Today another three suppliers failed: ENSTROGA, Igloo Energy and Symbio Energy all announced they have ceased trading. ENSTROGA had around 6,000 domestic customers, Igloo had roughly 179,000 domestic customers, while Symbio supplied around 48,000 domestic customers and a small number of non-domestic customers.

Igloo and Symbio were two of the five suppliers warned by Ofgem last week after defaulting on their Feed-in-Tariff levelisation payments. This means that nine suppliers have now closed this month after Hub Energy closed in August. Next month sees the Renewable Obligation late payment deadline which typically precipitates supplier failures so it is unlikely that we have seen the last of this particular trend.

“…our core business of energy retail operates in a market that is sadly no longer sustainable for Igloo. The energy price cap which was introduced by Government has been an important tool for ensuring that consumers are not unfairly penalised on standard variable rate tariffs.

While we continue to support the price cap mechanism, the basis on which it’s calculated by Ofgem is designed to favour the largest suppliers and any calls to review this by the challenger brands, like Igloo, continues to be resisted. The current extreme price shock that we’re experiencing is one that few, if anyone, anticipated,”

– Matthew Clemow and Henry Brown, founders, Igloo Energy

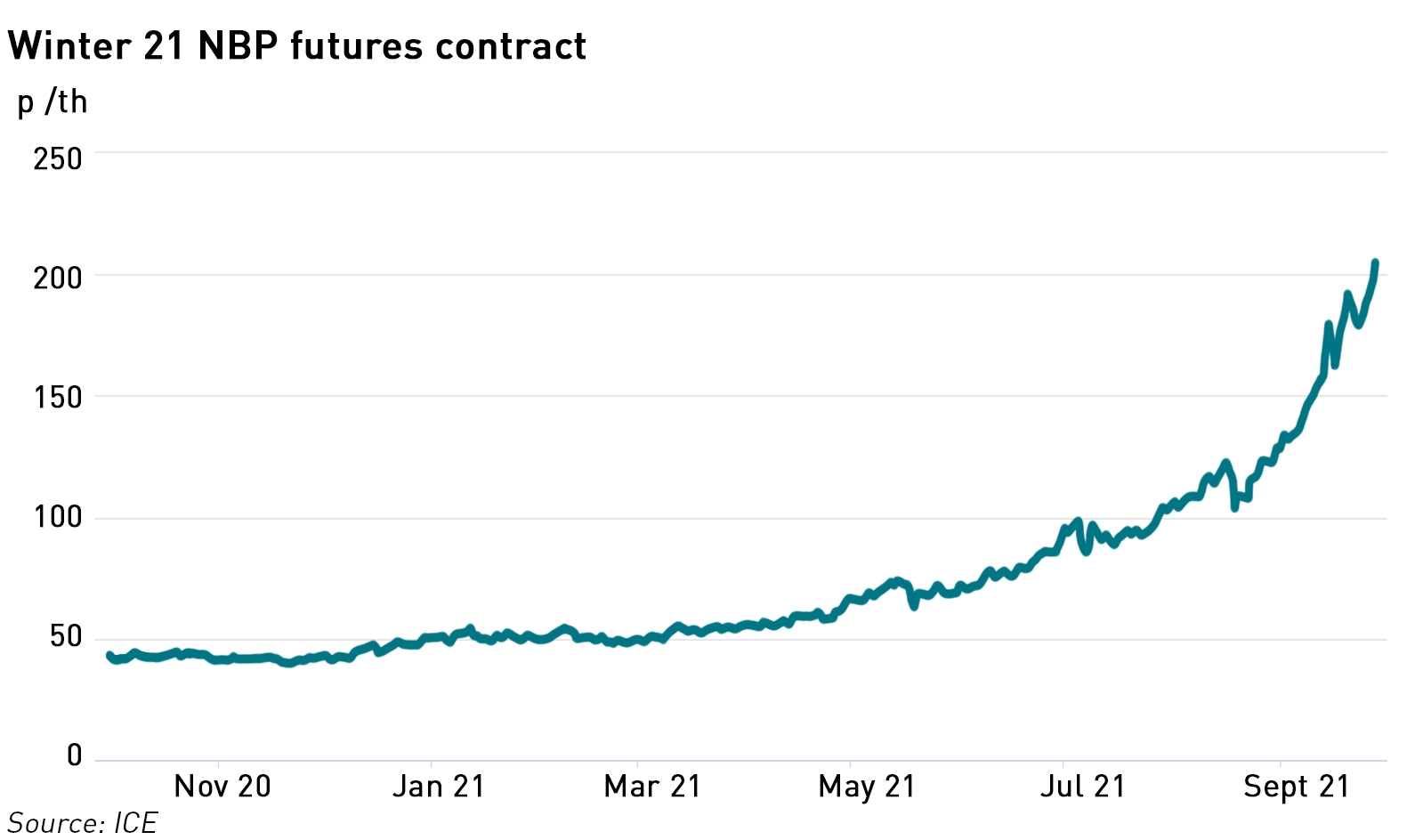

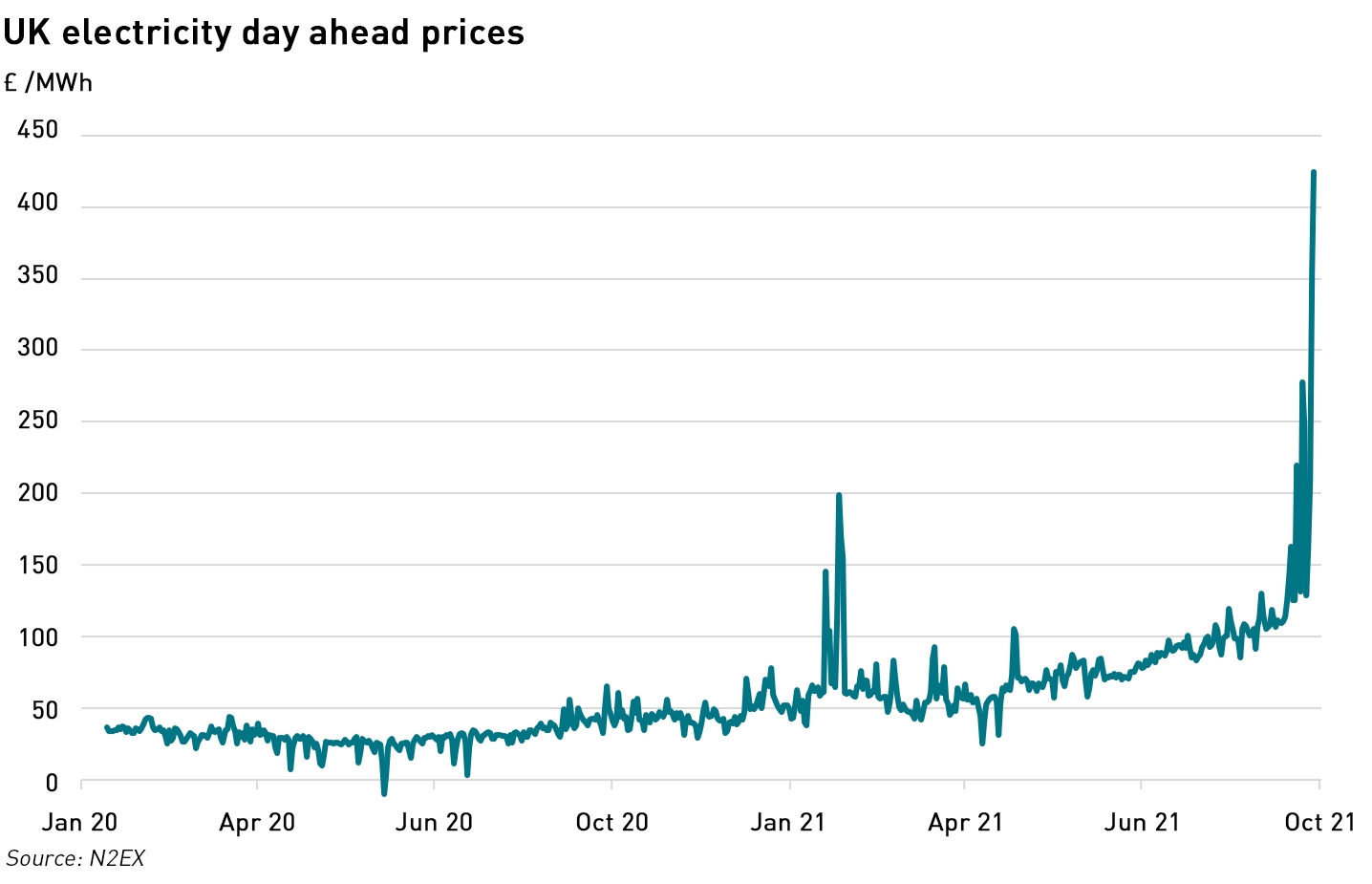

Electricity prices have fallen back from their highs of the last few weeks as a change in weather conditions has brought wind generation back on to the system, but gas prices are continuing to rise, with day ahead prices passing 180 p/th (they briefly touched 196 p/th two weeks ago before falling back). But electricity prices, like gas prices, remain at levels three times higher than those seen this time last year.

Business are bearing the brunt

In my previous posts on the issue I have focused on the domestic segment as this is where the price cap is relevant and is hurting suppliers, but the business supply market is also struggling amid reports that suppliers are increasing their fixed price contracts to business consumers.

