Having written about the somewhat dubious goings on at Octopus Energy recently (still nothing on Companies House about the Kraken de-merger), here is my analysis of the OVO Group’s published accounts, which indicate the business is, in my opinion, in seriously bad shape with a realistic chance of bankruptcy within the next 12 months.

OVO Energy is a Bristol-based supplier, founded by Stephen Fitzpatrick, that began trading in September 2009, supplying gas and electricity to domestic properties throughout the UK. According to consumer group, Which?, OVO now supplies more than 4 million homes. SSE Energy Services customers moved to OVO Energy in 2023, after OVO Energy bought SSE’s domestic customers. Pay-as-you-go brand Boost Power was also part of OVO Energy. Its customers moved to OVO after the parent brand announced its pay-as-you-go arm was closing down, also in 2023.

But all is not well. OVO Energy got the lowest score of the 17 energy companies rated by 11,945 members of the public in the annual Which? customer survey in 2025. Scottish Power was the only provider to receive a similar score, with 62%. The next highest was 65%. OVO Energy had poor two-star ratings for every aspect of the survey, including for overall customer service, customer communications and value for money.

OVO is also one of five suppliers in breach of its regulatory capital obligations with Ofgem, something it shares with Octopus. And it was recently forced to resort to refinancing its operations on a sub-investment grade basis with a loan paying 12% plus an unspecified uplift.

And if that wasn’t bad enough, it was recently fined £2.7 million for failures to apply the Warm Homes Discount correctly. This came after a September 2024 fine of £2.37 million relating to inadequate handling of customer complaints.

OVO’s accounts tell a concerning story

There’s something revealing about a company that goes long on glossy group narratives and “path to net zero” language across its entire corporate tree, yet quietly uses the exact same going concern uncertainty in the statutory accounts of multiple legal entities. At first glance this may look like sloppy drafting – after all, each company in the group also shares the same preamble about objectives and mission – but when the repeating language extends from the regulated supplier at the bottom of the structure, up through finance companies and holding companies, it stops being about drafting and starts being telling.

OVO Energy Ltd, the licensed supplier, has big turnover and significant customer numbers. It is covered in mainstream press as a decarbonisation story – a challenger supplier taking on the legacy “Big Six”, and a provider of greener energy. But scratch the surface, and a different picture emerges – one where the financial engine is fragile, where capital adequacy is well, inadequate, and the consumer experience is underwhelming.

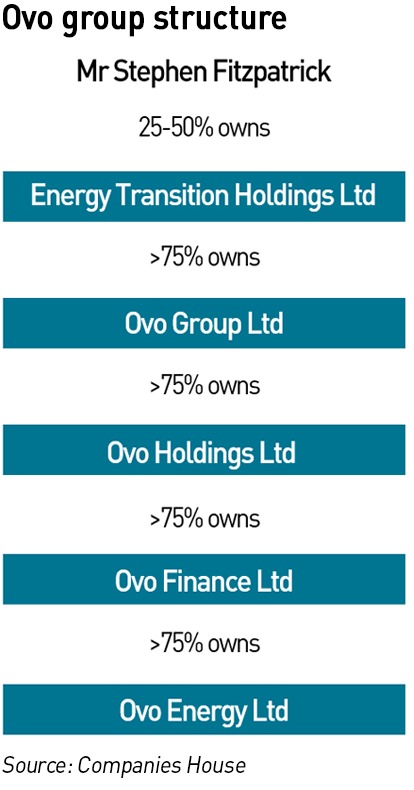

At its base, the OVO corporate family is structured with several distinct legal entities: from the ultimate parent (Energy Transition Holdings), through OVO Group and OVO Holdings, down to OVO Finance and the licensed supply entity OVO Energy Ltd. In legal and regulatory terms, those entities serve different purposes, but from an economic standpoint, what they all reference, describe and depend on is the same underlying activity, that is supplying gas and electricity to consumers in the UK.

That is apparent in the repetition of the directors’ report preamble across multiple company accounts. Instead of distinct narratives that reflect independent business activities, the text is lifted verbatim – not just generic corporate boilerplate, but the same description of customers and strategy applied to entities whose only real purpose is to hold shares, raise finance, or manage intercompany balances. This is a structural flag which says that despite claims that the group operates “in multiple areas and markets”, it really boils down to a single, simple supply business.

OVO Energy Ltd, is the company with the supply licences, the bills, the hedging, the customer receivables and payables, and the regulatory capital obligations. Over the past four reporting years (2021–2024), the statutory accounts of OVO Energy Ltd show a supply business whose reported performance has been dominated by wholesale price volatility and derivatives accounting, while its underlying capital position has remained weak.

