In recent months there have been increasing calls for the introduction of prudential regulation in the energy markets, in response to the large number of suppliers that has failed this year. Supplier failures are a cause for concern because, unlike in many other industries where the costs of failure are borne primarily by shareholders, in energy markets some of the costs of failure are socialised, ie met by other market participants, and ultimately consumers.

Prudential regulation is a form of financial regulation which requires firms – typically financial firms such as banks – to control risks and maintain adequate capital. Regulations set out capital and liquidity requirements, and impose concentration risk (or large exposures) limits, and regulated firms are required to meet certain disclosure and reporting obligations. Micro-prudential regulation focuses on individual firms, while macro-prudential regulation monitors system-wide risks.

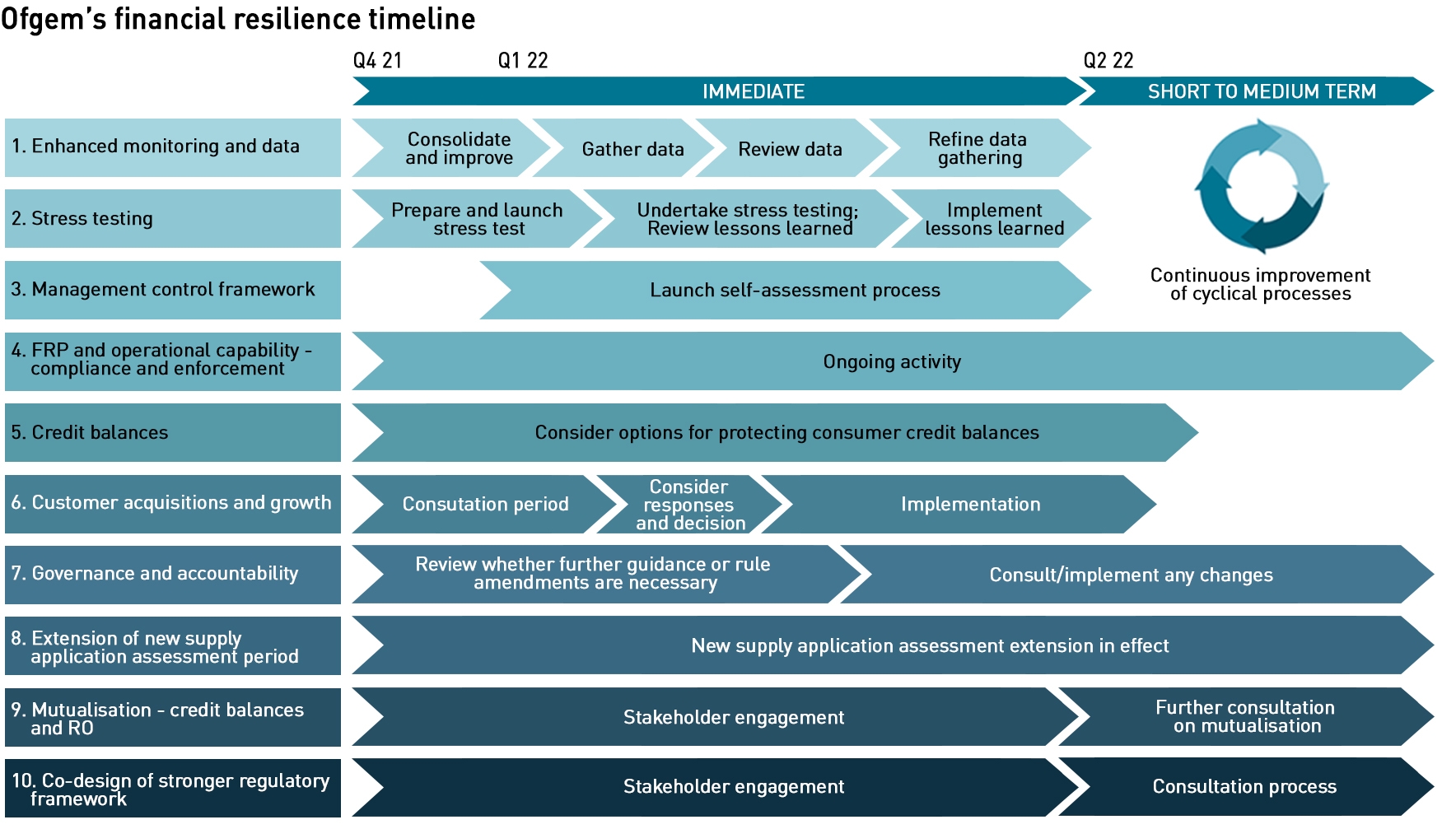

Yesterday Ofgem published a slew of new consultations (closing on 22 January) setting out a new approach to prudential regulation within the energy markets:

