Today I was invited to speak at this month’s meeting of the Parliamentary Group for Energy Studies on the subject of the current energy crisis, and what should be done about it. Here is my presentation, setting out the regulatory mistakes that resulted in the collapse of so many suppliers, and how a new approach to energy regulation is needed:

.

Crisis? What Crisis?

A new approach to energy regulation

Good morning. I’m very happy to be here today to share my thoughts on the energy crisis, and what should be done about it.

We’ve all heard about rising wholesale gas and power prices and the large numbers of energy suppliers that have failed as a result.

Briefly, the reason that prices have risen is that during 2020 gas demand fell by 2.1% while producers responded by cutting output by 3.1%. A cold winter last year eroded gas inventories across Europe. This year demand recovered, but supply was affected by maintenance work held over from 2020, and inventories failed to recover to historic norms by the start of winter. Since gas is the marginal fuel for electricity generation, a tight gas market has pushed power prices higher.

This year 29 suppliers have gone bankrupt representing 56% of companies serving the domestic market.

The Government and Ofgem tell us that these suppliers are poorly run, and that they should have hedged in order to protect themselves against these price rises.

I would like to challenge these assertions, and show how BEIS and Ofgem together created the conditions for the current crisis within the domestic energy market. I will then propose an alternative approach to retail energy regulation.

.

.

Since privatisation, the Government has had a very narrow view of competition: more suppliers = more price competition = lower prices = a benefit to consumers

So the market was opened up and companies encouraged to enter to compete with the large incumbent suppliers. Barriers to entry were virtually non-existent allowing people with minimal experience and little capital to set up shop as an energy supplier.

This was the first mistake.

.

.

Because many of these suppliers were small and poorly capitalised they struggled to access hedging. In order to hedge, companies need to provide collateral, and many of these new suppliers could not afford the collateral required to hedge properly.

Suppliers also need to re-balance their hedge positions as they approach delivery to account for daily shape. For suppliers with small numbers of customers, the trades they need to make to hedge this shape risk are smaller than the clip sizes traded in the market.

Ofgem introduced the Supplier Market Access rules, also known as Secure & Promote in order to improve the ability of small suppliers to hedge, but these rules did not solve these credit and liquidity problems.

This was the second mistake.

.

For a number of years, things were fine. Wholesale prices were low, and challenger suppliers began to win market share from incumbents. But the Government felt this was going too slowly, and Ofgem meddled constantly with different rules on how suppliers could set tariffs.

For a number of years, things were fine. Wholesale prices were low, and challenger suppliers began to win market share from incumbents. But the Government felt this was going too slowly, and Ofgem meddled constantly with different rules on how suppliers could set tariffs.

This culminated in 2016 with the investigation into the energy market by the Competition and Markets Authority which determined that consumers faced a detriment of £1.4 billion as a result of supplier behaviours.

In fact this number was incorrect, and as former regulator Stephen Littlechild has demonstrated, the CMA failed to follow its own guidelines in calculating the detriment. Had the guidelines been followed, the figure would have been 10 times smaller, which was actually a result of Ofgem’s simple tariffs policy.

However, as a result of this erroneous determination, the retail price cap was introduced.

But it is not difficult to imagine that when consumer prices are restricted but wholesale prices are not, suppliers might get into difficulties and ultimately require bailouts. This is exactly what happened in California in the early 2000s.

This was the third mistake.

.

The other thing that happened in 2016 was the collapse of GB Energy, the first supplier in 8 years to fail, as market prices began to rise.

When a supplier fails, its customers are transferred to another supplier through the Supplier of Last Resort or SOLR process. The new supplier must honour any customer credit balances and if the failed suppliers defaulted on green levies such as the Renewables Obligation or Feed-in-Tariff, the shortfall is paid by all other suppliers in the market.

This means that some of the costs of failure are not borne by the shareholders of the failed company but are socialised and ultimately met by consumers.

This was the fourth mistake.

.

In 2018 the price cap legislation was passed. Section 6 of the Act required Ofgem to review the level of the cap at least every six months, but placed no limit on how many times within each 6-monthly period the cap could be adjusted.

Ofgem then needed to ensure that suppliers abided by the cap, which it did through amendments to gas and electricity supply licences. But, crucially, in doing so, Ofgem restricted itself to only reviewing the cap on a fixed 6-monthly schedule.

This was the fifth mistake.

.

Which brings us to the rapid increases in wholesale prices, which Ofgem has described as, and I quote, “unprecedented and unexpected”.

But this is not really true – high prices and bull runs are very common in commodities markets. We are all familiar with oil price shocks, and periods of high prices are common in agricultural commodities where adverse weather can cause crop failures. There is currently an ongoing bull run in the iron ore market.