Turnover rose from £0.96 billion in 2021 to £5.04 billion in 2022 and £8.17 billion in 2023, before falling back to £5.46 billion in 2024. Gross profit increased from roughly £99 million (2021) to £387 million (2022) and £884 million (2023), before easing to £760 million (2024). However, this headline gross profit has had to absorb very substantial operating cost: administrative expenses were £354 million in 2021, rose to £418 million in 2022, peaked at £670 million in 2023, and remained high at £562 million in 2024. In parallel, bad debt /impairment has been material throughout. Net impairment losses on financial assets were £80 million in 2021, £113 million in 2022, £214 million in 2023, and £212 million in 2024. The overall impression is of a business with scale, but with cost and credit pressures that consume much of the gross margin.

Hedging has a major impact on OVO’s finances

The statutory profit and loss account is also heavily distorted by derivatives remeasurement, which swings violently year to year. The “remeasurement of derivative energy contracts” line moved from a gain of £429 million in 2021 to a loss of £1.446 billion in 2022, back to a gain of £1.086 billion in 2023, and then to a smaller loss of £60 million in 2024. Unsurprisingly, profit after tax follows the same rollercoaster: £279 million profit (2021), £1.273 billion loss (2022), £810 million profit (2023) and £110 million loss (2024). This is important because it highlights that statutory profit is not a stable indicator of underlying retail margin; it is largely an artefact of how the hedge book is valued at each year end.

The hedging question is very interesting. If OVO were hedging in the straightforward way most domestic suppliers appear to hedge, that is broadly tracking the Ofgem cap methodology, then two things ought to be true. First, a supplier with around four million customers should be one of the easiest businesses to achieve hedge accounting as the underlying demand base is large and statistically stable, the hedged item (forecast wholesale purchases to serve domestic load) is well defined, and the procurement approach is anchored to a published and repeatable methodology.

Second, even if the company chose not to adopt hedge accounting, it should still be able to show, in its disclosures, that year-end mark-to-market positions unwind into realised procurement cashflows over the next accounting period and, over time, stop dominating the story. What we see instead is violent derivative remeasurement volatility over several years, without an accompanying repair in the licensed supplier’s equity position.

One explanation for this is that OVO is running a more discretionary procurement strategy, trying to outperform the cap allowance, shifting timing, or taking exposures that aren’t cleanly cap-mirroring. But if that were working effectively, you would expect to see it in the fundamentals with stronger and more stable underlying profitability and, crucially, an improving capital position. Instead, the licensed supplier remains deeply balance-sheet insolvent and its deficit worsens from 2023 to 2024.

Another explanation is sheer operational ineptitude – that OVO “can’t” implement hedge accounting or doesn’t have the necessary internal controls to evidence hedge effectiveness. That’s hard to believe for a supplier of this scale. While hedge accounting is not without challenges, it’s routine for commodity-exposed businesses, and a four-million-customer domestic book should be close to a best-case scenario. If auditors truly refused to accept well-documented hedge relationships, a competent management team would typically fix the process, upgrade systems, or change audit approach rather than tolerate years of reputationally damaging volatility. Ultimately the management can choose to replace the auditors with a firm more familiar with hedge accounting if this is the barrier.

Another possibility is the “evil genius smokescreen” argument where the company is using large MTM hedging swings to distract readers of the accounts from its underlying financial weakness. This argument does not hold water – if the management were truly capable of orchestrating sophisticated opacity, they would be capable of running a more stable and profitable business.

This leaves the most plausible alternative – the hedge book has been managed under distress constraints, shaped less by a cap-tracking philosophy and more by what is fundable given liquidity, collateral and counterparty limits. In that world, hedges are entered when the stars align in terms of collateral and funding rather than when it’s optimal for managing the underlying risk. This would prevent the use of hedge accounting, and result in the persistent MTM swings that do not “wash out” into a healthier equity base. This is what we see in the OVO accounts, possibly because the cash cost of carrying those positions (margin, credit terms, refinancing) and the wider survival costs (bad debt, operating strain) permanently damage capital. And this suggests that even before the recent refinancing (see below) OVO was not operating its business on a stable footing.

