While working on my new training offering, I have been reading about the very earliest days of electricity and reflecting on how some of the early trends of local electricity markets and de-centralisation are experiencing a renaissance.

The 19th century saw a great many important discoveries and inventions, notably by Thomas Edison and his one-time colleague and later rival, Nikola Tesla. Edison favoured direct current, while Tesla (and his colleague George Westinghouse) preferred alternating current since at the time it allowed electricity to be transported over longer distances.

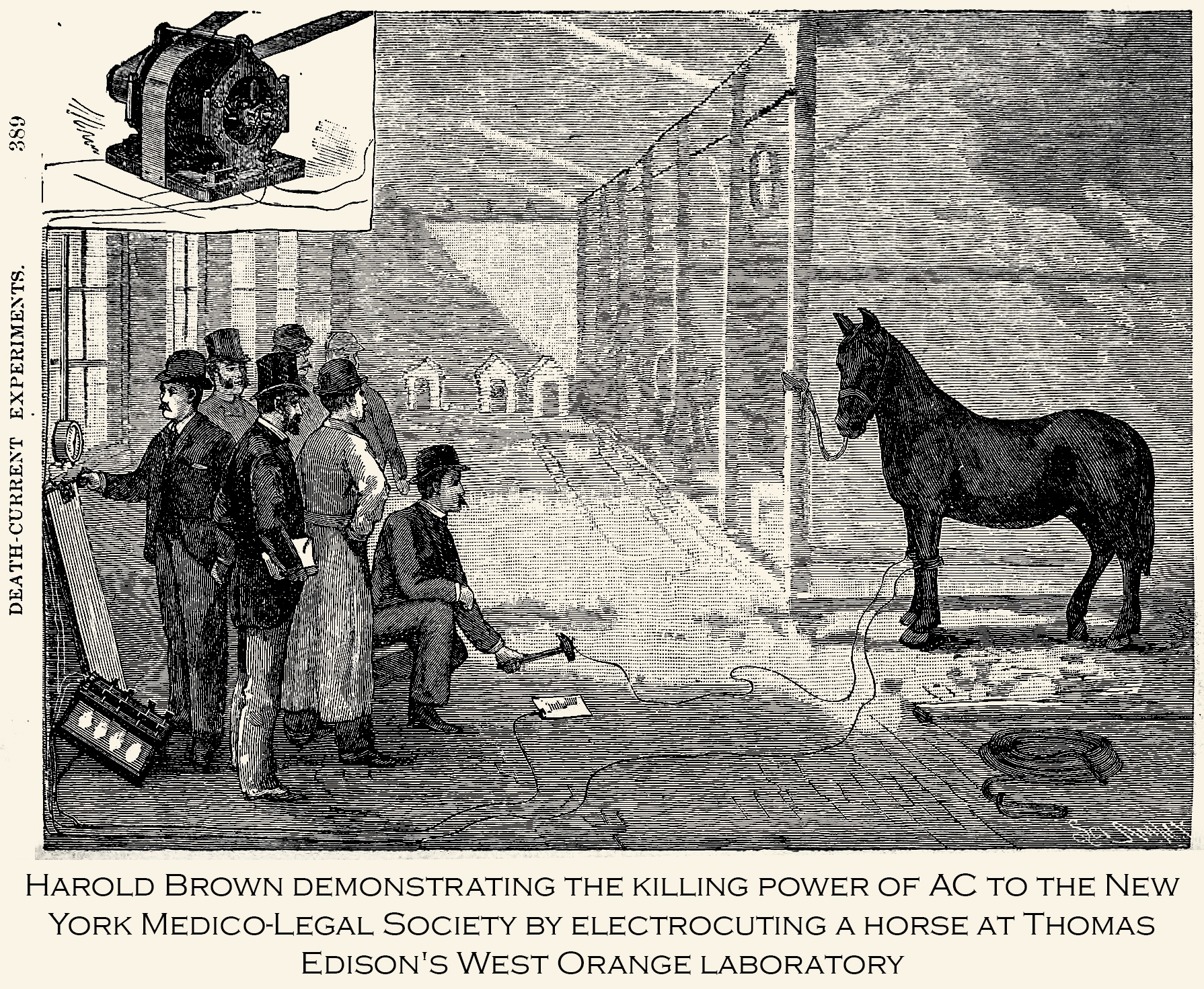

This rivalry came to be known as the “Battle of the Currents” and involved all sorts of dirty tricks, mostly on the part of the dc camp. Edison claimed that the high voltages used to transport alternating current were hazardous, stoking up public outrage over fatalities linked to pole-mounted high-voltage ac lines, which were dangerous due to their un-regulated and unsafe deployment.

