March saw the latest capacity market auctions: the T-1 auction for delivery in 2021/22 was held on the 12th and the T-4 auction for 2024/25 was concluded on 22nd. The assets leaving the auction compared with those succeeding highlight changes that are taking place in the market, with large dipatchable assets being replaced with smaller, flexible assets (and of course renewables which in general do not participate in the auctions).

The forced exit of coal, the unexpected early closures and low reliability of the aging nuclear fleet, as well as older CCGTs (and the loss of the Calon units) is changing the structure of the market, as small peakers, DSR, batteries and interconnectors step in to fill the gap.

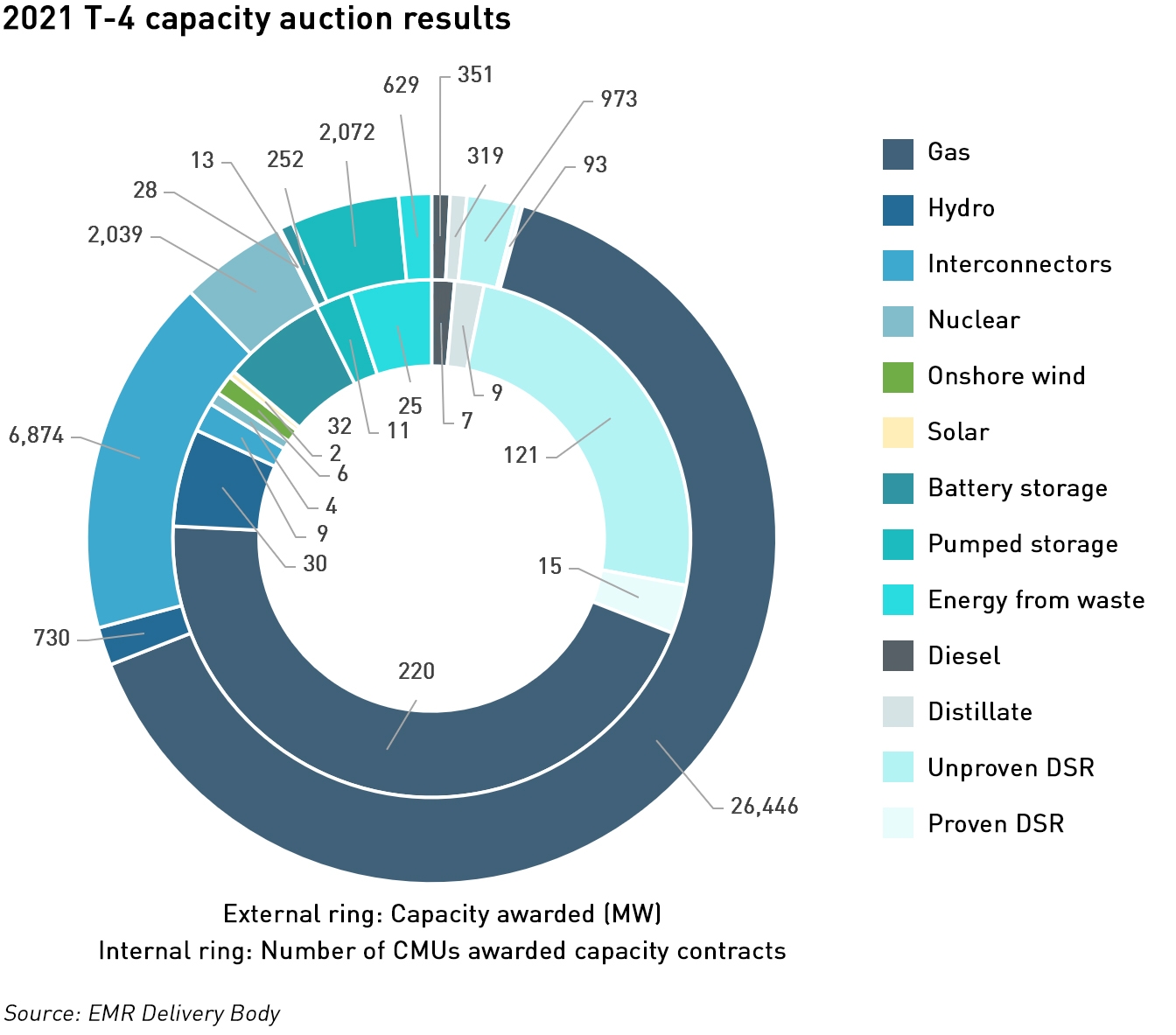

Another high clearance price in the T-4 auction

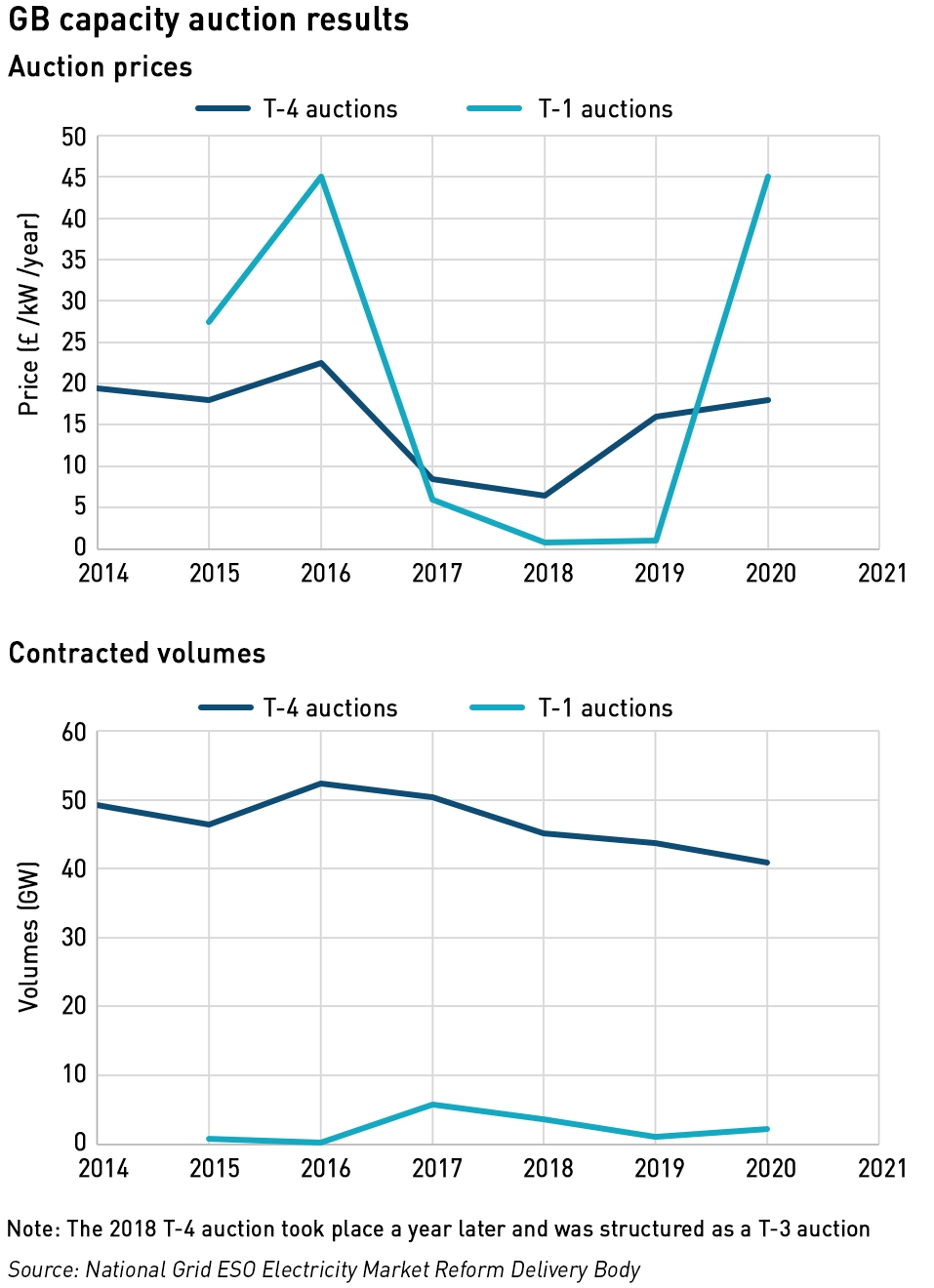

Following the T-4 auction held in 2020 which cleared at £15.97 /kW/y, the most recent T-4 auction cleared at £18 /kW/y and procured just under 41 GW of capacity. This resulted in another good year for new-build developers, with just under 12 GW of contracts secured.

