Against the backdrop of the current energy crisis comes the news that the Government is looking at new proposals for a nuclear reactor at Wylfa Newydd. The original proposal was for an Advanced Boiling Water Reactor (“ABWR”), but after developer Hitachi failed to agree a financing arrangement with the Government it withdrew its proposal. Now there are two alternatives on the table using different technologies.

Another roll of the dice for the Westinghouse AP1000…

Bechtel wants to build two Westinghouse AP1000 reactors and is seeking an alternative approach to funding with an initial two-year plan to deliver the front-end engineering design with government funding which could then “create the conditions” to attract potential investors and a developer. This could be achieved by modifying the proposed RAB funding model or through some other mechanism of cost recovery.

“It is a complex build but where the risk comes is not in the engineering. It comes in the supply chain, materials, labour costs and productivity. The government can help by providing certainty of upcoming projects. If the supply chain knows what’s coming there is improved pricing,”

– Barbara Rusinko, president of nuclear, security & environment at Bechtel

The idea is that a project that has state support through the early stages is more likely to succeed given the large capital investment requirement needed before any returns would be seen. The capital costs of new nuclear projects have risen to an extent that they are too large for private investors to absorb without some form of state backing. Bechtel hopes that its funding model would provide a viable alternative to the previous developer-led approach to nuclear projects.

The proposal would be modelled on Plant Vogtle in Georgia, where two AP1000s are set to begin operating in 2022. The AP1000 design received Government approval in March 2017 for the proposed plant at Moorside near Sellafield in Cumbria. The project had an indicative commissioning date of 2025 at the time, but was cancelled by developer Toshiba in 2018. Toshiba’s subsidiary, Westinghouse, filed for Chapter 11 bankruptcy protection in 2017 following major cost over-runs at a number of its nuclear projects. In mid-2018, Westinghouse was bought by asset management company Brookfield, and the subsequent restructuring allowed the company to exit Chapter 11.

The Vogtle reactors are expected to begin commercial operation in 2022-23, after significant delays and cost over-runs – a history shared with the similarly troubled European Pressurised Water reactor (“EPR”) technology. The two Vogtle units were supposed to open in 2016 and 2017, and have seen their costs rise from US$ 14 billion to a potential final price of US$ 27 billion. Consumers in Georgia pay an additional 11% on their energy bills to fund the site.

….or the first roll for small modular reactors

Shearwater Energy has made an alternative proposal that would involve using both the Wylfa Newydd site and the nearby site of the existing Wylfa Magnox site which is being de-commissioned. The scheme would have 12 small modular reactors (“SMRs”) with an initial capacity of 924 MW alongside a 1,000 MW wind farm. The plant would produce three million kilograms of hydrogen for use in the transport sector.

Shearwater Energy has made an alternative proposal that would involve using both the Wylfa Newydd site and the nearby site of the existing Wylfa Magnox site which is being de-commissioned. The scheme would have 12 small modular reactors (“SMRs”) with an initial capacity of 924 MW alongside a 1,000 MW wind farm. The plant would produce three million kilograms of hydrogen for use in the transport sector.

The company has signed a memorandum of understanding with US SMR developer NuScale, which last year became the first company to win approval for its small reactors from US nuclear regulators. Once fully developed, the company expects the scheme to have a capacity of 3 GW.

NuScale expects to have its first power plant up and running by the end of this decade, in Idaho, USA. The first NuScale Power Module is planned to begin generating electricity in 2029, with the remaining modules coming online for full plant operation by 2030. The company has secured US$ 200 million of investments this year to support its plans.

Meanwhile EDF continues to push its troubled EPR technology

After Toshiba pulled out of the proposed AP1000 project at Moorside, it wound up its subsidiary, NuGeneration, which was to be operator of the project, and the site was abandoned. Since then a group consisting of 15 major companies including EDF, has put forward plans for a Clean Energy Hub at the site. Also in the group are Altrad, Atkins, Balfour Beatty Bailey, Bilfinger, Cavendish Nuclear, Doosan Babcock, GMB, Jacobs, Laing O’Rourke, Mott MacDonald, Mace, Prospect, Quod, Unite the union, and economic development specialist John Fyfe. They plan to develop two EPRs – the same technology as at Hinkley Point C – as well as potentially hosting small modular reactors (“SMRs”) on the site.