One supplier who I won’t name has had the letter they sent to customers announcing price increases posted on LinkedIn. They are justifying their actions by saying that although they considered themselves to be fully hedged, they under-estimated customer demand coming out of the pandemic and therefore were actually under-hedged. They have indicated that the price increases will not apply uniformly to all of their customers and that they will try to compensate the affected businesses by offering them reduced rates in subsequent renewals.

This letter has prompted some debate as to whether demand fluctuations have been large enough to justify this level of action. I can have some sympathy with suppliers in that it is clearly more difficult to forecast demand this year than is usually the case because businesses have been ramping back up after the pandemic at different rates, but failing to honour a fixed price contract rather negates the benefits of having a fixed price in the first place.

This highlights the limited recourse non-domestic consumers have in the energy sector – almost all consumer protections are aimed at households, with some limited additional protection for micro-businesses. But for all other business consumers, the phrase “caveat emptor” is writ large across their contracts (not literally, obviously!)

Unlike in financial services, where financial institutions must demonstrate the suitability of the products they offer to customer, there are almost no protections for non-domestic consumers in the energy markets. Ofgem is only interested if a supplier breaches the terms of its licence, but concepts such as treating customers fairly simply don’t exist in the energy sector.

What is hedging and why does it matter?

The other issue that is becoming more apparent is that a depressingly large number of people in the market are confused about what hedging actually means. Someone created a LinkedIn poll asking what their client should do given they were OK with current prices but very averse to price increases. Several people responses saying it would be a “gamble either way” in terms of whether the client signs a fixed price deal now or later, and that signing onto a fixed price deal now would be “crazy”!

