The need for reform of the retail energy market is increasingly clear – the past week has seen the failure of another new entrant supplier, bringing the total number of failures in since the beginning of 2018 to 17*. At the same time, suppliers are struggling to meet the requirements of the Renewables Obligation (“RO”) scheme, with a final order being issued last week to one non-compliant supplier, and a new forecast from Cornwall Insight that this year could see another significant shortfall. Requiring other suppliers to meet these shortfalls could lead to further stress on those suppliers that are already stretched.

This comes as the Government has launched yet another investigation into the retail energy market. The Future Energy Retail Market Review was originally announced in November by Business Secretary Greg Clark during a speech in which he also declared, somewhat optimistically, that the “trilemma” is no more.

The new review will also look at the arrangements that will apply after 2023 when the price cap is due to expire. Whether the price cap will survive that long remains to be seen, after a 10% increase was announced by Ofgem in February, just months after the scheme launched. Both large established suppliers and new entrants raised their tariffs in response.

* By my count, 14 small suppliers closed in 2018: Brighter World, Future Energy, Flow Energy, National Gas & Power, Gen4U, Electraphase, Spark Energy, Iresa, Snowdrop, Usio, Extra Energy, Planet9 Energy, Affect Energy and One Select. In 2019, Economy Energy, Our Power and now Brilliant Energy have failed.

RO mutualisation adds to the pain for small suppliers

London-based supplier Brilliant Energy ceased trading this week after falling into credit default. The company had around 17,000 domestic customers as well as a white label agreement with Northumbria Energy. The company is the third supplier to fail this year (after Economy Energy and Our Power), affecting over a million gas and electricity consumers.

“The failure of another supplier is a clear sign Ofgem needs to urgently move forward with its reforms to better monitor existing companies and take action earlier when problems arise,”

– Gillian Guy, Chief Executive, Citizens Advice

Last year, Brilliant Energy was one 14 suppliers which failed to meet its RO payment by the late payment deadline of 31 October.

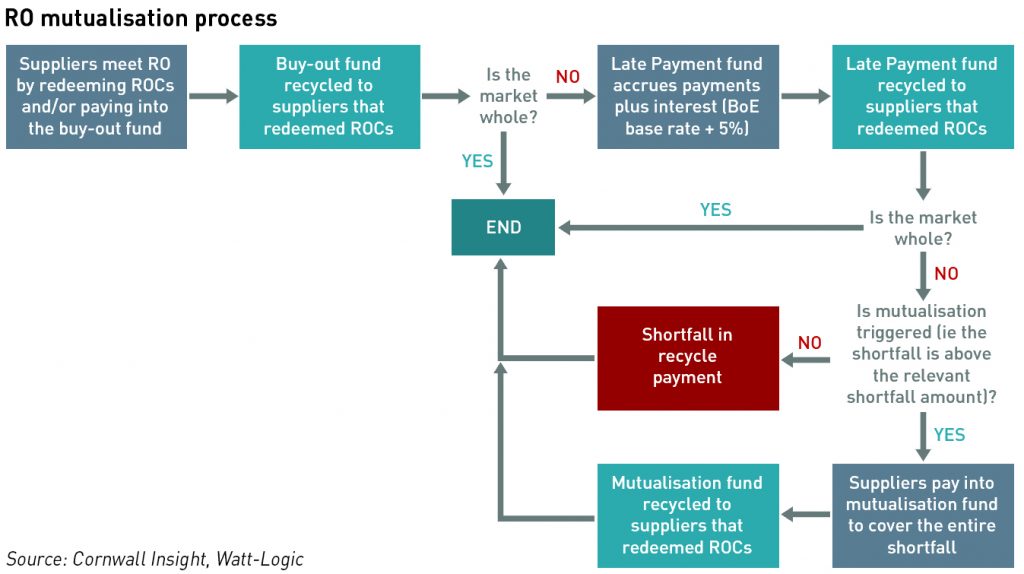

Under the Renewables Obligation scheme, for each megawatt hour of electricity it has sold to its customers in a given yearly compliance period, a supplier must submit a set number of Renewables Obligation Certificates (“ROCs”) to Ofgem or make up the difference through buy-out payments. ROCs can be bought from accredited renewable generators, which receive a set a number for each megawatt hour of electricity they produce.