This rivalry came to be known as the “Battle of the Currents” and involved all sorts of dirty tricks, mostly on the part of the dc camp. Edison claimed that the high voltages used to transport alternating current were hazardous, stoking up public outrage over fatalities linked to pole-mounted high-voltage ac lines, which were dangerous due to their un-regulated and unsafe deployment.

In 1888, Harold P. Brown, a New York electrical engineer, tried to prove that ac was inherently more dangerous than dc by publicly killing animals with both currents, with technical assistance from Edison. Edison and his gang also contracted with Westinghouse’s main ac rival, the Thomson-Houston Electric Company, to make sure the first electric chair was powered by a Westinghouse ac generator, to further persuade the public of the dangers of as current! But by 1893 the battle was all over when the organisers of the World Fair in Chicago chose ac to power the exhibition.

Local to national and back to local again

From there things developed slowly – in 1920 just 6% of British homes had electricity, and those that did had widely varying services – in London alone there were 24 voltages and 10 different frequencies. In 1921, there were more than 480 authorised suppliers of electricity operating in the UK, generating and supplying electricity at a variety of voltages and frequencies.

Of course, this highly fragmented local approach was highly inefficient. Electricity was more expensive than in other countries which had taken a more standardised and centralised approach, and it was inconvenient for consumers to have to get their appliances and electrical items adapted for a new system when they moved house.

The Electricity Act of 1926 created a central authority to promote a national transmission system, initially with regional grids, which were kept separate until the eve of the World War II. In late 1938, and with some trepidation, the inter-regional isolating switches were closed and the regional grids were all connected to each other for the first time. As nothing untoward happened a decision was made in spring 1939 to keep them closed, except in the case of an emergency, and so the national transmission system was finally realised.

After the war, there was a general political consensus that certain industries including electricity were so important to the national interest they should be under state control, and so the entire electricity market from generators to suppliers, was nationalised. In fact, the newly created nationalised companies were made statutory monopolies making competition effectively illegal.

After the Electricity Act of 1957 passed, the nationalised market was established and continued until the Thatcher government of the 1980s. By this time, the market was characterised by over-capacity and poor cost-control, and the power cuts and brown-outs caused by strike action in the late 1970s had undermined confidence in the model to deliver security of supply. A decision was made to privatise many of the industries that were nationalised after the War, and also to un-bundle the electricity sector, separating different parts of the value chain into difference companies, formalised in the Electricity Act 1989.

This process took around a decade to complete, and it wasn’t until the Utilities Act 2020 that the final part – the separation of supply and distribution – took place, and the market structure with which we are familiar today emerged.