Sustained increases in commodities markets are neither unprecedented nor unexpected. They are something the regulator should have anticipated.

Not doing so was the sixth mistake.

.

As the wholesale price increases began to bite early this year, suppliers began telling Ofgem that they were struggling. By the end of the summer, suppliers were falling like flies, and despite raising the cap in October, this increase was not enough to enable suppliers to recover wholesale costs from their customers.

The capped default tariff became the cheapest tariff in the market, something former Ofgem CEO, Dermott Nolan recently said the regulator had not anticipated.

This was the seventh and fatal mistake.

.

Ofgem is now trying to put things right and has launched five separate consultations on the cap, one of which would raise it to enable wholesale prices to be recovered and another would insert into gas and electricity supply licences the ability for Ofgem to change the cap level more frequently should market conditions make it necessary.

But Ofgem’s processes are too slow, and it does not intend to implement these changes until April, after the end of the Winter when prices would begin a seasonal easing.

This slow response is likely to see more suppliers fail in the interim.

This is the eighth mistake.

.

Ironically, despite all of these mistakes Ofgem supports the Government’s narrative that only poorly run suppliers are failing. Yet with 56% of suppliers having closed so far this year, surely allowing more than half the market to be poorly run is in itself a major regulatory failure.

Research by Despoina Mantzari and Francesca Pia Vantaggiato of the Centre for Law, Economics and Society, highlights that time and again Ofgem has failed to fully understand the impact of its decisions, and that its un-founded assumptions about the markets and consumer behaviour have led to higher costs and worse consumer outcomes.

Their paper cites the non-discrimination policy of 2009 and the simple tariffs regime of 2010 as particular examples which “attracted wide criticism from the academic community at the time of their introduction”.

They concluded that Ofgem deliberately ignores its own economic analysis in favour of what it believes to be the Government’s preferred course of action.

To the market it often appears that Ofgem lacks a basic understanding of the mechanics of gas and electricity markets, and that it is biased against the supply segment in particular.

Ofgem has certainly lost the confidence of suppliers.

So where should we go from here?

I believe an entirely new approach is needed to retail energy regulation, requiring a change not just in regulatory personnel but also in ministerial supervision.

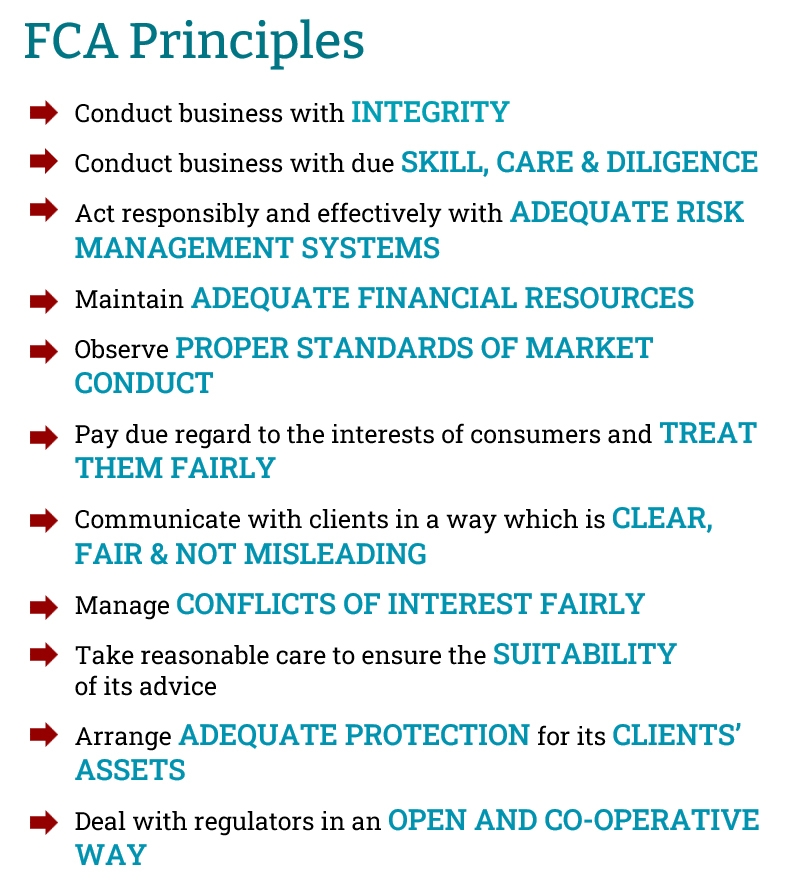

Regulation of the supply segment should be moved from Ofgem to the Financial Conduct Authority, under the supervision of the Treasury.

Energy retail is a fundamentally virtual business – the very features that enabled inexperienced people to set up a supply business from their spare bedroom illustrates that.