If any supplier fails to meet its obligation by the 31 August payment deadline, it has until 31 October to make the payment, plus interest of 5% above the Bank of England base rate. Failure to comply with this deadline leads to a shortfall in the scheme for that compliance period, and, if the shortfall exceeds the relevant shortfall amount (currently £16.9 million), the mutualisation process is triggered, whereby all operational suppliers must make payments to the mutualisation fund in proportion to their market share.

The proceeds of the late payment and mutualisation funds are distributed on the same basis as the buy-out fund.

Last year (the 2018/18 compliance period) saw a shortfall of £58 million, with 14 suppliers defaulting on their oblgations:

- Three suppliers, Ampoweruk (£368), Brilliant Energy (£77,446) and Planet 9 Energy (£1) paid in full after the deadline, although two of these have since ceased trading;

- Enforcement action was launched back in November against Economy Energy (owing £15.7 million to the RO and £1.4 million to RO Scotland (“ROS”)), and Spark Energy (owing £13.4 million to the RO and £1.0 million to ROS), both of which subsequently ceased trading;

- A further suppliers six suppliers ceased trading while in default of their RO/ROS payments: Future Energy Utilities (owing £0.6 million to RO and £322 to ROS), GEN4U (owing £19,143 to RO and £782 to ROS), Extra Energy Supply (owing £14.3 million to the RO and £1.3 million to ROS), Iresa (owing £8.9 million to RO and £0.6 million to ROS), Electraphase (owing £0.2 million to the RO, £6,765 to ROS) and Snowdrop Energy Supply (owing £0.2 million to the RO and £736 to ROS);

- Two suppliers were placed on payment plans, with a requirement to make monthly payments to clear their obligations by the end of March: URE Energy (£209,014) and Eversmart (£367,150). On 8 March, Ofgem issued URE Energy with a final order requiring the supplier to pay the outstanding amount overdue payment by 31 March. The amount listed in the order suggests that no monthly payments have been made, and it seems likely that URE will be forced to close.

- The final supplier, Click Energy (owing £0.8 million to NIRO) has been referred to the Utility Regulator in Northern Ireland (mutualisation does not apply to the Northern Ireland fund).

As there has been no word of action against Eversmart, it seems likely it has been making payments, even so, the amount of the shortfall subsequently recovered by Ofgem looks quite small – below £0.5 million unless it has managed to recover anything from the administrators of the failed suppliers where the RO debt would be treated like any other unsecured obligation.

The result of this is that all remaining suppliers (including those who only partially met their original obligations), will need to meet the shortfall by paying into the mutualisation fund in proportion to their market share. This effectively means that compliant suppliers are penalised for the non-compliance of others, and those suppliers that complied through the submission of ROCs will need to wait longer to receive their share of the payments.

There is also a possibility that some smaller suppliers may struggle to meet their new payment obligation under the mutualisation rules – the payments will be made in four quarterly instalments, beginning in September.

