The saga of the UK’s attempts to re-invigorate its nuclear industry continues, with further criticism of Hinkley Point C, this time by the Public Accounts Committee, speculation that an investor has finally been found for the Moorside project, and the expectation of a decision from the Government on the design of the new reactor proposed for the Horizon site in Wales.

Chasing economies of scale

The reason this is a saga, is that nuclear projects have ballooned over the years to a point where they are becoming extremely challenging to deliver. As this article from Nuclear Engineering International points out, the trend over the past four decades has been for nuclear reactors to increase in size and output, from 500 MW in the 1970s to over 1,500 MW now, driven by the notion that, through building larger plants, economies of scale could be realised as the cost of building larger units would rise more slowly than their output, lowering unit energy costs.

“The economy of scale is an idea that has a solid foundation in both the power industry and in other capital goods sectors. However, in nuclear there is no evidence that larger and larger reactors have reduced the unit capital costs. In fact, the evidence is in the opposite direction. Large economic studies in the US and French nuclear power programmes show that capital costs increased with size.

Safety improvements and tighter regulation will have played a part. The evidence is that larger nuclear reactors are more difficult to build, take longer to complete and as a result cost more. Studies in the late 1980s pointing out this relationship observed that the industry was designing reactors (then 1,000 MW output) that were beyond their ability to construct in an efficient manner.”

The combination of increased size and higher engineering requirements is leading to huge project costs, in the region of £4,000-£5,000 per kW of capacity, or £7-12 billion for the project as a whole. This is unaffordable now for any company that does not have some form of government backing, either through its ownership structure, or through project guarantees and other forms of support.

High upfront costs were traditionally offset by low in-use operating costs, however the price of new nuclear looks less attractive. The HPC strike price is starting to look uncompetitive versus some large-scale renewable projects (although not necessarily when the costs of intermittency are taken into account), and is certainly above the current cost of new gas-fired generation.

The other problem is that such large projects are difficult to build, with multiple problems arising during construction that are stretching lead times to almost a decade. Over the decade that the current generation of new nuclear reactors has been in development, other energy technologies have evolved at a rapid rate, with renewable generation achieving levels of cost and penetration that would have been unthinkable ten years ago.

European Pressurised Water Reactor (“EPR”) is a case in point

This is the design of the Hinkley Point C (“HPC”) project. There are currently four EPRs under construction apart from HPC, all of which have suffered significant delays and major cost over-runs, and so far none is operational. The two Chinese projects at Taishan are expected to open later this year or early next year almost five years late; the plant at Olkiluoto in Finland is due to open next year, nine years after its original start date; and the flagship French newbuild plant at Flamanville is expected to open in 2019, six years late.

HPC has already attracted a great deal of controversy – in June the National Audit Office (“NAO”) published a highly critical report saying the project was marginal at best, and a report issued on 13 November by the House of Commons’ Public Accounts Committee cited “grave strategic errors” in the Government’s handling of the £19.6 billion project.

The echoed many of the NAO’s concerns:

- BEIS has no plan in place for securing the wider benefits of the project;

- No one was protecting the interests of energy consumers in doing the deal;

- BEIS/DECC pressed on with locking consumers into an expensive deal, despite the case for Hinkley Point C and nuclear power weakening during its negotiations;

- BEIS/DECC and HM Treasury did not sufficiently appraise alternative ways to finance the deal that might have offered better value for consumers;

- There is uncertainty over whether the project will be completed on time;

- We are concerned about the BEIS’ ability to identify any possible delays as early as possible, given government’s poor track record on effective contract management.

The Committee felt that it is of vital importance that the Government is alerted in plenty of time if HPC is likely to be delayed so it can secure alternative power supplies. The four-year lead time for new CCGTs was referenced, as were the T-4 capacity auctions.

It is interesting to read the evidence given to the committee. It is clear that the EPR technology was chosen as it was deemed to be the only technology available at the time, and the top civil servants involved in the project still claim that it was a relatively modest development from previous PWR designs of which some 277 are currently in operation. This is despite the fact that even in 2013, the problems with delivering the EPR were already evident at Olkiluoto and Flamanville.