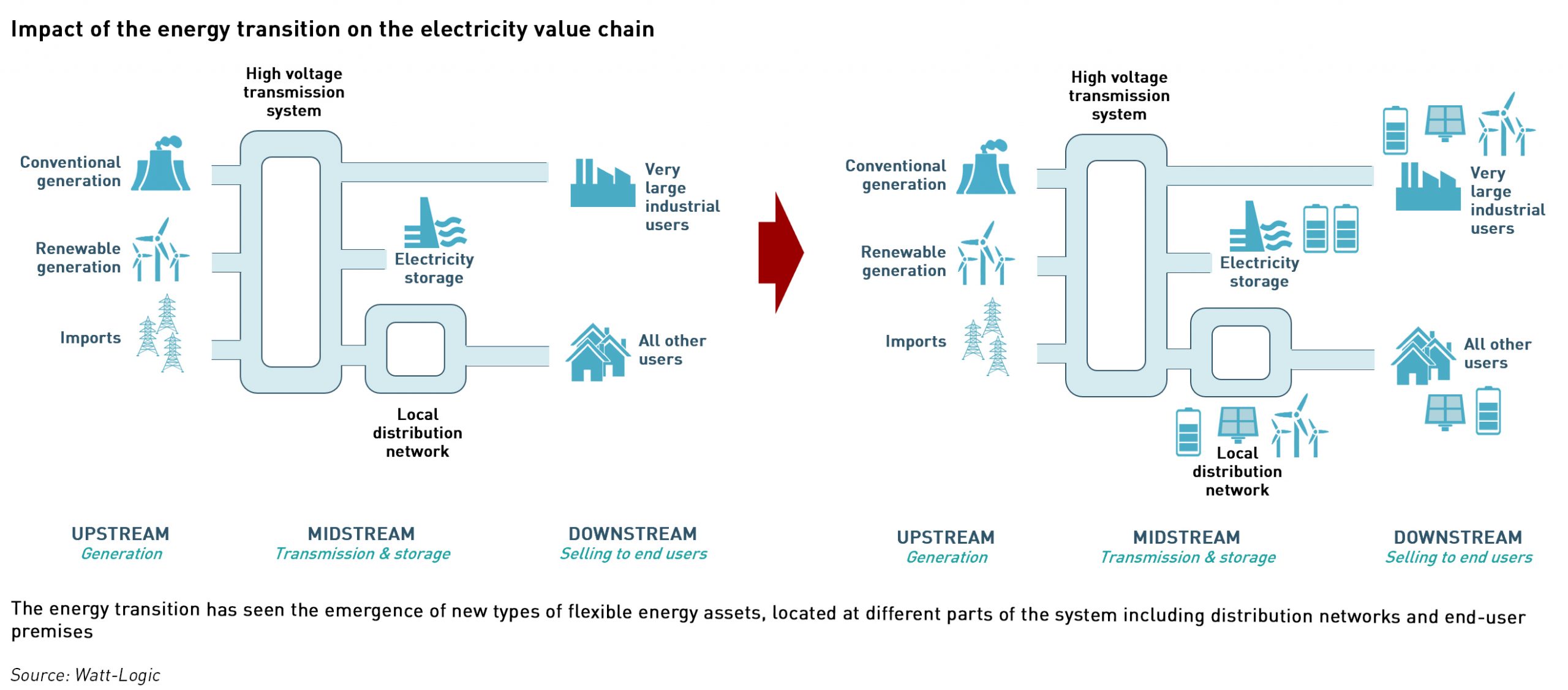

Now we have around 60 suppliers operating in Great Britain, over 450 licenced generators, and generation no longer has the centralised structure it had during the second half of the 20th century, with small-scale generation embedded in local distribution networks, and micro-generation in homes and businesses. Community schemes are politically popular if not yet making a significant contribution, and people speak approvingly of local electricity markets featuring peer-to-peer trading.

I attended a digital conference last week where one speaker commented that he thought the balance of supply and demand was determined at the local level and should be solved locally. We have also seen in the last few weeks, the decision by National Grid to purchase Western Power Distribution, the largest of Britain’s Distribution Network Operators, a move which will likely see it forced to divest fully its arm’s length transmission system operation business, NG ESO. This would effectively mean swapping a national business for a regional one.

There is even an interesting postscript to the Battle of the Currents. High Voltage DC cables are now capable of transmitting dc current over large distances, and most forms of renewable generation produce direct current which is converted to alternating current for export to the grid, while maintaining voltage stability on the transmission system is an increasingly difficult and expensive task. There may come a time when maintaining an ac system is no longer optimal, although the extensive legacy infrastructure would be a barrier to any significant change.

What about local electricity pricing?