- An action plan on retail financial resilience;

- A statutory consultation on strengthening milestone assessments and additional reporting requirements;

- A call for views on potential adaptations to the price cap methodology for resilience in volatile markets;

- A supporting statutory consultation on potential short-term interventions to address risks to consumers from market volatility;

- A decision letter regarding the time period for assessment of supply licence applications and tacit authorisation; and

- A decision letter regarding the revocation of dormant supply licences.

“Our aim is a competitive and innovative retail market, where consumers have secure energy supplies at fair prices, and have confidence in efficient, competitive suppliers; and where suppliers are resilient to market shocks and can earn reasonable profits commensurate with the risks that they are taking,”

– Jonathan Brearley, CEO of Ofgem

In this post I will explain what Ofgem is proposing and whether it is likely to be successful in protecting consumers from the effects of supplier failures, without unduly inhibiting competition.

Ofgem’s action plan contains sensible provisions, but does it have the skills to implement it properly?

Ofgem’s immediate focus is on the domestic market, although it recognises it may need to extend some of these new provisions into the non-domestic sector, something many energy users would welcome. There is also an increased focus on gas shippers as well as gas and electricity suppliers, in the aftermath of the CNG collapse.

The key principles of Ofgem’s new approach are as follows:

- Robust minimum standards: robust minimum standards to ensure commercial risk is well managed, for example, suppliers need to be “adequately hedged” or hold sufficient capital to manage a wide range of market scenarios. Within this, suppliers are responsible for their own commercial strategy but must have a robust management control framework in place to support it and manage their risks;

- Protecting customer money: suppliers should not pass inappropriate risk to consumers, eg through use of customer monies or levy payments to fund wider business activity. Socialisation of losses when suppliers fail must be minimised (in line with firms in the broader economy);

- Accountability: there should be minimum requirements for staff in significant leadership or executive roles and board members, eg fit and proper person tests and capability requirements, and appropriate board governance;

- Proportionality: regulation should be necessary, and no more than needed. The regulatory burden of data exchange should be minimised through use of data and digitisation techniques, for data provision and monitoring

- Transition: any regime should enable a sustainable, innovative and competitive market, to promote the transition to net zero.

To support these objectives, Ofgem intends to expand the information it collects from suppliers – something unlikely to please many suppliers who already devote significant resources to meeting existing reporting requirements. Ofgem already collects significant amounts of information from suppliers, but was unable to anticipate or prevent the large number of supplier failures this year. Ofgem needs to make sure that the information it collects from suppliers is useful, and crucially, that it employs people capable of interpreting it.

“We already receive data from suppliers and other parties relevant to supplier and retail market resilience. We are reviewing, refining and consolidating the information that we collect and, where necessary, will expand the scope of this reporting from suppliers. This will be an ongoing and iterative process. We expect suppliers to be responsive and engaged in this process and provide prompt, robust and accurate information to us. Failure to respond fully or accurately to these requests will be met with robust enforcement action.”

Unsurprisingly, Ofgem intends to introduce stress testing, beginning in January, “to assess whether suppliers are robust to a range of scenarios, whether through capital cover or risk management.” Ofgem plans to engage with suppliers through Energy UK in January to determine the shape and content of the initial stress tests, with an iterative process to determine the longer-term approach. It will be essential that Ofgem designs the sensitivity analyses appropriately, otherwise there are significant risks that the process will add costs but fail to prevent supplier closures. To date Ofgem has not demonstrated a good understanding of how hedging works in the energy markets, taking an unrealistic attitude to the risks that can be offlaid through hedging. In order to design and operate an effective stress-testing approach, Ofgem will need to significantly up-skill its staff, and it seems doubtful that this is something that can be done quickly. At the very least, Ofgem should engage with the Financial Conduct Authority (“FCA”) to leverage its experience of implementing a stress testing regime in the banking sector.