This betrays a fundamental mis-understanding of the purpose of hedging, which is to provide price protection. There are different ways in which price protection can be structured, involving varying degrees of risk, but in this case, a fixed price energy contract should be thought of as a means of securing price certainty, in the same way that a fixed price mortgage does. The holder of the contract is then protected against price increases but is unable to participate in the benefits of falling prices. This situation is often referred to – incorrectly – as “losing money on hedges”, but no money is lost on the hedge as it has done exactly what it was supposed to do – provide price certainty.

There are still risks associated with such hedging, typically around volumes. Many business contracts have volume-related obligations which need to be meet, usually remaining within a certain range. This protects the supplier from being over or under-hedged on its side since it is likely to want to run a reasonably flat book by matching fixed price deals with fixed price hedges.

The other big risk is counterparty default. A fixed price supply contract is not treated like a derivatives contract although in effect that is what it is. As such it does not have the embedded credit protections a derivatives contract would have where the parties are expected to make payments or exchanges of collateral to each other based on the mark-to-market value of the contract from time to time and if certain thresholds are triggered.

Energy consumers are unlikely to want to make margin payments under their energy contracts, although larger consumers are likely to have treasury operations doing exactly that for interest rate and currency hedging. The flip side of this is that they don’t receive collateral payments from their supplier, so when fixed price contracts are heavily in the money for the buyer, as is the case at the moment for many consumers, they face the risk that their supplier goes bankrupt, or tries to impose a price increase despite the price in the contract being fixed.