If this is true, the coming months could result in real stress for the business. We’re seeing significant price volatility at TTF, with another inversion of the WIN-SUM spread as low storage levels imply a large buying imperative through the summer. Gas storage levels in the EU are now just 41% according to the EU’s Aggregated Gas inventory Database – lower than any year since 2018 except 2022 when it was 37% at the end of January, and well below the 9-year average of 55%. Withdrawals accelerated rapidly in January from over 61% at the start of the year, due to cold weather, and the combination of diminished pipeline flows (notably following the post-Ukraine shifts in Russian supply) and continued reliance on LNG imports.

Supply concerns have driven prices to their biggest monthly increase in more than two years, with TTF rising to €42.60 /MWh in the past week, a ten-month high. Prices have also been affected by severe winter storms in the US, affecting LNG exports – the EU is missing roughly 130 full-sized cargoes’ worth of gas compared with a year ago.

The European benchmark forward curve has yet again inverted, with winter prices now trading below the summer, a condition that weakens the commercial incentive to fill storage and complicates hedging strategies. This leaves the EU in the same bind it faced a year ago when a similar inversion forced a relaxation of the storage filling mandate. Utilities do not want to fill storage when it will be loss-making to do so, regardless of wider security of supply concerns which no individual company feels inclined to fund.

The result is higher near-term volatility and elevated forward prices, as reflected in recent TTF price behaviour where near contracts spike on weather or supply news even while out-year prices remain softer. As TTF volatility tends to translate to NBP volatility, this will inevitably impact OVO, whose hedging programme exhibits signs of structural weakness. This volatility will increase the risk of asymmetric mark-to-market impacts and make them more expensive to carry as short-dated prices jump, and collateral requirements can be triggered even if the longer-dated economics eventually converge.

The risk isn’t that OVO will struggle to buy gas, but that the collateral and funding requirements that go along with it will drain it of liquidity, forcing the business into insolvency.

OVO resorted to borrowing at sub-investment grade levels

The OVO balance sheet tells an even more worrying story about capital strength than the P&L – despite the profitable 2023 year, the company ended 2024 with a shareholders’ deficit of £726 million, worse than the £617 million deficit at the end of 2023.

In other words, the licensed supplier remains deeply balance-sheet insolvent: liabilities exceed assets by £hundreds of millions, and the direction of travel from 2023 to 2024 is negative rather than improving. This matters not just from a creditor perspective but from a regulatory perspective, as the 2024 audit report includes a material uncertainty related to going concern, explicitly linked to Ofgem’s capital adequacy framework effective from 31 March 2025 and the requirement for a recapitalisation plan supported by the group.

Liquidity and working capital are the other major stress point. At 31 December 2024, OVO Energy Ltd reported current assets of £987 million against creditors due within one year of £3.097 billion, leaving net current liabilities of around £2.110 billion. This is an extremely large negative working capital position, and it implies that the business is being funded by short-term creditor balances and the timing of customer cashflows. Funding supply business through consumer credit balances is something rival Centrica has consistently campaigned against, lobbying Ofgem to require suppliers to ring-fence customer money and not use it to fund ongoing supplier operations.

Negative working capital is not unusual in energy supply, but at this scale it becomes a key vulnerability as any tightening of credit terms by counterparties, any increase in collateral requirements linked to wholesale hedging, or any deterioration in customer payment behaviour can create an immediate liquidity squeeze. The financing response appears consistent with that risk profile. In January 2025 the company granted a comprehensive security package in favour of GLAS Trust Corporation Ltd (fixed and floating charges, mortgage, security over trademarks/IP and a negative pledge), which is consistent with secured “special situations” funding and aligns with reports of an expensive £60 million facility priced at junk levels. This is almost certainly connected with the a £60 million facility paying 12% interest taken out with Cheyne Capital Management, which was reported last year and is likely the facility referred to in the accounts.

At the time, the Times Newspaper said: “Ovo has been working with bankers from Rothschild for more than a year to explore fundraising options as it seeks to shore up its balance sheet. David Buttress, chief executive of Ovo, told The Times earlier this year that it was seeking to raise a sum “in the hundreds of millions”.”

The GLAS filing is not the kind of routine security you see on ordinary corporate borrowing – it reads like a classic distressed-credit debenture, giving the lender extensive control rights through fixed and floating charges over the company’s assets, including a legal mortgage and security over intellectual property (including trademarks), alongside negative pledge-style protections. Healthy utilities do not generally need to pledge the corporate crown jewels to access liquidity.

At the same time OVO repaid its £300 million term load facility and £100 million second lien term loan facility. It also secured a £50 million capital injection from OVO Holdings Ltd (ie not the immediate parent) and sold subsidiary Kaluza Ltd to OVO Holdings for £185 million.

