Today Ofgem has launched a couple of new price cap consultations (wholesale costs review and additional debt costs review consultation) which both close on 17 January. The debt costs review in particular has hit the headlines and is widely being reported as a done deal – Ofgem is proposing a £16 increase to the price cap from April to allow suppliers more headroom for managing bad debts. This one-off adjustment – equivalent to around £1.33 a month – would be paid between April 2024 and March 2025. A decision on whether to implement the proposal is expected in February.

The wholesale costs review is less interesting as it essentially says that as the allowances for last year broadly covered the relevant costs, no further adjustments are necessary.

What are bad debts?

Financial difficulties for customers mean that some energy bills are never paid, and are ultimately written off by suppliers. The energy price cap includes an allowance for bad debt costs, which means that the cost of bad debt is socialised across customers who do pay their bills.

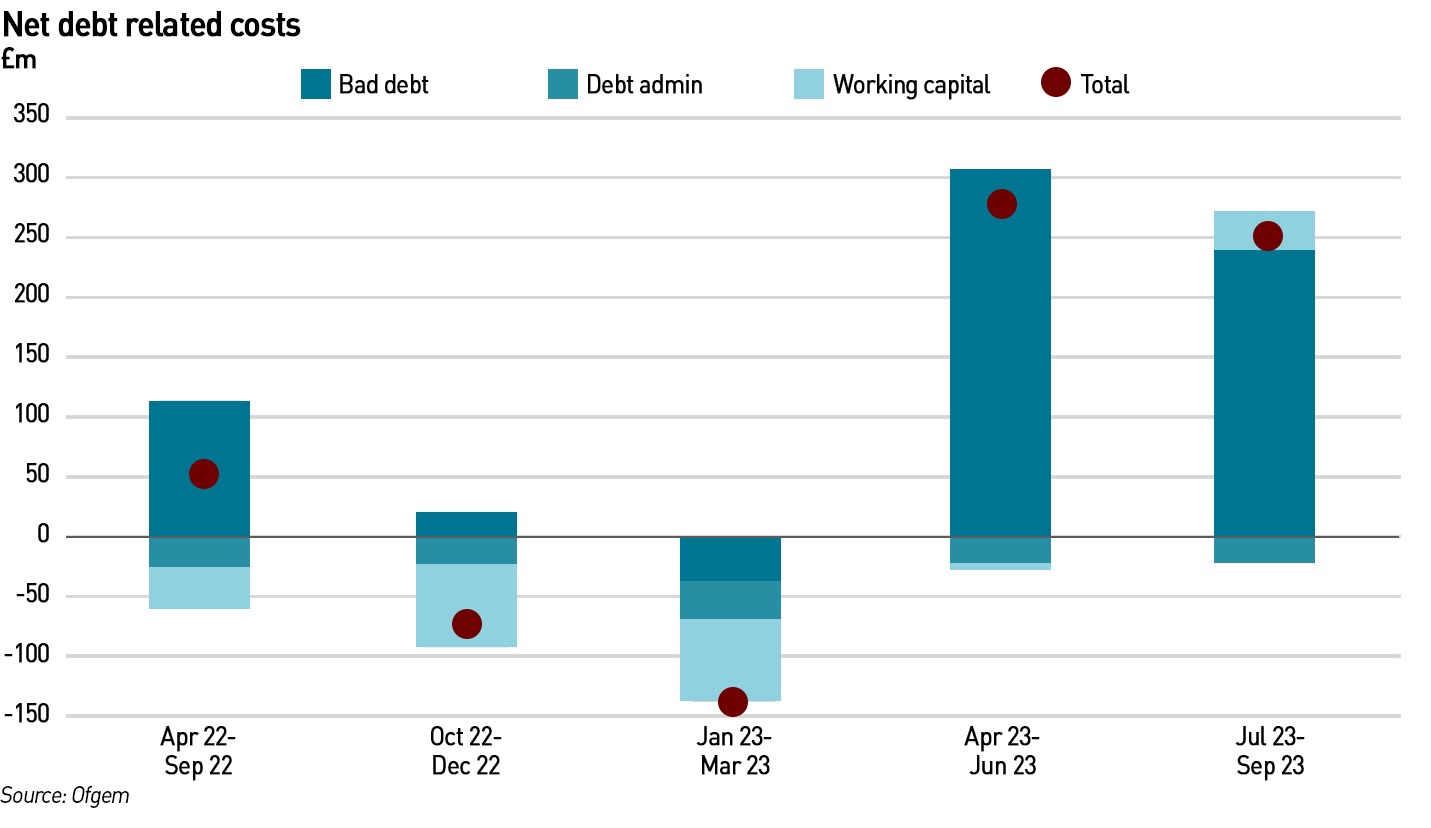

The term “bad debt” is generally used to refer to all debt-related costs, but Ofgem includes three specific costs in the term: the bad debt charge, debt-related administrative costs and associated working capital costs. The largest of these is bad debt – suppliers report these in their accounts through the bad debt charge in the income statement. Eventually, provisions turn into write-offs, although these take some time to crystalise as suppliers try to recover the debt (which can incur further costs). However, suppliers begin to incur costs (eg working capital costs) as soon a customer stops paying.