A new challenge to the EPR revolves around EDF’s partnership with China General Nuclear Power (“CGN”) which has a 20% stake in the Sizewell C project, another proposed EPR. UK-Sino relations have deteriorated in recent years, and there are increasing concerns about the involvement of Chinese companies in strategic infrastructure in the UK, which may impact the future of the project. This weekend The Guardian newspaper has reported that Government could announce plans to take a stake in Sizewell C as early as next month, ahead of Cop26.

EDF’s board is due to meet in November to discuss the project, but according to The Guardian, it is wary of investing tens of millions into the project without a firm commitment from the Government. In the meantime it is understood that the US Government is pressuring the UK to extract the Chinese from British nuclear infrastructure. EDF’s main board only just approved Hinkley Point C by 10 votes to 7, with one board member resigning ahead of the vote saying the project was financially risky and would lead France further away from renewable energy. There are other reports suggesting that EDF intends to delay its internal decisions on Sizewell C as a result of the concerns over Chinese involvement.

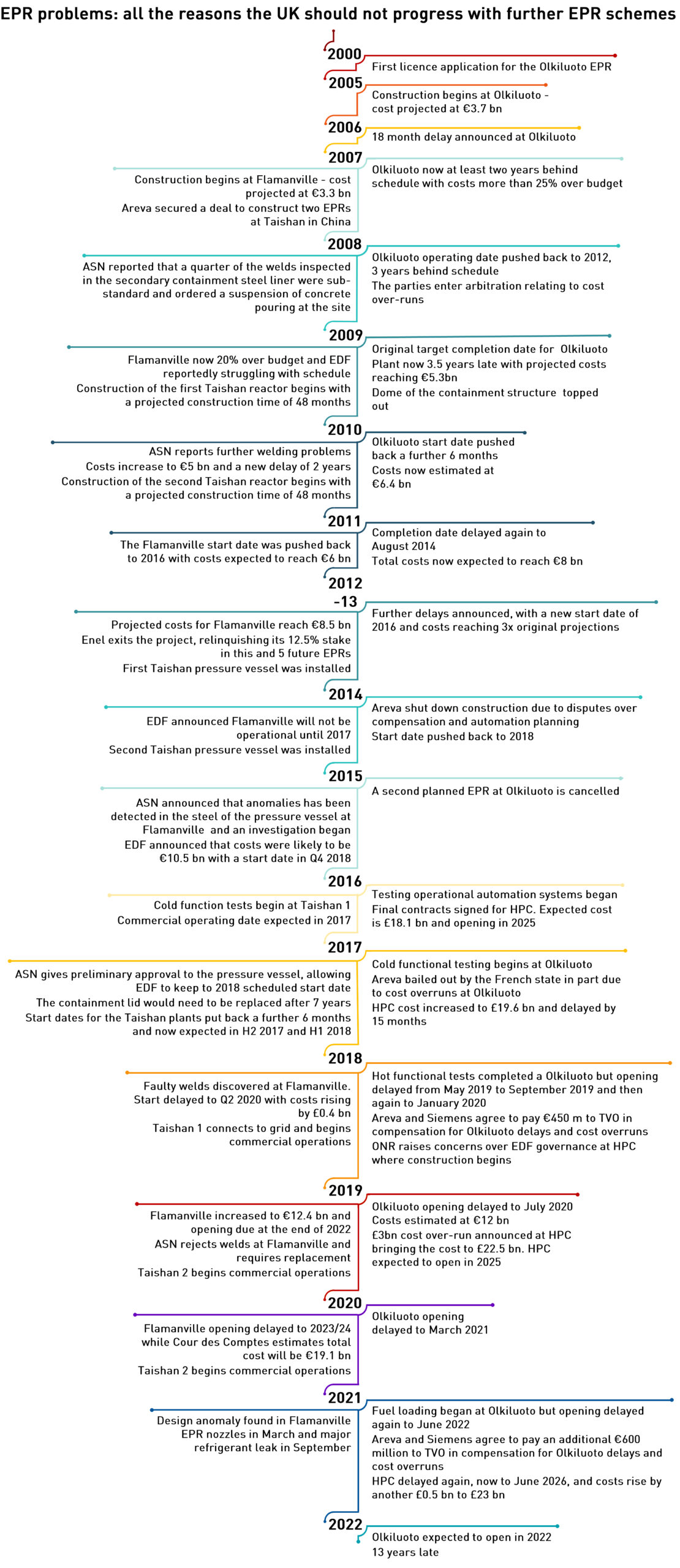

I sincerely hope that these rumours about a Government stake in Sizewell C are unsubstantiated. Until such time as EDF manages to deliver a working EPR in Europe the Government would be foolish to commit taxpayer money to the technology. At least at Hinkley Point C the burden on taxpayers comes through a generous Contract for Difference but that only applies once the station is running. The timeline beneath this post illutrates the sorry history of the EPR project and should give pause to anyone considering putting money into the failing technology.

