Over the past few days forecasters have been warning of a cold snap, with particularly cold weather hitting the north of the UK, which began on Tuesday – as I began writing this post at lunchtime on Tuesday 7 March there had been some light snow in London and it felt very cold. As is often the case, cold weather translated into still weather, significantly lowering wind generation, particularly in Scotland, although not to the degree seen in the summer.

On Monday evening, National Grid ESO issued its first Electricity Market Notice (“EMN”) in a couple of years – these are a more serous sign of system tightness than the Capacity Market Notice (“CMN”) since they involve an assessment by control room staff whereas the CMN is automatic and can often be easily rectified by a few simple actions in the Balancing Mechanism (“BM”).

The first EMN was issued at 22:05 on Monday 6 March covering the period from 16:30 to 20:30 on Tuesday 7 March citing a shortfall of 980 MW:

An ELECTRICITY MARGIN NOTICE has been issued by the System Operator to encourage market actions to increase System Margins. For the period: from 16:30 hrs to 20:30 hrs on Tuesday 07/03/2023 There is a reduced system margin. System margin shortfall 980 MW The current contingency requirement is 700 MW. 0 MW of generation is excluded from the available system margin due to system constraints. Maximum Generation Service may be instructed. Trading Points, Control Points and Externally interconnected System Operators are requested to notify National Grid of any additional MW capacity. Suppliers please advise National Grid of any additional Demand Control available…

An ELECTRICITY MARGIN NOTICE is used to send a signal to the electricity market. It highlights that, in the short-term, we would like a greater safety cushion (margin) between power demand and available supply. It does not signal that blackouts are imminent or that there is not enough generation to meet current demand.

The EMN was re-issued at 12:24 on 7 March citing a shortfall of 700 MW for the same period with a current contingency requirement of 370 MW. In other words, since the initial EMN, there had been a small reduction in the shortfall but the market had not responded to the degree needed to ensure an adequate margin. It was expected that interconnectors would be needed to meet demand, but there were some doubts about the French links due to extensive strikes in France – including nuclear plant technicians – and as of lunchtime, GB was net exporting to France.