“There was, in fact, only one nationally approved technology available at the time, and if we were to get new nuclear moving in the timescale that we needed to in order to fill the type of gap that was going to be created by old nuclear coming off, we needed to go forward with the EPR technology,”

– Stephen Lovegrove, former Permanent Secretary, Department for Energy and Climate Change“I thought I might just add a couple of words: we talk about the technology of the EPR, and it is right to say that it is not operational now, and we do not expect it to be until 2019, in those countries – China, France and Finland. Nevertheless, it is not a completely new type of technology. It is the new generation for the pressurised water reactor. It is bigger, more sophisticated and more controllable, but it is not fundamentally different. It is the same technology as the 277 other pressurised water reactors that have been tried and tested and are operating around the world today, so I do not want to over-emphasise the extent to which this is a big leap forward,”

– Alex Chisholm, Permanent Secretary, Department for Business, Energy and Industrial Strategy

In reality, the Government (and for that matter the Civil Service) is completely dug-in as far as HPC is concerned, and it is unlikely either that there will be any meaningful change to the project or that there will be any acceptance of the flaws in the decision-making process. Even if HPC manages to open on time, which is already in doubt, it is extremely doubtful that it will ever represent a good deal for consumers.

Advanced Boiling Water Reactor

Horizon Nuclear Power, a wholly owned subsidiary of Hitachi Ltd is developing an advanced boiling water reactor (“ABWR”) at Wylfa Newydd on the Isle of Anglesey. The plant will have a capacity of 2,700 MW of energy from two Hitachi-GE modular reactors.

Advanced boiling water reactors the first Generation III reactors to be built, with four reactors operational in Japan at the time of the Fukushima disaster. Boiling water reactors (“BWRs”) are the second most common type of nuclear reactor worldwide accounting for about 20% of global installed nuclear generating capacity. The equivalent share for Pressurised Water Reactors (“PWRs”) is about 67%.

The fundamental difference between a BWR and a PWR is that water is allowed to boil in the BWR core and is then used directly to drive a turbine and generate electricity. The primary circuit pressure in a BWR is typically around half that necessary in a PWR. By using this “direct cycle” strategy a BWR has no requirement for any of the secondary circuit components which are necessary in a PWR.

A PWR precludes boiling in the primary circuit by means of the high primary circuit pressure. The thermal energy from the primary circuit is used to raise steam in a secondary circuit via large steam generators – typically 4 per reactor in modern PWRs. This secondary circuit steam is then used to drive the PWR turbine generator to produce electricity for the grid.

![]()

Reactivity control also differs between the two designs. In a PWR the core reactivity is principally controlled by the use of boric acid which is dissolved in the primary coolant. Since the BWR has boiling water in the reactor core, boric acid cannot be used as the primary means of reactivity control. Reactivity management in a BWR is accomplished via (i) burnable poisons such as gadolinia intimately mixed with the UO2 fuel, (ii) deeper control rod insertion and (iii) changing the amount of neutron moderation in the reactor via the control of coolant flow, eg in some BWR designs by varying the reactor coolant pump speed.

Although a BWR has fewer components compared with a PWR (no steam generators, less piping) it should be noted that the BWR pressure vessel is much taller than for an equivalent PWR since steam separators and driers are located above the reactor core. Also, in a BWR the primary circuit extends much further meaning that the same water which passes the fuel rods also passes through the turbine, and means that any water-borne contamination or activation products will be transported through the turbine and condenser, requiring additional shielding.

ABWRs have a modular design, with large sections of the reactor building able to be assembled in a factory, complete with wiring and components, before being shipped to site and lifted into place. The development of the ABWR design was unique, which has led to the unusual situation where three different companies offer a variation on the technology, which was initially co-developed by Toshiba and GE, who then worked with Hitachi to construct the first two units in the late 1990s. GE and Hitachi went on to form joint ventures of their nuclear businesses, resulting in two daughter firms: GE-Hitachi and Hitachi-GE. Both those joint ventures can build ABWRs, as can Toshiba, although its version differs in some technical respects due to intellectual property issues. The first four ABWRs were each built in 39-43 months – on time and on budget.