The cap already includes an allowance for the three debt-related costs, which broadly scales linearly with the overall level of the cap and are therefore, much higher now than prior to the increase in gas prices from September 2021, as a result of increases in the overall cost of energy. Ofgem estimates that for cap period 11b (January – March 2024), debt-related costs will represent approximately 6% of typical dual fuel standard credit bills, 1% of typical dual fuel direct debit bills, and 1% of typical dual fuel pre-payment meter (“PPM”) bills. The overall debt-related cost allowance is split between the unit rate and the standing charge, with the standing charge proportion counting for around a third of the overall allowance in cap period 11b (January – March 2024).

Ofgem has also been working on levelisation between different payment methods. Historically, the cost-to-serve for PPM customers was higher than for those on direct debits, in part because customers bought credit on cards or fobs sold by shops which took commission on such sales. With smart meters, this premium no longer exists and Ofgem is under pressure to harmonise cap levels across the different payment methods. However, as bad debt costs generally apply to direct debit and not PPM customers, this tends to argue against harmonisation.

What is Ofgem proposing in relation to bad debts, and why?

Ofgem says that energy debt has now reached almost £3 billion, despite recent reductions in the price cap and the support provided last year under the Government’s Energy Price Guarantee. Energy debt stood at £2.9 billion in September 2023 – an increase of £0.3 billion since Ofgem’s previous estimate in Q2 2023. Ofgem says it is beginning to observe the conversion of arrears into debt-related costs, and in particular an increase in bad debt in more recent quarters due to wider cost of living pressures and following the end of the Energy Bill Support Scheme in March 2023.

As the cap is intended to reflect the efficient cost of supplying energy to customers, it may be necessary to ensure that these costs are reflected in the cap – this consultation considers whether and to what extent the cap should be adjusted for these additional debt-related costs. On the one hand, increasing the cap level increases the risk of bad debt, but not doing it increases the risks of supplier failure which could result in even bigger cost impacts on bills.

Earlier in the year, Ofgem imposed a moratorium on the forced installation of PPMs. Its analysis of supplier data suggests that this created around £25 million per month of additional debt-related costs between February 2023 and September 2023, and that there is the possibility of larger and uncertain costs over the winter given higher demand. The PPM moratorium represents 19% of bad debt over February 2023– September 2023.

“The scale of this debt means that it is crucial that suppliers have sufficient funding to ensure they can meet the strict regulations Ofgem has in place around how they treat customers facing payment difficulties,”

– Ofgem

Ofgem believes the proposed adjustment to the cap will “ensure suppliers have the resources to support customers struggling with debt” by:

- setting up payment plans

- writing off unmanageable debt on a case-by-case basis

- working out affordable repayment holidays.

Similar provisions are made in other sectors, however, because of the nature of energy regulation, Ofgem can use the cap to ensure these costs are “recovered as fairly and efficiently as possible”. The measure would not apply to those on pre-payment meters as they typically are not part of the customer base responsible for these debts.

Ofgem has analysed the costs suppliers have faced for debt-related costs against the allowances provided through the cap between April 2022 and September 2023 and an estimate for October 2023 to March 2024, and has determined that there is “a material and systematic net under-allowance of costs”.

Any potential options should meet the following initial requirements:

- Customers in debt are adequately protected and treated fairly by suppliers, providing the required level of support;

- Protect all customers by ensuring the fairest allocation of debt costs across different customer groups;

- Suppliers remain incentivised to manage their bad debt costs efficiently whist protecting vulnerable customers;

- The costs of bad debt are shared fairly;

- The price cap reasonably reflects the actions suppliers have to, and should be, taking towards customers in payment difficulty and debt and suppliers are not disincentivised from retaining vulnerable customers who are at risk of falling into debt; and

- The approach is proportionate and practical.

Ofgem remains very concerned about the amount of debt in the system and the risk that it will increase further. It does not think that this adjustment is the answer to the debt problem in isolation, but does believe some higher level of recovery through the cap is necessary. It will review this effect of this temporary adjustment by April 2025.