Ofgem also intends to require suppliers to carry out a self-assessment of management control frameworks, with the directors of supplier businesses providing assurance that risks are appropriately managed. These assessments should reference the governance, policies, processes, controls and management information used by the supplier to manage and monitor commercial risks. Ofgem is also considering strengthening existing “fit and proper” requirements on senior staff (Ofgem would do well to consider the FCA’s senior managers regime here).

Last March, Ofgem introduced rules requiring suppliers to manage costs that could be mutualised in a responsible way, ensuring that business plans are adequately financed, and that firms have the funds to meet Renewables Obligation and other payment obligations. Ofgem now intends to evaluate whether suppliers are meeting these requirements, something most people would have expected Ofgem to have been doing anyway. Indeed, as the recent report from Citizens Advice highlighted, Ofgem has frequently failed to enforce its own rules, which could in some cases have prevented supplier failures. Of course, Ofgem should be monitoring compliance with its rules, but as we have seen before with the 2019 blackout, there is often no ongoing monitoring in place (in that case it was Grid Code compliance that was not monitored).

Ofgem intends to consider rules to protect consumer credit balances, such as auto-refunding of excess amounts and credit protections. There are also proposals on managing consumer growth to ensure that suppliers are able to manage the risks of a growing customer book, particularly as various additional obligations (such as the Energy Company Obligation (“ECO”)) apply as customer numbers grow.

Statutory consultation on strengthening milestone assessments and additional reporting requirements

Milestone assessments are designed to ensure that suppliers have the right resources in place to manage the increasing regulatory and operation obligations that arise as supplier numbers grow, specifically as they reach 50,000 and 200,000 domestic customers (150,000 would be more appropriate since this is the level at which the ECO and other obligations begin to apply). Ofgem is considering amending supplier licences to limit customer growth until these assessments are carried out, with each assessment expected to take between 30 and 60 days.

The requirement could be removed if suppliers demonstrate financial readiness ahead of reaching the milestones, but these assessments would also apply ahead of “significant commercial developments and personnel changes” such as a sale of the customer book. Of course the risk, particularly in the case of distressed trade sales, is that this assessment process will lead to significant delays that could result in a sale not being completed and the supplier entering the Supplier of Last Resort (“SOLR”) process.

Ofgem recognises that these proposals will slow the growth of new entrants and may inhibit competition. That should not be a problem as long as Ofgem is able to meet the timing commitments set out in the consultation – the danger is that the new Action Plan represents a material increase in Ofgem’s workload and it may lack the resources to meet these commitments, leading to worse outcomes for consumers.

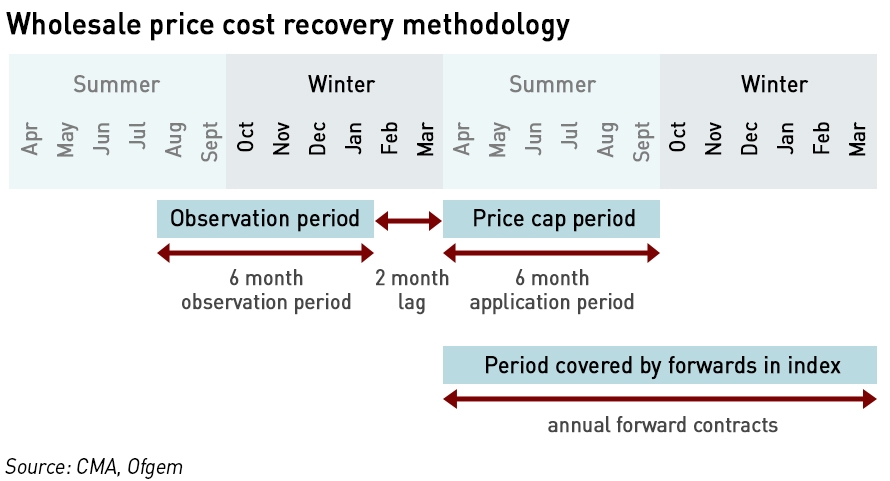

Amending the price cap methodology

The wholesale component of the price cap methodology is a 6-2-12 semi-annual model:

The relevant wholesale index is observed for a 6-month period which ends 2 months before the start of the cap period in question. The index in question is annual forward prices (ICIS) with the weighted average of contracts being determined, and semi-annual refers to the price cap period of 6 months.