This is best understood not as a conventional refinancing, but as a re-ordering of the group’s capital structure under stress, where the objective is to keep the regulated supplier viable (and fundable) while the market is simultaneously signalling a deterioration in credit quality. On the face of it, repaying a £300 million term loan facility and a £100 million second lien term loan sounds like a strong deleveraging move. But the context matters, and here the paydown is occurring alongside the raising of a much smaller, very expensive facility (£60 million at junk-like pricing) and accompanied by a package of intra-group transactions.

That pattern is not what you see when a borrower’s credit profile is improving. It’s what you see when the group is being forced to shrink the quantum of external debt it can sustain, to remove imminent maturities or covenant pressure, and to replace it with short-term, highly secured liquidity that lenders are willing to provide only on “special situations” terms. In other words, the apparent reduction in gross borrowings does not reflect increased financial strength, but more likely reflects reduced access to mainstream credit and a strategic pivot to whatever liquidity remains available, even at punitive pricing and with heavy security.

The intra-group elements are particularly telling because they look less like genuine recapitalisation and more like financial engineering designed to create capital where it’s needed most. A £50 million capital injection from OVO Holdings (rather than the immediate parent) suggests that capital is being routed through the group structure in a deliberate way, potentially because of restrictions, regulatory optics, or lender requirements about where cash can sit and what it can be used for.

The £185 million sale of Kaluza to OVO Holdings strengthens that interpretation – a sale of a subsidiary within the same corporate family does not create new value at a consolidated level, but it can materially alter the presentation of solvency and liquidity at the level of the regulated entity (or the borrowing entity) by converting an illiquid “strategic asset” into cash or an intercompany claim, and by shifting valuable assets into a different perimeter for security, governance, or future monetisation. This is a classic move in groups under pressure. Assets are ring-fenced, moved, or sold internally, not because they have suddenly become less important strategically, but because the core operating entity requires immediate balance sheet support and the group needs to demonstrate capital adequacy to regulators and funders. Crucially, this does not necessarily make the group safer – it can simply redistribute risk and delay the day of reckoning.

Finally, the going concern language at the TopCo level is key as it undermines the comforting narrative that the group is a stable sponsor propping up a weak operating company. If the entity providing support has its own going concern sensitivity, then support is not a one-way transfer from strength to weakness, it’s a circular dependency within a stressed corporate ecosystem. This makes the package of transactions looks like a managed survival exercise, that reduces externally visible leverage because the market will not fund it at scale, substituting in expensive secured liquidity to bridge near-term needs, and using intra-group transfers to improve regulatory and covenant optics without fundamentally curing the underlying fragility.

Essentially, the OVO Group looks like a snake swallowing its own tail.

Overlapping uncertainties and the going concern disclosures

One of the most striking features of reading the statutory accounts across the group is how often the same going concern caveats appear. Whether in the licensed supplier’s accounts, in the finances of OVO Finance, or up at the ultimate parent company level, there is near-identical language about dependency on support, recapitalisation plans, and regulatory capital compliance.

This is not a sign of diversified risk – in fact, it’s the exact opposite. It reflects an internal circularity where the operating entity needs backing from the group, while the group’s financial health relies on the operating entity, and the regulator’s confidence hinges on plans that have not yet been fully executed. In corporate finance terms this is not a structural hedge so much as a Rube Goldberg of internal claims where one company’s assets are another company’s receivables, and every entity is linked by internal guarantees or support letters that may not survive stress.

Compare that with a truly diversified group, where different subsidiaries have independent cash flows, distinct client bases, and separate capital bases. OVO’s structure does not fit that pattern. Instead, it fits the pattern of a single cashflow engine whose financial health is re-expressed multiple times in slightly different legal wrappers. When each one says “there is material uncertainty over the ability to continue as a going concern unless certain plans are implemented”, it suggests that none of them has a truly independent going concern footing. This is not defensive drafting, it’s systemic ambiguity.

Which brings us to the core question: when you collapse out all the intra-group receivables and look at the real economic balance sheet, do you see a strong group with genuine capital resilience, or something closer to a house of cards?

On a consolidated basis, OVO might show revenues and cash that look respectable. But when you strip out the intercompany transfers, the only real cash generator is the licensed supply business – a business which is technically insolvent on a standalone basis. Negative equity is not something that goes away because a different company up the tree has a positive net asset position.