“We know that cost of living pressure is hitting people hard and this is evident in the increase in energy debt reaching record levels…However, the record level of debt in the system means we must take action to make sure suppliers can recover their reasonable costs, so the market remains resilient, and suppliers are offering consumers support in managing their debts. The proposals set out today are not something we take lightly. However, we feel that they are necessary to address this issue. This approach will ensure the costs are recovered fairly, without penalising a particular group of customers,”

– Tim Jarvis, Director General for Markets, Ofgem

Specifically, the proposals are:

- An adjustment to the cap for additional debt-related costs covering April 2022 to March 2024, and to include the costs of the PPM moratorium;

- That the adjustment is made using a float and true-up approach. Ofgem will set an initial estimate of the additional costs in the April 2024 cap and review whether outturn costs align to the float. Where they do not materially align, Ofgem would consider carrying out an update (true-up) on the initial allowance;

- Ofgem does not anticipate the debt situation to materially improve over the winter, so proposes to roll forward the Q3 2023 net debt-related cost data to set an allowance for October 2023 to March 2024. The adjustment would be recovered over a 12-month period but not uprated for inflation;

- Ofgem does not propose to pursue a levy mechanism for its April 2024 implementation but will leave the option open for further consideration in the context of levelisation.

In a previous consultation in October, Ofgem set out the case for a debt adjustment, including several options for such an adjustment, including setting an initial estimate and truing up the estimate later (float and true-up approach), setting an allowance now with no true-up, and delaying the adjustment to set it on an ex-post basis. Ofgem also considered a alternative mechanisms such as a levy to mutualise debt-related costs, treatment of PPM moratorium costs and whether to uplift any allowance for inflation.

It received nine responses from suppliers, twelve from consumer groups and charities and two from industry bodies. Generally, suppliers and industry bodies supported an adjustment and consumer groups and charities were against. Consumer groups and charities generally opposed increasing costs to consumers and the inclusion of PPM moratorium costs within the adjustment. Ofgem received 243 responses from individuals, most of whom aligned with the consumer groups with some saying that an adjustment to the allowance would prioritise the interests of suppliers over consumers. Ofgem also received a petition which had approximately 80,000 signatories asking Ofgem not to increase bills, saying that the government should pay for energy debt.

Supplier profits have risen as a result of previous Ofgem interventions

Energy supplier profits have, for a change, been higher this year after Ofgem increased the price cap to allow them to recover wholesale energy costs incurred when they had to buy additional energy for customers taken on through the Supplier of Last Resort process. British Gas reported record profits of £969 million for the first six months of 2023, up almost 900% from £98m in the same period of 2022. EDF reported its UK business made profits of almost £2 billion for the first half of last year (including earnings from its nuclear division) up from £738 million in H1 2022. Scottish Power reported a £576 million profit for the H1 2023, E.On made £723 million, and SSE reported pre-tax profits of £565.2 million.

Predictably, this is causing outrage among customer advocacy groups who oppose supplier profits when consumers are struggling with high energy costs.

“This outrageous tax on energy consumers is simply not fair. Energy suppliers have posted billions in profits already this year while millions of people struggle in cold damp homes. The record levels of energy debt are due to Britain’s broken energy system, not the fault of the hard-pressed public,”

– Simon Francis, coordinator of the group End Fuel Poverty Coalition

However, some do recognise that it is for the government and not suppliers to manage this, since rising wholesale prices are outside their control. They also point out that a high cost environment risks creating a negative cycle where bad debts increase, causing prices to rise, making them unaffordable for more people, leading to more bad debts.

“Energy bills continue to spiral and now the amount householders owe has reached record levels – almost £3 billion. Sadly, this is no surprise, with the chancellor failing to protect low-income households from high energy bills in his Autumn Statement. Ofgem’s response, to increase prices further, may well be necessary. But it will only serve to increase debts and does not address the underlying issues. There is now a desperate need for the UK Government to step in and to help low-income households clear their debts and make sure bills are affordable. People are already going without energy, heat and light and it’s not enough to stop their debt rising. It’s going to be a bleak and cold Christmas for millions,”

– Matt Copeland, head of policy and public affairs, National Energy Action

The point about vicious circles is a good one. Prior to this year, supplier margins were thin or negative, meaning they had little ability with survive large levels of payment delinquency. Some firms such as Centrica and EDF benefit from having diversified business models – when the supply market does poorly they often make up the difference with higher income from production (gas in the case of Centrica and electricity for EDF) but that has become rare in a sector which in the past few years has “un-integrated” through various divestments and business re-organisations.