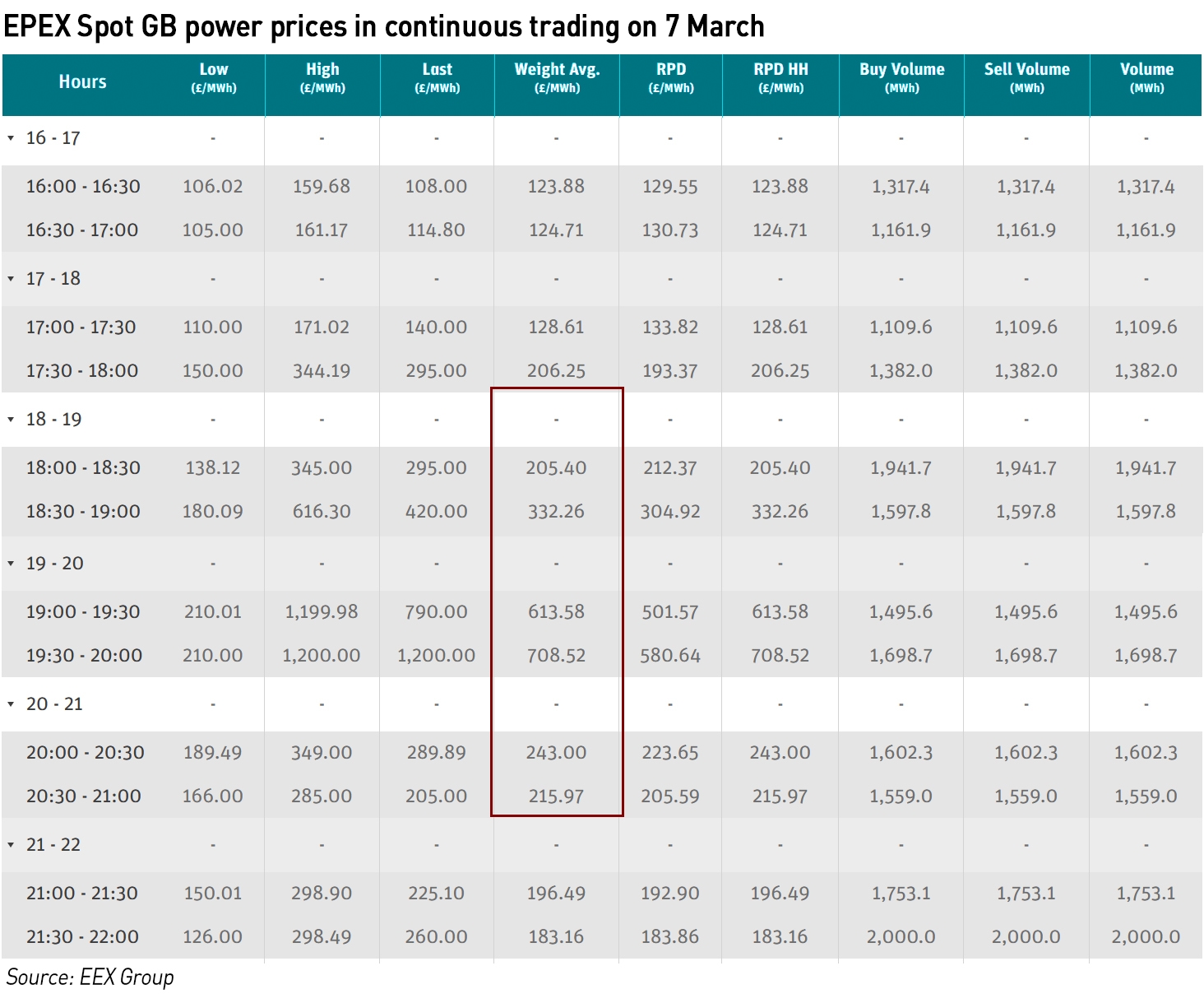

What is interesting is that none of this was reflected in forward prices which did not react in any particular way. Both day ahead and within day prices were in line with normal trading in almost all settlement periods, and prices in the Balancing Mechanism remained normal until late afternoon when we started to see prices first reaching £500 /MWh and then later £750 /MWh (Rocksavage). The cashout price also jumped late afternoon reaching £725 /MWh in SP35 (17:30). The lack of a response in the traded markets may explain the muted reaction from interconnectors.

