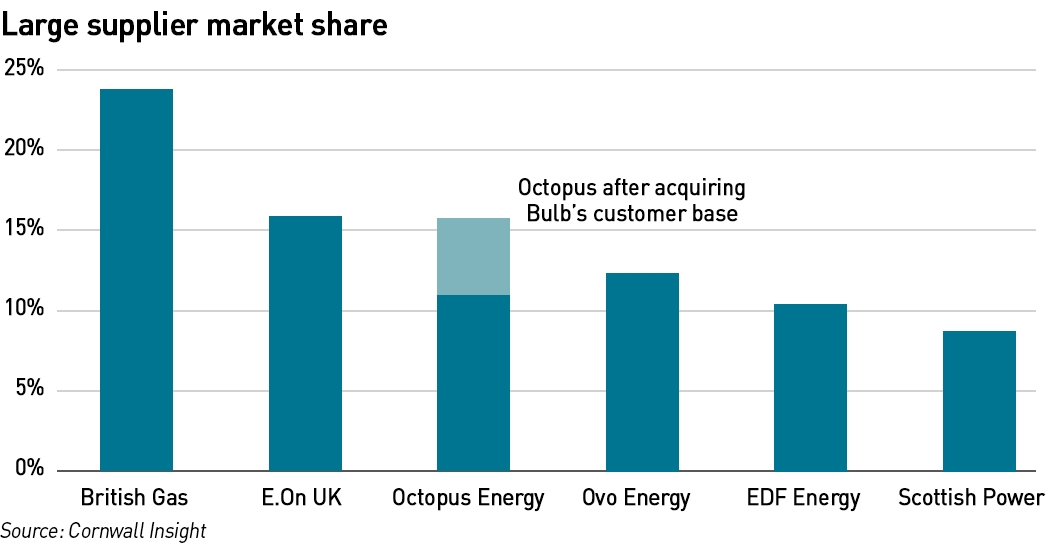

Over the weekend, the Government announced that failed supplier Bulb which entered Special Administration back in November last year, is to be acquired by rival Octopus Energy. Although the sale process was described as “competitive” it is widely believed that there only ever was one serious potential buyer, so it is hardly a surprise it “won”. The move is likely to see Octopus overtake Ovo as the third largest supplier in the GB market behind Centrica (British Gas) and E.On (Ovo had also flirted with buying Bulb, but it’s unclear how serious its approaches were).

Bulb has around 1.5 million customers and 650 staff, and was the country’s seventh largest supplier at the time of its collapse. The sale will be completed following a statutory process known as an Energy Transfer Scheme (“ETS”), which will transfer the relevant assets of Bulb into a new entity (Bulb UK Operations Limited). This entity will then be sold to Octopus but will remain ring-fenced from the rest of the Octopus business for a defined period. The process is subject to approval by the Business Secretary following consultation with Ofgem (which was granted on 31 October), and the acquisition close at a time ordered by the High Court – the order is be expected to be made by the 11 November to take effect on 17 November.

“I have therefore approved the Octopus bid transaction and associated amendments to the existing funding facility and establishment of their new loan facility. The BEIS-led consultation process on the energy transfer scheme (ETS) has commenced. Subject to Government approval, the energy administrators will arrange for a court hearing date for commencement of the ETS and to enable the completion of the transaction as all agreements take effect by mid-November,”

– Grant Shapps, Secretary of State for Business, Energy & Industrial Strategy

The Government will provide financial support to the new entity for the procurement of gas and electricity for Bulb customers for Winter 2022, which will be repaid by the new entity in line with an agreed repayment schedule. A profit-sharing agreement will be implemented for the ring-fenced business until the agreed funding is repaid by Octopus – payments to shareholders or the wider Octopus group from the ring-fenced entity will be restricted until the repayments are completed.