One way to see this is to ask, if the holding company disappeared tomorrow, would the supplier still be solvent and capital-adequate? The accounts suggest the answer is no. The licensed supplier depends on an ongoing capital plan, and the regulator has made clear that it expects that plan to be executed in a way that demonstrably improves the capital base. Without that plan, the going concern uncertainty flag remains.

Now layer on the fact that part of the group’s funding effort involved repaying £400 million in earlier facilities and then taking on a new £60 million facility at distressed pricing. That is a classic signal of refinancing risk where creditors are only willing to lend a relatively small amount on expensive terms, secured by comprehensive charges over assets and intercompany rights, because they see the risk as real and immediate.

So where does that leave the true going concern position? It means there is a supply business that is operationally viable for now – the lights stay on, payments go out, customers are billed – but financially tenuous in the absence of ongoing support. The regulatory regime in the UK after the failures of the early 2020s has made it clear that suppliers must hold resilient capital and withstand stress without collapsing. OVO’s own accounts show that it has agreed a plan with Ofgem for transition to new requirements, but they also show that the plan’s execution has timing risk and is not yet completed.

Is OVO a robust supplier or a basket case?

Whether OVO is truly robust depends on the strength of the parent guarantees it has in place and whether there is support from Stephen Fitzpatrick himself or one of his entities that is not formally within the OVO Group. If so there is no documentation of such an arrangement in the public domain. The repeated going concern disclosures at each level of the corporate ownership chain do not inspire confidence – to be sure the Group was really robust there should be some form of guarantee from an entity whose own going concern status is not in doubt.

Nor does it appear that there are either other material cash generating businesses in the group that could assist the credit profile, or significant assets that could be sold to strengthen the group balance sheet.

OVO’s approach to hedging appears to be somewhat chaotic. While large MTM swings are not in themselves a cause for concern, the fact they do not resolve into a more stable equity position and there is no effort by the company to demonstrate that its hedging approach is effective, is concerning. Hedge accounting can be a straight-jacket for companies that inhibits optimal economic hedging, but this is not really the case in the British retail energy supply business where most consumers buy on the regulated tariff which has a very regimented calculation methodology most companies seek to emulate to ensure they can efficiently pass wholesale costs through to consumers. So why is OVO not doing the same? A credible explanation is that it can’t due to credit constraints, and this is also a major source of concern, not least as we face a period of elevated gas market volatility.

One detail that deserves more attention is the group’s reported use of Rothschild. The Times reported that OVO had been working with Rothschild bankers for “more than a year” to explore fundraising options, seeking to raise “hundreds of millions” to shore up the balance sheet. This is not the kind of advisory mandate a well-capitalised utility takes on for routine housekeeping. When a company hires a top-tier restructuring and capital markets adviser for an extended period, it’s usually because the situation has moved beyond incremental tweaks and into the realm of capital stack triage. It’s also noteworthy that OVO has hired such an expensive advisor over an extended period.

Finally, raising capital on what can only be described as distressed debt terms is a real red flag.

Should the FCA regulate energy suppliers?

Regular readers will know that this has been a bugbear of mine for a while. Energy suppliers are virtual businesses whose key role is to handle customer money and do some accounting. This shares more in common with a retail bank than with either a generator or regulated network business. The fact that Ofgem has been forced to develop a prudential regime at all is telling…and I have argued that once this became clear, the job should have been passed to the banking regulators who have more experience with this.

If OVO were to fail, the political fallout would not be confined to one company, because OVO is big – more than double the size of Bulb when it failed with 1.7 million customers. Such a failure would land squarely on Ofgem’s prudential regime. Ofgem’s culture and toolkit are those of a utilities regulator with price controls, consumer protection, licence conditions and political balancing. But prudential regulation is built around a different philosophy. It assumes that confidence itself is a system variable, and that transparency is not a threat but a stabilising factor.

The FCA/PRA model in financial services is premised on the idea that markets function better when there is credible supervision, clear disclosure, and enforceable constraints on growth when capital is weak. Ofgem, by contrast, still tends to treat supplier capital weakness as a quasi-private supervisory matter, rather than something that customers and counterparties should be able to understand and price. That approach might have been defensible when supplier failures were small, but less so when one or two suppliers are now systemically important.

An OVO failure would bring this into sharp focus. It would force the question of why a supplier on a recapitalisation plan could continue to acquire customers, and why the regulator withheld basic information about the scale of capital shortfalls and the remedies agreed. In banking, it would be unthinkable for a regulator to allow an undercapitalised institution to expand aggressively while the public was kept in the dark about its remediation status. Yet that is close to the current position in energy supply. It’s hard to avoid the conclusion that Ofgem is trying to strike a balance between commercial confidentiality and consumer confidence, but may be striking it wrongly, by over-protecting supplier confidentiality at the cost of market discipline and informed consumer choice.