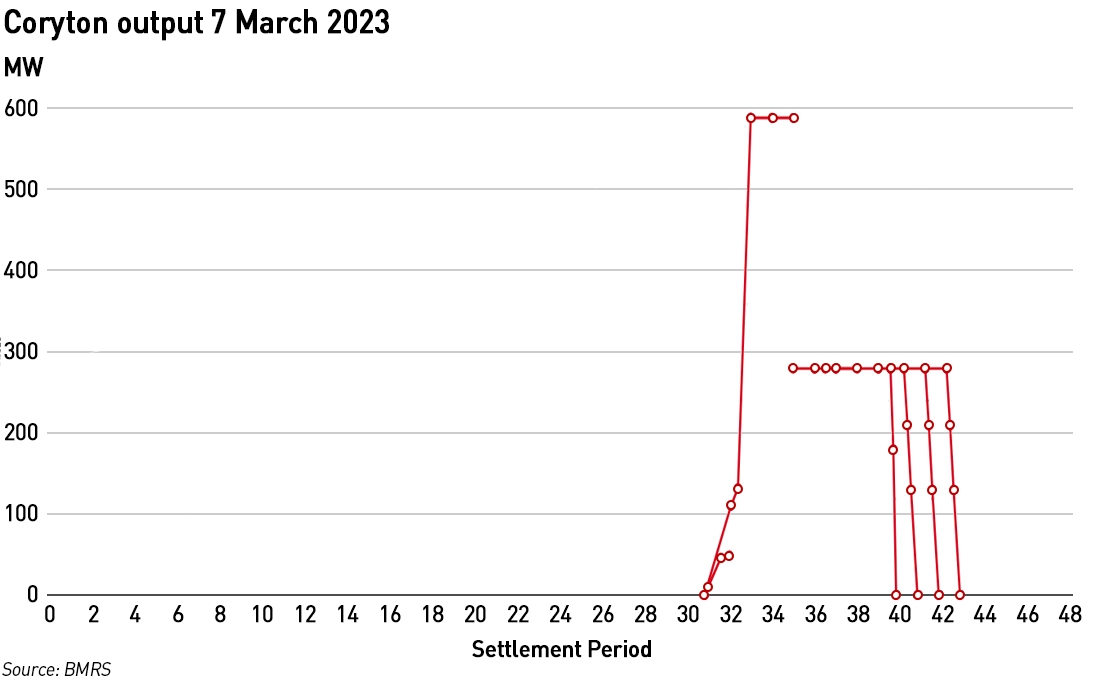

The cashout price peaked at £1,950 /MWh at 18:00 and Balancing Mechanism prices rose to the same level with Coryton CCGT getting accepted at £1,950 /MWh in the same settlement period. Coryton had kept itself out of the market during the day, likely in anticipation of high BM prices, a good strategy given the lack of price response in the forward markets to the expected tightness this evening. Connahs Quay 2 was accepted at £999 /MWh for SP36 and £1,845 /MWh in SP37, having also been held out of the market until the BM.

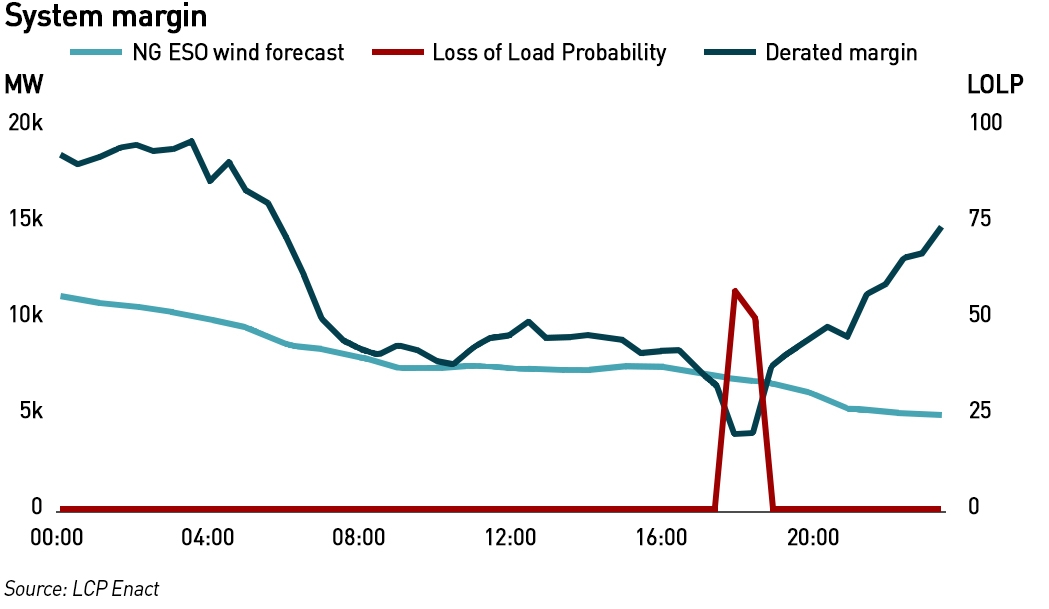

Just after 1pm on 7 March, there was a Loss of Load Probability of 56% forecast for 18:00 that evening. Forecasts from Amira Technologies indicated that 8 March would be even tighter – wind forecasts in Scotland were lower although they were higher for England, with overall wind output expected to be higher.

NG ESO put its coal contingency on standby but did not activate the Demand Flexibility Service (“DFS”), noting that it might be needed for the following day. So far this winter, the two have gone hand in hand, with the coal units being stood down after warming, but on Tuesday the DFS was not activated so additional support could only come from the coal units. As I have noted previously, warming the coal units has both a financial and environmental cost – coal is burned to do the warming – so warming them and not using them is quite wasteful. Certainly, I believe that the financial cost of warming the coal units and then running the DFS instead is economically inefficient.

Another interesting factor with the coal contingency is that both units at Drax and both units at West Burton A were warmed but not Ratcliffe. EDF has previously indicated that it would only make one unit available at a time. Ratcliffe appears to have been available, and other units at the plant were running in normal market operations. The two units at West Burton synchronised to the grid at around 3pm with instructions to run until 7pm, later extended to 8:30pm for unit 1 and 8:45pm for unit 2. They ran throughout this period with stable output which is a testament to the hard work EDF has put in to keep these old units serviceable this winter.