Clearly, this methodology creates a significant timing difference between the cap observation period and its application period, and since suppliers struggle to predict how many customers will be on the variable tariff when markets are volatile, they may have bought too little or too much energy ahead of the cap period using the contracts in question. The other issue is that annual contracts deliver an equal volume of gas or electricity during each day in the delivery period, ignoring both seasonal, weekly and intra-day shape. While the cap methodology does attempt to adjust for this shape risk, it is done in a fairly high-level way which does not necessarily line up well with what suppliers are able to do in practice, particularly in the case of smaller suppliers.

Ofgem is now proposing three tools for managing high price volatility:

Enhanced Status Quo: retaining the existing methodology, but with an enhanced ability for Ofgem to adjust the price cap in extreme circumstances, with an automatic “circuit breaker” triggered by certain circumstances. A further change, which could potentially be applied to all three options, is to reduce the two month gap between the observation window closing and the price cap period starting;

Quarterly Updates: using the existing cost-based price cap methodology, but updating the wholesale component every three months to reflect changes in wholesale prices more quickly. The price level could be set using forward prices for three months, six months, or twelve, with different balances of price smoothing for consumers versus the risk remaining with suppliers; and

Fixed Term Default Tariff: a tariff that is set by Ofgem which is fixed for 6 months (for consumers starting their tariff that month), with an exit fee that would potentially decline over the six months. The way the wholesale cost element is calculated would change, but all the other costs would follow the existing calculation approaches. The price of the tariff could be based on either 6 or 12-month forward prices. Another variation would be to have an annual fixed contract, with matching 12-month forward pricing.

Ofgem has also considered three other options: a monthly wholesale cost pass-through, a market-wide relative cap based on a basket of competitive tariffs and a relative cap per supplier comparing their most and least expensive tariffs.

Ofgem’s analysis of these options gives significant weight to the issue of smoothing prices for consumers, and the extent to which suppliers rather than consumers should bear the risk of price volatility. This strikes me as being outside the scope of the cap which was intended to protect consumers from unfair pricing practices, not from market behaviours which suppliers cannot control.

Short-term interventions to address risks from market volatility – removing the price cap would be better

Ofgem is considering changes to the price cap methodology, but any such changes would not be implemented before October 2022. This leaves suppliers, and consequently consumers, exposed to the risks of market price volatility in the meantime, so Ofgem is exploring whether temporary measures should be introduced in April to address this risk. The disappointing aspect of Ofgem’s plan is that it has no intention to act through this winter, when prices and price volatility are at seasonally higher levels – the mills of God might grind slowly but they have nothing on Ofgem!

The particular risks suppliers face relate to the intersection of volume and price risks: when suppliers hedge they must estimate both the number of customers they will have on any given tariff, and the volume of energy they will consume. When market prices rise sharply, as has happened this year, the capped default tariffs become cheaper, so more customers are likely to remain on the default variable tariff when their fixed contracts expire. Similarly as prices fall, more customers are likely to fix to lock in the lower rates.

In the first instance, suppliers will not have bought enough energy at the cap level to meet all of the customer demand that results, meaning suppliers must cover these positions at the higher prevailing prices. In the second instance suppliers will have bought too much energy at the higher prices and will face losses when they subsequently sell at the new, lower levels. These dynamics are very difficult to predict when prices move rapidly, and the issue is not so much whether suppliers have hedged or not hedged, but whether they have correctly anticipated how much to hedge. Suppliers acting as a SOLR have the same problem – they become price takers for hedging new customers they could not have anticipated having.

Ofgem has analysed a number of scenarios:

- Requiring suppliers to make all new tariffs available to existing customers

- Allowing suppliers to charge exit fees on certain Standard Variable Tariffs

- Requiring suppliers to pay a Market Stabilisation Charge when acquiring new customers.

The first option would deter suppliers from offering much cheaper tariffs to new customers as price pressures ease and costs fall below the cap, and customers that do not wish to change supplier would be able to benefit from cheaper tariffs. This measure would be time-limited to September 2022, but in some ways this is surprising since similar measures have been proposed to reduce the “loyalty” penalty faced by consumers that do not switch. It is also unclear what this means in practice – most suppliers will offer existing customers their best tariffs if the customer calls them up to ask for them (under the threat of switching). Ofgem seems to be assuming that inactive consumers will switch to these cheaper tariffs, but this seems unlikely unless suppliers are required to actively market them rather than just “make them available”.