No coal units participated for the first time because the delivery date for this auction is after the 2024 cut-off for coal to exit the market. The gap left by coal was more than covered by the overall drop in the amount of capacity being procured, which at just under 3 GW less than in the previous auction was significantly greater than the 1.3 GW awarded to coal last time.

The amount of nuclear power in the capacity market has almost halved, continuing a downward trend. Given recent reliability issues, it may be that EDF was risk-averse in its bidding strategy to avoid the possibility of non-delivery penalties. It could also be keeping the capacity in reserve in the hope of securing higher prices in the T-1 auction for that delivery year.

Interconnectors now hold a share of 16.8%, an increase on the 12% held previously. As regular readers will know, I am sceptical that interconnectors can genuinely support security of supply at times of high winter demand since most of our interconnected markets share a high degree of weather correlation with us.

During winter cold spells, French demand often outstrips British demand due to widespread use of electric heating compared with dominance of gas heating in the UK, meaning that Britain can end up exporting power at times of high system demand. For example, in Winter 2019, Britain exported electricity to Continental Europe during 13% of the hours with the top 5% of demand.

The other issue with interconnectors is that since the UK left the EU, it has also left the market coupling regime, meaning that interconnector capacity is allocated via explicit auctions which take place before the market prices for electricity are known due to the timings of the various auctions. Most interconnector capacity is traded in the day-ahead market with very little intra-day liquidity, so it is unclear to what extent interconnector flows could be adjusted in the short timeframes applicable in a system stress event.

According to Timera Energy, this auction “provides an interesting insight into the structural transformation of the UK power market as it decarbonises”. As older nuclear and CCGTs exit the market, and with the coal fleet now gone, new capacity in the form of DSR, gas peakers, batteries and interconnectors are taking an increasing share.

“These structural changes in the capacity mix are supporting clearing prices in the capacity market. They are also driving a transformation of UK wholesale & balancing market price signals. The current winter is evidence of how price volatility is rising, and with it the returns on flexible capacity,”

– Timera Energy

The evidence of this trend can be seen from the plant which exited early versus that which secured agreements:

- 3 EDF nuclear units (Dungeness, Heysham & Torness) totalling 1.5 GW exited

- Rocksavage & Keadby 1 CCGTs (2.1 GW) exited

- New interconnectors secured 3.5 GW

- 2.1 GW of new and refurbished gas-fired capacity secured contracts

- Almost 1 GW DSR secured contracts

Of the new interconnector projects, three out of four had secured capacity contracts in previous auctions (Eleclink, IFA2 and NSL), meaning that only the 0.7 GW Viking Link is genuinely new interconnector capacity in this auction. But all of the new interconnector projects that have passed their Final Investment Decision have now secured capacity contracts, meaning that the genuinely new interconnector capacity is unlikely to be seen in the next auctions since the project pipeline is already now represented.

The successful DSR capacity was dominated by large ENEL X, E.ON and Centrica projects, which are likely to be met by some genuine demand response (such as commercial and industrial processes) in combination with behind-the-meter batteries and engines. Larger distribution-connected flexible assets (or aggregations of smaller assets) are finding success with economies of scale driving the increasing dominance of a small number of established portfolio players compared with large numbers of small projects in earlier years.