Tinkering with the price cap is a further sign it is unfit for purpose

Consumers are struggling with high costs, and suppliers have struggled with a structurally low margin environment. Consumer groups want to ease the burdens on consumers, but this cannot realistically be done at the expense of suppliers, and although they point out that many of Ofgem’s interventions in the past year have been to the benefit of suppliers, this reflects a correction to a regulatory environment that had been too hostile to suppliers. Part of the reason that so many suppliers failed was anti-supplier regulation, and the heavy-handed way in which the price cap was implemented. Ofgem tried to play politics by showing itself to be “tough” on suppliers, and perpetuating the accusations that suppliers were taking advantage of their customers. This led to high levels of supplier failures which imposed significant additional costs onto consumers.

Ultimately energy is not, and should not be free. Energy suppliers, like any other providers of goods or services, are entitled to get paid for the energy they sell, and to make a decent profit. As I have said previously, there is no pressure applied to supermarkets to give food away, nor are they criticised if their security guards prevent shoppers from stealing. Yet somehow people do think it’s wrong for suppliers to require customers who fail to pay to have a pre-payment meter. This double standard is unfair.

Suppliers are not responsible for either the high cost of energy or the wider cost of living crisis. The solution to this challenge lies with the Government and only the Government. The price cap must be abolished, and we need to stop thinking supplier profits are wrong. Struggling consumers should be supported either through increased benefits, tax cuts or a social tariff, all of which are within the purview of the government and not the regulator or individual suppliers, whose hardship funds, while well meaning, are inadequate given the wider low margin environment.

“The price cap has helped to protect consumers from a volatile gas market. However, it remains a blunt instrument in a changing energy sector, and the way it works may need to change in the future, so customers continue to be protected,”

– Tim Jarvis, Director General for Markets, Ofgem

Ofgem is repeating its calls for reform of the price cap, arguing that it isn’t delivering the best outcomes for consumers. Really the cap needs to be abolished. It fails to deliver on just about all of its objectives, and worse, its existence misleads consumers into believing that energy should be cheap and that suppliers will cheat them unless they are heavily policed (which undermines competition since consumers are entitled to prefer the “devil they know”).

An additional £16 over one year is not realistically going to make the difference between affording energy bills and not, and not applying this increase is not going to make bills any more affordable for many households. But it is yet another round of tinkering which demonstrates the impossibility of setting and maintaining an effective price cap. I don’t blame Ofgem for wanting change – the whole exercise is a huge waste of time and resources. But I have little confidence that a government facing election defeat in the next year will make such a contentious change. The price cap is unlikely to go anywhere for the foreseeable future.

The problem is not just the Price Cap. And it’s not just the recent rise in gas prices – gas is still cheaper than electricity. The bigger issue is Net Zero. In our rush towards the fantasy of Net Zero many households are struggling to pay for the rising costs of weather and light dependent energy, and associated batteries. This is hardly surprising because these renewables require a parallel system of traditional thermal power stations to be fuelled and maintained to support the minute to minute fluctuations in renewable power and the long durations when renewables deliver no power. At the same time as paying for these two parallel systems we will also have to keep paying for the replacement of the massive amounts of new infrastructure required to capture the very dilute and diffuse energy that the sun and wind provide, as the working life of wind turbines and solar panels is roughly less than half that of thermal power stations. So Ofgem is now saying that the shrinking pool of people who can still afford their household energy bills will have to pay more to cover the bad debts of the growing number of people who can’t. That doesn’t seem very sustainable to me, but it’s where our dysfunctional energy policies have got us. The only way around this is to replace old power stations and intermittent renewables with nuclear power stations.

I tend to agree. The problem is that policy-makers still think renewables are cheap despite all the evidence to the contrary. I challenged Claire Courtinho to include ALL costs to the consumer down to de-commissioning costs for all technologies when updating the LCOE. They need to compare like for like costs to understand which give the best and worst value.

Hi all….so much activity on this lively blog selecting a particular posting to reply to is not straight forward. However I’m drawn to the closing sentence of IMO an excellent contribution by mairede thomas & Kathryn’s follow up comment.

The decommissioning of nuclear sites is well under way with more to follow within a few years leaving behind major infrastructure & access to the national 400kv supergrid network. Surely such sites could be repurposed for new build big nuclear power plants. I’m with Kathryn favouring ABWR reactors rather than the EPR designs currently under construction. Upgrading to the existing 400kv supergrid network is well under way. Nothing new here, similar to the 1950/60’s emergency uprating of the 132kv grid to 400kv involving large area’s of 275kv interim stage’s; a major task, achieved in record time.