Ofgem sees the downside of this proposal being reduced competition between suppliers since under such rules they would set their cheapest tariffs at a higher level than might otherwise be the case.

Under the second option, suppliers would be able to cover some of the costs of being over-hedged in a falling market by charging exit fees for variable tariffs for a limited period (other than in the case of deemed tariffs where the customer did not choose to be with that supplier and on that tariff eg where they have moved house or been part of a SOLR process). Any such fees would need to be proportionate, and not exceed the direct economic loss to the supplier. While this would limit the benefit to consumers of switching to a cheaper tariff, it would reduce the chance of supplier failures and the consequent socialisation of costs, thereby benefitting consumers. Ofgem notes that suppliers may not be able to enforce exit fees when customers switch away to other suppliers and is asking for evidence from the market on this point.

Option three would see any supplier acquiring a domestic customer to pay a “Market Stabilisation Charge” to the losing supplier, to cover a proportion of the economic loss to the losing supplier based on a customer’s estimated annual consumption. Ofgem proposes that this option would only apply if prices were to fall by 30-50% below the level assumed in next summer’s price cap, and would only apply between April and September next year.

These approaches are designed to limit the likelihood of consumers switching suppliers in the event of significant market volatility, particularly if wholesale prices fall below the level of price cap, which would provide scope for lower fixed deals which would normally incentivise switching in a way that the current market does not. The measures would be temporary, and are intended to reduce the risks that suppliers would collapse, imposing costs on consumers.

While these measures might work as intended, surely a simpler approach would be to abolish the price cap, or at the very least, re-set it more often – something Ofgem expects to have the powers to do (again) by April. The existence of the price cap in the context of variable tariffs is what creates the problems Ofgem is seeking to avoid: in an un-capped market, suppliers are able to pass through changing variable costs to their customers, limiting the need for hedging (pass-throughs are rarely perfect, so some degree of hedging is prudent). Fixed price tariffs should always be hedged because they contain an embedded derivative, but variable tariffs only require hedging if there is a limit on the supplier’s ability to pass costs on to consumers by a price cap or other limiting mechanism.