The Government has committed to providing the remaining funding necessary to ensure the special administration is wound up in a way that protects customers’ supply – under current regulations the costs of Special Administration are recovered through future bills rather than from the taxpayer, although it is unclear how this will be achieved against a backdrop of high and subsidised retail energy prices. Although the Government maintains that the Bulb bailout will not cost the taxpayer money, the reality is that bill-payers and tax-payers are largely overlapping groups, and bills are already being inflated by the costs of all of the other supplier failures in the past year and a half. These costs add to the affordability challenges in the market, and as half of them are being recovered through standing charges, they also make it harder for consumers to cut their bills through reductions in energy use.

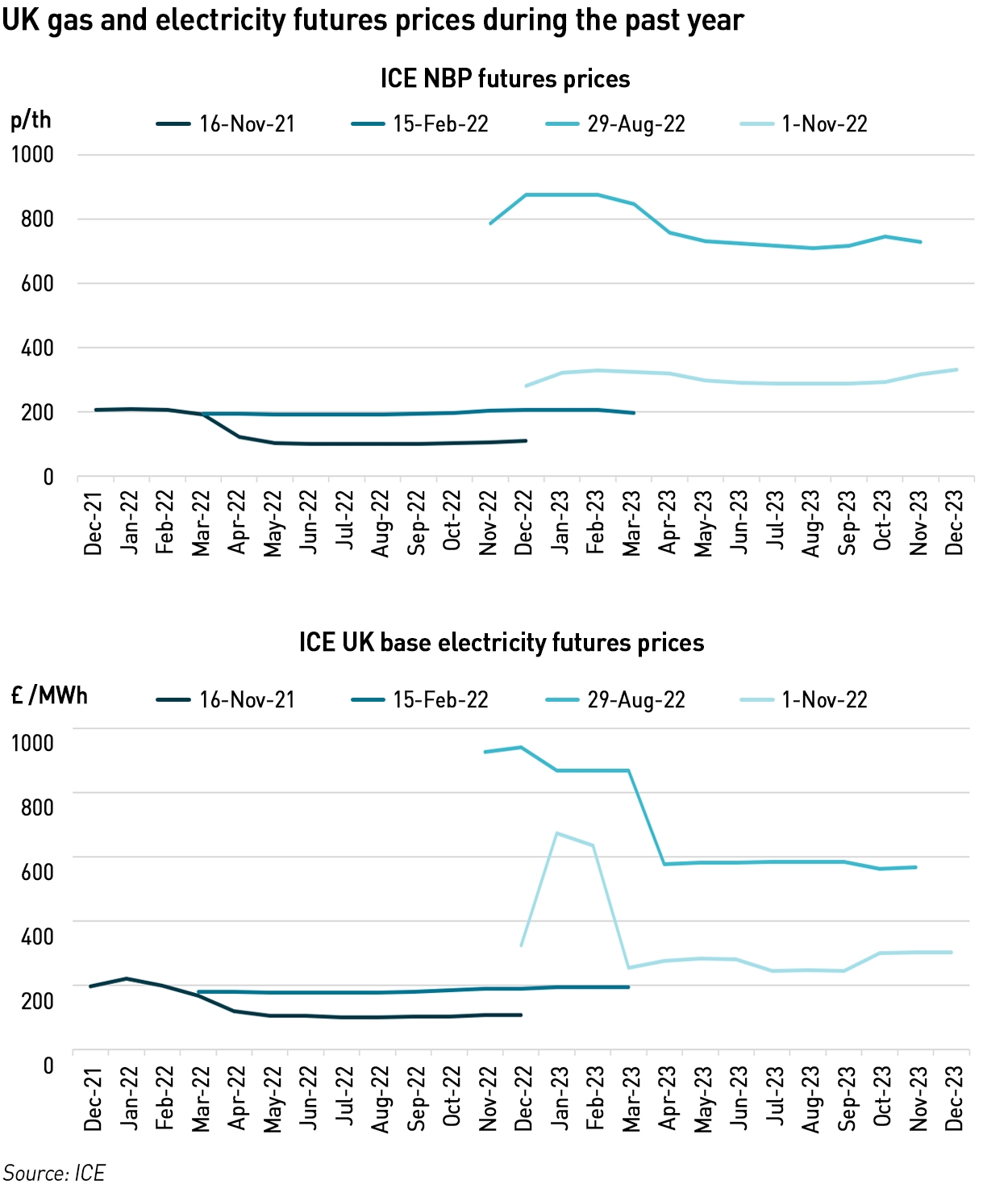

The price paid by Octopus has not been made public although it is described as “above market value”…quite what that means is unclear, but it is thought that the costs of the Special Administration will exceed £4 billion by the time it is completed. There has been significant controversy around the question of hedging Bulb’s wholesale price exposures, with then Business Secretary Kwasi Kwarteng telling the BEIS Select Committee that hedging was “risky”. In fact, he also explained that the Government looks at its market exposures in the round, and having a long gas position through North Sea taxes and royalties may have meant that separately hedging Bulb’s energy purchases did not make sense – except that Bulb has been treated as a ring-fenced entity, and so was not able to benefit from the Treasury’s wider long gas position.

“The Government’s bailout of Bulb Energy incurs a £1.2 billion cost in 2021-22 and a further £1.0 billion in 2022-23, to cover the company’s operating losses. Given the volatility in global energy markets, there remains uncertainty around the final cost,”

– Office for Budget Responsibility, Economic and Fiscal Outlook, March 2022

Bulb is believed to be un-hedged, meaning it is purchasing gas and electricity for its customers close to the time of delivery. Assuming it is buying on a month-ahead basis (and did so for October and November), its procurement costs for this winter will be in the region of £2.5 billion (ignoring the costs of shaping). This is lower than it would have been in late August when gas prices peaked – then it would have cost £3.7 billion, but had the hedging taken place last November when Bulb first went into Special Administration, the costs would likely have been under £1 billion for Winter 22 (this is a bit of an estimate since at that stage the end of Winter 22 would not have been very liquid, so hedging the months would not have been a particularly good strategy). In any case, ignoring other factors, not having procured on a forward basis at the time it entered Special Administration will likely cost consumers (or potentially taxpayers) over £1.5 billion for Winter 22 alone. That is ignoring the additional costs of being un-hedged in the intervening months.

While I sympathise with the argument that the Government should manage its risks globally, I do not think this should have been applied to Bulb since the intention was always to sell the business and therefore it was treated on a standalone basis. The costs of the Special Administration have not been off-set by any value from the Treasury’s North Sea income, which greatly inflates the costs that will be faced by the public.

While there is some argument that those North Sea receipts are in part funding the Energy Price Guarantee, this benefit would be received in any case. There is really no justification for not having locked in Bulb’s procurement costs a year ago when prices were very much lower. While at the time, prices were high on a historic basis due to the effects of covid, they were expected to settle sometime in the second half of 2022. The subsequent invasion of Ukraine in late February should have signalled further price increases were likely – not having hedged in the hope prices would fall is to speculate, and in this case, it was a bet that went disastrously wrong.

In any event, the sale of Bulb should now put a limit on the costs faced by the public, and that can only be good news.

I listened to Rees Mogg defending his actions on the energy price guarantee. Whilst he didn’t really mount a completely successful defence he did admit that in large measure failed government energy policy lies behind the crisis, and that in reality government will have to continue with large elements of bailout until the crisis is over: Hunt’s cancellation of future support beyond April is not credible, even though it should be better targetted in future. So I think that only part of the liability has been shifted. The price guarantee offers no incentive in the short term for hedging, because it provides the hedge.. In any event the capacity of the market to provide hedges remains extremely limited, and the process can be the punishment with heavy collateral demands especially against hedges made at disadvantageous forward prices. It will be the losses on hedges taken out during the summer price spike that will prove most expensive for the government cap scheme.