The first ABWRs were Tokyo Electric Power Co’s (“Tepco’s”) Kashiwazaki-Kariwa units 6 & 7 which started up in 1996-97. These were built by a consortium of General Electric (USA), Toshiba and Hitachi. They were shut down in 2011 following Fukushima, but earlier this year they were certified as meeting Japan’s new safety standards. They are expected to re-start in 2020.

Hamaoka 5 entered operation in 2005, but it’s future continues to be in doubt after the recently elected governor of the province announced that he is opposed to the plant re-opening. Shika 2 commenced operations in 2006, but ongoing studies to establish whether the seismic fault-lines beneath the plan are active means there is no immediate prospect of a re-start.

Shimane 3 was due to open in 2012, but work was halted due to Fukishima. As of September this year, no application had been submitted to the nuclear authorities for a conformity examination under the new regulatory standards. Work on the Ohma 1 plant was about 40% complete at the time of Fukushima. Construction of the additional safety features required by the new standards is expected to conclude in 2020, however there is currently no re-start date scheduled.

![]()

There has been some suggestion that the ABWRs were unreliable, with low operating factors, however there is also a view that the issues that led to the plant outages were fairly standard for Japanese reactors. The problems referenced in relation to Lungmen in Taiwan may not be technology-specific – the project was halted multiple times due to political objections, and the project sponsor entered into separate contracts with suppliers and contractors rather than opting for a turnkey delivery from GE Hitachi.

The ABWR design was certified in the US in 1997, and is now in the detailed assessment phase of UK certification. The licensing of the plant is more complicated in the UK than in the US, France or Asia, as the nuclear industry has been less active in recent years. Regulations predominantly rely upon an agreement that the plant is adequate and fit for use, as opposed to strict prescriptive rules.

The Government’s preliminary conclusion is that it considers many of the environmental aspects of the ABWR design would be acceptable. However, at the current stage of the detailed assessment work there are 3 issues to be addressed before a full statement of design acceptability can be issued:

- Decommissioning: Hitachi-GE must provide sufficient evidence to demonstrate that the UK ABWR has been designed to facilitate decommissioning and minimise associated waste and environmental impact of decommissioning;

- Source terms: Hitachi-GE must provide a suitable and sufficient definition and justification for the radioactive source terms during normal operations;

- Consideration of “best available techniques” and “as low as reasonably practicable” in optimisation: Hitachi-GE must demonstrate that appropriate consideration has been given to both environmental and safety aspects, in order to achieve an optimised design

The Government’s decision is expected sometime this month.

Should the licencing and consenting process go smoothly, first concrete could be poured in 2019. If the construction process runs proceeds as for the Japanese plants, it could be open within 5 years, potentially beating HPC’s expected commissioning date expected in late 2025.

Other projects

New hope for Moorside

In October, NuGen, Toshiba’s nuclear project at Moorside in Cumbria announced that it expects to secure a new investor early next year, assuring the project’s future, which was thrown into doubt after developer Toshiba’s nuclear arm, Westinghouse, went bankrupt this year. Toshiba’s previous NuGen joint venture partner, Engie, subsequently withdrew from the project.

South Korea’s Korea Electric Power Corp (“KEPCO”) and China General Nuclear Power Corporation (“CGN”) have both said they are interested in bidding for the project, and there has been speculation over the past few days that KEPCO is close to announcing an investment in the scheme.

It was initially hoped electricity generation would begin by 2025 but these delays will push back the likely start date towards 2030, with the timing depending on which of the bidders is successful, as both are likely to want to use their own reactor technology. Whichever technology is chosen, it will need to go through the four-year, Generic Design Assessment (“GDA”) approval process.