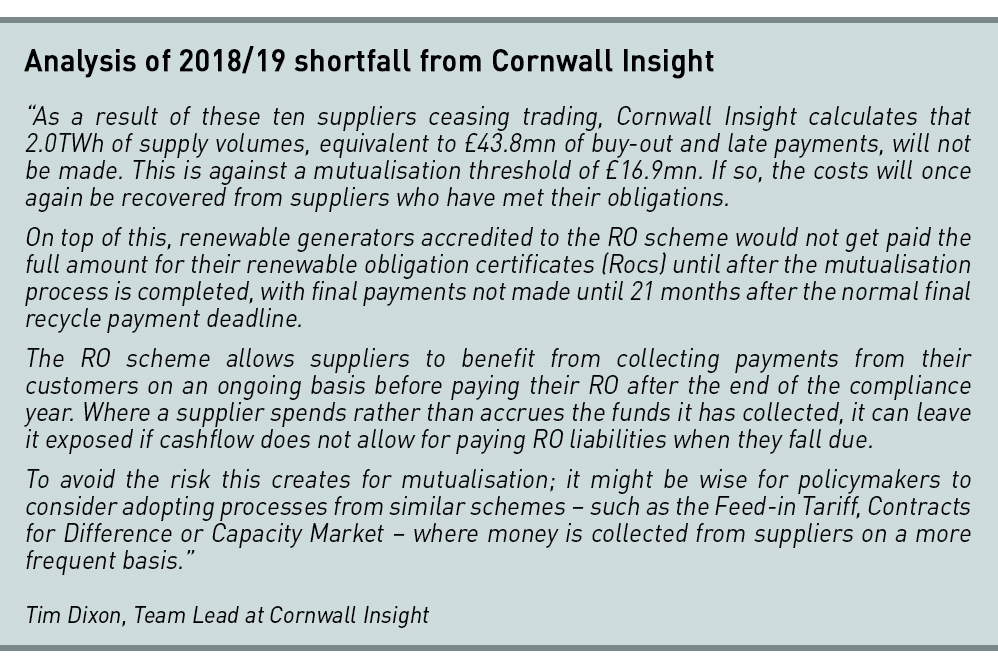

Analysis from Cornwall Insight suggests that the shortfall for 2018/19 will also be large, although not as large was last year, at around £44 million, based on an assessment of the supply volumes of the suppliers that have exited the market in the past year. However, the number could rise if more suppliers fail.

Cornwall also highlights one of the possible abuses of the current system, where suppliers collect RO payments from their own customers before they are required to make payments to Ofgem, creating the ability for them to use these RO payments as working capital. Another possible abuse of the system arises due to the relatively low level of interest that Ofgem applies to late payments – for some suppliers this can be cheaper than their normal cost of debt, creating an incentive for them to pay as late as possible.

If the supplier subsequently falls into financial difficulties (which is not unlikely where companies are trying to squeeze working capital as much as possible), the consequences of these choices will then fall on all other suppliers that have not behaved in this way.

Larger suppliers are not immune to retail market challenges

Despite the problems being faced by new entrant suppliers, the Big 6 continue to lose market share – according to the latest State of the Energy Market report (June 2018), the Big 6 collectively have their lowest ever share of the market, although at 75% for gas and 76% for electricity, this is still significant.

SSE recently reported its customer numbers had fallen from 6.45 million in December 2017 to 5.88 million a year later, with a loss of around 160,000 customers in the final quarter of the year. SSE also saw its credit ratings downgraded by both Moody’s and Standard and Poor’s by one notch to Baa1 (stable outlook) and BBB+ (stable outlook).

After failing to agree terms for merging with SSE’s retail business (which is now up for sale) npower has seen significant customer losses – around 650,000 in 2018 – and announced in January that it will cut 900 jobs, representing 14% of its workforce. There are reports that the company may even be wound up as losses continue with parent company Innogy’s chief financial officer Bernhard Guenther, saying its options include “selling the customer book and winding down the operations of the business”. Innogy is also open to offers to buy all of npower, or the business could still be transferred to E.On as part of a wider asset swap.

Npower is the smallest of the Big 6 suppliers and lost money in each of the past four years despite restructuring efforts and heavy job cuts. Losses increased from €63 million in 2017 to €72 million in 2018 last year, and is expected to lose about €250 million this year after the price cap forced it to cut prices.

This week E.On published its 2018 results, announcing the loss of 200,000 UK customers, primarily in the electricity market, and a huge 43% reduction in operating profits in its UK supply business, despite revenues having seen an 8% increase (driven by higher power prices and increased gas sales in the cold weather). The business incurred an operating loss of €1 million in the final quarter of the year, compared with a €108 million profit in the same period in 2017, which it attributed to “persistently challenging market conditions, higher restructuring expenditures, regulatory effects, and a weather-driven decline in power sales volume”.

EDF Energy also saw its customer numbers fall by 200,000 in 2018, and an operating loss of €172 million (across all divisions), and was forced in January to deny rumours it was planning a retreat from the UK energy market. The company has been particularly affected by the suspension of the capacity market, losing £69 million in expected capacity payments in the fourth quarter of 2018.

Even the largest supplier, British Gas, is struggling, with parent company Centrica seeing its share fall to a 16-year low after reporting that it lost 742,000 customers in 2018 and could see profits hit by £300 million as a result of the price cap, including a one-off impact of about £70 million in the first quarter of 2019. The company also announced between 1,500 and 2,000 job losses on a like-for-like basis in 2019, which are part of the 4,000 cuts to 2020 announced last year.

Only Scottish Power managed to buck the trend, with customer numbers holding steady, and delivering 3% margins on its supply business which helped the supply and generation division earn profits before interest, tax and other charges of £272 million for last year, up from £95 million in 2017.