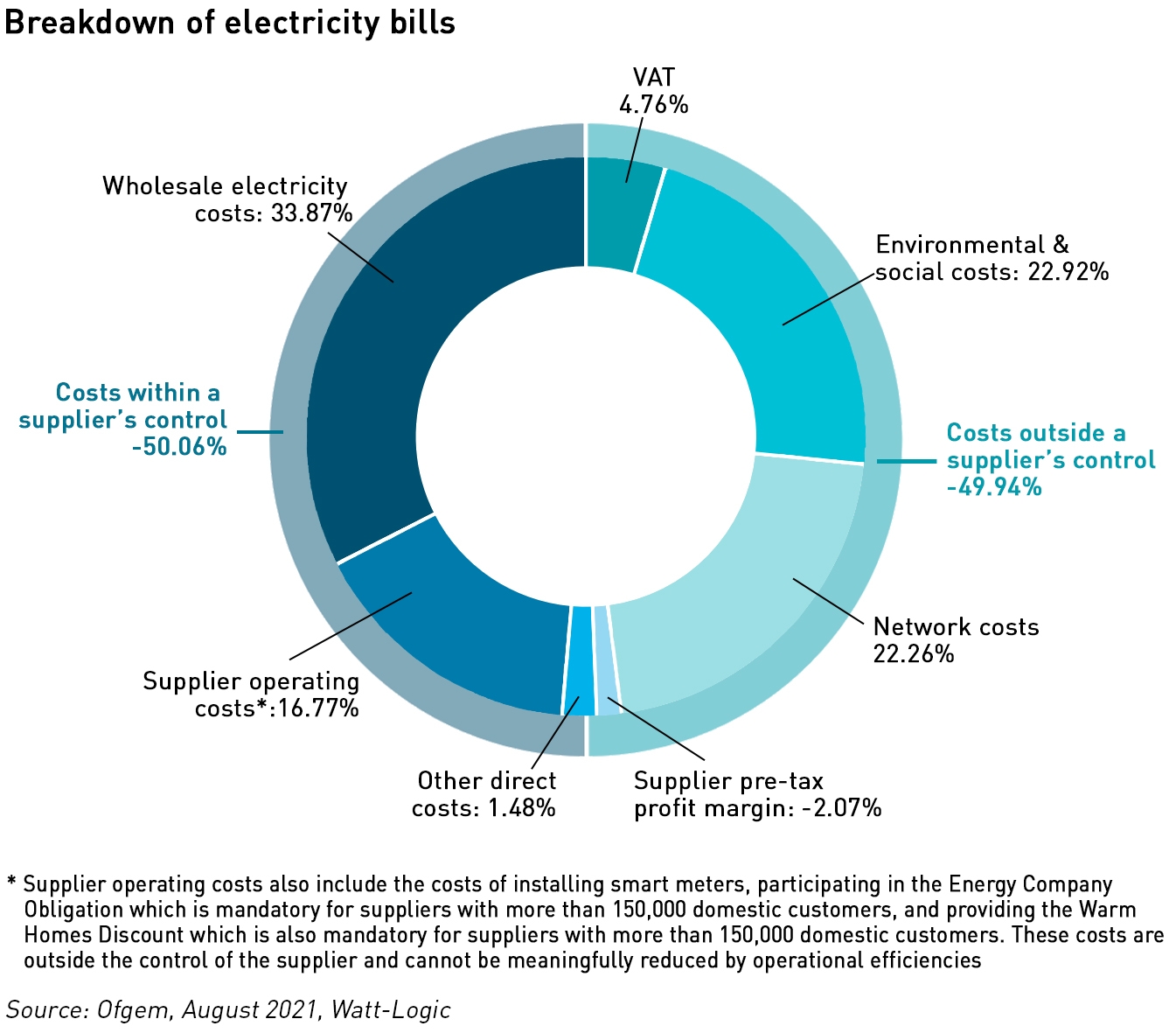

Since suppliers cannot control wholesale prices, there is a good argument for the wholesale component of energy bills to be excluded from the cap altogether. Unfortunately, when you look at the components of energy bills, suppliers also cannot control network costs and environmental and social costs, which together make up 45% of the bill. VAT at 5% is also outside the control of suppliers. The only component of bills that suppliers can reliably control are their own operating costs, and even here there are limits due to the wide ranging costs that cannot be avoided (smart metering, the ECO and the Warm Homes Discount (“WHD”)). This is really why the cap makes little economic sense – to a large extent suppliers are not able to control their costs since they are external to their businesses, and therefore large amounts of end-user bills are simply passed through from other parts of the supply chain.

Introducing more market distortions in order to mitigate the effects of previous market distortions really makes little sense, and simply adds further complexity and therefore further costs to supplier business models to the detriment of consumers. Ofgem’s argument that the cap has helped to smooth the impact of price volatility is completely spurious since this was never the intended purpose of the cap, and if the Government wants to insulate consumers from wholesale price volatility it should take the costs of that onto its own balance sheet.

Ofgem is pausing market entry for new suppliers

While it gets to grips with changing financial resilience requirements, Ofgem is increasing the review period for new supply licences from 75 days to 9 months and licences that have not been approved in that time will no longer be deemed to have been granted.

“We have put in place these emergency measures without undertaking consultation as it is vital that we act now to control the harm that is caused to consumers and the market by multiple supplier exits. While the recent rise in gas prices is unprecedented, we need to plan on the basis that shocks like this could happen again,”

– Ofgem

Ofgem is also taking steps to revoke dormant or unused licences, presumably to prevent new entrants by-passing the approvals processes by acquiring a company with a dormant licence or indeed for the holders of such licences to rely on historic approvals to operate when their circumstances may have changed significantly.

If hedging rules are too prescriptive the industry “may as well be nationalised”

In recent days, various suppliers have expressed concerns that Ofgem might introduce some form of mandatory hedging, in which case the industry “might as well be nationalised”. While there are good reasons for introducing prudential regulation, with capital adequacy and liquidity requirements, it is not the job of the regulator to determine how suppliers run themselves if the risks of failure are managed. Hedging is one way to manage those risks, but by no means the only way, and suppliers should have the choice to run loss-making positions if they have enough of a financial cushion to afford it.

This raises real questions over Ofgem’s role, and whether it should have the ability to exert pressure on suppliers which choose not to hedge according to the cap.