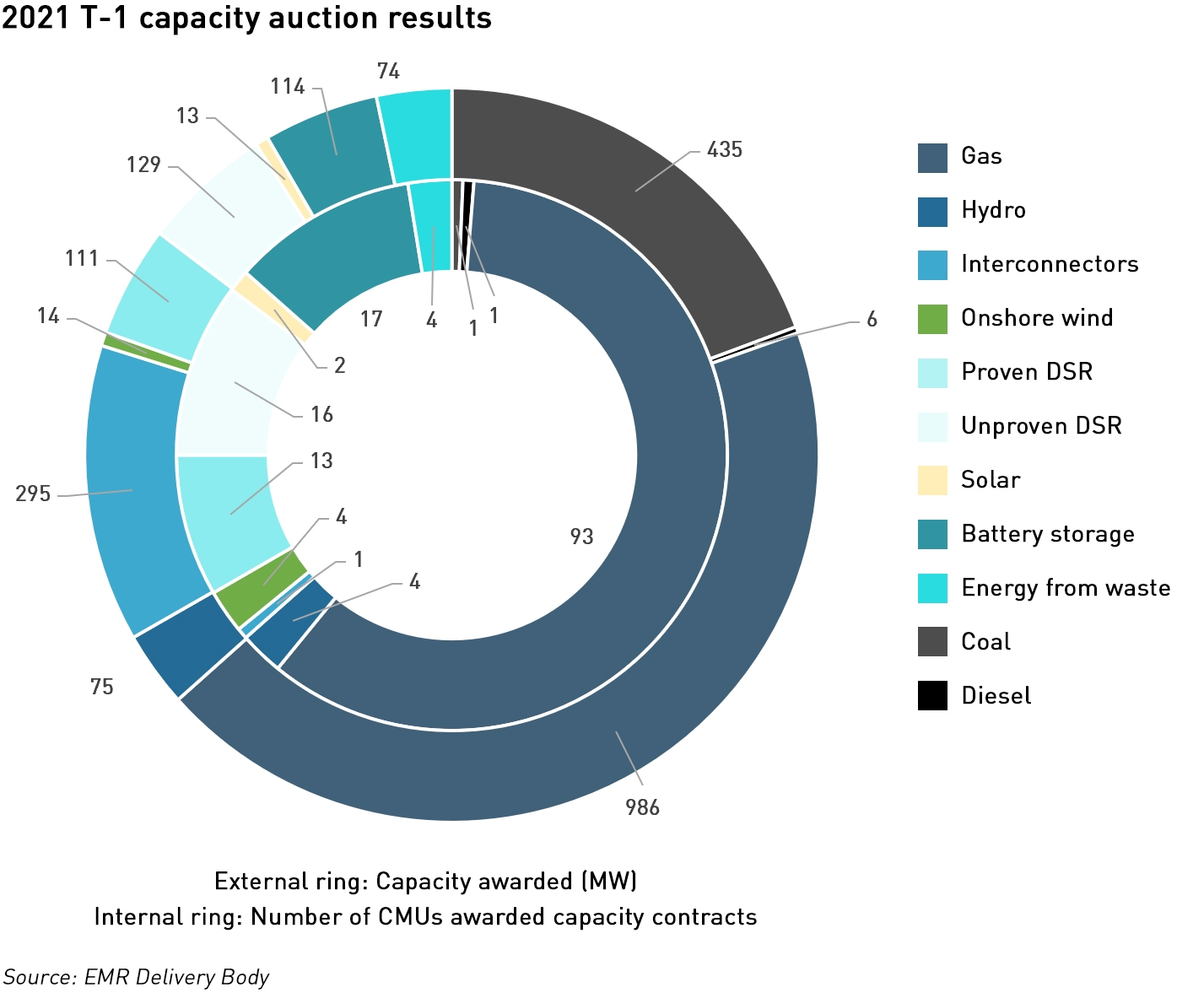

A completely different result in the T-1 auction

Last year, the T-1 auction procured just over 1 GW at £1 /kW/y. This year, just under 2.3 GW was procured at £45 /kW/y. Aside from the price increase, the other major difference was in the share of interconnectors which fell from around 80% last year to just under 15% this year.

This significant increase in price was largely due to the early exit of most of the West Burton coal units from the auction, coupled with the higher procurement target – 2.4 GW versus the previously approved 0.4 GW. The increase was recommended by National Grid ESO due to the unexpected loss of the Calon CCGTs (Severn Power and Sutton Bridge) and a delay the opening of the 1 GW ElecLink interconnector with France, which is now expected to be completed in 2022.

West Burton exited in round 6 of the auction, which is where the auction cleared, so the bidding price for the plant was only just above the acution clearing price. This leaves just one coal plant – Ratcliffe-on-Soar – with a capacity contract.