“The grid has shown incredible initiative by moving on demand flexibility so quickly. But its commitment to keeping one foot in the past and sticking with the same polluting coal power plants that we have had for decades is sending mixed signals,”

– Alex Schoch, head of flexibility at Octopus Energy

The use of the coal contingency was criticised but the requirement to activate the DFS at the day ahead does restrict its usefulness. It’s unclear why NG ESO opted not to activate the DFS, perhaps the signs of market tightness did not emerge until later in the evening on 6 March, after the cut-off time – certainly the EMN did not come until just after 10pm. In any case, despite the fact that this was the first use of the coal contingency this winter, coal has made an important contribution, with Ratcliffe seeing high utilisation rates.

At around 15:30 on Tuesday the EMN was cancelled as was the DFS alert for 8 March since the wind forecasts for the 8th had picked up. The French interconnectors were still exporting to France at that point. By the evening, just before 6pm, the French interconnectors were at neutral, not flowing in either direction, and the LOLP was showing at just 1%. The French interconnectors did later switch to imports from about 7:30pm.

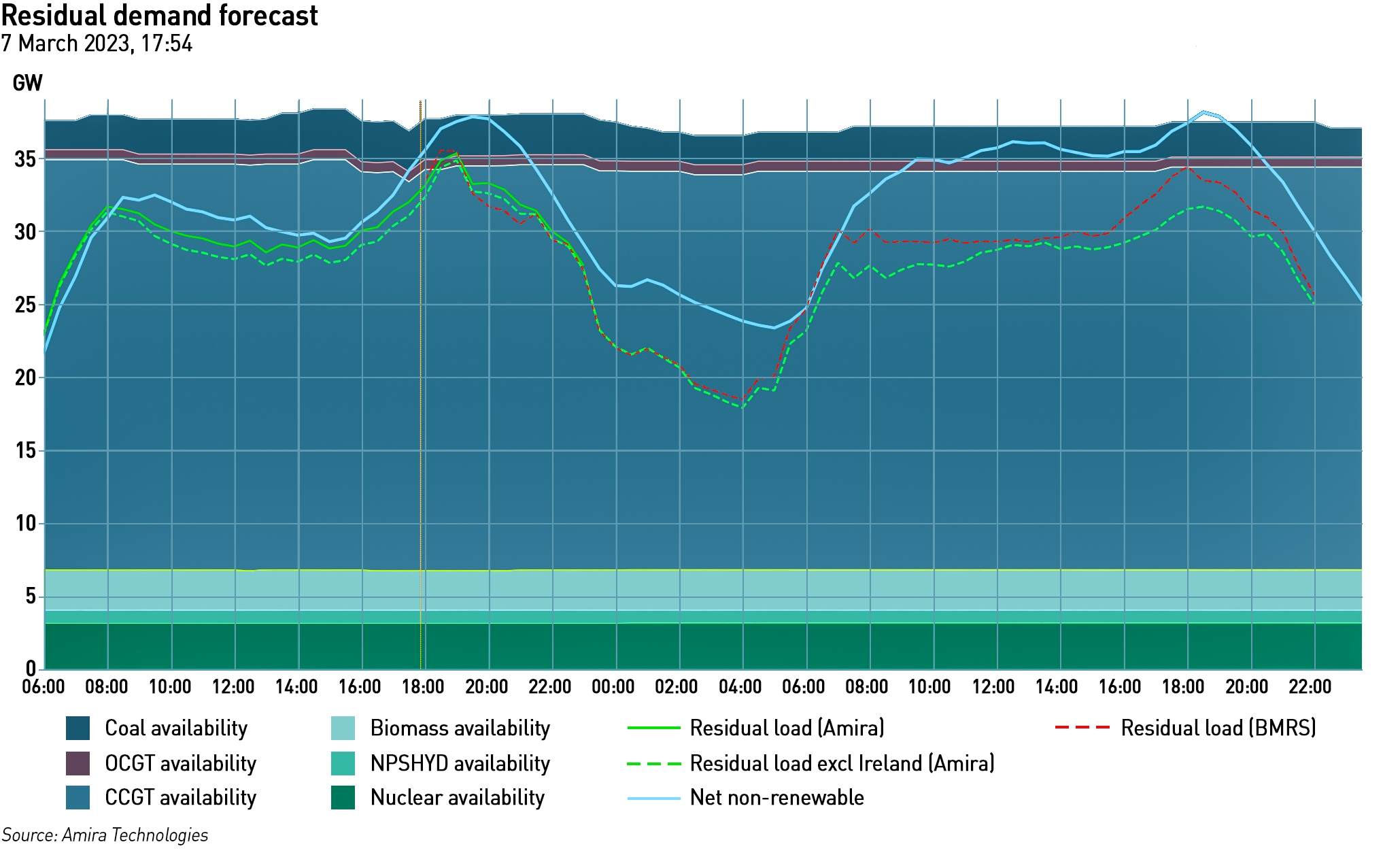

Wind output declined through the day on 7 March beginning the day at around 8 GW and dropping to below 700 MW at around 10pm, picking up to about 6 GW during the following day before declining again through the night of 8-9 March. By the early hours of 9 March all interconnectors with the Continent were importing at the max, and there were no exports to Ireland.