Excitement is building around nuclear fusion

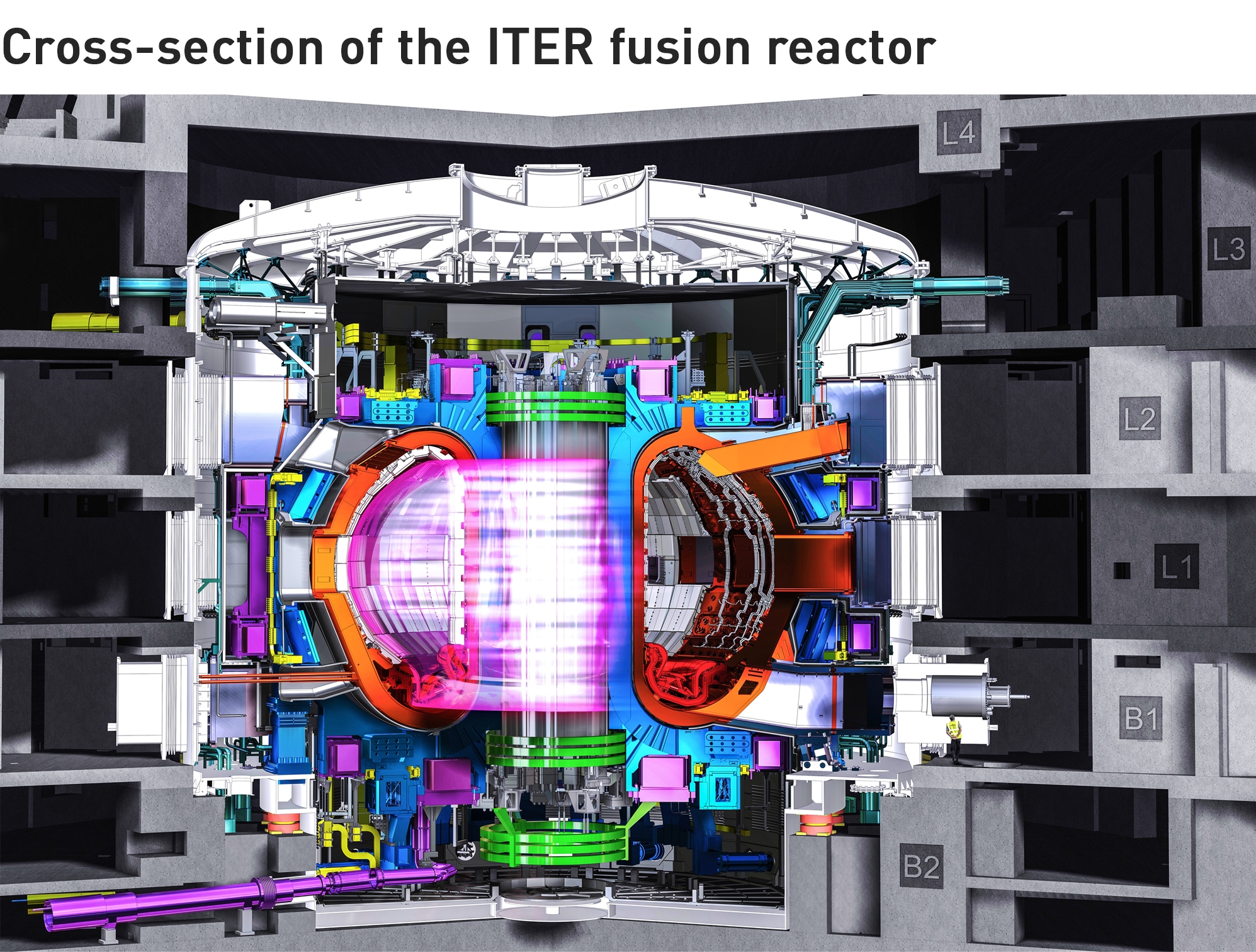

The Moorside site has also been put forward to host the first prototype spherical fusion reactor, known as the Spherical Tokamak for Energy Production, or “STEP”, which is slated for 2024. It is one of a number of sites hoping to make the final shortlist which is expected to be produced in the autumn. The UK Atomic Energy Authority will then make recommendations to the Secretary of State for Business, Energy and Industrial Strategy, who will make a final decision on the site by the end of 2022.