Battery storage saw a large increase in secured capacity, while unproven DSR more than halved since the last auction due to the closure of a loophole that allowed behind-the-meter batteries to be de-rated like DSR.

The T-4 auction for delivery in 2021/22 secured over 50 GW of capacity at £8.40 /kW, so the pricing of this top-up auction means that the procurement target was hit at an average price of under £10 /kW.

Is the capacity market fit for purpose?

The capacity market was introduced to solve the so-called “missing-money” problem: the growing deployment of near-zero marginal cost renewable generation reduces the utilisation rates of conventional generation to a point that it becomes uneconomic to remain open. However, intermittent generation cannot meet year-round demand, so to ensure security of supply a new source of economics for dispatchable plant was introduced.

Capacity contracts are only called upon as a last resort, when demand control measures are in place, after the Balancing Mechanism and Reserve products have been exhausted. Last winter saw multiple days on which market tightness led NG ESO to issue Electricity Market Notices and even Capacity Market Notices, and although these notifications have not to date actually preceded a system stress event, the increase in market tightness cannot be ignored.

The structural changes to the market described above will only serve to increase this trend. The closure of aging nuclear and gas plant, and the exit of coal is leading to much tighter winter capacity margins, which will lead to more instances of system tightness, and higher and more volatile market prices.

Of the flexible assets that are stepping in, batteries cannot address tightness that arises from periods of cold, still winter weather which last far longer than the 1-2 hours batteries typically last. Turn-down DSR is similarly limited – industrial and commercial process are also time constrained, and as noted above, interconnectors may be unable to deliver when the connected markets are experiencing similar weather-driven demand. Indeed they may increase system tightness is faster demand growth in other markets drives exports.

This means that gas and diesel engines will be filling the gap. These types of small peaking plant have been the big success story of the capacity market, yet their environmental footprint is significantly worse than the CCGTs and nuclear plant they are displacing. Indeed, the replacement of nuclear by gas (and as gas cannot currently be abated by CCS) is inconsistent with net zero targets.

Although the capacity market was never expected to support new nuclear, the Government had always envisaged that new CCGTs would be built, and yet virtually no new CCGT projects have emerged due to capacity market support. T-4 auction prices would need to rise to around £30 /kW/y to provide the necessary finance for new CCGTs.

With electricity demand likely to increase with the de carbonisation of heating and transport along with the loss of aging nuclear and gas plant and the coal exit there are real question as to where the market will go from here. Higher winter wholesale prices are not enough to support new large-scale conventional capacity, and while higher price volatility supports flexible assets, these cannot fill the gap left by large dispatchable plant.

But the amount of capacity being procured is sized to meet Loss of Load Probability (“LOLP”) targets and is not concerned with wholesale market pricing. The market can be tighter and prices higher and more volatile before LOLP begins to rise. As capacity margins fall, the market will become much more vulnerable to dunkelflaute, driving demand both here and in our interconnected markets, and to un-planned outages particularly in the remaining nuclear fleet. And to the quality of NG ESO’s market modelling. System stress events might be avoided, but high and volatile prices spell bad news for consumers.

.

This blog post was co-authored by Adam Porter.

Very informative and whilst the mainstream media will no doubt celebrate when Ratcliffe switches off the final time how long before they find out that diesel peakers are chugging away on industrial estates all round the country polluting local neighbourhoods..

Exactly. And at the same time they will be complaining about how expensive their electricity is!

I note the penny seems to have dropped finally at BEIS favourite consultant Aurora. They understand at last that interconnectors and storage won’t cut it, and we’ll need a lot more dispatchable capacity. However, they only comment somewhat obliquely on the net zero cost of fuelling it with hydrogen and CCS plants. Some slides here:

https://nkro22cl16pbxzrpzy39bezk-wpengine.netdna-ssl.com/wp-content/uploads/2021/08/Out_of_gas_Public-1.pdf

I can never make up my mind about Aurora. I think a lot of their work gets mis-represented, eg BEIS asks for some research on what a 100% renewables gird would look like so they go away and write something, which then gets reported as “Aurora says we’ll have 100% renewables by X date”.

On the other hand, they keep taking taxpayer money to write this stuff, some of which really tests the bounds of credibility