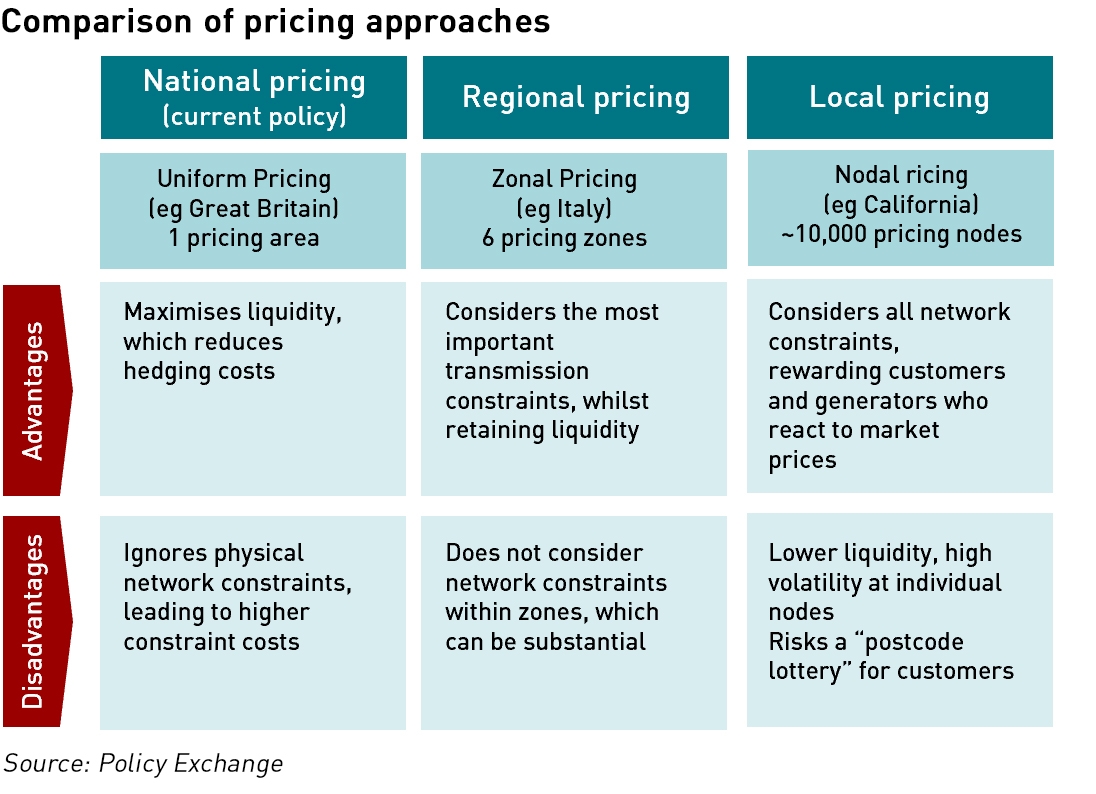

There are already calls for other major change. Recently the Policy Exchange called for the introduction of local rather than national electricity pricing, replacing the current national wholesale electricity price.

“[Local electricity pricing] would encourage electric car drivers in Cornwall to charge their vehicle when it’s sunny and those in Aberdeenshire to charge when it’s windy, reflecting local sources of electricity. Local pricing would also encourage energy intensive industries to build factories and data centres in the UK’s coastal industrial hubs, where they can benefit from the UK’s abundant offshore wind resources,”

– Ed Birkett, Policy Exchange

But the question of whether local is better than national in the electricity market is an interesting one, and I’m inclined to disagree with the speaker last week, and with the Policy Exchange’s recommendation. Although there are a great many local generators, they are small, and contribute a relatively little to overall demand needs. Bulk generation from large offshore windfarms, nuclear and traditional thermal plant still dominate, so while local dynamics are important for managing local grids, few local areas (and the speaker in question was from a large city), could manage their own needs without recourse to bulk generation supplied over the transmission system.

The idea of local pricing to encourage efficient use of resources and minimise network congestion is superficially appealing, but risks exacerbating social inequalities. Should drivers in Cornwall suffer when it’s not sunny and electricity needs to be imported into the county? Would rural dwellers find supplies more expensive and less robust mirroring their current experience with broadband connectivity?

Policy Exchange believes that lower local electricity pricing will incentivise manufacturing to move to areas where power is cheap, building local industrial clusters. This might work, but, electricity pricing alone may not be significant enough to drive the decision to re-locate. It could also carry significant risks. Wholesale electricity prices are increasingly volatile – local prices, with fewer market participants, would be likely to see both higher price volatility and lower liquidity.

And how would large industrial users respond to fluctuations in supply? If market pricing is local, depending on local supply and demand, and that supply is reliant on intermittent generation, unless consumers are able to flex their demand, they would have to pay much higher prices in periods of low generation output. Not all heavy industry has such operational flexibility, particularly when periods of low wind can last for days and even weeks. National electricity prices can be hedged, but its doubtful there would there be enough liquidity in local markets to support hedging for large users.

And then there are the energy costs of moving those facilities in the first place…buildings have embodied emissions, so moving facilities purely to be located close to renewable generation may not result in a net environmental benefit.

One of the key arguments made by Policy Exchange in support of local pricing is that it would take full account of transmission constraints. While these are ignored in wholesale electricity prices, they are not ignored in the end price paid by consumers. There is no reason that every price signal that is needed or desired in the market must be contained within the wholesale price, and there are good reasons for maximising liquidity, particularly given the fact that liquidity constraints present a significant challenge to many smaller market participants trying to hedge their shape exposure.

Another argument is that under a local electricity pricing model, demand and supply would align – demand would be more flexible and supply would locate close to demand. This is based on the findings of research it commissioned from Aurora Energy Research, but there is little recognition of other key factors. For example, the report cites floating windfarms serving the southern pricing regions, but there is no discussion on feasibility…where would these be located given the south coast borders one of the busies shipping lanes in the world?