This week I attended a presentation given by Ian Chapman, the Chief Executive of the UK Atomic Energy Authority who spoke enthusiastically about the prospects for nuclear fusion. He described the challenges to achieving an efficient fusion reaction that generates more power than it consumes and stated, quite compellingly, that a fusion-power power station could be a reality in 20 years (although fusion in 20 years has been promised for decades!).

The next milestone for fusion will be the completion of the ITER project in France, which he described as 80% complete. The aim of the project is to generate 500 MW of output energy for 50 MW of input energy (this is not electricity – turning the output energy into electricity will be the objective of the STEP project).

However, looking at the ITER website a couple of things jumped out…the 50 MW is referred to as “input heating power”, but the site itself will have an electrical load of 110 MW to up to 620 MW.

I reached out to Chapman for clarification, and he confirmed that the objective of ITER is to demonstrate a thermal gain of ten times, but that the site will have a parasitic load of 600-700 MW. In order to be a viable source of electricity, the technology will need to be developed further to yield even higher thermal gains.

He told me that they would expect a reactor with a similar parasitic load to have a heat output of 2 – 2.5 GW to produce 0.5 – 1.0 GW of electrical output. The STEP prototype will aim for a thermal gain of around 1 GW to produce a few hundred MW of electricity, with subsequent commercial units likely to go up in thermal power.

A 700 MW parasitic load is the output of a medium-sized power station, so it would make sense to co-locate a fusion reactor with SMRs as a means of having a guaranteed, stable and reliable source of input power.

Nuclear is critical for Britain’s security of supply

If Britain is to achieve its net zero ambitions, it will need a reliable source of zero carbon electricity that is not dependent on the vagaries of the weather – nuclear power. But the existing fleet is aging and closure dates are looming.