“That to me seems like a bit of an overstep. Ultimately these are commercial companies and it is a commercial decision. Whilst it’s an incredibly sensible one in my mind, to match the cap, it is ultimately up to the supplier… If anything, publishing that [hedging] information is like an early warning system. It’s an indicator. But what can the regulator then do with that – mandate them to behave differently? I don’t think so because then they might as well be nationalised,”

– Tom Eckerlsey, former head of hedge modelling and operations at Npower

People have been spooked by news that Avro had “no external funding or security over its assets” and relied solely on working capital to fund itself, while Bulb was known to hedge short. But Bulb’s business model was to offer only variable tariffs, which in an un-capped market to a large extent off-sets the need for hedging. It was the price cap which killed Bulb’s model, and not its hedging strategy per se.

Requiring suppliers to undertake particular hedging strategies would further undermine competition in a market where suppliers already have very little control over their costs, which will further undermine competition – if all suppliers face essentially the same costs and are restricted from offering loss-making tariffs, then the scope for tariff differentiation is effectively removed, and consumer choice will be largely removed. Ofgem does not seem to understand this point.

“It’s also important we remember that hedging is one of those areas where you can compete as a supplier, through different strategies, and so long as a supplier is in a position to support that strategy, you wouldn’t want to regulate out that ability to compete,”

– Dan Alchin, deputy director of retail at Energy UK

One option that has been floated by suppliers is that Ofgem could publish information that highlights which suppliers are relatively un-hedged so that consumers can make a choice as to whether they wish to buy from them, but others believe this would enable suppliers to inspect each other’s strategies without having much of an impact on consumer behaviour.

So what should suppliers and consumers make of all this?

For suppliers, there will no doubt be anxiety: there is too little information about how Ofgem plans to implement its stress tests and how it will define financial resilience. There are concerns it will require hedging to the price cap, or will set other metrics around what it considers to be “appropriate” levels of hedging. Yet time and again the regulator has demonstrated a weak understanding of how hedging works and what hedging strategies are actually possible. Any move to define “proper hedging” will further distort an already distorted market. The focus should be on resourcing levels – as long as suppliers can cover any losses they might sustain, then it should not be the business of the regulator how much risk they choose to carry.

There will also be concerns around price cap mission creep. The purpose of the cap was to protect consumers from abusive pricing practices by suppliers – it was not intended to insulate consumers from wholesale price volatility, yet Ofgem now seems to want to do exactly that. Arguably this is outside Ofgem’s remit – although the regulator would probably say that its mandate to “protect consumers” permits this.

There are two problems with this argument. The first is that someone needs to bear this risk, and if not consumers then who? Ultimately if suppliers fail as a result then those costs of failure are shared by consumers. This type of regulatory over-reach may also further undermine investor confidence in the sector, which would reduce consumer choice if fewer suppliers enter the market, or if suppliers adopt overly conservative approaches to risk.

The other problem is that Ofgem has repeatedly failed to use its existing powers to protect consumers from a wide range of rule-breaking by suppliers, as outlined by Citizens Advice. This means it is being selective in its application of consumer protections, without any transparency with the market on its approach. This is further complicated by the broadening of Ofgem’s remit to include the advancement of net zero, which will often conflict with issues of affordability. Ofgem has not shown itself to be capable of managing trade-offs and multi-dimensional thinking.

For consumers there is also significant uncertainty. That the price cap will see a steep rise in April is widely expected, but there is little clarity on what may happen next. From a fundamentals perspective, the timing of supply and demand imbalances in the gas markets easing is unknown and depends on the weather this winter. It is also not known how many more suppliers might enter the SOLR process and at what cost, or how the special administration costs of Bulb will be recovered (ie over what time-frame). Next year’s Renewables Obligation mutualisation threshold has already been exceeded, but the exact size of the shortfall cannot be predicted at the moment. This is before considering the potential effects of the raft of new proposals Ofgem has brought forth.

Consumers may take comfort from Ofgem’s desire to insulate them from price volatility, but this will also mean that falling prices will not materialise in end user bills as quickly as might otherwise be the case. And if Ofgem does impose prescriptive rules on hedging, consumer choice may be adversely impacted, which will lower engagement and raise costs. This is actually similar to the Simple Tariffs policy which created similar consumer detriments – it appears that Ofgem is not learning from previous mistakes.

Don’t mistake activity with achievement

Ofgem would do well to heed the words of renowned basketball coach, John Wooden who advised people not to confuse activity with accomplishment – bombarding the market with consultations neither absolves Ofgem for its significant regulatory failures to date, nor does it mean that these failings are being addressed. The fact that Ofgem continually makes excuses for its performance rather than owning its mistakes does nothing to inspire confidence.

