Last week saw the first T-1 capacity auction since the GB capacity market launched, clearing in the 14th round of bidding at £6 /kW/year. 10.7 GW of de-rated capacity entered the auction, with 5.8 GW of that being successful in securing contracts. Added to the 47.5 GW that was secured in the T-4 auctions this gives a total of 53.3 GW for 2018/19.

Existing generation dominated the auction, making up 4.7 GW of the total. 642 MW of new-build generation, 358 MW of unproven demand-side response (”DSR”), 85 MW of proven DSR and 4.7 MW of capacity to be refurbished made up the remainder. Unsuccessful bidders comprised 94 new-build generating plants, 26 existing generating plants, 68 unproven DSR facilities and 8 proven DSR facilities.

Gas is the dominant fuel while coal struggles

The auction cleared at £6 /kW/year, compared with £6.96 /kW/year in the early capacity auction last year. The Net Welfare Algorithm was used…a mechanism that is used to determine price and volume when the auction does not clear with an exact match of offered capacity and target capacity.

The algorithm subtracts the additional cost of procuring the marginal unit from the welfare gained by procuring that unit. If the result is positive i.e. the welfare is greater than the cost, the unit is included, and the clearing price is set to the exit bid price of that unit. The result of the Net Welfare Algorithm was positive and the marginal unit was procured.

The drop in prices has been attributed to an improvement in clean spark spread margins earned by gas generating plant, as well as an increase in demand response initiatives.

As a result, gas remains the dominant fuel-type in the capacity market securing over 75% of the capacity. CCGTs secured the largest share with 2.2 GW, followed by OCGTs with 1.7 GW. Coal and DSR we far behind with 7.57% and 7.45% respectively. Coal/biomass had received almost 20% of the available capacity in the T-4 auctions for 2018/19, while DSR only managed 0.4%, illustrating the progress made with DSR in recent years. Of the 16 DSR projects securing contracts, several had also been successful in the Enhanced Frequency Response tender in August 2016.

The declining competitiveness of coal has been reflected by a number of coal plant closures in recent years. Following last week’s auction, it was announced that Eggborough power station would be joining them in closing. Eggborough holds a capacity market contract for the current year, and will honour that commitment, but according to the owners, after September 2018 it will no longer be economically viable. In all, 2.8 GW of coal plant exited the auction, including Drax Unit 4 as well as Eggborough.

The government has already signalled its intention to remove coal from the generating mix by October 2025, however this news adds to speculation that the last coal plant will have closed well before that date. Commenting on the auction results Jonathan Marshall, energy analyst at the Energy and Climate Intelligence Unit, said

“It is yet another sign that old and polluting technology is losing out to demand side response and distributed capacity, at the same time as the capacity market clears at a record low price to ensure security of supply at low cost for homes and businesses. Coal-fired generation in the UK is in freefall, and more plant closures – as expected by the government – will see this continue.”

The closure of Eggborough will leave just seven coal-fired power stations in the market: Drax, Cottam, West Burton, Fiddlers Ferry, Aberthaw, Uskmouth, and Ratcliffe-on-Soar. The T-4 auctions due this week will give a stronger indication of the viability of coal over the longer term, however not all analysts agree that coal is set for an early exit.

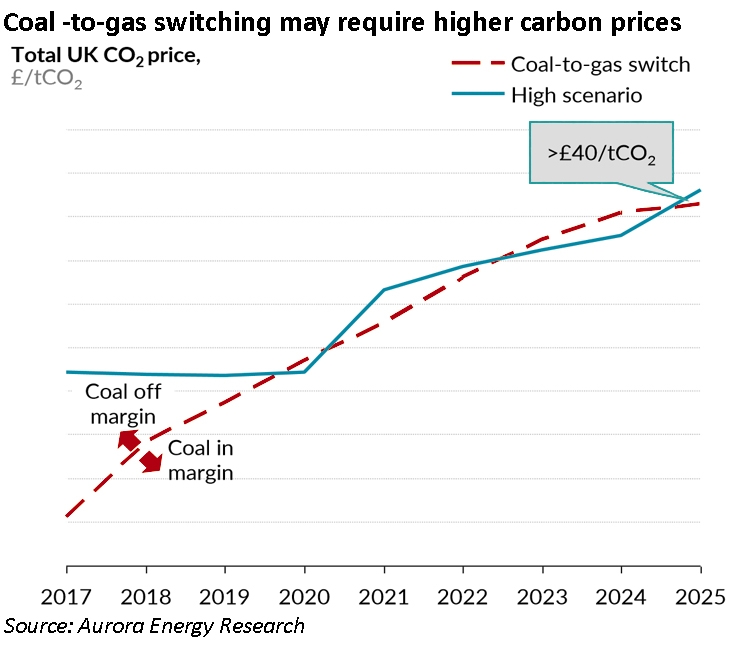

Analysis by Aurora Energy Research published last October suggests that the carbon price floor (“CPF”) would need to rise to at least £40 /tonne to secure the exit of coal by 2025, on the basis that after 2020 global gas prices will rise as the current over-supply re-balances, and the removal of China’s coal production restrictions will see coal prices fall.

The same report points out that increasing the CPF to £40 /tonne would add £0.9 billion to electricity bills, while removing it altogether from 2020/21 would lower energy costs by £2.6 billion.

Despite the lower auction price, the result is more pain for consumers

Energy and Climate Change Minister Claire Perry said in a statement:

“With the government’s intelligent intervention through the Capacity Market, we have achieved an even higher standard of energy security for next winter and at a low cost for bill payers.”

2018/19 will be the first delivery year for which the capacity market has been fully up and running. Following last week’s auction, it is now possible to quantify the cost of securing supplies next winter:

- T-4 auction: 47.528 GW @ £19.40 /kW/year = £376.36 million

- T-1 auction: 5.773 GW @ £6.00 /kW/year = £34.64 million

- Total = £411.00 million

This compares with the final year of the Supplemental Balancing Reserve (2016/17) which cost £121.50 million for 3.5 GW of backup capacity. The higher costs reflect the fact that the capacity market rewards all capacity for being available, rather than targeting the incentives at plant that would otherwise close or not be built.

Far from being a “low-cost” action, the cost of securing supplies for next winter is almost 3.5 times higher than the scheme it replaced. Consumers will be in for a shock next winter when these costs start to hit their bills.

Leave A Comment