For these reasons, the case for moving retail supply regulation under an FCA-style framework is becoming stronger. Retail supply strongly resembles a financial intermediary and should therefore be regulated as such by a regulator experienced with those dynamics rather than the dynamics of price controls and energy system adequacy. That is precisely the domain where the FCA/PRA model has decades of experience, mature disclosure norms, and intervention tools such as restrictions on growth, dividend bans, liquidity requirements and public remediation frameworks.

.

OVO Energy is one of the weakest businesses I’ve looked at in a while. It’s accounts make for painful reading and we know it is not meeting Ofgem capital requirements. It should focus its efforts on strengthening its balance sheet rather than issuing “climate transition plans” unless the climate in question is its borrowing environment. But as one of the largest suppliers in the market, more than double the size of Bulb which caused so much disruption when it failed, this all matters.

Since Octopus is also in breach of its capital requirements, it is untenable that it could be a Supplier of Last Resort for OVO as this would add some £460 million to its capital shortfall – only Centrica would have the balance sheet for this. Perhaps it would have the appetite, but perhaps not. In Centrica’s shoes I may shy away from being the backstop for the energy market, used only when all else fails. Maybe Centrica should sit back and watch the fall out, mopping up when the Government finally decides to get serious about energy supplier robustness, and the need to properly ringfence customer assets.

Another interesting and long read. The snake swallowing its tail seems a very pertinent description. As a customer, i have often tried to contact OFGEM and been successful only once regarding the poor competitive market for those using off peak E7 electricity for domestic heating, It seems that priority is given to EV users who get the best off peak rates, albeit for shorter times. Domestic heating should be a priority and OFGEM should recognise this and try to enforce tighter control. This from a customer who has used off peak electrity for heating for over 40 years (moving from fossi fuel) and had electric cars for 12 years.

Whatever happened to stodgy old utility companies, who kept the lights on and the gas flowing without much, if any drama like this? Where the hedging is done by the fuel purchasing guys inside the generating companies, based on their knowledge of how the energy demand works? The companies that made steady but not spectacular amounts of money, for widows and orphans, very much like government bonds are now go-go hedge fund operators, speculating on whether the gas supplies will arrive in the next tanker from Russia or the USA, where the political situation makes this speculation even more uncertain?

It is like someone in the utility business got bored with it, and decided to just start gambling, to make his life more fun and interesting. Who would ever think this could be a good idea?

One problem is that energy costs have become less predictable, with renewables and dispatchable capacity shortage adding to price volatility. Coal, gas and nuclear were all fairly stable costs before renewables.

We did see a gas price spike in 2005/6 because the Langeled pipeline was unexpectedly delayed, and prices crept up a bit after that because we were paying to import from Norway. The energy crisis was more general, and included the effects of reduced nuclear in France and the UK, and the Dutch decision to close Groningen and the effects of disappointing renewables output for wind, solar and hydro. It was not just Russia turning off Europe’s gas taps, followed by the Ukraine war and Nordstream sabotage.

Dear Kathryn, thank you for this.

I can say the relationship I have with Ovo Energy as a consumer is not great.

There is no way to give feedback.

I routinely get multiple view of my account, citing debt which is not the case.

Sometimes in a given month I get two versions of the invoice – never explained.

The whole thing feels like the company is using a Commodore ZX81 (a fine machine 44 years ago) as the primary IT server.

If they are funding their capital structure through customer credit, then is there a chance that if they do go bust that customers with a positive account balance will lose out?

Would it be sensible as an OVO customer to insist on moving to pay in arrears billing for what you have used?

The idea is of course sound.

However, I was a customer in the Orbit energy fiasco, where they tried to stick me for £4000 in one month (resisted, not paid, no apology for the error) but a months later went bust and took my credit cash with them.

No sign of Ofgem.

What is clear the ‘shops’ use billing as an ATM (exactly the change in behaviour with Ovo for about a year now, just as Orbit did before going bust) and Ofgem act for the few but not the consumer.

Overall, the energy retail sector stinks.

The SOLR regime guarantees customer balances, which is perhaps why OFGEM are insufficiently proactive in heading off bankruptcies. We all pay for that when firms implode. I don’t think it should do. If you deal with say a builder you take the hit on any advance monies if it goes bust before your extension is complete, so you try to choose carefully.