KEPCO’s reactor design has yet to start the process, while CGN submitted its application earlier this year as the company also plans to build a new plant at Bradwell in Essex. The initial plan included using the Westinghouse AP1000 technology which already has GDA approval.

Bradwell B and Sizewell C

Last year, CGN bought a 33% stake in HPC and agreed to jointly develop new nuclear plants at Bradwell in Essex and Sizewell in Somerset. Sizewell will use an EPR, while the plan for Bradwell is to use CGN’s Hualong One design (“HPR1000″). The GDA process for the reactor was launched in October lasts year.

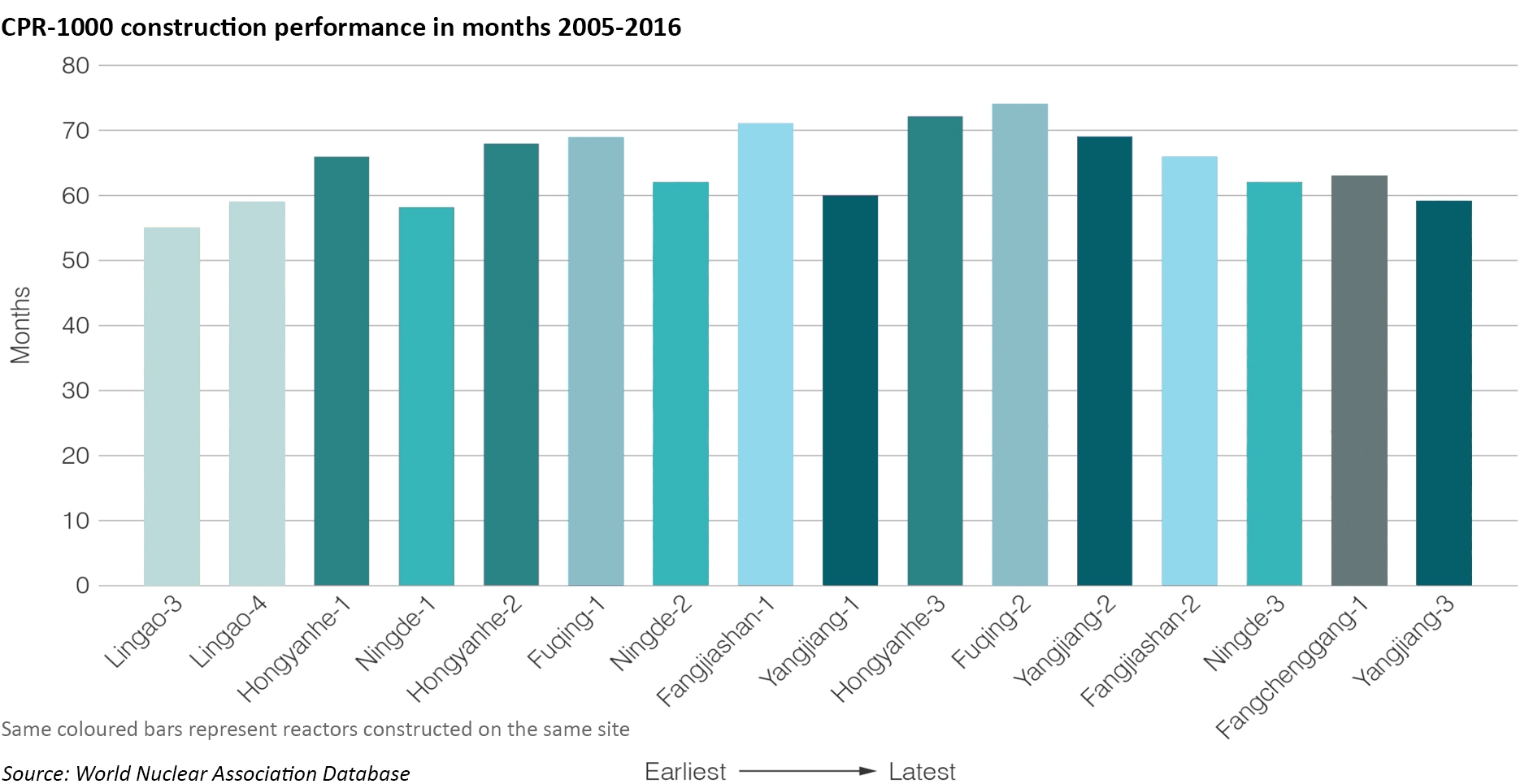

Hualong One is a standardised PWR design created by CGN and China National Nuclear Corporation, after the Chinese authorities directed the two companies to rationalise their reactor programmes. The resulting design is intended to be widely deployed in China and exported globally. The reactor is actually a French design, based on the designs of the two most recently-built reactors at the Gravelines power station near Calais. It is a three cooling-loop PWR developed in the 1990s, a forerunner of the EPR design. It is known as the CPR1000 in China, where 15 units have been built.

The chart indicates the construction times for CPR1000s build in China – the build times range from 55 to 75 months, longer than the average ABWR construction time.

Making new nuclear work

The Nuclear Engineering article describes three ways of reducing the costs of new nuclear projects:

- Standardisation of reactor designs and construction processes;

- New, simplified reactor designs;

- Small modular reactors (“SMRs”).

The South Korean experience is highlighted in support of standardisation: projects are smaller at 900 – 1,000 MW, using a standardised design, allowing development of a common supply chain and learning from experience. Since 1995, a dozen such reactors have been built, with construction times falling from 6.5 to 5.5 years and capital costs by 30%. Interestingly, although it is not small, the ABWR is designed on a modular basis, which may be supporting the shorter construction times for the technology.

The arguments for new technologies are less compelling since of the many new designs mentioned, none has yet reached the proto-type stage. The same can be argued for SMRs – while the theory is interesting, the practicalities may be harder since the upfront costs of individual reactors are replaced by the upfront costs of the SMR factory. That is not to say that new nuclear technologies such as molten salt reactors (although these are not strictly new) and SMRs could not play a meaningful part in the future of the sector, but there is currently no clear path to market for them.