The FCA has more experience of principles-based regulation and its principles could and should be applied to the energy market.

The FCA is ultimately supervised by the Treasury meaning that the hostile attitude held by BEIS towards suppliers would be neutralised.

.

Of course the price cap needs to go, and all the other mistakes I mentioned need to be corrected. In addition, there needs to be a proper re-think as to the role of suppliers in the market.

The Government has made a commitment to Net Zero, and would like suppliers to deliver innovative business models that will support consumers on this journey, but in order to do this, suppliers need to earn enough money to fund innovation.

.

So suppliers should stop having to collect taxes in the form of green levies. They should not have to distribute welfare in the form of the Warm Homes Discount. Nor should they be required to engage in home improvements, an area far outside their expertise where the Energy Company Obligation forces them to accept un-competitively priced work to meet their legal duties. And suppliers should not be made to install network equipment in the form of smart meters – this should be the job of network companies.

And, most of all, the relationship between suppliers and the regulator and the Government needs to be less hostile and less adversarial. For as long as both the Government and the regulator throw stones at suppliers, accusing them of profiteering and of being badly run, consumers will not trust them and will not engage with the changes needed to support Net Zero.

Spot on.

An excellent and succinct post – but were the audience receptive. The FCA principles are very sound – particularly not misleading clients (no green-washing), I have been told by my supplier that I receive no coal or nuclear generated electricity (although they have shot themselves in the foot by stating that their resulting CO2 emissions are higher than average).

As an engineer these ‘virtual’ supply companies are of peripheral interest. Does OFGEM understand the impact of its decisions on the ‘real’ world. Market economics are its main focus not the engineering systems which will drive real CO2 reductions. We have already “Unprecedented high winds from an unexpected direction” and in the future predominately wind and solar world “Unprecedented low wind and unexpectedly high demands due to an unprecedented cold spell”

Electricity has been below the political radar for many years – that is about to change.

Good, punchy analysis. I don’t know if you have been following the Lords Select Committee on OFGEM and Net Zero. They have just published transcripts of the oral evidence sessions with OFGEM and BEIS held 30th November which you can access here:

https://committees.parliament.uk/work/1320/ofgem-and-net-zero/publications/

The performance of Brearley was abject when he was tackled on regulation of risk and financial adequacy and consulting the FCA for suppliers. (See bottom of page 13 ff) Perhaps some of your work with the Parliamentary group is bearing real fruit.

More brickbats flew over regulation of DNOs in the aftermath of storm damage to networks. I suspect there will be a lot more to come on that, but we can surely have little confidence in OFGEM and BEIS marking their own homework in investigating. A role for E3C perhaps, who did the main report on the August 2019 blackout.

Interesting how often he began his answers with “honestly”…

It’s all very well saying we need prudential regulation in energy, but Ofgem has no experience of this, although I believe there has been some recruitment of former FCA staff. Better to just have the experts at the FCA take over. Getting to present this idea directly to MPs and Peers was the ideal opportunity for getting it in front of people that might actually be able to make it happen.

On the DNOs and Storm Arwen, I think Ofgem/BEIS need to understand the difference between resilience and redundancy. Our house is on the end of the network with one little wire connecting us to the rest of the village. We have a petrol generator just in case. I don’t necessarily think DNOs should try to protect against 1 in 20 year events – but I do think they should be equipped to support people who are disconnected for more than a few hours, by moving them to hotels or providing alternative sources of energy.

Very interesting insight and hopefully they were listening.

As you mentioned GB Energy Supply Ltd i gave them a look up on Companies House and five years on the administrators are still at work with nearly 500k in fees earned. Unsecured creditors took a 60% hit or about £10m. OK infinitesimal amount in the grand scheme of things but there another 29 now in the hands of administrators many a lot bigger than GB Energy so costs are just mounting up.

I see that the RO mutualisation bill for this year has been announced at £218m.

https://www.current-news.co.uk/news/ro-mutualisation-triggered-for-fourth-year-as-supplier-exits-leaves-shortfall-of-218m

Since RO generators have been making out like bandits from the higher market prices on top of their subsidies, I’ve a suggestion for BEIS and OFGEM. Cancel it. The generators don’t need the money, and bill payers deserve relief from some of the incompetence of policy.

Am just about to put up a post about the RO and the Citizens Advice report which is pretty damning.

You’re right about cancelling the RO for this year though – that’s a really good idea. Unlike CfD holders, they have absolutely been minting it in the current high price environment, and can afford to see a reduction in the RO receipts. The Government would need to legislate to do it, but I don’t see why not as long as it’s clear that the generators are no worse off than if prices had continued at historic levels (to avoid undermining investor confidence). Or a windfall tax could be applied to off-set it.