I’ve finally found something that I agree with Centrica about! There’s no way that customers funds should be allowed to be risked by a business without that risk being made explicitly clear to customers. Allowing this to happen without moral hazard is wrong – Bulb customers were effectively insured by the rest of us despite buying unrealistically inexpensive products. It appears that OVO are heading the same way and that the taxpayer may not get off the hook this time.

I agree absolutely. Customers who have benefited from unduly cheap power used to buy their business should share the pain of bankruptcy, not be bailed out by the rest of us. If they wish to avoid that risk they should pay insurance, like ABTA in the travel industry.

Chris O’Shea of Centrica had a lot to say about under-capitaliseed retailers here

https://committees.parliament.uk/oralevidence/16535/html/

He suggests there should be a public register of financial soundness.among other ideas.

Exellent work. Could this be sent to all MPs at Parliament? Then await comments if any are capable of reading it.

Many people have their accounts in credit. All companies should be made to ring fence customers money by law as this belongs to the customer and not OVO. Its ridiculous that its trying to baleout of an impossible position. Where is the regulatory body in all this.

Thank you for an intriguing and fascinating insight into the parlous state of the supply industry.

And all that despite us having some of the highest domestic pricing.

Ive been watching what little commentary there has been on Octopus as I am a customer.

I find the entire structure of the industry and its many payment mechanisms mind boggling.

Would be intersting if you did a piece on how you think it should ideally be re-structured to make it efficient and cost effective.

OVO is currently trying to force me to have a Smart Meter fitted. They can pry my GEC ‘Bake-o-lite’ electromechanical meter out of my cold, dead hands.

I would be a bit more enthusiastic about Smart Meters if it weren’t for the specification that mandates all of them to have a remote-controlled disconnector inside them. What is the reasoning for that, aside from making cyber-attackers very excited?

My guess would be that future electricity supply contracts will start disconnecting customers on cheaper rates when there is a shortage. Pay us extra to be further down the list of those who will be disconnected. This would of course be a mafia-style protection racket, but with privatised utilities skimping on infrastructure spend, I could see it happening.

I can maybe ask for a ‘dumb’ meter even if OVO insists it must be Smart, but even then I expect it would still be a Smart meter, just one operating in fixed-price mode without an IHD, and still containing that remote-disconnect switch.

Rather than replacing all meters just because of their age, they should carry a calibrated check meter to re-certify old meters. It would be so much cheaper than replacing them all.

Hi Tom

Utilities companies will not do a calibration check on meters because this would mean putting a check meter in to see if the meter is reading correctly, then if it wasn’t replacing it with a heritage meter and this would all be done at the Utilities company own expense costing millions.

Smart meters are all rented part of your daily standing charge goes to paying that rent and the company they are rented from pays the utilities company to fit that smart meter

Which is why you need to get progressing towards self-generation and an off-grid system, that you can run entirely independently of the grid. With Hybrid warfare, a National Grid is a liability, and as you say, with cyber-attackers represents a clear weakness, which, if you want a stable electricity supply, the only way is by self-generation. With AI advancing, it won’t be too long before every crackpot state has the same cyber-warfare capability as the reasonable democratic countries. Then there are the criminals and international ransom attacks. Things aren’t going to be stable for many years, and it’s not the technical ability of the people working in the electricity industry that will be causing the problems. There are too many people around willing to damage the interests of others or willing to gain a benefit from causing misfortune/problems for others.

Ed Hogbin: “As a customer, i have often tried to contact OFGEM and been successful only once regarding the poor competitive market for those using off peak E7 electricity for domestic heating, It seems that priority is given to EV users who get the best off peak rates, albeit for shorter times.”

That’s because EV charging demand is all-year round; domestic (space) heating demand is only for (generally) just over half a year, but concentrated in Winter, when >50% occurs in the winter quarter.

Great Britain’s space heating energy demand profile by season is roughly: Winter (D,J,F) ~52%; Spring (M,A,M) ~26%; Summer (J,J,A) ~1%; Autumn (S,O,N) ~21%

Well, indeed, as you say, but that will make the conundrum of how to deal with electricity for domestic heating even harder. Demand will be much higher in the winter months as people switch to heat pumps but will be in the daytime just as it is with gas. For every 3 heat pump homes, it would be wise to have one with domestic thermal storage. New and better technology does exist ie with better insulated and fan assisted storage heaters or the Tepeo boiler. And, of course, this type of storage costs the industry nothing. Yes, increasing use of EVs will be consumer funded storage but this will be flat all year round. Taxing EV use is already coming but really government and industry need to have a plan of how they will provide the increasing electricity we need over the next 30 years in a timely, flexible and efficient way. But, I forgot, thats not how government and industry work; so, chaos ensues.