The Government and senior Civil Servants remain resolutely convinced that HPC is the best answer to the UK’s need for new nuclear power, however, based on global experience to date, the ABWR would seem to be a safer bet. ABWR has been shown to be a viable technology with a number of plants in successful operation before the Fukushima-driven shutdown, and they were delivered on time and on budget. Construction times were also shorter than either the EPR or the Chinese equivalent.

Agreeing the HPC strike price at such a high level was not only an error in hindsight, but one which could have been reasonably predicted to be problematic at the time. The Government should, without compromising safety standards, be seeking to secure proven technologies as a first step to meeting capacity challenges in the next decade – ABWR looks to be the most promising of the alternatives, and may yet come to market before HPC. That would be good for the market, but a further embarrassment for the Government.

Excellent overview. Thank you for the research

Good overview. Andy Dawson’s reviews of competing designs are also worth a look:

http://euanmearns.com/an-overview-of-the-kepco-apr1400/

http://euanmearns.com/chinas-hualong-1-passes-the-first-stage-of-the-uk-gda-process/

A further post is forthcoming on the Wylfa design.

Andy Dawson’s ABWR review:

http://euanmearns.com/the-hitachi-advanced-boiling-water-reactor/

Moorside remains in doubt, now Hinkley Point C wavering.

Does this suggest that privatisation of nuclear generation (NG) back in the 1990’s was a bridge too far ?

Beyond business who are not keen on such lengthy payback & risky projects.

In my view the NG part of the Central Electricity Generating Board (CEGB) should have remained in public ownership.

NG delivers quietly & efficiently 24/7 essential & well suited the UK electricity demand profile currently & in the future.

We must appreciate that what we have now was developed & constructed by the excellent skills within the CEGB.

All this expertise was dispersed & lost at privatisation.

Overall privatisation of the electricity supply industry has been a success, it’s just the NG part that I question.

I feel that NG need’s to be part of a national infrastructure programme under public ownership.

Barry Wright, Lancashire