2017 could see further interesting and potentially dramatic changes to the UK energy market. In this post I explore some of the key themes for the coming year.

# Creation of an Independent System Operator

Throughout 2016 pressure was growing for the UK to explore adopting an independent system operator model, with a report from the House of Commons Energy and Climate Change Committee calling for the government to put in place plans for a fully independent system operator as soon as possible in order to manage the risks of conflicts of interests. National Grid continues to speak out against such a change (repeated this week by CEO John Pettigrew in an interview with Network), and is reportedly strengthening its internal governance to address the concerns raised.

Ofgem has announced that it will soon be consulting on system operator incentives, with a view to applying any changes from April 2018. It will be interesting to see how the role and nature of the SO will feature in this consultation or whether National Grid has managed to neutralise the concerns around its role.

# What next for the Capacity Market

The first capacity auctions were dominated by existing plant, with small – often diesel-fuelled – peakers being disproportionally successful. The auctions failed to deliver the new large CCGTs desired by the government (only one such plant won a capacity contract in the first auction, but has since surrendered it having failed to secure financing for the project), so various changes have been made to the market structure with a view to changing the mix of successful plant.

The most recent auction in December saw a slightly higher clearing price and a small amount of new gas plant being committed, but still significantly short of the government’s ambitions. There are also questions about whether the focus on capacity alone is appropriate given the importance of flexibility in an increasingly intermittent generation landscape.

It is likely that changes to embedded benefits and emissions regulations will make small peakers less attractive, and there may well be further changes to the capacity market rules in order to achieve the government’s objectives. It will also be interesting to what happens in the T-1 auction for 2017/18 due on 31 January.

# New rules for Battery Storage

Battery storage sites won over 500 MW capacity on December’s capacity auction, including some projects that were unsuccessful in the earlier EFR auction. However, prior to the auction concerns were raised about the suitability of batteries to provide capacity, where in some cases they can only discharge over a 30-minute period. Since the auction, further concerns have been raised relating to the de-rating factors applied to batteries, with Aurora Energy Research claiming they are unreasonably high given observed reliability.

Despite these successes, battery storage providers have argued that existing market frameworks pose a number of disadvantages, in particular double charging of climate levies and system use fees which are applied both when the battery charges and discharges. A recent report from the Policy Exchange recommends updating the Electricity Act 1989 and other regulations in order to properly accommodate both battery storage and DSR.

Despite these successes, battery storage providers have argued that existing market frameworks pose a number of disadvantages, in particular double charging of climate levies and system use fees which are applied both when the battery charges and discharges. A recent report from the Policy Exchange recommends updating the Electricity Act 1989 and other regulations in order to properly accommodate both battery storage and DSR.

The Energy and Climate Change Committee report, The energy revolution and future challenges for UK energy and climate change policy also recommended amending the Capacity Market rules in relation to storage, considering increasing the contract length and addressing restrictions around the stacking of revenues for storage projects.

# Curtailment of Embedded Benefits

In December, Ofgem published an open letter outlining its intention to amend transmission network charging arrangements for embedded generators and setting a timetable of early 2017 for issuing draft code modifications ahead of planned implementation by April 2018. Both Ofgem and the government believe the Transmission Network Use of System (TNUoS) demand residual payment, known as the “Triad” payment, is too high – it currently stands at around £45/kW, and is forecast to increase to £72/kW by 2020. This payment forms a significant part of the income available to embedded generators, and allows them to undercut large new generators in the capacity auctions.

The proposals will be viewed with interest as there is some speculation that embedded generators may find it is more economic to renege on capacity contracts than to continue to operate if their economics change significantly. This could lead to capacity shortfalls.

There is also a view that the changes currently proposed by Ofgem are rather piecemeal in nature and a more radical overhaul of network charging is needed.

# Nuclear power developments

This week has seen the formal launch of the Generic Design Assessment of the UK HPR1000 reactor – the reactor planned for Bradwell B in Essex, being developed by China General Nuclear Power Corporation (CGN) and EDF.

The GDA process will take years rather than months and it will be interesting to see in the meantime how the pressure-vessel forging issues uncovered by the French nuclear regulator will impact UK projects. The ASN is due to rule on the safety of the Flamanville reactor by the end of June, and will need to decide whether to require EDF to replace the pressure vessel, which would push its completion date beyond the 2020 deadline for the UK Government’s support for Hinkley Point C.

# Investment landscape

According to the Green Alliance, investment in wind, solar, biomass power and waste-to-energy projects will decline by 95% between 2017 and 2020 in the face of subsidy cuts, so investors will be looking for other types of projects to support.

There are some positive signs for tidal energy – despite the failure (financial and technological) of Tidal Energy last year the MeyGen project in Scotland has just received €20 million of funding from the European Commission. There are also reports that the government will announce its support for the Swansea Bay tidal lagoon, when it publishes its review into the feasibility of the technology this month. A group of manufacturing executives has written to the Financial Times with their support for tidal power in the UK, claiming it could become a “major pillar of the UK energy mix”.

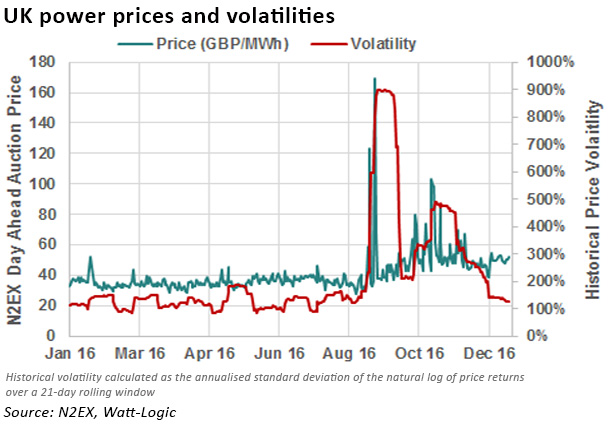

# Prices and Volatility

November 16 saw the collapse of GB Energy in the face of higher wholesale prices (and a lack of a hedging programme). The second half of last year saw an increase both in prices and in volatility, and while both have retreated to a certain extent recently, levels are higher than they were before the increase.

With the growth of intermittent generation and the closure of significant amounts of baseload plant, increasing price volatility can be expected to persist. This may have a particular impact on smaller market participants, who will face increased hedging costs as a result, potentially changing the competitive dynamics of the market, particularly in the retail segment.

Other relevant areas to watch

I have not included Brexit in my list of key themes for 2017 as I don’t believe this is going to be a 2017 issue for the UK power market. Assuming Article 50 is triggered at the end of March, there will be a further two years before the UK actually leaves the EU, and therefore the lead times for any Brexit-related energy market impacts will be longer. Although Brexit provides the government with a number of policy alternatives, in the absence of state aid restrictions for example, it remains to be seen how far the government will want to go in the early stages when set against other Brexit priorities.

Another area that could promote major disruption to the sector but not necessarily in 2017 is the development of the Internet of Things. For the benefits of smart meter programmes to be realised, consumers need to have greater control over consumption (in addition to suitably granular time-of-use pricing). As the IoT develops, consumer control over consumption will increase, with the ability to vary the timing and level of power draw on a wide range of devices. The entrance of large technology companies such as Google or Apple would be a natural step and could well dislodge existing home energy platforms developed by the utilities, since the service is more aligned with the technical capabilities of IT companies than energy providers.

Whatever 2017 brings to the UK energy market, I’m confident in predicting further surprises and plenty to keep us on our toes!

Leave A Comment