Illuminating but worrying. Thank you, Kathryn, for this detailed analysis.

“An OVO failure would bring this into sharp focus. It would force the question of why a supplier on a recapitalisation plan could continue to acquire customers”

Worth mentioning that OVO has stopped “actively” seeking to acquire customers, by agreement with OFGEM. So they are off comparison websites and are doing no marketing or promotion. But you can still sign up if you actively want to.

Thank you for your investigative journalism. When I asked Google about the bankruptcy risk of Ovo Energy, this is their response. I’m glad I’m not a customer.

Based on recent reports, Ovo Energy has faced significant financial headwinds, including a return to loss in 2024 and failing to meet new regulatory cash-holding targets, though it remains a major operator in the UK energy market.

Key details regarding OVO’s financial status and risks as of late 2025/early 2026:

Financial Performance: OVO reported a loss of £135 million for the end of 2024, a sharp downturn from a £1.1 billion profit reported at the end of 2023. Annual revenues fell by over £3 billion to £5.5 billion, and adjusted EBITDA dropped from £225 million to £42 million.

Regulatory & Operational Pressures: Following the 2022 UK energy crisis, new regulations require suppliers to hold specific cash reserves. As of late 2025, OVO was reported as one of three firms that failed to meet these targets.

Restructuring and Stability: The company has undergone leadership shifts, including the return of a former chief, and has been reported to be cutting hundreds of jobs.

Operational Incidents: In January 2026, OVO was fined £2.7 million for failing to properly manage the Warm Home Discount program, which resulted in late payments to roughly 12,000 customers.

Kaluza Risk: Kaluza, the software arm of OVO, saw its default probability rise during the energy crisis, peaking in 2023, though it showed signs of decline by late 2025.

While these factors highlight significant financial pressure, they do not indicate an imminent collapse. However, the company has faced a challenging period of reduced profitability and increased regulatory scrutiny

The apparent recent departure of the Head of Trading is not a good sign, whether he chose to go or not. Here he is giving an excellent explanation of the hedging process

https://modoenergy.com/research/en/podcast-retail-power-trading-gethin-musk-ovo-energy-2025-transmission

Yet it seems that he now is working for Veolia.

https://uk.linkedin.com/in/gethinmusk

Lucy Ovo’s got some ‘splaining to do…

I am £300 in credit with EDF and they have just increased my SO by £10/month.

They also are trying to get me to install a smart meter.

I can’t go on to their cheapest tariff because I won’t!

Hello

Reading your analysis, it’s clear that OVO’s financial fragility is structural, not just cyclical. From a tax and accounting perspective, I’d add that monitoring intercompany balances and derivative mark-to-market volatility is critical, as these can distort both regulatory capital and taxable profits if not reconciled regularly. Implementing stricter internal controls around hedging, collateral, and short-term liquidity reporting could help flag solvency stress before it becomes a crisis.

Thanks

Hello

Your breakdown shows how revenue growth and customer scale can mask weak fundamentals when negative equity, heavy working-capital reliance, and volatile derivative remeasurements dominate the picture. When I review accounts like this, I focus on cash conversion, covenant headroom, and whether hedge documentation supports consistent accounting treatment, since unstable MTM swings often signal liquidity or control issues rather than strategy. It also helps to track customer credit exposure, provisioning policies, and intra-group transactions closely, because these areas often reveal solvency stress earlier than headline profit figures.

ouch, the stress is not only in the balance sheet! I wonder what this now all looks like as we head towards July 2026 with supply shortage driving raised buying costs, a bare shoppng basket as other capital availability to buy will also itself be under stress. May be a perfect storm of which the business could use the situation to colapse and blame it on global fallout the losers being customers and employees.

Here’s an update to your 4 February 2026 article from the 24 April 2026 Mirror by Ben Hurst, “Martin Lewis urges Octopus, E.ON, OVO and EDF customers to act now in Iran war update.” Seems like big price increases related to natural gas supplies as a consequence of the Iran war are likely. Ouch!

It seems Ovo may have solved their problems through a fire sale buyout by Eon.

https://www.energylivenews.com/2026/04/27/is-e-on-about-to-buy-ovo/

The current market conditions are taxing for energy retailers. Assuming the transaction goes through industry concentration will rise sharply, which may concern OFGEM. In reality it is an effect of their micro regulation..