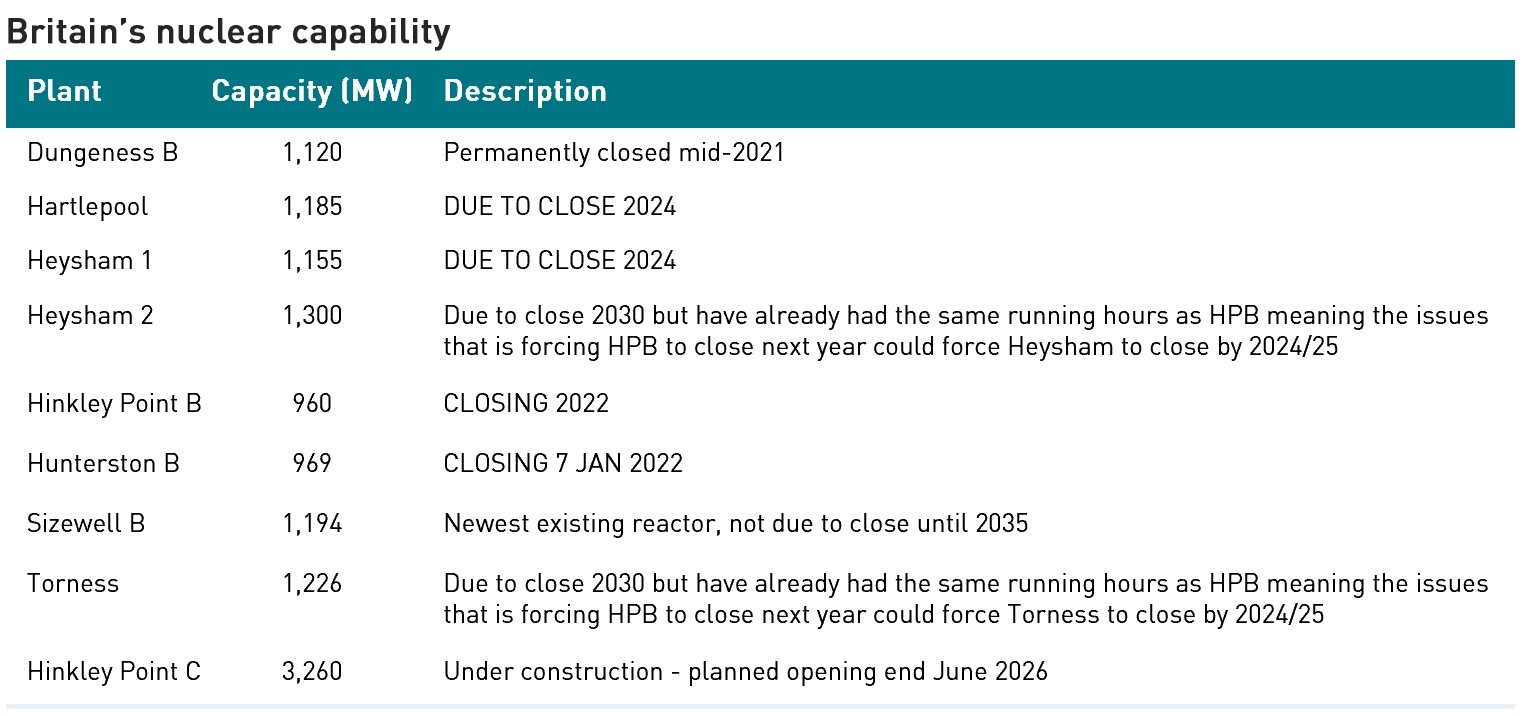

This time last year there was notionally 9.1 GW of nuclear plant operating and 3.26 GW under construction at Hinkley Point C. I say notionally because the 1,120 MW Dungeness power station had been offline since 2018, and EDF eventually took the decision this year to close it permanently. Excluding Dungeness, there was 8 GW of nuclear capacity, but available capacity was significantly less. The average winter availability last year excluding Dungeness was 67%.

The 969 MW Hunterston B reactor is due to close on 7 January next year, half way through the winter. The 960 MW Hinkley Point B station is also planned to close in 2022. Hartlepool (1,185 MW) and Heysham 1 (1,155 MW) are set to close in 2024. This means according to EDF’s schedule, the fleet will be reduced to 3.7 GW. However this could be reduced further depending on the condition of Torness and Heysham 2 – EDF announced this year that both could shut years ahead of their planned 2030 closure dates due to safety concerns.

The issue is that these reactors have already generated almost as much power in running for 33 years as Hinkley Point B and Hunterston did in 45 years. Those stations are closing early due to cracking in the graphite cores, a problem that is linked to the radiation levels generation from running, so given their higher utilisation levels, they could potentially develop this cracking at any time. Once cracks emerge, the plants would only have three or four years of safe running left. It is entirely possible both could close by 2025, meaning that only the relatively new 1,194 MW Sizewell B plant would remain by the middle of the decade.

The current planned start of operations for Hinkley Point C (3,260 MW) is the end of June 2026, so even if it opens on time (which is a big “if” given the delays across all of the European EPRs), there will be a significant nuclear gap, and the fleet would be only half of its current size.

The Government needs to act on the looming capacity crunch

The current energy crisis is bringing the UK’s looming capacity crunch into focus, and the Government is sounding increasingly enthusiastic about new nuclear. But caution is required: before throwing more money in the direction of as yet un-proven new technologies such as the Sizewell C /Moorside EPRs or the Wylfa AP1000, the Government should see some proof of concept.

The only next generation nuclear technology with any kind of track record is the Advanced Boiling Water Reactor, and while Hitachi has withdrawn its proposal for the Wylfa site and liquidated the company through which it planned to deliver the project, it still owns the land, and might be persuaded to re-kindle its interest for the right funding package. I still believe this is the best option despite it not being currently on the table, and greatly preferable to committing more money to technologies which so far are failing to materialise.

SMRs also merit support. Unlike the EPR and AP1000 reactors, they lack a track record, good or bad, but they show enough promise that they are worth developing further. The Government should provide the support needed to get them to the next stage of development. It’s time to stop prevaricating and make a serious commitment to credible new nuclear solutions.

On form, please check the spelling of “fresh” in the title.

Thanks – fixed!

Thanks Kathryn. Great article on the inflation in costs and delays in big nuclear projects.

It is a cautionary tale for those who expect salvation in nuclear energy, as a complement for intermittent renewables and in the end, it leaves us with 3 difficult choices:

– leave the Chinese on EPR projects because only they were capable of commissioning their EPRs (though there were problems there too). This is geopolitically unpalatable;

– pull the plug on Hinckley Point C in favor of SMEs which are, you point out, also unproven

– retain gas-fired plants as capacity back-up, and considering commissioning new gas storages to replace Rough.

Michael Grossmann

(writing from France)

There is so little transparency around Taishan that I generally exclude them from any analysis of the EPR. The safety regime is different in China, and we really don’t know on what basis the reactors were completed, what they cost, or what sort of reliability they have had.

