures, like not having a unionised labour force: the extant Teesside unions were notoriously “conservative”, having grown up on a diet of playing games with ICI and the other traditional industrial incumbents there.

The point about today’s supply-chain shortages is of course perfectly fair.

(Before anyone with a long memory says, “yes, but Enron didn’t initially build an adequate cooling system at Teesside and had to retrofit it”: they built exactly the cooling system the planning authorities insisted upon, even while telling them it wouldn’t be adequate. Sure enough, it wasn’t, and hence the retrofit – which didn’t take very long at all, and wouldn’t have delayed the two-year schedule if it had been done first time around.)

A seriously good article & replies. Thank you.

A book I recommend for those wishing to understand nuclear power is Merchants of Despair

by nuclear PhD engineer Robert Zubrin. He makes clear that nuclear power stations require

enrichment to only 3% whereas nuclear bombs require enrichment to 90% & some exquisite

engineering to bring together a critical mass of fissionable uranium, features which power stations simply lack.

He also exposes the fraud behind the global warming movement, showing the nasty

Malthusian and racist Darwinian and Nazi roots of this death cult.

A most valuable read.

Zubrin also makes the case that fusion power has been deliberately underfunded to fail & deliberately buried under unnecessary layers of bureaucracy.