Life for consumers isn’t rosy either

It might be tempting to assume that if life is difficult for suppliers, things must be good for consumers, but this is far from the case. As I have described previously, suppliers have decreasing control over end-user bills, given the growth in external factors such as policy costs and network costs which are all recovered through bills.

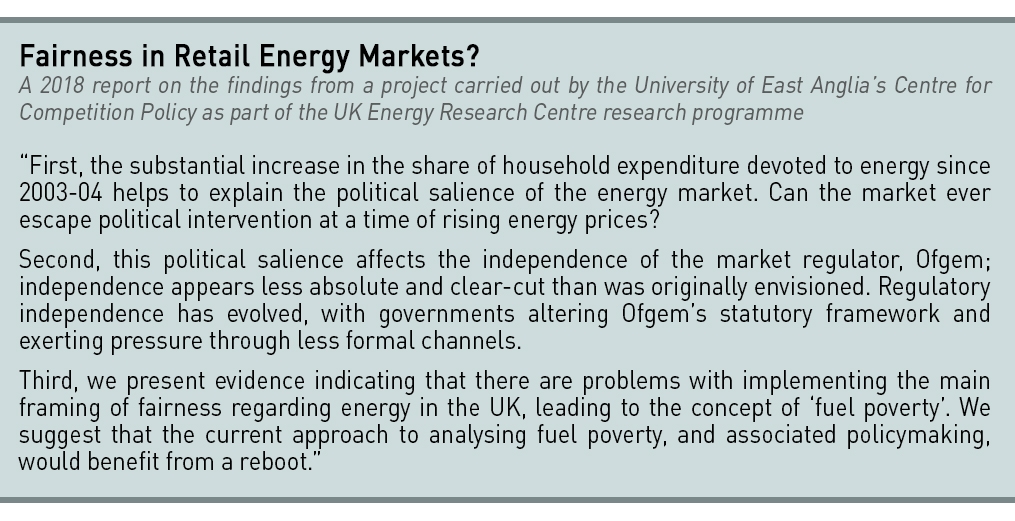

The result has been steadily rising domestic prices whose unpopularity led to the implementation of the retail price cap last year. However, so far the outcome is as expected – the cap level has had to rise to account for increases in these external factors (which also includes wholesale prices), meaning that consumers continue to face higher prices. Research published last year on fairness in energy markets indicates that the proportion of household income being spent on energy has returned to the levels last seen in the late 1970s, with the least well-off households spending the highest proportion of their income on energy.

It is clear that retail market reform is needed. Since de-regulation, the Government has sought ways to reduce market concentration and the risk of monopolistic behaviours by encouraging new suppliers to enter the market. However, this has come at the same time as de-carbonisation and other environmental policies have arisen, and the choice by successive governments to recover the costs of these from consumers through the bills they receive from suppliers, adds burdens onto smaller suppliers that they are ill-equipped to manage.

These difficulties are recognised, and so not all environmental and social obligations are borne by all suppliers, but this adds further complexity, with new suppliers needing to assess which obligations apply to them, and when new ones will arise, for example as customer numbers grow. This is surprisingly difficult for suppliers to do, as the number of schemes and requirements is large. The exemptions also encourage aggressive pricing models that become unsustainable as customer levels grow.

On top of this, energy is largely commoditised in that is difficult to supply a “better” kWh of gas or electricity. Some suppliers try to create differentiation by supplying electricity from local, community schemes and/or renewable sources (there is no equivalent for gas), however the key drivers for most consumers when choosing their suppliers are price and service.

While cheap tariffs can attract new customers and help challenger suppliers to gain market share, delivering good service is the key to retaining customers. Smaller suppliers can struggle to maintain low prices, particularly when wholesale prices rise, as they struggle to hedge themselves effectively – even if they have the expertise to understand how to construct an efficient and effective hedge portfolio, they generally find access to credit and liquidity (in the size and shape they need) to be a major barrier.