All in all I think 7 March was the tightest day so far this winter, with the EMN reflecting genuine market tightness. What’s interesting is the under-reaction of the traded markets – typically traders over-react to news so this under-reaction is interesting and was un-helpful when it came to delivering the necessary market signals to secure imports. If any readers have any insights about this please do share them in the comments.

It was my understanding that NG ESO’s strategy to get through this winter was to use DFS in preference to running the coal contingency units. I believe this has been stated as such in the NG ESO Operational Transparency Forum.

Recently there was an article (Times ?) which raised the possibility that NG ESO were going to lose large sums of money on the coal stocks they have bought at West Burton and Drax.

It always struck me that NG ESO’s strategy in terms of buying coal stock was extremely naive. The coal handing plant at power stations is usually designed to be one way. It is not normally capable of putting the coal back off stock back onto trains, meaning it will be expensive to transport it if you sell it. I also believe that if you sell it / move it to another site, you end up having to pay the Carbon Floor tax on it a second time. This is the reason the likes of Fiddlers Ferry chose to use up their coal stocks at a loss / low electricity prices.

I wonder if the penny has dropped with NG ESO and they have realised that having bought the coal, it makes more sense to use it rather than buying electricity at high prices via interconnectors or using DFS ?

I don’t believe that the latest 2035 electricity decarbonisation plan includes “security of supply”. The phrase was used 7 times in the original BEIS written “Net Zero Strategy” but not once in the more recent BEIS written “Mission Zero”, which also dropped “abundant, cheap, British Renewables” and replaced with “behaviour change”.

The recent NAO report on the 2035 decarbonisation said that the government has no clear delivery plan or costing and I cannot see any evidence for long-term grid scale backup in either the “Mission Zero” or the latest NG ESO FES’s 2035 or 2050 energy flow diagrams.

I see that the results of the first round REMA consultation are out.

https://www.current-news.co.uk/rema-consultation-summary-the-uks-first-step-to-electricity-market-reform/

It seems more disagreement than agreement on the future, but also a clear lining up of vested interests. Wind is obviously against locational marginal pricing that would see its income heavily eroded, and likewise against equivalent firm power because it would limit its expansion. Consumers are hopelessly under represented in all this. The industry letter the other day begging Shapps to grant even greater dictatorial powers to OFGEM to ram through net zero plans over the heads of consumers is where we are at.

Someone needs to turn over the stones and shine a torch on the cockroaches.

Could the answer to your question be down to the ongoing conceptual battle between power and energy.

Power companies have become energy companies. The post war minister of power has become the energy minister. The terms have become interchangeable even though their meaning in everyday language is clear and distinct. “The power of an elderly and infirm dictator” “The energy of young healthy children”.

The electricity energy market balances estimated energy supply and energy demand over a period of time but the NGESO control room has to balance actual spot power demand at every instant in time.

Electrical power system modelling has become, for whatever reason, predominantly energy modelling. In the extreme they balance energy over a year. ( In setting policy the Welsh Government uses this method ). Some balance energy over a day or a part of a day but even this is inadequate and misleading. Unfortunately the NGESO Future Energy Scenarios fall into this trap and produce results that despite ambitious creative thinking produce results that are totally non viable.

The only valid way to test the operability of future plans is to look at the spot power boundary conditions. This is a simple task that does not require energy modelling. You look at the highest and lowest customer demand requirements coupled with the highest and lowest generation outputs.

In the fantasy world of energy balancing everything on average is fine but in the real world of the control room the actual feast and famine of power production somehow has to be resolved.

So the CCGT capacity was there, the operators were just choosing to price-gouge (again). Looks to me like NGESO lit up the coal to minimise their revenue.

DFS can’t supply much of a demand reduction beyond an hour so it wasn’t much use on the 7th.