The lack of regulatory protection means that consumers really only have legal recourse under contract law, and if the move by the supplier was a last ditch effort to avoid bankruptcy the suing it is unlikely to be beneficial even if legally the supplier is in the wrong.

Unfortunately it is difficult for consumers to hedge themselves separately to their supply contract since gas and electricity are primarily traded physically. In the oil markets, there is a highly liquid market for financial swaps, so companies can separate their physical deliveries from their hedging.

They pay their physical supplier a floating price for oil or refined products, and can separately enter into financially settled swaps and options contracts with a hedge provider. This works well because there is a small number of internationally recognised price benchmarks for the different products which allows providers such as banks to provide hedging without ever needing to trade the underlying physical product.

While there are also international benchmarks for gas pricing, they are less liquid and liquidity is concentrated in physical trading. This is even more the case in electricity where the markets are of necessity smaller because electricity is for the most part generated and consumed within similar areas, generally within national borders. There have been arguments for making electricity markets smaller still by introducing regional pricing, but this would drive down liquidity still further.

The upshot of that is that energy hedging for consumers tends to be embedded into their supply contracts, meaning that suppliers reneging on a fixed price deal can create unexpected, un-manageable risks.

Bigger is probably better in the GB energy market, as more supplier failures likely

The conclusion of all of this seems to be that both domestic and commercial consumers would be better of with larger suppliers that have the operational and financial resources to put in place effective hedging programmes and the balance sheet strength to survive periods of high price volatility. This is clearly not what successive governments have had in mind since privatisation, but it seems pretty clear that smaller suppliers are simply too small and too poorly capitalised to withstand the current market conditions.

In the meantime, the FT is reporting that the Government is planning to move green levies from electricity bills onto gas bills. This is not a good idea. Recovering these levies though energy bills is regressive and make supply businesses overly complex – these costs should be recovered through general taxation. (To learn more about non-commodity costs, visit my training website.)

The Government is clearly concerned that it will be difficult to move people away from gas heating to electric heating when gas is so much cheaper due to the absence of these levies, but at best this can only be a short-term measure: if the Government is successful in its electrification drive then it will be recovering these amounts from a shrinking tax base. Time to solve the problem properly and remove them from energy bills altogether.

More suppliers failures are likely in the coming weeks, and there is talk of the market shrinking back to between six and ten suppliers by the end of the winter. It’s past time to enact meaningful market reform.

Aside on petrol shortages

When I first saw the pictures of queues outside petrol stations my first thought was to wonder what was happening in oil and refining to create such a shortage. The answer is nothing – this is not a fuel crisis but a logistics crisis. There is plenty of oil and enough refined products around, but unfortunately there was a concern that these products would not be where people needed them when they needed them.

Whether this concern was legitimate or not, when it became public there was effectively a run on petrol stations with people queuing up to buy because other people were – a classic loss of confidence creating a worse situation than there was to begin with, in the same way that even the best bank will collapse if a sudden loss of confidence causes a run.

This is the price we pay for just-in-time logistics, but it does still make sense because the cost of trying to hold a high level of inventory all the time on the off-chance there might be periodic supply disruptions probably isn’t worth it.

“This is the price we pay for just-in-time logistics, but it does still make sense because the cost of trying to hold a high level of inventory all the time on the off-chance there might be periodic supply disruptions probably isn’t worth it.”

I totally disagree with the last half of that !! … living hand to mouth can turn a minor inconvenience into a disaster.

It’s always good to keep a FULL storeroom a as a buffer against the unexpected; lots of lessons from history & in folk-tails …

Genesis 41 ‘ The seven years of plenty that occurred in the land of Egypt came to an end, and the seven years of famine began to come, as Joseph had said’.

We are not wacko prepers, but apart from perishables we keep a 3 mth stock of most things that we top-up when convenient (or cheap), we always go into winter with 12mths supply of fuel & freezer full. never have less than 50% fuel in a car.

We haven’t had any problems with lockdowns & shortages … but some of our neighbours have.

A small gen-set & changeover switch removes any problems with power cuts.

Any capital cost of doing it this way is offset by buying when prices are low.

Remember the Scout & Guide Motto. “Be prepared”.