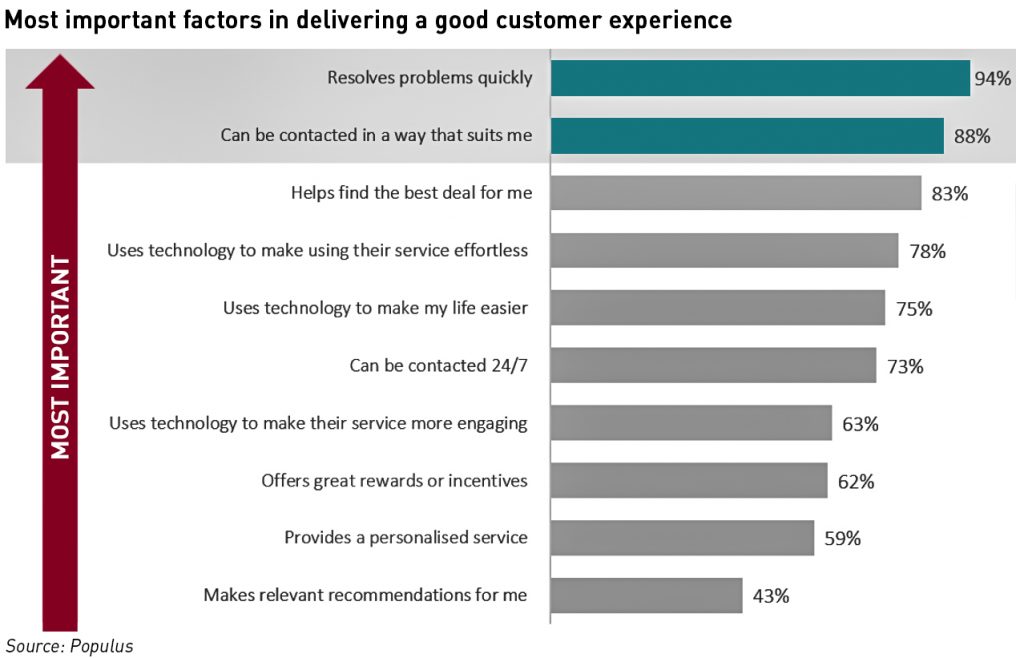

Delivering good customer service is also difficult as it requires investment in good billing systems, call centres and the technology to deliver the customer experience the most active customers (ie most likely to switch to or away from a new supplier) require. Research carried out last year by Populus in behalf of Which? shows that there are three crucial components to customer satisfaction for energy customers: resolving issues quickly; integrating technology to make life easier and more fun; and keeping things relevant for the individual.

Smaller suppliers are struggling to deliver these levels of customer service. This leads to complaints and poor reviews, with customers leaving and not being replaced as the company gains a reputation for poor service.

“The collapse of energy firms is becoming far too commonplace and consumers must not be made to shoulder the costs for these failures. It is vital for the regulator to press ahead with measures to ensure that current and future suppliers are financially sustainable and able to deliver excellent customer service,”

– Sarah Threadgould, Chief Customer Officer at Which?

Retail market reform

In November, Ofgem launched a consultation into the licence conditions for new energy suppliers, proposing tighter standards of financial resilience and ability to deliver good customer service for new entrants before a supply licence would be granted. The consultation closed in late January, and Ofgem was originally expecting to finalise its proposals for new entry criteria early this year, with a new consultation on the revised Regulations for licence applications, with implementation of the new rules in Spring 2019. However, Ofgem is yet to publish the results of the November consultation, so this timetable appears to be slipping.

“It’s right for consumers that Ofgem is starting to look at the financial strength of companies going forward, otherwise we’ll end up with more and more companies ceasing to trade and pushing more and more costs back on other companies who have been responsible,”