I’m aware that big nuclear’s lack flexibility of output, designed to supply base load demand. I would argue that things have moved on with more load balancing options like pumped-storage & increased connections to mainland europe etc. Norway many non pumped reservoir’s a particular point of interest.

Obviously there will be consequences to any solution to the UK current energy policy mess. My take on this is balancing the output from big nuclear plants using pumped-storage etc. is a better option than coping with intermittent supplies from renewables.

Not wishing to ignore the excellent R/R initiative re SMR’s there are likely to be some opportunities I’m sure in the UK but would suggest a global market the major way forward.

Finally; The Koreans build conventional coal fired power station’s on time, on budget yet never achieve similar with nuclear power stations WHY!

Jack Devanney, Gorden Knot Group.

Barry Wright, Lancashire.

IIRC the retail industry os sitting on some £8bn of customer credit balances extracted via DD and PPM. In the higher interest rate environment we now have that is a large benefit to retailers and cost to consumers, and is an offset against the bad debt. The origin of the increase in bad debt is bad energy policy dictated by government, so it bears the responsibility for it.

A combination of the way the law works and the actions in pursuit of bad debt mean that the process is very costly. Charges for securing a warrant and dispatching bailiffs and commissions on debt recovery can multiply an outstanding debt substantially, putting the already poor customer into extreme poverty if they have to pay all the costs to clear their debt, and adding to the bill for debts written off. It would be useful to examine whether a cheaper and more effective scheme and process could not be devised. Clearly there is a need for a social tariff, or a tariff that offers a tier of low cost supply.

The moves towards loading all fixed charges onto customer bills and substantially increasing standing charges have been unhelpful. I called for that to be reversed back in summer 2021 when it became evident that we were headed into a high cost crisis. It also fails to provide the right incentives on the expansion and location of renewables if they don’t see the associated grid and balancing costs: it distorts proper market competition where it is already distorted by subsidies.

I know we agree that the financial aspects of the supplier/customer relationship should really be regulated by the FCA and not OFGEM. Indeed, the government is in a regulatory mess since it decided to make OFGEM responsible for net zero. That is a clear clash with consumer interest. Consumers need their own, dedicated champion to fight against government excess. I’ve a feeling that will have to come via politics replacing the Uniparty., rather than reform within government. With the prospect of Ed “Mr Cap” Miliband returning to policy control, it seems unlikely that this particular mill Ed stone will disappear otherwise.

One of Ofgem’s biggest failures was not pushing back on the price cap. It said “oh yes, we can run it”. Now it’s seen how running it means non-stop adjustments it wants to get rid. Ofgem spends too much time trying to show the Government it’s on side and not enough time challenging it…Ofgem answers to Parliament not the Government, but because Parliament rarely organises itself to hold regulators to account, it’s oversight is patchy.

Why should people that pay for there Energy have to pay for people for people that can’t or won’t.

Exactly! This is why supporting the vulnerable should be funded through taxation and not bills.

Hi…excellent reply comment.

The closing sentence most insightful.

In the UK we were there, way back in the 1970’s under the nationalised Central Electricity Generating Board (CEGB).

The Wylfa Magnox nuclear power station, commissioned 1971, shut down 2015, 44 years operational.

Feeding into the 400kv supergrid national network & including the suburb Dinorwig pumped-storage hydro. facility, the latter commissioned 1984, still operating today (24/7/365). Here IMO was the perfect model worthy of expansion, carbon free energy throughout the UK, big nuclear plants plus pumped-storage hydro. balancing. Shame that all the existing infrastructure & that all important licence for new build at the Wylfa site seems so out of favour in this case. I question why the North Wales model all those years ago could not have been expanded under a nationalised nuclear energy industry. Big nuclear plants on the coast, with essential access to abundant seawater for cooling. Uninterrupted continuous electrical output feeding into a robust national supergrid network. Flexibility provided by pumped-storage hydro.

I make no apology for this arms length approach (always vulnerable to deep science) to a huge national & global problem but feel the UK was well on the way all those years ago…….Solar, wind, batteries no contest IMO……Barry Wright, Lancashire.

The unacceptable other side of the coin

https://www.dailymail.co.uk/news/article-12878671/Terrified-EDF-customers-claim-sudden-increases-monthly-bills-ruined-holidays-left-unable-remortgage-homes-scared-heating-on.html

‘Consumers are struggling with high costs’.

Reading this highly informative article we can see very clearly:

1. Ofgem is a complete failure.

2. The cap is a case of the Public Sector talking to itself and expecting everyone else to pay regardless.

3. The economics joins much of the Public Sector in that it is criminal. If I ran a company like this, it would be called fraud.

4. The author points out this feeds distrust. Ofgem – a corporate paper weight with no point at all.