And it’s all too little, too late. There is repeated use of the phrase “working at pace”, but Ofgem must have a very different understanding of the word “pace” to the rest of us – the previous five price cap consultations will not see any changes implemented before April, and there will be no substantive change to the price cap methodology before next winter. (It’s also hard to overlook the really poor grammar in these documents, which may seem beside the point, but is hardly evidence of high standards or good attention to detail, particularly when these documents are produced by teams of people.)

“All worthwhile ideas, but the big worry is Ofgem’s ability to make the reforms stick and to enforce them. Confidence is not improved by its chief executive, Jonathan Brearley’s, tiresome habit of talking endlessly about the “unprecedented” rise in global energy prices while glossing over Ofgem’s failure to model for extreme events (which have always happened in commodity markets),”

– Nils Pratley, writing in The Guardian

As Nils Pratley points out in his column in The Guardian, Ofgem could have introduced these new measures at any time, and it reviewed the licencing regime as recently as 2019, opting for minor tweaks rather than fundamental reform. He also points out that by its own admission, Ofgem does not appear to have much of an idea of how the stress tests which are due to begin in January will be run, stating that it will be “learning lessons and adapting over time”.

The ink was barely dry on Ofgem’s pronouncements when Business Secretary Kwasi Kwarteng announced another review of the energy market:

“Earlier this year, the Government published an Energy Retail Market Strategy for the 2020s… This vision remains the right one. However, we also need to take account of the lessons from recent months to ensure that the energy retail market is resilient, sustainable, and continues to protect consumers as we move to a net zero energy system. The Government therefore intends to review these lessons as part of a wider refresh of the current Energy Retail Market Strategy, with the aim of publishing an updated Strategy as soon as possible, once the market has stabilised,”

– Kwasi Kwarteng, Secretary of State for Business, Energy and Industrial Strategy

That a review is to take place is hardly a surprise – it is the default response to any failing and has the benefit of giving the impression of action where nothing meaningful is happening. But what is particularly disappointing in this case is that the Government feels the need to review and update a strategy which is less than a year old. What this does do is add regulatory risk to a sector already subject to an excess of bad regulation.

Nothing that has been said by the protagonists in recent days has changed my view that retail energy market regulation should be moved to the FCA, under the supervision of the Treasury.

Another fascinating post.

OFGEM desperately require more information from the Suppliers to help it understand the world it has created. To misuse your quote “Don’t mistake information with knowledge or wisdom” They are looking for trees while failing to see the forest.

Continuous iterative improvement of cyclical processes. Patches upon patches. Make do and mend. Is it time to start afresh?

Is achieving net zero an existential necessity or a business opportunity? What are the priorities? – pick some or all of these – price stability, the level of prices,lowering CO2 emissions, supply resilience, profitability. Can a free Market achieve these or is command and control required?

OFGEM also needs to understand that the greatest threats to the consumer will be from nerdy resiliance issues like Grid Code non-compliance or untested commercial innovations with unanticipated real world consequences.

Frankly OFGEM are completely out of their depth. They need some energy derivative pricing specialists to even begin to understand the implications of things like price caps. This paper lifts a corner on modern modelling techniques – and it doesn’t even discuss how to estimate the model parameters applied to the pricing of Asian options (effectively OFGEM’s cap), gas storages and swings (offtake options where customers ditch their deal) under different combinations of jump-diffusion market models.

https://arxiv.org/pdf/1908.03137.pdf

There is no discussion about who is going to take the other side of hedges, or what the real costs of offering these complex derivatives really are. It is interesting to note that one real market cap offered by Octopus – their Agile tariff that supposedly reflects spot prices per half hour has been anything but agile, locking customers into the cap strike price of 35p/kWh almost all the time.

https://agileprices.co.uk/

No-one is even discussing the huge increase in Balancing Mechanism payments that apply to the unhedgeable post gate closure regime. In Q3 BM payments averaged over £13/MWh supplied: these would have been heavily concentrated among those who don’t own generating assets they can turn up to collect £4,000/MWh from the other players (a tad more than £10 for it being your birthday…), and so would have been a large multiple of that for them.

I think OFGEM is set to fail. Whether Kwarteng’s consultation will get anywhere I also doubt. Minds are too fixated on net zero. Perhaps only if there are further major failings will more radical ideas get proper consideration.