While I am sympathetic to arguments that current locational price signals may be too weak, I am far from convinced that local wholesale pricing is the solution – it may create more problems than it solves.

What is the role of competition?

Another interesting recommendation in the report was to increase the role of competition, reducing the role of the Government and Ofgem. This is in fact contrary to the recent trend of increasing barriers to entry for suppliers due to the escalating numbers of supplier failures. So how much competition should there be in the energy market? The free-market reforms of the 1980s onwards assumed there should be no limits to competition, and the concern was more around market concentration leading to market power and potential market abuse.

But there are four factors in that set the electricity market aside from other markets:

- Electricity cannot be easily stored, meaning supply and demand must be balanced in real time;

- Some types of electricity infrastructure investment require so much capital that they need state support;

- Some of the costs of failure in the electricity market are socialised rather than being solely borne by the failed party’s shareholders (and sometimes creditors); and,

- The consequences of failing to match supply and demand are such that security of supply must be maintained in a way that is not the case in other markets.

Currently, no organisation has overall responsibility for maintaining security of supply in the GB market. National Grid ESO is required to maintain reserves, known as the SQSS (the Security and Quality of Supply Standard), but these are designed to ensure sufficient reserves are in place to cover the single largest infeed loss, which may be insufficient, for example if the event which interrupts the single largest infeed (generator or interconnector) may also interrupt other generation, as happened during the 2019 blackout.

In the same way that regulation was originally introduced to ensure safety and standardisation, there are clear limits to the extent to which de-regulation would be possible, and it is important that the Government and Ofgem step in when the market is unable to deliver desired objectives. Historically these have been secure and affordable supplies, and more recently environmental standards have also been introduced.

This means that electricity markets require a level of direction that is not needed in other markets. Competition is important and a useful means of incentivising new technologies to respond to the changing needs of the market, but there are clear limits to what competition can achieve in the electricity industry. To be fair, Policy Exchange was arguing for competition to be the means of determining the mix of installed generation capacity, which at the moment is heavily influenced by Government policy.

But for this to be effective, the rules of the market would need to be carefully designed, and experience to date does not inspire confidence. For example, capacity auctions were introduced as part of the Electricity Market Reforms (“EMR”) surrounding the de-carbonisation agenda, and yet the most successful technologies have been small diesel engines and open-cycle gas plant, which are at the dirtier end of the generation spectrum.

“History may not repeat iself. But it rhymes,”

– James Eayres

Even in the past few days there have been calls for more localism with MP Philip Dunne, chairman of the Environmental Audit Committee suggesting that local communities should be able to use community-generated electricity themselves without having to get a grid connection and export to the grid. This sounds eminently sensible, but the free-for-all of the early 20th century cannot be repeated. If a local generator is to supply the local community without connecting to the grid, it still needs to supply electricity at 230 volts and 50 Hz, and there need to be billing arrangements to make sure consumers only pay for what they use, and arrangements to ensure they can still receive power from the grid when needed (otherwise local generators would have to take on security of supply responsibilities as well).

I’m instinctively a free-marketeer, and prefer high-level, principles-based regulation where possible, but I firmly believe that the electricity markets require a more regulated and more directed approach. I would go as far as to say that I would prefer for the Government to step in and directly support some new generation (specifically Advanced Boiling Water Reactors) because I worry about a capacity crunch as coal exists and old nuclear plant see declining reliability and availability. Of course, there are limits, and a return to the over-capacity of the CEGB days is undesirable, but not all central planning is bad.

Despite recent trends to increase competition and greater localism, the electricity system is still strongly national in its composition, and, while local networks may be more dynamic than in the past, the system is fundamentally a national nature and likely to remain so over any meaningful forward-looking time horizon.

Interesting post. I think local microgrids within a national grid probably wouldn’t work. It would be interesting mechanistically to find out how a competitive market between local microgrids and a national grid might actually operate. However, I can’t think of a way that a microgrid would win-out over a larger national grid. It’s not like they can offer a higher quality product, because one KWh of electric is all the same quality, so the economies of scale are going to hurt them when it comes to costs.

Thanks for sharing this great overview of electricity markets. I found your points on local vs. national systems really interesting.

I appreciate you sharing this informative summary of electricity markets. Your insights on the differences between local and national systems caught my attention.

This post is literally worth reading.

Thank you for providing such a comprehensive overview of electricity markets. I particularly appreciated your insights into the differences between local and national systems.