I think we should go for ABWR as they are proven and can be delivered much more quickly than the alternatives. I wouldn’t pull the plug on HPC as the only risk there is that it isn’t delivered “on time” – costs to the taxpayer only really hit once the thing is running, so until the risk is all on EDF and I see no real reaason to make them stop.

SMRs are unproven but there are reasons for optimism given the history with sub-marine propulsion, so I would like to see the Government support SMR development alondside ABWR.

Then I think we need to keep coal open until a new large nuke can open, and make sure there is enough gas capacity. Quite a lot of new gas (mostly OCGT, but some quite large) was successful in the last capacity auction which also saw the higest prices so far. It looks as if the capacity market is slowly starting to catch up with reality, but I think the capacity issues are going to hit before those contracts start to deliver.

You cannot run a sensible discussion on this topic without considering how much demand for electricity there is likely to be, and what policies can affect that level

. The present concept of a new” family” of nuclear fission power stations was created in the Gordon Brown energy white paper of 2006 . This presumed that consumption levels of electricity in 2019 would be some 30% higher than has actually occurred.

With new SIs covering not just consumption standards for LEDs but also much other electricity using equipment and products, there is every likelihood of further dramatic improvements in electric energy consumption levels.

I don’t think anyone believes electricity demand is going to fall given electrification will be a significant pathway to net zero. If you look at the NG Future Energy Scenarios every scenario including Steady Progression has significantly higher electricity demand in 2050 with one scenario seeing electricity demand doubling. I don’t think it’s credible that efficiency measures will offset the electrification of a significant amount of heating and light transport, and I’m not aware of any forecasts that support that view (or that electrification will turn out to be insignificant). If you’ve seen some I’d be interested if you could post links.

It would be sensible actually to read what I wrote., before seeking to rebut a statement I did not make.

I was simply pointing out that official projections seem inevitably to underestimate the role that improved energy efficiency had had upon actual consumption levels. To go back even further, who fifty years ago was projecting we would be the time wealthier by now, whilst actually using less energy?

I think another advantage of SMRs is that they’re small enough to take the risk on one, “just to see” as it were, and then roll out if it works. I hope that the lead time is lower too.

That sounds good in theory but it’s not how SMRs are being approached. The theory with SMRs is that they can be “mass” produced, so they have very large up-front costs (£ billions) in terms of building the production facilities. So yes, small trial reactors can be built but the proof of concept is more around whether they can be produced at scale and that required a large up-front investment.

Some years ago (July 2015) Euan Mearns invited Hubert Flocard to write a piece on molten salt reactors. Flocard was a very senior French nuclear engineer. The piece was very interesting. At the very end of the comments I asked him a question whose answer has stuck with me ever since. Flocard said that current safety standards for nuclear reactors made them, essentially, impossible to build. It’s the ingrained fear of nuclear that does this. It may mean that old style large reactors are now all but impossible and we will have to wait for SMRs

The Flocard piece is still available at: http://euanmearns.com/molten-salt-fast-reactor-technology-an-overview/

Did you see this project?

https://www.dailymail.co.uk/news/article-10046765/Tiny-Devon-village-population-286-connected-MOROCCO.html

3.6GW of solar power via interconnector almost next door to Hinkley Point, trolling it. I see no plans for further grid distribution to cope. Mind you, I suspect the £16bn is just for the interconnector. 20GWh of batteries at £400/kWh is £8bn, 10.5GW of solar at say $2,000/kW and unspecified wind and you end up with much the same cost as Hinkley Point. Plus a battle over power lines crossing near Exmoor.

I did see it but am not holding my breath. This would require an interconnector double the length of Viking which is already the longest in the world, and for all the talk of African solar solving Europe’s power problems nothing has so far happened. I think issues such as sand on the panels are actually harder to solve than people might think.

And I agree with you on the costs – I’d rather pay for nuclear which has reliable output once built – assuming the technology works – maybe they’re betting HPC won’t work and they get the grid connection for free!

Why is it the first thing the government thinks of is regulation?

https://www.current-news.co.uk/news/government-details-regulation-plans-for-fusion-energy-in-world-first

It might seem depressing but I think it makes sense. Nuclear power involves huge amounts of energy whether it is fission or fusion, and in order to gain public acceptance there needs to be appropriate regulation. It might feel like putting the cart before the horse, but if you’re developing a project involving temperatures 10x hotter than the centre of the sun, I think it’s reasonable for that to be regulated.

Thanks to Pedantic Fan for pointing out the typos – I deleted your comment as requested, but I’m happy to receive corrections, particularly ones autocorrect misses!