– Alistair Phillips-Davies Chief Executive, SSE

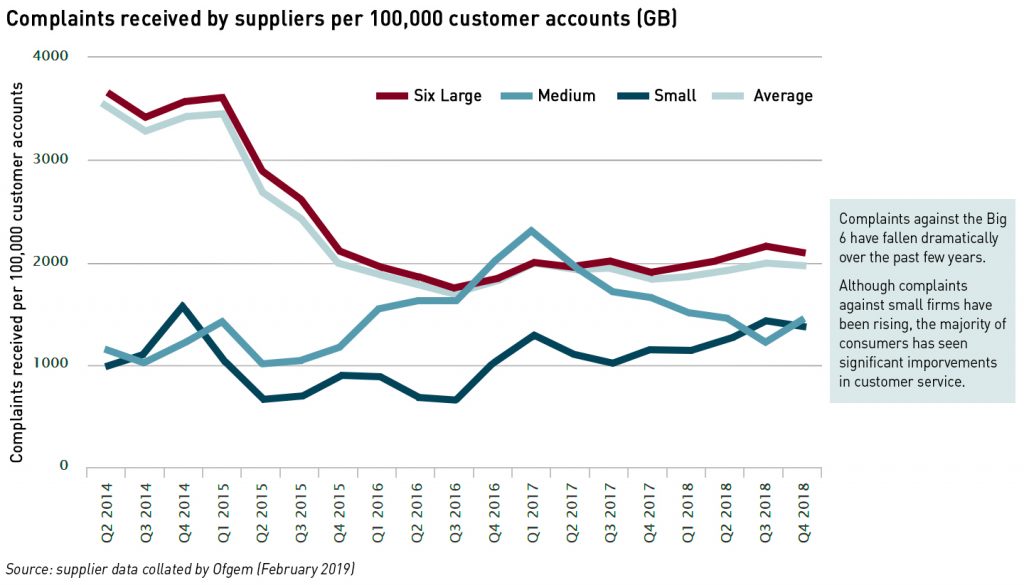

Some observers argue that focusing on the failures risks ignoring the benefits of increased competition in the retail energy market, with growing numbers of consumers switching suppliers and falling numbers of customer complaints about their suppliers.

The Government has launched the Future Energy Retail Market Review, which it claims will “identify ways to unlock additional benefits from the energy transition by enabling greater system efficiency, which will reduce consumer costs, support decarbonisation and improve security of supply”. The review will also ensure that appropriate protections are put in place for all consumers once the price cap expires in 2023.

In launching the review, the Government referred to Ofgem’s response to its Call for Evidence on Future Supply Market Arrangements in which suggested that fundamental reforms of the current retail market model may be needed:

“We consider that the current supplier hub model may not be fit for purpose for energy consumers over the longer term. Specifically, we are not confident it will enable consumers to benefit fully from the greater levels of innovation, digitalisation and competition made possible by the energy system transition.

We are also not convinced that the consumer protections framework in place under the current supplier hub model will be able to ensure existing and emerging risks are effectively managed into the future. Therefore, we have concluded there is a strong case for considering fundamental reforms to the supplier hub model, and for evaluating how alternative arrangements might operate in practice,”

– Ofgem

The Government and Ofgem expect to publish a consultation document on the potential options by this summer, and will take account of the review in the Energy White Paper that is due later this year.

Structural reforms probably necessary despite regulatory fatigue

The pace of regulatory change in the energy markets has been rapid over the past few years, but the process is of necessity iterative – implementing the regulatory framework for the target retail market design (if one could even be specified) would result in long delays in achieving political and regulatory goals.

The market changes that were triggered by climate legislation have been supplemented by technological advances and the emergence of new types of energy company – Shell, which entered the supply market last year with the acquisition of First Utility has announced its ambition to become the world’s largest power company, while other non-energy companies such as car-maker Volkswagen are establishing supply businesses. So far technology companies have remained on the sidelines, but there are obvious synergies between energy supply and connected homes full of networked appliances.

These companies may be able to extract value from the domestic supply market that traditional suppliers are struggling to realise, by leveraging technologies and business methods developed elsewhere. This trend could also help to solve the issue of dis-engaged consumers, many of whom would become indirectly engaged if their energy supply was embedded as part of another, higher value-added service as part of a connected home, or electric vehicle charging programme.

The regulatory framework needs to evolve in order to ensure businesses with innovative models do not face un-necessary barriers to entry, but without creating incentives to behave recklessly or engage in abusive market practices, particularly where energy supply is bundled with other products or services (for example in the way that Microsoft’s bundling of Internet Explorer with Windows was eventually deemed to be a monopolistic practice).

While the growing number of supplier failures may be seen as a sign of a functioning competitive market, care should be taken not to undermine either consumer confidence in the sector, particularly where consumers may have significant credit balances with failed suppliers, or investor confidence which can be deterred by an uncertain regulatory environment.

While the sheer number of significant regulatory reforms in the pipeline is undoubtedly challenging for all industry participants, the status quo is unsustainable for just about all stakeholders, meaning further reforms are both necessary and inevitable.

Leave A Comment