Well I think there needs to be some balance with this…take petrol stations as an example…they could hold more stocks of fuel but only by expanding their sites or going under neighbouring sites (which may not be considered safe given the nature of the product). This would be expensive both in the construction cost and in the cost of the inventories, while the benefits of these additional inventories might only be seen every few years. There is a point at which the additional costs are not justified by the costs of the shortages, and that argument can be made both in terms of petrol and gas (hence the closure of Rough).

This current fuel situation is just temporary – people are filling their cars and a few jerry cans, but because people don’t have the capacity for bulk storage at home, that’s all it will be. People aren’t suddenly driving more, so once they have met these limited “stocking up” needs demand will fall quite quickly and things will go back to normal.

Your neighbours may have been inconvenienced by shortages, but were they actually harmed by them? There’s always a cost-benefit analysis to be made and people will have different levels of risk aversion, but there is a point where being prepared is just too expensive, and I believe that is the case with road fuels.

On motor fuel storage it’s not quite true that there have been no changes. We used to be obligated to maintain 60 days of supply as crude plus product stocks while we were in the EU. In practice, some of that stock was held on the Continent. At the beginning of the year we switched to the IEA obligation which is stock equal to 90 days of net imports. As a result, the Continental holdings were dumped and indeed there are small amounts of stock in UK tanks that are providing compulsory storage for other countries. Demand overall was hit hard by lockdowns, and as at June was still only about 80% of pre pandemic levels, so some scaling back of storage probably occurred on that front. Perhaps we will see in the next quarterly Energy Trends release.

Here’s a chart of monthly deliveries.

https://datawrapper.dwcdn.net/amcBl/1/

So far as the maths of the panic is concerned on average a driver gets through a tank of fuel every three weeks or so. On average tanks may be slightly less than half full: some drivers don’t fill up completely probably offsetting those who tend to run with fuller tanks. Create a panic and you condense 10 days of demand into instantaneous demand. Forecourt petrol pumps can deliver at 30 litres a minute or more so 10 pumps can dispense a tanker load in 100 minutes plus the time for switchover between vehicles. Normally that would be a day’s sales at a busy supermarket site, or a week’s sales at a more typical site. There is no way that delivery capability has slack to cope with such a demand surge. It handles bank holiday demand which is probably 20-25% above normal.

Now imagine using V2G to support a wind lull…

I was really talking about changes in terms of what happens at the pump. I remember the discussions around changing the strategic reserves, but don’t really think that makes a difference when the issue is getting the deliveries to petrol stations rather than having the product in the first place.

I had an interesting discussion with some people on LinkedIn about the V2G issue. They were suggesting DNOs might be able to over-ride charging preferences if there was a similar run on car charging, but I thought that would be dangerous since the DNO would not be able to tell which users needed to have their cars ready to use when. You can imagine the scandal if labouring women couldn’t get to hospital because the DNO disconnected their car charger or worse ran down the battery for grid support at the cruicial time. No-one would agree to smart charging on that basis…

Volume flexibility, including cancelling your contract with a hedged supplier, needs to be recognised as put and call options. Options require very active hedging, and can be very expensive when prices are volatile. Implied volatility in prompt electricity and gas markets goes way beyond other markets, and it is no longer good enough to use traditional options models either.

The OFGEM hedging model that assumes hedging 12-18 months forward is probably an inappropriate basis for the industry. We have great tracts of generation that have price guarantees many years forward, granted by governmental fiat, not by hedging demand, partly because the prices have been way above market levels. Some gas production is forward hedged as a condition of financing (and an opportunityforbanks to make more money), but most long term gas contracts are based on spot or nearby futures commodity pricing with limited periods of averaging. In the US it is normal for monthly pricing of consumer supply, which largely eliminates the need for long duration hedging unless the customer demands it. Of course when prices go into orbit as in Texas in February, where gas was trading at $300/MMBtu and power at $9,000/MWh, or about 10 times our already sky high prices you have a different problem. Real shortage. You can’t hedge that.

I see the EV fanatics were celebrating over the fuel issues and of course they can but I do wonder whether we we will see a parallel time when EVs are the dominant form of transport where we are short of generation and we experience a leccy shortage such that they won’t be able to charge up!! Ive seen some RECs suggesting that the chargers should be controllable already to manage demand on local distribution networks so I don’t believe im being that far fetched.